Hormuz Standoff Hands the Dollar a Weekly Gain

7 min read

Share

A mixed retail sales beat couldn't save the sterling. Weak PMIs weighed on the euro. With Hormuz still shut and oil above $100, the dollar took the week, with its first weekly gain in three weeks; five central banks take the stage next week.

GBP: Retail Strength Meets Oil Shock Pressure

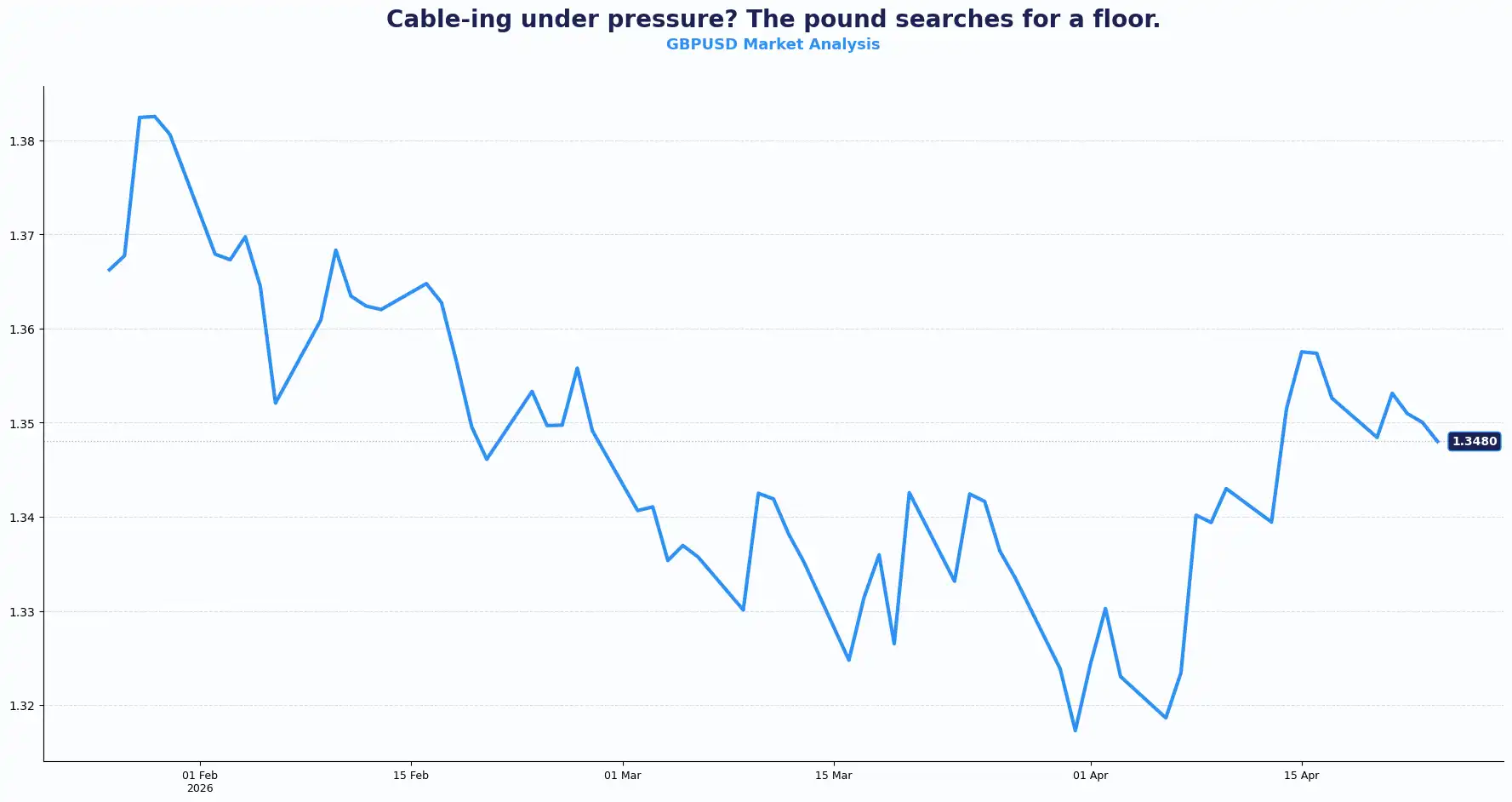

GBPUSD: 1.3462 | EURGBP 0.8675

Cable trades at 1.3462. That puts it back at late-February levels and on course for a weekly decline of 0.4%.

