Trading the Rumour, Bracing for the Rate

8 min read

Share

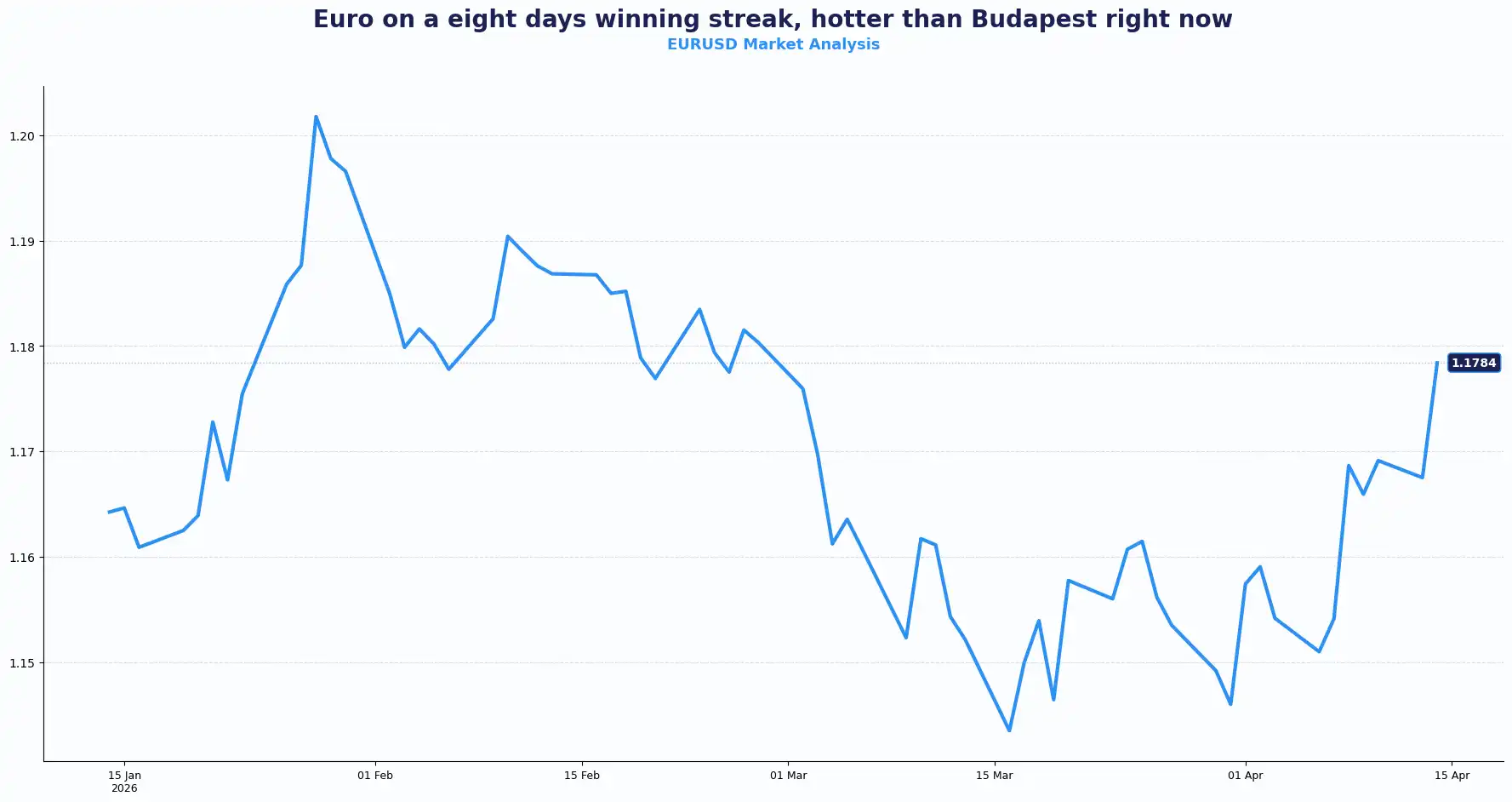

Oil near $98, Iran talks live, ceasefire still unsigned. GBP at 1.3514, EUR on an eight-day winning streak, and the dollar edges toward its longest losing run since December. A tense Tuesday opening where diplomacy is doing the heavy lifting.

