Ceasefire Extends, UK CPI Rises, Dollar Keeps Its Edge

7 min read

Share

UK CPI beat on headline at 3.3% YoY but core eased, keeping BoE rate hike bets capped. Sterling holds $1.35. Ceasefire extended but few are fully buying it. The Strait of Hormuz stays shut and Brent hovers near $100. Dollar firms on strong retail sales and Warsh's hawkish tone, while the ECB is in no rush. Energy risk continues to drive the majors.

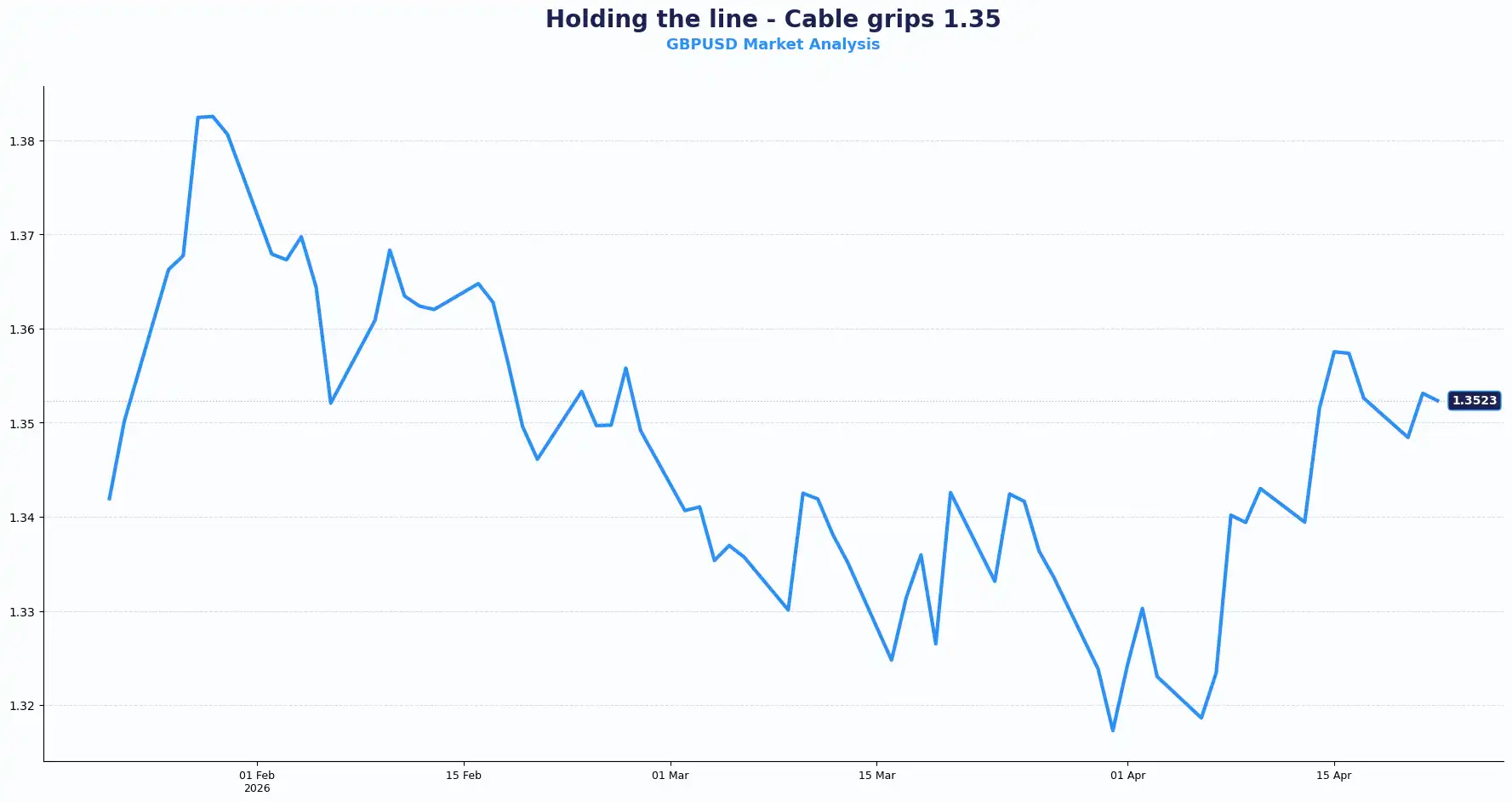

GBP: Inflation Beat, but the Core Tells a DIfferent Tale

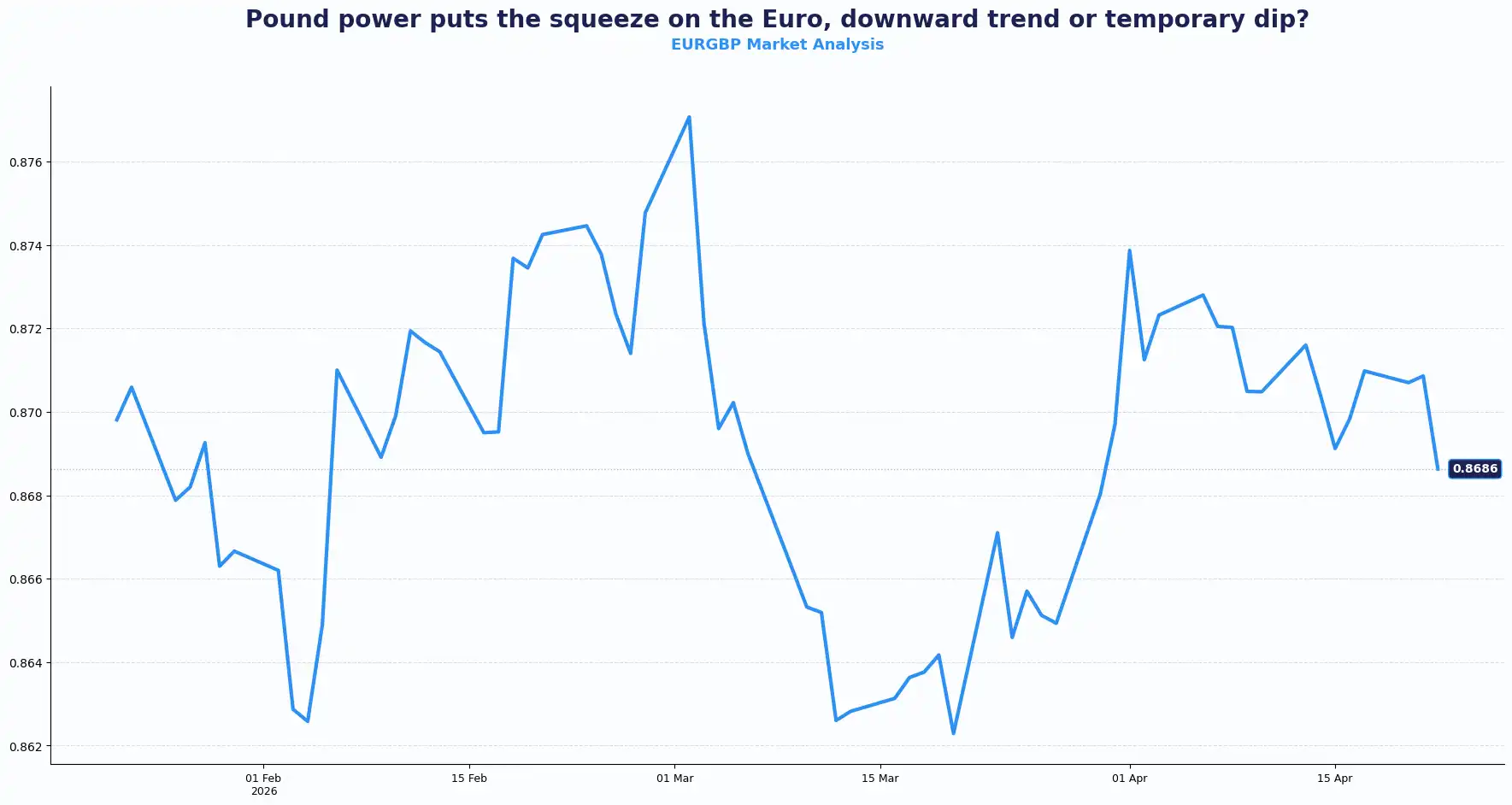

GBPUSD 1.3528 | EURGBP 0.8690

Sterling held just above $1.35 in the early European session on Wednesday. The pound absorbed a mixed inflation print while finding its footing amid renewed uncertainty over the Iran ceasefire.

UK CPI for March came in at 3.3% YoY, in line with consensus, but the monthly read nudged higher, at 0.7% vs an expected 0.6% and previously 0.4%. Core CPI eased slightly to 3.1% YoY, from 3.2% prior. This tells us that headline inflation is rising on energy costs, but the second-round effects on core inflation have not yet arrived.