UK Retail Sales data painted a mixed picture; while the headline figure grew 0.7% MoM, the underlying sentiment feels fragile. The headline figures beat the 0.2% consensus, reversing February's 0.6% contraction. Year-on-year, sales rose 1.7% against a 1.3% forecast. The ex-fuel reading came in at 0.2% MoM, in line with expectations, while the annual figure was 1.7%, just below the 2.0% consensus.

The headline beat suggests UK consumers fared better than expected in March. Retail sales, a key ONS gauge, would typically support sterling on a strong reading. However, the cautious ex-fuel result tempers any positive outlook for GBP.

The pound has not rallied because the macro backdrop now favours the dollar. Safe-haven flows have boosted the dollar as the Middle East standoff intensifies. Iran's footage of commandos boarding a cargo vessel in the Strait of Hormuz has shut down hopes for a near-term reopening of this critical shipping lane.

Brent Crude closed above $105 on Thursday and hovered near $100 Friday morning. With the Strait effectively closed, energy costs show no sign of retreating, which could impact the Bank of England's (BoE) calculus.

UK business surveys published this week reinforced the mounting pressure. S&P Global's April Flash UK Composite PMI recorded the biggest single-month jump in input prices in the survey's 28-year history, reaching its highest level since the double-digit inflation episode of late 2022. The Confederation of British Industry's manufacturing confidence gauge fell to its most pessimistic reading since the start of the COVID-19 pandemic. Firms' expected selling price gauge surged to +32 from +12 in March, the largest monthly jump since records began in 1975.

Money markets now price a 75% probability of a BoE rate hike by June, up from a 50/50 call at the start of the week. The BoE announces its policy decision next Thursday. With energy costs still climbing and cost surveys at historic extremes, policymakers face a genuine dilemma: move on inflation, or hold given the demand destruction that elevated energy prices are already inflicting. Britain's budget deficit for the last financial year narrowed to a six-year low as a percentage of GDP (one marginally supportive data point in an otherwise complicated picture.

Against the euro, sterling strengthened. EUR/GBP dipped to 0.8659 intraday before settling around 0.8675, as the euro carried its own weight of weakness into the end of the week.

Sterling holds a modest data tailwind from retail sales. Investors are looking forward to the BoE decision next Thursday; the gap between the probability of a 75% rate hike and any signal of a pause is where volatility is likely to sit, potentially impacting sterling's near-term direction.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3500, 1.3570 and Support sits at 1.3400, 1.3320

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700, 0.8750 and Support sits at 0.8600, 0.8550