GBP: Pound Hit a Six-Week Ceiling

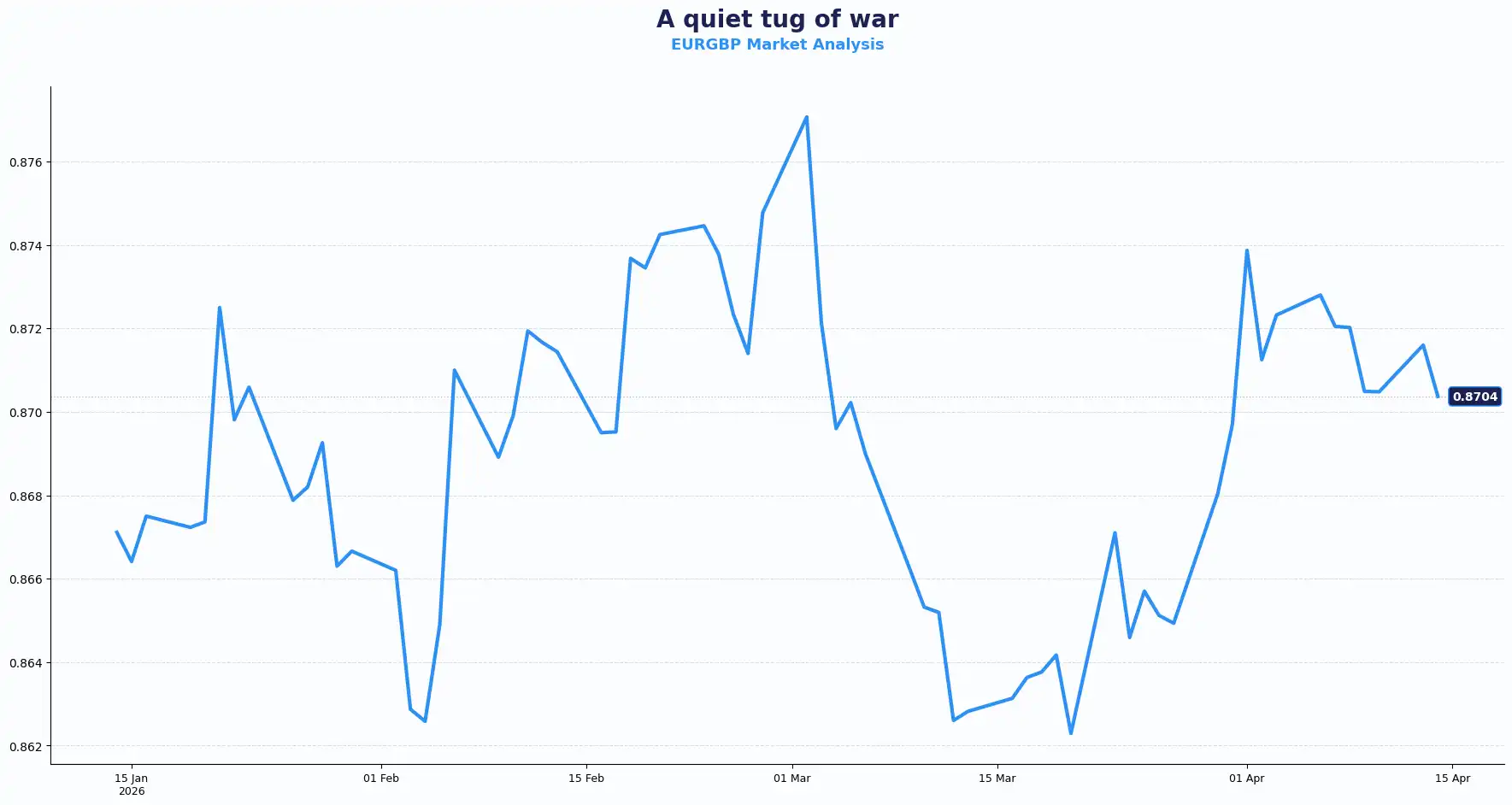

GBP/USD hit a fresh six-week high above 1.3500, printing at 1.3514 during the Asian session. EUR/GBP sits at 0.8702.

