GBP and EUR Bought the Optimism. The Strait's Still Closed.

8 min read

Share

Sterling and the euro climb as Middle East optimism unwinds the dollar's safe-haven bid. Ceasefire hopes push GBP and EUR to seven-week highs as central banks strike a cautious tone on rates. Energy risks hold quietly in the background. Strategic eyes turn to the Strait of Hormuz for the next move.

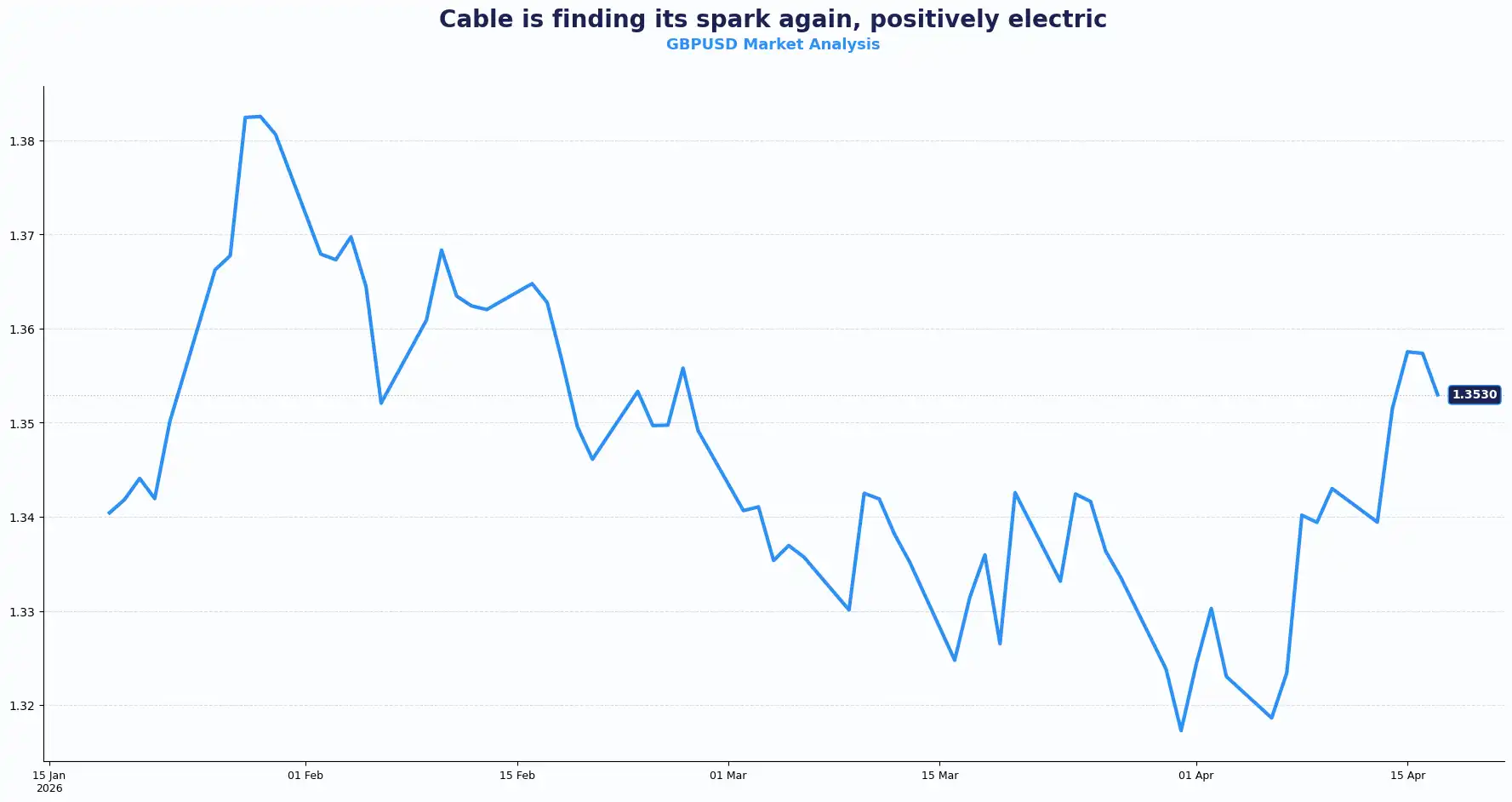

GBP: Sterling Steadies as Risk Cools

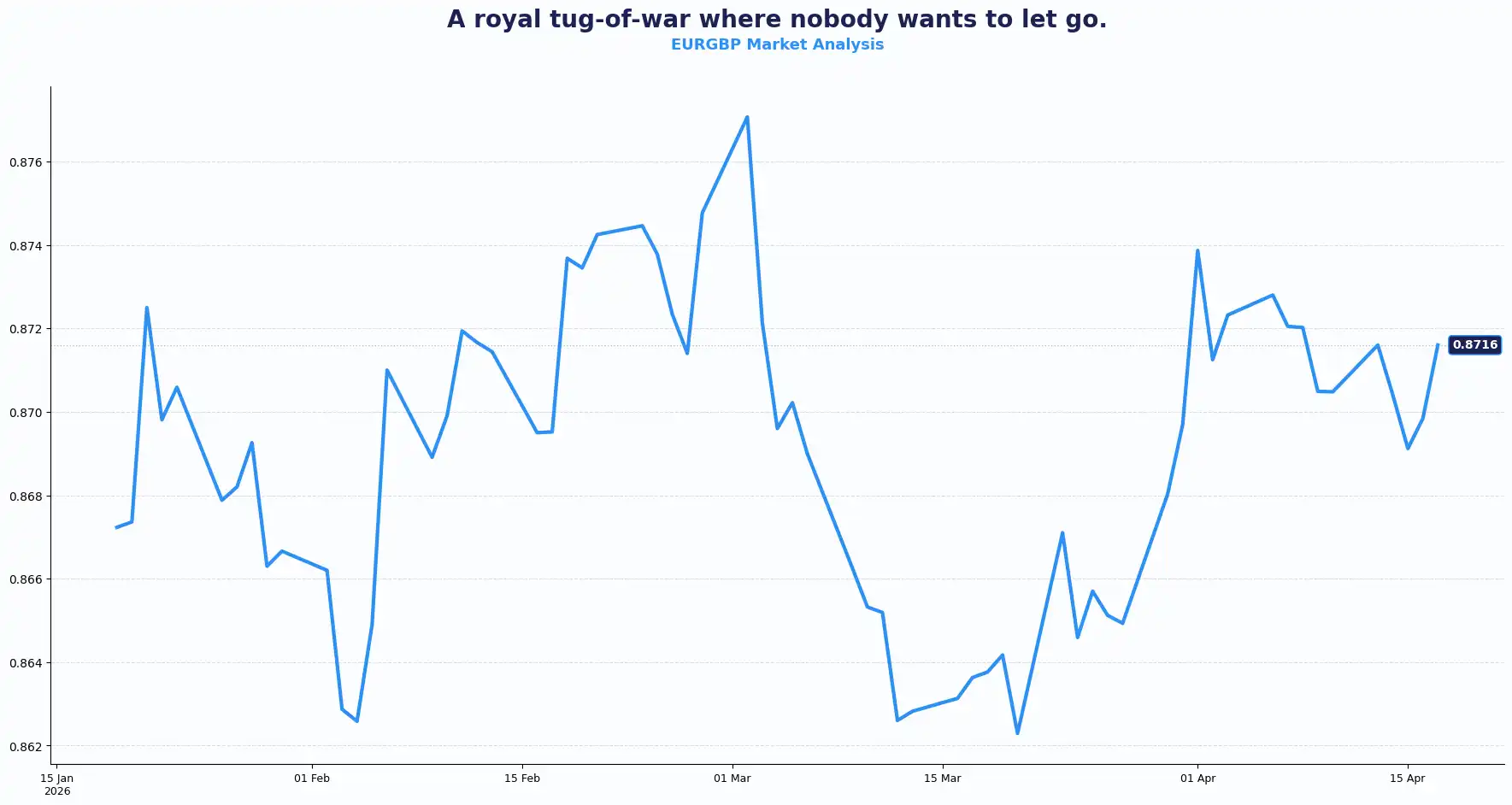

GBPUSD: 1.3521 | EURGBP: 0.8715 | GBPJPY: 215.63

Sterling fetched 1.3521 against the dollar on Friday, trading near its seven-week highs, having nearly recouped all the losses triggered by the US-Iran conflict in March. The EUR/GBP pair held near 0.8715, broadly rangebound across the Asia session as traders absorbed the week's noise ahead of the weekend.

The structural picture for sterling is one of carefully managed uncertainty. BoE’s Taylor laid out the tension plainly: the oil shock struck an already fragile economy, yet the labour market has not yet shown meaningful weakness in response. Taylor noted “3%” as his reading of the “neutral rate" and described a high bar to further rate hikes, framing the March vote to hold as a “pause” rather than a directional shift. He acknowledged BoE’s Andrew Bailey was correct to push back against the wave of multiple hike expectations priced in after the March MPC meeting.

The implication for sterling is nuanced. Two central bank governors who "paused" but signalled readiness to act if second-round inflation effects materialise produce a currency that is well-supported but not explosive to the upside. Price action shows a clear rejection of recent lows. Peace talks reduce the need for safe haven hoards.

GBP/JPY at 215.63 captures the risk-on bid well; sterling outperforms on the crosses when sentiment is constructive.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3600, 1.3700 and Support sits at 1.3420, 1.3400

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8780 and Support sits at 0.8650, 0.8600

EUR: The Continental Hesitation

EUR/USD: 1.1783

The euro held steady near 1.1783 against the dollar on Friday, hovering near seven-week highs as investors weighed a slightly higher inflation print against an ECB governing council that collectively pumped the brakes on near-term hike expectations.

Eurozone HICP for March printed 1.3% MoM versus a 1.2% consensus, lifting the year-on-year reading to 2.6% from 2.5%. Core HICP held at 0.8% MoM and 2.3% YoY, both in line with forecasts. The headline beat is marginal but directionally notable: supply-side pressure from elevated energy costs continues to filter through. Today's session also brings the eurozone's seasonally adjusted trade balance for February; a positive surplus reading would add a modest constructive layer to the euro's near-term technical picture.

