Dollar slides to six-week low as soft PPI reprices Fed cut odds sharply

5 min read

Share

US producer prices undershot forecasts by a wide margin on Tuesday, with core PPI delivering its softest monthly print in months. Oil fell 7.90% on renewed US-Iran diplomacy signals. The dollar extended its losing streak to an eighth consecutive session, dropping to its lowest level since late February. Every major pair is repricing on USD weakness this morning, not domestic strength. April 21 remains the date that matters: if the ceasefire fails to hold, this entire trade reverses.

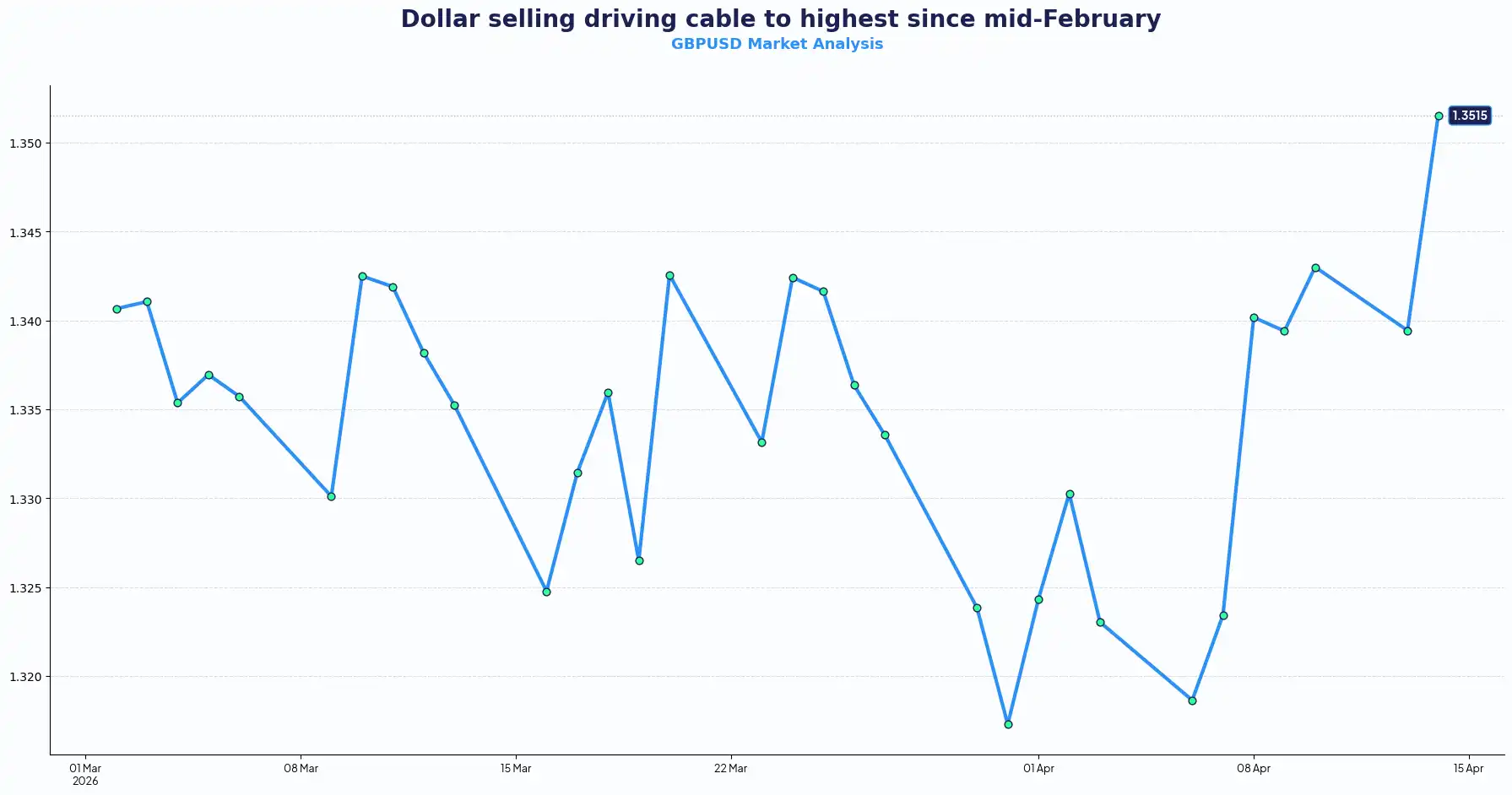

GBP/USD | Daily | Dollar selling driving cable to highest since mid-February

GBP/USD is trading at 1.3567 (as at time of writing), having cleared prior resistance at 1.3514, which now serves as support. The weekly high at 1.3590 is the immediate ceiling; 1.3650 is the next level worth watching.