The pound took on a risk-on tone as Trump and Vice President JD Vance both publicly signalled that Washington-Tehran negotiations had forward motion, enough to keep appetite for riskier assets intact. Sterling, which tends to outperform when global risk sentiment firms, caught that bid.

Back home, the domestic story carries a hawkish undertone that is doing sterling no harm. The energy price surge has fed through to UK inflationary pressures, and traders now price at least one Bank of England (BoE) rate hike before the end of 2026, to counter the “higher-for- longer” energy pulse. This is a sharp reversal from where expectations sat before the conflict began. The rate repricing underpins GBP against currencies where other central banks are cutting or keeping rates on hold. The pound isn't just rising on peace hopes; it’s rising because the UK economy must tighten to survive the current cost shock.

Investors are watching closely for remarks from BoE Governor Andrew Bailey today, followed by MPC members Catherine Mann and Megan Greene. Any signal that the Bank views energy-driven inflation as persistent rather than a shock, and that it can look through, reinforces the hawkish read.

Thursday brings the UK's February GDP, alongside industrial production and manufacturing output. February GDP is expected to print at +0.1% MoM. This modest but positive reading, which could confirm that the economy held its footing heading into the conflict period, may be constructive for sterling sentiment.

We are seeing a classic policy divergence play. A BoE tilting hawkish against a Federal Reserve (Fed) too uncertain to move in either direction, gives sterling a relative rate advantage that has become a live driver of the GBP/USD pair in the near-term.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3550, 1.3600 and Support sits at 1.3400, 1.3330

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8750, 0.8800 and Support sits at 0.8650;

EUR: Euro Reclaims Its Edge, Budapest Bonus

EURUSD: 1.1763 | EURHUF: 362.90 | USDHUF: 308.41

EUR/USD sits at 1.1763, flat on the session but building on yesterday's 100-pip surge, the pair's eighth consecutive daily gain, its strongest run since early March. The pair touched 1.1765–1.1770 during the Asian session.

Two very different stories are underpinning the euro right now.

Hungary: A Political Earthquake with FX Aftershocks

Sunday's Hungarian parliamentary election produced a watershed result. Peter Magyar's pro-EU Tisza party secured 138 seats in the 199-seat parliament on 53.6% of the vote, handing Viktor Orbán a historic defeat after 16 years in power. The forint surged to a four-year high, appreciating 2.9% to 363.84 per euro, with further gains following Magyar's statement that Hungary's accession to the euro area was in the country's interest.

For the euro, this matters beyond the forint headlines. The proposed reforms could align Hungary more closely with EU standards and help release more than EUR 20 billion in EU funds currently frozen over rule-of-law and corruption concerns. Orbán had also blocked a €90 - 103 billion loan package for Ukraine and repeatedly stalled EU sanctions. His exit clears a significant institutional logjam. Some analysts note that no European policymaker has done more to weaken EU cohesion than Orbán and that his removal is therefore structurally positive for EU fiscal coordination and, at the margin, supportive of the single currency.

Germany: Growth Cut, Inflation Sticky

On the macro side, Germany cut its 2026 growth forecast to 1.0% (from a prior estimate above that), keeping 2027 at 1.5%. Inflation projections for 2026 sit at 2.7%. Industrial production is weak, exports are holding, and core inflation is stable. The picture is one of an economy muddling under the weight of energy costs and Middle East uncertainty.

The European Central Bank (ECB) held rates unchanged in March. Markets now anticipate two 25bp hikes in June and September, with some pricing of a hike in ECB’s April meeting. The deposit rate sits at 2.0%, seen as neutral. Eurozone Core Harmonized Index of Consumer Prices for March is expected at 2.3% YoY and HICP 2.5% YoY unchanged from previous month.

Historically, when the ECB pivots to a hiking path while global uncertainty is elevated, EUR/USD tends to find base support rather than a sustained surge because risk-off flows simultaneously drag on European assets, and that tension is precisely what keeps EUR/USD in a grind higher rather than a breakout. The Ukraine war resolution potential via a now-cooperative Hungary adds an asymmetric upside scenario that is not yet fully priced.