The Retail Price Index for March printed 0.8% MoM against a 0.7% forecast, and 4.1% YoY vs a 3.9% consensus expectation. PPI Output came in at 0.9% MoM against a 1.0% forecast. Taken together, input and output price pressures are building, but not yet running away.

This is the first of the UK CPI data covering the period after the US and Israeli airstrikes on Iran in late February. Higher energy costs, particularly oil prices, were widely anticipated to push headline inflation higher. The key question for the Bank of England (BoE) is whether those pressures feed through into persistent, second-round core inflation, and on today's data, the jury is still very much outBoE policymaker Megan Greene addressed this recently: "We won't have definitive evidence of second-round effects for a while; it could take months."s." She added that the Bank "can't just look through negative supply shocks" and that a more nuanced assessment is needed.

Rate expectations have shifted considerably. BoE rate-hike bets over the next 12 months dropped from as much as 100 bps in late March to just 25 bps currently. The BoE itself estimates a negative output gap of around -1% of GDP in 2026, slack that weighs against aggressive tightening. Recent UK jobs data added further nuance, with wage growth slowing, unemployment unexpectedly falling, and vacancies declining. The report had little impact on sterling, however, as it pre-dates the Iran conflict and does not capture how the labour market is evolving under current conditions.

On the political front, former Foreign Office chief Olly Robbins testified about his role under Prime Minister Keir Starmer amid the Peter Mandelson ambassador controversy.sy. Robbins stated that while he felt pressure to approve Mandelson's appointment, there was no direct contact from Number 10 during the vetting process. Labour's standing ahead of the May local elections continues to generate uncertainty, and UK political noise remains a background factor in sterling sentiment.

EUR/GBP is holding below 0.8700, caught between fading BoE tightening expectations on one side and ECB caution on the other. The cross reflects a broadly balanced picture between two central banks in no particular rush.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3560, 1.3600 and Support sits at 1.3480, 1.3440;

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8710, 0.8740 and Support sits at 0.8660, 0.8630; Bias: rangebound, mild bearish

