Sterling Had a Good Morning. The Dollar Has Had a Bad Week.

8 min read

Share

UK GDP surprised at 0.5%, five times the forecast. The euro is on a nine-day streak. The dollar near six-week lows at 98 and losing its footing as risk appetite returns. Peace talks and energy shifts keep reshaping the board. FX reacts fast to shifting policy and geopolitics.

GBP: Sterling's Moment, With a Catch

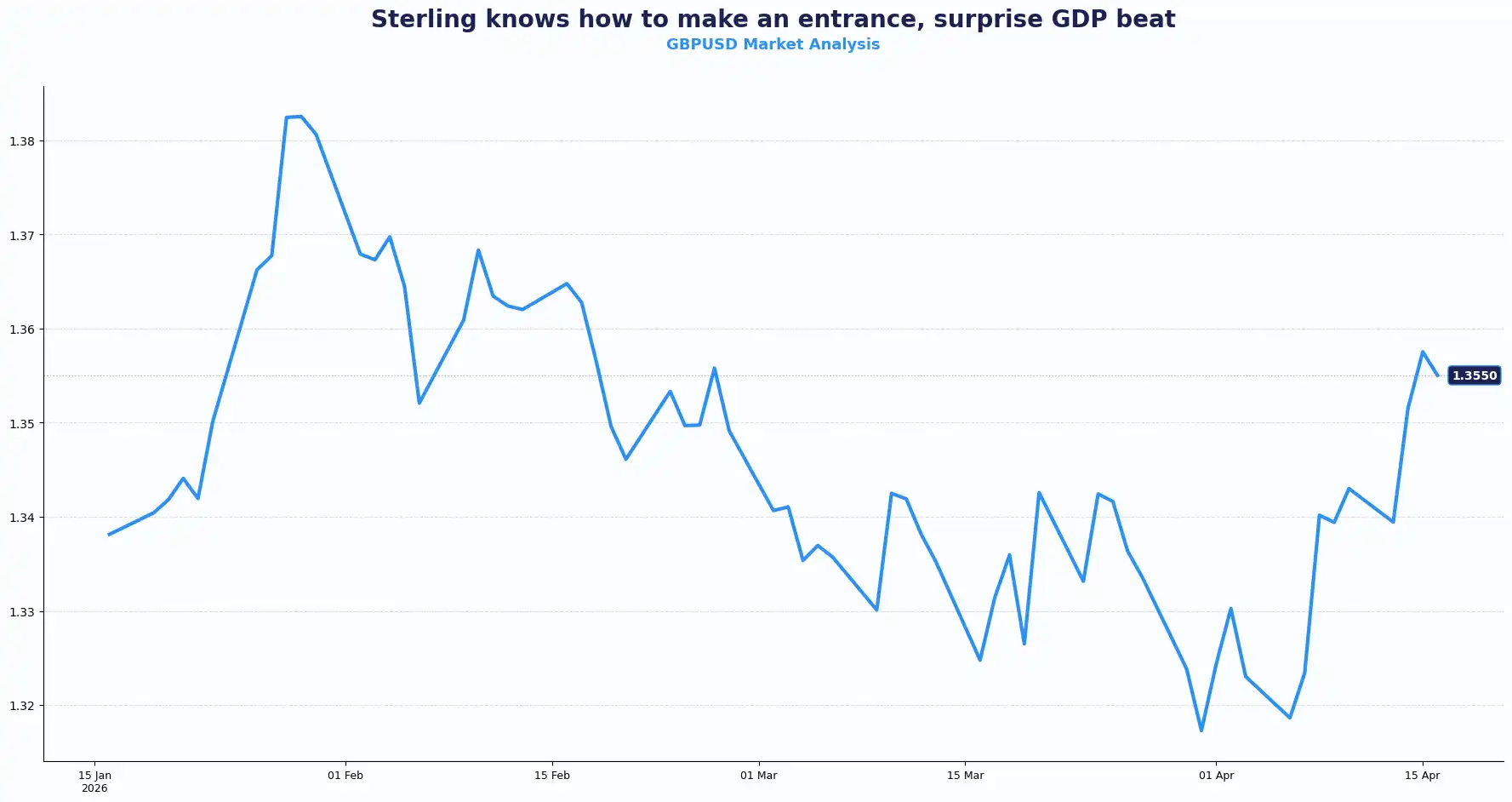