EUR: Euro Wilts as Risk Aversion Dominates

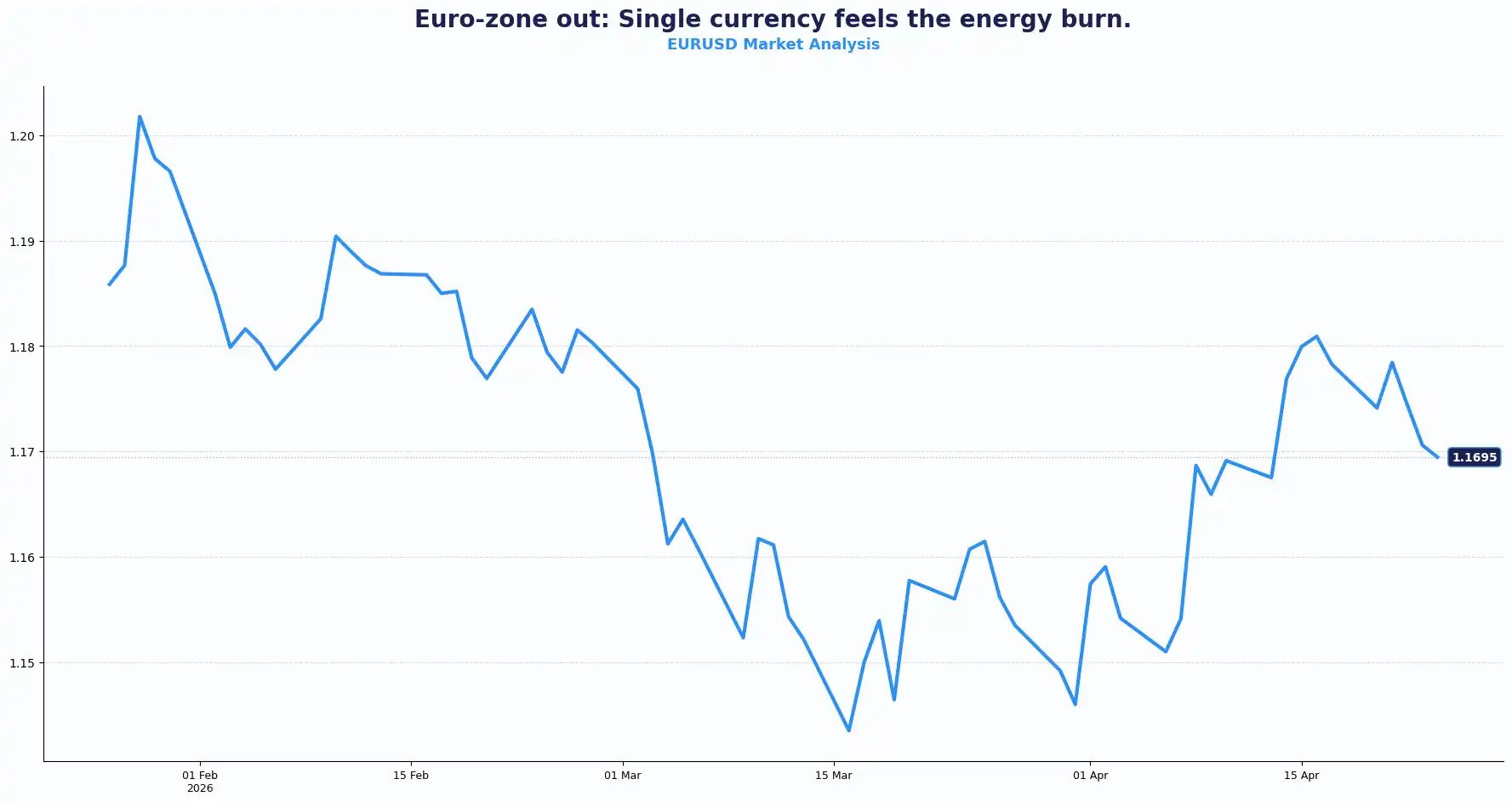

EURUSD: 1.1679

Euro trades at $1.1679, on course to lose 0.7% for the week.

Recent Eurozone PMI data paints a bleak picture. The composite reading fell to 48.6. This miss against the 50.2 consensus signals contraction. Manufacturing holds some ground at 52.2, but services slumped to 47.4. With services - the larger component in contraction, the overall picture is one of an economy losing momentum precisely as energy costs climb. Investors now look toward the German IFO Business Climate index for signs. This index surveys 7,000 businesses and serves as the primary health check for the bloc’s largest economy.

The European Central Bank (ECB) is expected to hold its deposit rate on 30 April and move toward a hike in June. The ECB's deposit facility rate decision is scheduled for Thursday next week, alongside the BoE's. With the Eurozone now showing composite activity below the 50 expansion threshold, the ECB faces a version of the same dilemma as the BoE: whether to tighten policy to address an energy-driven inflation surge or hold rates unchanged given the growth risk.