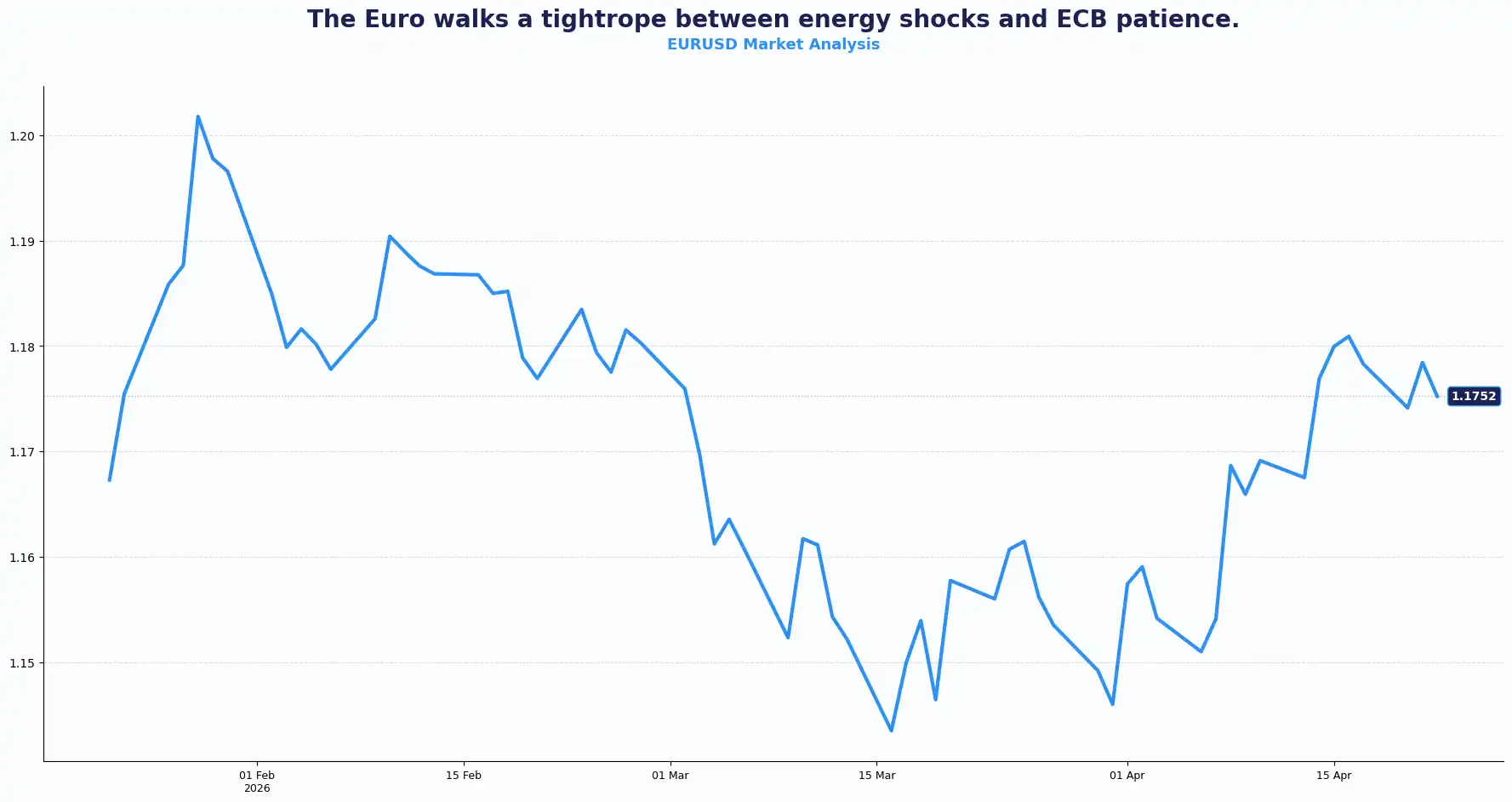

EUR: Euro Sensitivity to Energy Shocks

EURUSD 1.1755

The euro was steady on Wednesday. EUR/USD held near 1.1755, broadly supported by dollar shakiness rather than any particular euro-area catalyst.

Markets are currently digesting warnings from ECB President Christine Lagarde, who flagged that the eurozone outlook is highly uncertain, amid what she described as an"enormous" energy supply shock stemming from the Strait of Hormuz blockade. She noted that energy prices have not yet reached worst-case levels but that the picture remains fragile.