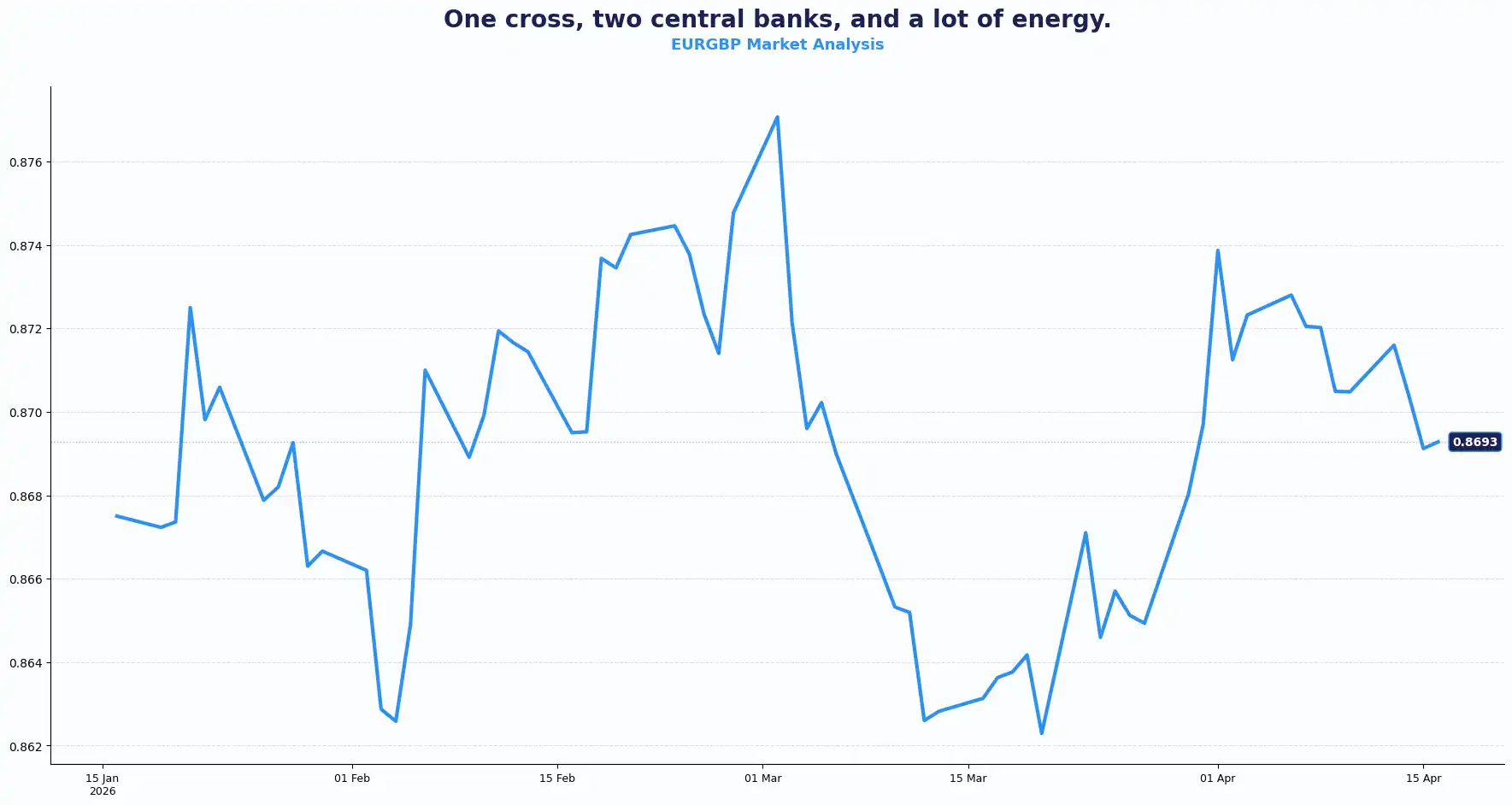

GBPUSD: 1.3580 | EURGBP: 0.8699

Sterling seized the spotlight this morning. The pound pushed 0.14% higher to $1.3580 against the dollar after the Office for National Statistics (ONS) delivered a February GDP reading of 0.5% MoM; five times the 0.1% forecast and a sharp acceleration from January's 0.1% prior. This GDP beat alone gave sterling a clear tailwind during the early European session.