The dollar's position reinforces pressure on the euro, as the US economy is widely viewed as better placed to absorb the current shock than the Eurozone, and that differential is reflected in EUR/USD's weekly decline.

With the euro dipping to 86.59 pence against the pound, it signals that the euro is underperforming even a pound that is itself under pressure. Against a strengthening dollar, the euro's room to recover is limited until the macro backdrop stabilises or the ECB signals a more decisive policy path.

The German IFO reading on Friday and the ECB decision next Thursday are the two events that are likely to shape the euro's near-term direction. A composite PMI already in contraction adds to the complexity of any hawkish ECB signal.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1700, 1.1750 and Support sits at 1.1600, 1.1520

USD: Safe Haven Demand Rebuilds

DXY: 98.65

The dollar index (DXY) trades at 98.85, headed for a weekly gain of 0.58%.

The dollar's bid comes from safe-haven demand rather than domestic data outperformance, though US data this week has done nothing to undermine the currency's position. Weekly initial jobless claims rose 6,000 to 214,000. The four-week moving average stands at 210,750. The insured unemployment rate held at 1.2%. In practical terms, the labour market continues to show stability despite the elevated macro uncertainty.

Fed funds futures now price just a 24% probability of a rate cut by year-end. The Federal Reserve (Fed) announces its monetary policy decision on Wednesday. With labour data resilient and energy-driven inflation risks building, the Fed has less reason to pivot than it did earlier in the year. This dynamic between stable US data and elevated global risk aversion is keeping the dollar supported even on days when the headline-driven optimism of the previous session fades.

The Swiss franc trade illustrated the dynamic. USD/CHF strengthened 0.08% to 0.7850. The Swiss National Bank's stated willingness to intervene to limit franc appreciation has, for now, contained franc strength - a notable counterpoint to the broader risk-off environment.

Against emerging Asian currencies, the dollar extended its gains. The Philippine peso fell 0.29% to $60.70. The Malaysian ringgit weakened 0.17% to $3.97.

Investors are now looking forward to the Fed decision next Wednesday. Any softening in tone could shift the dollar's near-term trajectory.

Global Ripples and the Intervention Watch

AUDUSD 0.7126 | NZDUSD 0.5851 | USDJPY 159.78 | GBPJPY 215.21

The Japanese yen hovered at 159.78 per dollar, a hair’s breadth away from the 160.00 level. This specific price point often triggers "decisive action" from Japanese authorities. Meanwhile, the Australian dollar and New Zealand kiwi saw modest gains of 0.04% and 0.07% respectively, though these antipodean currencies stay vulnerable to the broader safe-haven trend.

Japan faces a unique dilemma. Core inflation is accelerating due to energy costs, yet it remains below the Bank of Japan’s 2% target. Finance Minister Satsuki Katayama has renewed warnings of intervention. Because Japan relies heavily on imported oil, the standoff in the Strait of Hormuz directly weighs on the yen. All eyes now turn to the BOJ meeting next week. GBP/JPY trades at 215.21.

Bitcoin gained throughout the week. Ethereum rose. Crypto markets continue to track risk sentiment with a lag.

Currency moves reflect a mix of policy stance, energy exposure, and intervention signals. Volatility across these pairs continues to align with shifting macro drivers.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3462 | Bearish bias below 1.3500 |

| EUR/GBP | 0.8675 | Mild bullish |

| EUR/USD | 1.1679 | Range to bearish |

| USD/JPY | 159.78 | Bullish, intervention risk |

| GBP/JPY | 212.21 | Range |

| AUD/USD | 0.7126 | Neutral to mild bullish |

| NZD/USD | 0.5851 | Neutral |

| USD/CHF | 0.7850 | Bullish |

Market Lookahead

Tue, 28 April

- Bank of Japan Rate Decision

Wed, 29 April

- Federal Reserve Policy Decision

Thu, 30 April

- Eurozone HICP Inflation, UK GDP Q1

- Bank of England Rate Decision

- ECB Deposit Rate Decision

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.