The ECB appears more patient than its peers. ECB Governing Council member Martins Kazaks notes that the ECB has "the luxury" of waiting on interest rate decisions. "There is no urgency to raise interest rates just yet," Kazaks said. "We are not in a rush." He acknowledged that the impact of the Middle East conflict on the real economy is feeding through only gradually and that the ECB can monitor developments before acting. He did confirm that "if necessary, we will of course move." While oil prices have retreated from March peaks, the continued maritime blockade keeps the threat of an inflationary shock alive. The Eurozone outlook stays fragile until energy flows normalise.

This is a central bank that has optionality and is choosing to use it. With data still clouded by geopolitical disruption and energy price volatility, the ECB's wait-and-see posture is deliberate and data-dependent.

Continental uncertainty keeps the euro in a reactive state. With the ECB in "monitoring mode," the currency is highly sensitive to tomorrow’s manufacturing and services reports. Any sign of economic resilience might embolden the hawks.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1800, 1.1850 and Support sits at 1.1700, 1.1650; Bullish Bias

USD: Oil and Data Keep the Dollar Supported

DXY 98.24

The dollar index (DXY) held near 98.24 on Wednesday, briefly touching a one-week high in Asia before pulling back. Its strength was driven by strong retail sales, the hawkish tone from Federal Reserve nominee Kevin Warsh, and scepticism over the Iran ceasefire announcement.

US retail sales rose 1.7% in March, beating the 1.4% consensus. This was mainly due to a record surge in service station receipts as oil prices rose and tax refunds boosted spending.

Warsh, at his Senate confirmation, emphasised Fed independence and rejected President Trump's call for rate cuts. His tone was interpreted as slightly hawkish. That said, Overnight Index Swaps (OIS) pricing barely moved, implying Warsh's impact was limited. The dollar's gains appear driven by higher oil prices and geopolitical news rather than a shift in Fed expectations.

Fed funds futures now price a 59.7% implied probability that the Fed holds rates steady as late as its April 2027 meeting, up from 56.7% the day before, according to CME FedWatch. Rate cut expectations are being delayed.

President Trump extended the Iran ceasefire indefinitely but said the US blockade on Iranian ports would continue. The Strait of Hormuz stays effectively closed, and Brent Crude is near $100 a barrel. An internal power struggle within Iran, between the hardline Islamic Revolutionary Guard Corps (IRGC) and more moderate factions continues to cloud the path to any durable resolution.

The timeline for normalising energy export flows through the Strait of Hormuz remains open-ended.

Global Flows, Quiet Moves

AUDUSD 0.7172 | NZDUSD 0.5916 | USDJPY 159.14 | GBPJPY 215.30

The Australian dollar nudged higher and the New Zealand dollar edged up modestly. Both pairs reflected the broader risk-on tone as ceasefire optimism provided a mild tailwind to risk-sensitive currencies.

USD/JPY was flat near 159.14. Recent data showed Japan's exports rose for a seventh consecutive month, with no major disruption from the Gulf conflict apparent in the figures yet; though the yen remains pinned by the wide interest rate gap with the US.

Commodity-linked currencies like the AUD and NZD are tethered to the pulse of the peace talks. As long as energy exports remain in limbo, volatility is likely to stay elevated across all G10 pairs.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3528 | Sideways/mild bullish bias |

| EURUSD | 1.1755 | bullish bias |

| EURGBP | 0.8690 | Rangebound, mild bearish |

| USDJPY | 159.14 | Dollar mildly bid |

| AUDUSD | 0.7172 | Mild Bullish |

| NZDUSD | 0.5916 | Mild Bullish |

| GBPJPY | 215.30 | Bullish Bias |

(as at the time of writing)

Market Lookahead

Thu, 23 April

- Eurozone & Germany HCOB PMI (Manufacturing, Services, Composite)

- UK, US S&P Global PMI (Manufacturing, Services, Composite)

- US Initial Jobless Claims

Fri, 24 April

- UK GfK Consumer Confidence

- Japan National CPI

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.