The BoE narrative has shifted. OIS pricing reflects roughly 30–40bp of hikes for 2026, a notable pullback from the most aggressive repricing seen earlier this month. JPMorgan has trimmed its BoE call from two hikes to one in June, directly citing Governor Bailey's assessment that markets were "getting ahead of themselves." The front-end 2Y Gilt dropped 12bp to 4.21% while the 10Y rose. That curve steepening reflects front-end rate expectations being walked back, not a broad risk-off move.

MPC member Greene is the counterweight that keeps the BoE story from fully unravelling. She warned on April 14 that second-round inflation effects could take months to confirm, and she frames the inflation risk as more pressing than the growth softness. One hike remains priced. That is enough to put a floor under GBP for now.

Thursday's UK February GDP print is the next GBP-specific test, with consensus at +0.1% MoM. A miss hands the bears a reason to fade the rally and gives Bailey's patience narrative added credibility.

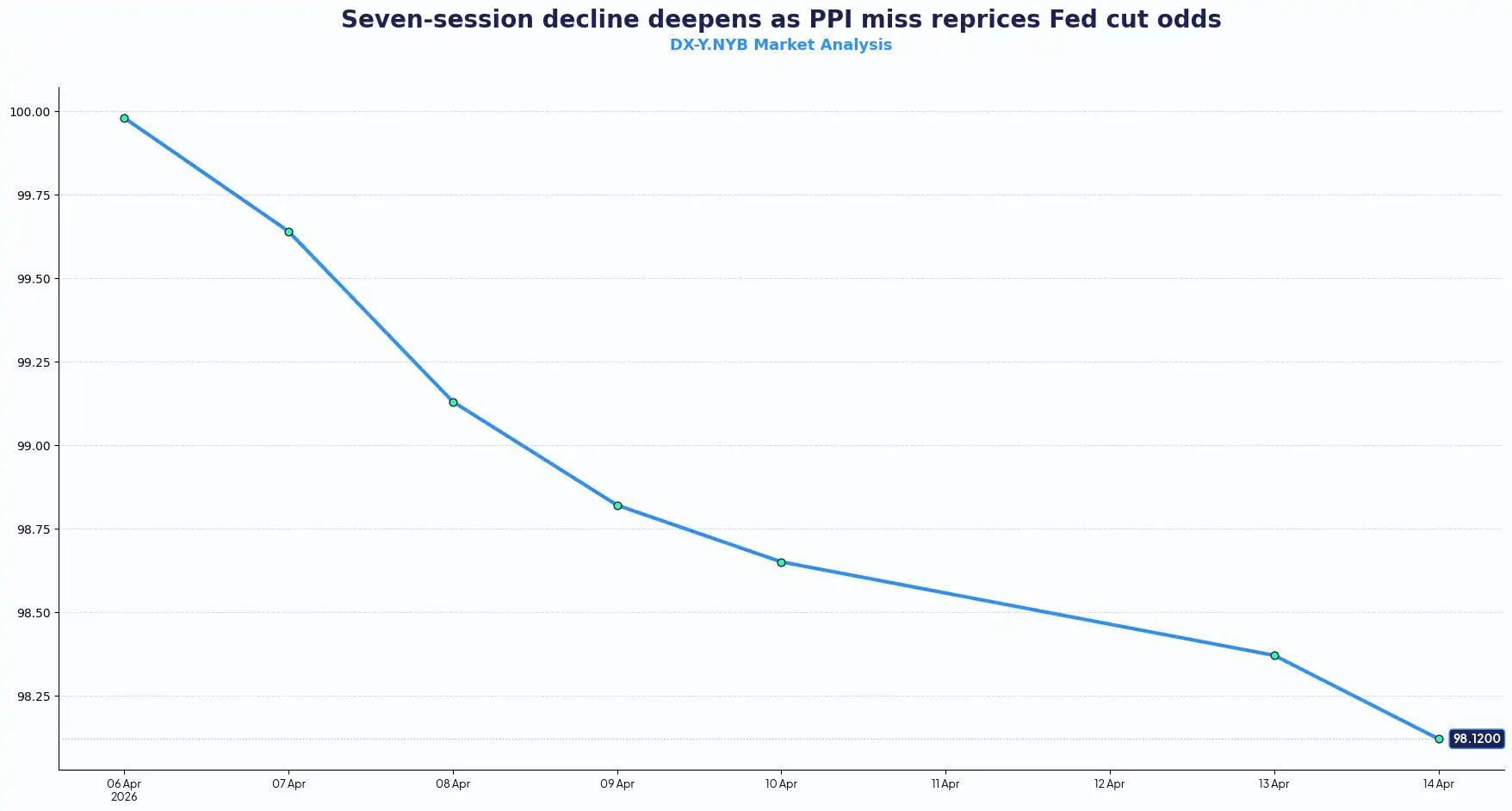

USD/DXY | Daily | Seven-session decline deepens as PPI miss reprices Fed cut odds