ECB President Lagarde speaks today. Her tone on the ECB outlook, will set the near-term direction. Traders are also watching for any language on the persistence of energy inflation, which is currently acting as the ECB's primary justification for the hike path.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1765-1.1770, 1.1850 and Support sits at 1.1680, 1.1580;

USD: Dollar's Seven-Day Slide, A Fading Safe Haven

DXY: 98.34

DXY sits at 98.34, near its weakest level since 2 March, the first trading day after the US-Israel-Iran conflict broke out. A seventh consecutive daily decline would be the dollar's longest losing streak since December.

This is the dollar's fundamental paradox this week. Historically, it climbs with geopolitical tension as a safe-haven bid, reinforced by the US being a net energy exporter and therefore relatively insulated from an oil price shock. But diplomacy is chipping at that bid. As hopes of a US-Iran deal live on, the safe-haven premium that propped up the dollar through the conflict's early weeks is slowly deflating.

Chicago Fed President Austan Goolsbee offered a measured take: oil futures are pricing in an expectation that the price surge will be short-lived. If that holds, the economic impact on the US may prove limited. If the conflict extends, he acknowledged it would require a full reassessment. Money markets now show less than a 20% chance of a Fed rate cut this year, a dramatic reversal from pre-war expectations.

Today arrives US PPI for March PPI, figures expected at +1.2% MoM (prior: +0.7%) and +4.6% YoY (prior: 3.4%). Ex-food and energy: +0.6% MoM, +4.2% YoY. A beat on these figures would reinforce the hawkish repricing already underway, providing fresh support for the dollar at a time when geopolitical optimism is pulling the other way. A miss opens the door to further downside for DXY.

Erin Browne: The Treasury Nomination by Trump

The Under Secretary for International Affairs post manages US currency policy and relationships with foreign finance ministries on global economic matters. Trump's nomination of PIMCO Managing Director Erin Browne fills a role that has been vacant and consequential. Browne must undergo Senate confirmation to take up the post.

Her appointment signals continuity with a pragmatic, market-aware approach to currency policy. Browne has publicly taken the view that the Fed's policy path is constrained by inflation persistence, a view broadly consistent with the current market narrative. For the dollar, a confirmed Under Secretary focused on international financial relationships could bring greater clarity to currency policy communication at a time when the DXY's direction is genuinely contested.

Antipodeans & Japan: Risk Sentiment Drives the Bus

AUDUSD: 0.7083 | NZDUSD: 0.5870 | USDJPY: 159.116 | GBPJPY: 215.22

The Aussie dollar edged lower after briefly touching $0.71 overnight. Resistance at 71 cents proved firm. Business and consumer confidence surveys in Australia showed a sharp deterioration linked to the Iran conflict; an ominous sign for an economy already running on thin growth margins. The Antipodeans trade as proxies for global risk, and until the Middle East situation resolves, that dynamic keeps both AUD and NZD on a short leash despite the broader risk-on tone.

The Kiwi dollar held near $0.5870, supported by the NZ central bank's unexpected hawkish turn last week. NZD has gained approximately 0.3% against the Aussie on Tuesday on that policy divergence, with NZD/AUD trading around 1.2055.

USD/JPY sits at 159.02, down 0.3% on the session. The yen faces a structural headwind: Japan's trade balance is expected to deteriorate as oil prices stay elevated, and the Bank of Japan is widely expected to stand pat at the end of April. Positioning points to a test of 160 if the BoJ holds. That level is where speculation about intervention intensifies.

Brent crude at $98.58. WTI at $97.39. Both well off the $100 handle, but not far enough below it to remove the inflationary pressure reshaping central bank expectations globally.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3514 | Bullish |

| EUR/USD | 1.1763 | Bullish |

| EUR/GBP | 0.8702 | Neutral, Flat |

| DXY | 98.34 | Bearish |

| USD/JPY | 159.116 | Cautious |

| GBP/JPY | 215.22 | Bullish |

| AUD/USD | 0.7083 | Rangebound |

| NZD/USD | 0.5870 | Mild Bullish |

| USD/HUF | 308.41 | HUF Strength |

| EUR/HUF | 362.90 | HUF Strength |

Market Lookahead

Tue, 14 April

- US PPI March

- ECB President Lagarde Speech

- BoE Governor Bailey speech; BoE's Mann and Greene commentaries

Thu, 16 April

- UK GDP Feb

- UK Industrial Production data

- UK Manufacturing output

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.