Industrial production backed the headline, rising 0.5% MoM against a 0.2% consensus and printing at -0.4% YoY, which still beat the -0.9% consensus. Both reads pointed to an economy holding up better than anticipated.

The complicated story comes from manufacturing data. UK’s February manufacturing production contracted 0.1% MoM, and came in at -0.5% YoY, both missing forecasts. A notable divergence from the headline GDP number, reflecting that the economy grew, but not because factories were humming. The trade balance figures also showed a widening deficit at -0.72 billion pounds vs a prior £3.018 billion surplus, and non-EU figures also landed on a softer note. In a nutshell, the external account deteriorated sharply. Despite these mixed details, the headline growth keeps the pound in a position of command for now.

This data could change the narrative for the Bank of England (BoE) as robust growth gives policymakers room to breathe. MPC member Megan Greene recently noted that inflation is likely to jump to 3-3.5%, precisely the threshold at which households begin to notice. She flagged that second-round effects from the energy price shock could take months to become clear, and warned that waiting until those effects are visible amounts to moving too late. She was equally candid about the labour market weakening, though less dramatically than previously feared, with the risk of non-linear deterioration still alive. By contrast, BoE Governor Andrew Bailey notes that financial imbalances appear less worrying than in previous crises.

The policy picture is still not as straightforward. Greene's comments suggest that the MPC is closely watching the inflation-demand trade-off. The structural "why" rests on this domestic resilience. The UK economy refuses to buckle under high rates and this strength forces a wedge between the BoE and more dovish central banks.

The EUR/GBP pair trades choppy below 0.8700, with a broader upward bias due to the ECB's comparatively more contained inflationary position. However, sustained oil price declines from peace negotiations could ease BoE pressures, increasing chances of UK rate cuts and weighing on sterling against the euro.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3620, 1.3700 and Support sits at 1.3480, 1.3400

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8730, 0.8780 and Support sits at 0.8650, 0.8600

EUR: Euro Climbs a Nine-Day Ladder

EURUSD: 1.1804

The euro briefly broke through $1.18 and is on course for a ninth consecutive day of gains against the dollar, a streak that traces back to the onset of the Iran conflict in February, when the dollar initially strengthened sharply on safe-haven demand. As the dollar’s war premium unwinds, the euro has been among the primary beneficiaries.

Today brings the eurozone HICP data for March. The consensus expects core HICP at 2.3% YoY, unchanged from the prior reading, and headline HICP at 2.5% YoY with a 1.2% monthly print, also in line with the previous figures. These numbers confirm that price pressures hold a firm grip on the Eurozone. While a surprise reading is unlikely, confirmation at the consensus level would underline that eurozone inflation is tracking as expected, even as energy costs stay elevated.

ECB President Christine Lagarde has acknowledged that elevated energy costs have pushed the bloc off its baseline economic path, though she has stopped short of signalling imminent rate moves. ECB’s Nagel echoed this concern: "We're somewhere between the baseline scenario and adverse scenario," he said, adding that the inflation risk is rising. He views the current situation as shaky despite orderly equity behaviour. The ECB Monetary Policy Meeting Accounts, releasing today, could provide more detail on this stance, giving the Governing Council room to assess. Nagel confirmed that the ECB will have considerably more information when it meets later this month. The structural shift comes from the realisation that inflation might not return to target without further intervention.

Traders are pricing at least two ECB rate hikes by year-end. That trajectory is doing more for the EUR/USD pair than any single data point. The question: Will the eurozone's comparatively contained inflation backdrop (relative to the UK) sustain the policy divergence that has been supporting the cross?

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1850, 1.1920 and Support sits at 1.1720, 1.1650;

USD: The Dollar Slides as Peace Talks Gain Ground

DXY: 98.00

The dollar index (DXY) trades near 98.00 after hitting 97.96, a six-week low. The index is down 0.7% for the week and trading at its weakest level since early March. Optimism regarding a US-Iran ceasefire fuels the greenback’s retreat.