DXY is trading at 98.10–98.13 (as at time of writing), below the 98.34 level that now acts as resistance. The next two levels to watch are 97.80, the intraday low, and 97.50, which marks the February range low.

March PPI came in at +0.5% MoM headline against a +1.1% consensus; core at +0.1% MoM versus +0.3–0.4% expected. The read points to businesses absorbing cost pressures at the margin rather than passing them downstream. Fed rate cut probability for 2026 repriced to approximately 33%, up sharply from below 20% in the prior session. The US 10Y yield fell to around 4.29%.

The Fed is not speaking with one voice. Chicago President Goolsbee warned cuts could slip to 2027 and raised the spectre of unmoored inflation expectations. Fed Governor Miran, who dissented in March in favour of a cut, countered that inflation is "running pretty close to our target" and expects it near the 2% mark within a year. Markets sided with the softer data. That is the resolution that matters for FX desks today.

WTI fell 7.90% to $91.28/bbl on resumed US-Iran talk signals, stripping out the energy cost pillar that had underpinned the dollar's safe-haven premium. The Fed Beige Book releases today and could add another layer to the narrative. April 21 remains the single most important date: a ceasefire breakdown is the cleanest path back to a stronger dollar.

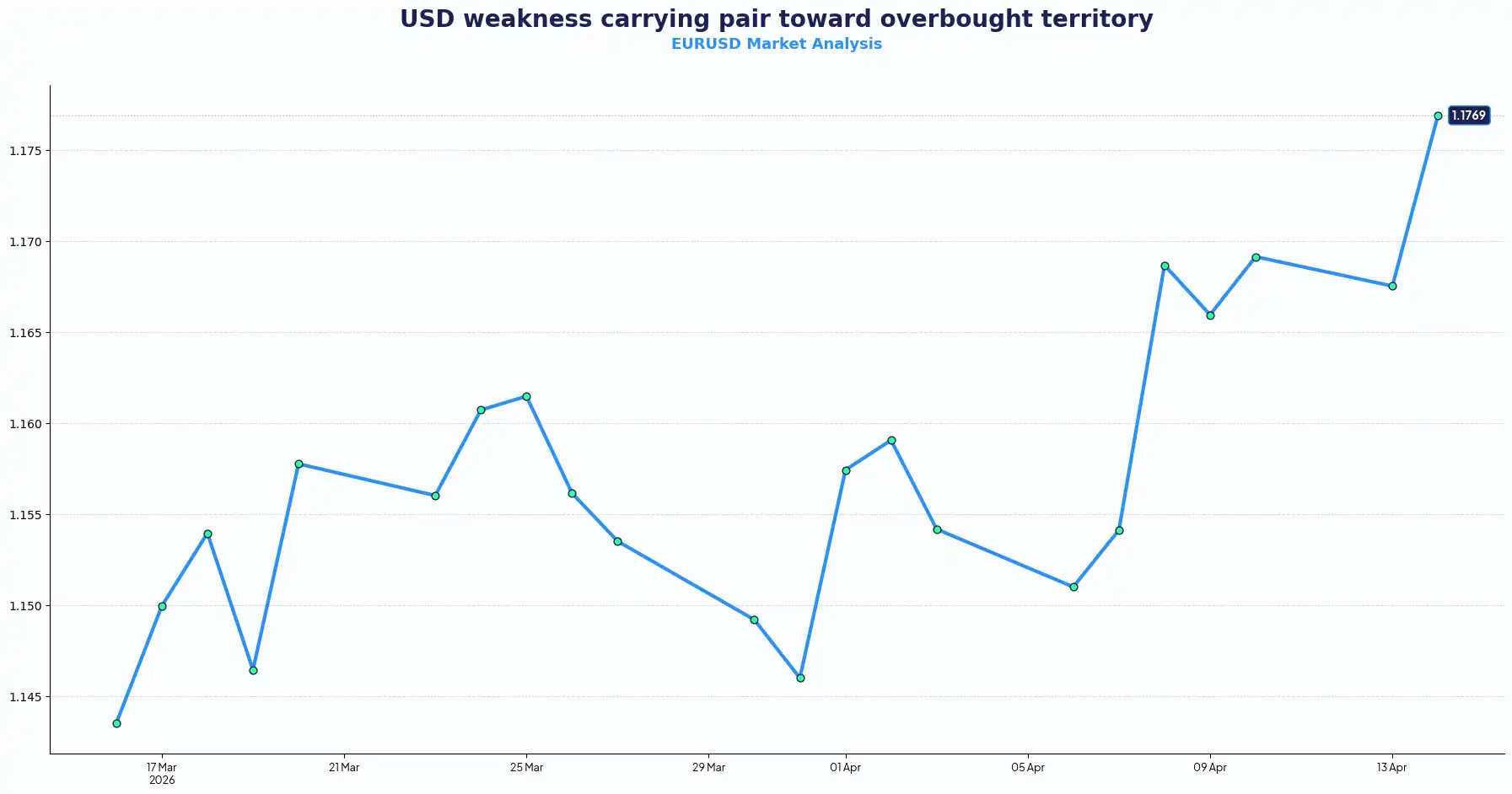

EUR/USD | Daily | USD weakness carrying pair toward overbought territory

EUR/USD is trading at approximately 1.1798 (as at time of writing), having touched a weekly high of 1.18085. Support sits at 1.1760 (prior breakout level) and 1.1725 (20-period SMA per FXStreet). Resistance is at 1.1808, then 1.1850.

The pair's seven-to-eight session winning streak is a dollar story, not a euro story. ECB President Lagarde told the IMF/World Bank Spring Meetings that conditions are "not yet enough to warrant leaning toward raising interest rates," which trimmed the most aggressive ECB repricing that had been building. Markets still expect roughly two hikes by year-end, implying a year-end rate around 2.50–2.60%, with June pricing at approximately 76% probability. But Lagarde's framing was notably cautious relative to prior expectations, and it shows. EUR is not outperforming on the crosses. EUR/GBP is broadly flat. Euro-specific demand is thin.

RSI is approaching 73 on the daily (per FXStreet), a level that historically precedes consolidation or corrective pullback after extended directional runs. Tomorrow's Eurozone final March HICP is the key near-term test. The flash read showed headline inflation at 2.5%, driven entirely by energy flipping from -3.1% to +4.9%; core actually ticked down to 2.3%. If the final print confirms that split, the "energy-driven, not core-driven" inflation narrative holds and limits how hard the ECB needs to act. That is the framing to watch if you have EUR payables to hedge this month.

Market snapshot

| Pair | Spot rate | 1-week range | Key technical level | Next risk event |

|---|---|---|---|---|

| GBP/USD | 1.3572 | 1.3514–1.3590 | Resistance 1.3590 | UK Feb GDP, Thu 17 Apr |

| EUR/USD | 1.1791 | 1.1760–1.1811 | Support 1.1725 (20-SMA) | Eurozone HICP final, Thu 17 Apr |

| DXY | 98.13 | 97.97–98.34 | Support 97.80 | Fed Beige Book, today |

| USD/JPY | 158.98 | 157.53–160.09 | Resistance 160.09 (intervention zone) | Ceasefire expiry, Tue 21 Apr |

| AUD/USD | 0.7124 | 0.7057–0.7127 | Resistance 0.7150 | China Q1 GDP, Thu 17 Apr* |

| USD/CAD | 1.3760 | 1.3732–1.3948 | Resistance 1.3850 (200-day EMA) | BoC Outlook Survey, Mon 20 Apr |

Week-ahead calendar

| Date | Time (GMT) | Event | Consensus / Prior |

|---|---|---|---|

| Tue 15 Apr | 19:00 | Fed Beige Book | Qualitative |

| Thu 17 Apr | 07:00 | UK Feb GDP MoM | +0.1% / +0.4% prior |

| Thu 17 Apr | 10:00 | Eurozone final March HICP | 2.5% flash / 2.2% prior |

| Thu 17 Apr | TBC | China Q1 GDP YoY | 4.8% consensus |

| Tue 21 Apr | TBC | US-Iran ceasefire expiry | Binary: talks resume or conflict escalates |

All spot rates are indicative and subject to change. This briefing is for informational purposes only and does not constitute financial advice or a recommendation to transact. Currency Solutions is authorised and regulated by the Financial Conduct Authority.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.