President Donald Trump suggested that the US-Israeli conflict with Iran is "close to over" and indicated further in-person talks would likely take place in Pakistan. Trump also posted on his socials that Israel-Lebanon talks would take place the following day. Resolving Lebanon has been one of the sticking points in the broader negotiation. Those headlines have been enough to encourage investors to dump safe-haven positions in favour of riskier assets. Global equities hit record highs while the dollar hit its weakest level since February. In the oil sector, Brent Crude rose slightly to $95.23. Reports suggest Iran might allow free passage through the Strait of Hormuz.

The structural decline of the dollar stems from a "peace dividend" and political tension. The standoff between President Trump and Federal Reserve Chair Jerome Powell has resurfaced as a market concern. Trump threatened to remove Powell from his separate seat on the Fed's Board of Governors if Powell does not vacate when his term as Fed Chair ends on 15 May. That adds another layer of uncertainty around Fed independence at a moment when the institution's path is already contested.

On the energy side, EIA crude oil inventory data showed a surprise draw of 0.9 million barrels vs expectations of a 2.1 million barrel build, adding another layer of complexity to the inflation outlook.

Technically, 98.00 is flagged as a key near-term support level. A sustained break below that level opens the door to further downside and would resume the broader downtrend for the dollar that has been building since last year. This weakness in the dollar alters the cost of imports and exports globally.

US initial jobless claims and the four-week average figures also arrive today. Given the broader dollar trajectory, a notable surprise in either direction could add to the day's volatility.

The Rest of the Board: Risk On, Broadly

AUDUSD: 0.7190 | NZDUSD: 0.5916 | USDJPY: 158.71 | GBPJPY: 215.47

The Aussie dollar hit a four-year high at 0.7190 against the dollar, buoyed by the broad risk-on environment and an Australian employment print for March that came broadly in line with expectations, sufficient for markets to sustain pricing at roughly a 70% probability of a third RBA rate hike in May.

The kiwi dollar advanced to a near one-month high at 0.5916 against the dollar.

USD/JPY sat near 158.71. Japan's finance minister noted that Tokyo and Washington agreed to intensify communication on exchange rates following her meeting with US Treasury Secretary Scott Bessent on Wednesday; enough to keep market participants watchful, though no direct intervention has been signalled yet.

The offshore yuan traded near 6.8152 per dollar, close to a three-year high. The onshore rate printed at 6.8174. The yuan has strengthened around 2.5% against the dollar YTD, driven by strong Chinese export flows and corporate conversion of dollar holdings into yuan. Since the onset of the Iran conflict, the yuan has been the strongest-performing currency, outperforming even the dollar during its initial safe-haven surge.

Asian equities advanced as optimism around a US-Iran settlement grew. Regional earnings commentary has pointed to AI-related demand as a relatively insulated driver, even if broader global demand faces headwinds from sustained energy costs.

GBP/JPY trades near 215.47. GBP/AUD sits at 1.8878, with the Aussie at multi-year highs and Australian bank rates pointing up, sterling faces comparative headwinds on this cross.

Risk-sensitive currencies move with global sentiment and the outlook for interest rates. Stability in growth expectations keeps upward pressure intact, though moves appear to be headline-driven for now.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3580 | Uptrend |

| EUR/GBP | 0.8699 | Range / Up bias |

| GBP/JPY | 215.47 | Uptrend |

| GBP/AUD | 1.8878 | Range, bearish |

| EUR/USD | 1.1804 | Bullish |

| AUD/USD | 0.7190 | Uptrend |

| NZD/USD | 0.5916 | Mild bull, up |

| USD/JPY | 158.71 | Bearish |

| USD/CNH | 6.8152 | firm |

| DXY | 98.00 | Bearish |

(as at the time of writing)

Market Lookahead

Thu, 16 April

- Eurozone Core HICP (March)

- Eurozone HICP (March)

- ECB Meeting Accounts

- US Initial Jobless Claims + 4-week average

- Speeches from ECB and BoE officials

Fri, 17 April

- Eurozone Trade Balance (February)

Ongoing

- US- Iran peace talk developments

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.