ECB governing council members navigated carefully around the meeting-by-meeting question. Philip Lane declined to share scenario distribution thinking. Olli Rehn flagged that if inflation expectations deteriorate due to the conflict, the ECB stands ready to act "rapidly, forcefully." Isabel Schnabel described the eurozone as having shown resilience in the face of the recent shock.

The ECB minutes from the 18-19 March meeting, published this week, confirmed that the governing council agreed on the importance of standing ready to act and held to a broadly neutral stance, treating the unchanged rates decision in March as not diminishing readiness to move if required. Crucially, the minutes noted supply-side shocks "pose a dilemma for central banks" and that wages would need to catch up before second-round inflation effects take hold.

The conflict that erupted on 28 February with US-Israeli strikes on Iran forced the International Monetary Fund (IMF) to downgrade its global growth outlook and injected meaningful uncertainty into European corporate earnings visibility, from airlines to retailers. The Strait of Hormuz, through which a fifth of global oil and gas supply typically passes, is still largely shut. G7 finance ministers and central bank governors agreed this week to stay ready to act on economic and inflation risks posed by the energy shock.

The market's willingness to look through the conflict and energy shock in just two weeks has been striking. The contrast between what policymakers are flagging and what markets are implying looks complacent, and it seems unlikely that no additional risk premium should be priced in for growth or inflation. That gap between an ECB that is watchful but not yet moving and a market that has largely priced in equanimity is the central tension for EUR positioning going into the weekend.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1850, 1.1920 and Support sits at 1.1720, 1.1700

USD: The Greenback’s Descent on Peace Hopes

DXY: 98.21

The dollar index marked its eighth straight session of losses on Friday, trading near its lowest level since early March. The reversal closely mirrors geopolitical sentiment: the dollar surged as investors sought safe-haven cover at the outbreak of hostilities and has unwound those gains as ceasefire optimism built through April.

This week's catalyst was US and Iranian negotiators lowering ambitions for a comprehensive peace deal in favor of a temporary memorandum to avoid renewed conflict. President Trump announced on his socials that Israel and Lebanon agreed to a 10-day ceasefire, in effect since Thursday (yesterday). He also said the next US-Iran meeting might happen this weekend. The nuclear issue continues to act as the core obstacle to a fuller agreement.

Fed governor Miran's recent comments were notable; he sees three or four rate cuts as appropriate this year, but described the inflation scenario as "a little bit more problematic." He does not view the Iran conflict as materially shifting the inflation picture over the next 12 to 18 months. He flagged higher energy costs as a drag on growth and a risk, but held to a preference for forecast dependency over backward-looking data dependency, and said rates should now be neutral, not below. New York Fed President Williams maintained his view of GDP growth at 2%–2.5% for the year. Fed funds futures now price the Fed on hold this year, a sharp reversal from the two cuts priced in before the conflict began.

Thursday's US initial jobless claims printed below expectations, pointing to a resilient labour market and giving the Fed the latitude to hold while monitoring the inflation pass-through from elevated energy costs. US Treasury yields held steady on Friday after rising in the previous session, with oil prices still above pre-conflict levels, keeping the inflation concern alive. Brent dropped to 98.14 USD per barrel; WTI fell 1.6% to 93.15 USD per barrel, and both benchmarks held below 100 USD.

US equities stormed back to record highs from the March selloff. The consensus view is that solid earnings have supported the rally, but with the Strait of Hormuz still effectively shut, any reversal in ceasefire progress could produce rapid corrections. A full reopening of the Strait is the catalyst that makes the risk-on trade structurally sound. Until then, the move is largely a hope trade.

The dollar's path is no longer one-way. As safe-haven demand fades with negotiations for a temporary memorandum, the dollar awaits its next catalyst for a clear move.

Global flow: other currencies and the commodity bloc

AUD/USD: 0.7169 | NZD/USD: 0.5888 | USD/JPY: 159.48

The yen hovered near 159.40–159.48 per dollar on Friday, once again approaching the 160 level that prompted intervention concerns in prior episodes. BOJ Governor Kazuo Ueda steered clear of signalling a rate hike at the 27-28 April policy meeting, and that lack of clarity pushed markets to trim bets on a near-term move. The yen's immediate intervention risk looks less acute than in previous rounds. The safe-haven bid that compresses USD/JPY in periods of acute stress is less forceful given calmer geopolitical conditions this week.

Asian currencies broadly drifted; the Indonesian rupiah, Philippine peso, and Thai baht fell 0.26%, 0.22%, and 0.18% respectively, while the South Korean won and Hong Kong dollar edged lower.

The commodity-linked currencies told a different story. The Aussie dollar at 0.7163-0.7169 hovered near a four-year high, with Thursday's touch at the top end representing one of the more significant technical prints of the week. The kiwi near 0.5888 pulled back fractionally. The Norwegian krone, Canadian dollar, AUD, and NZD are seen as gaining ground in an environment where rising global commodity prices are reshaping geopolitics and supporting their export-driven economies, even as higher energy costs weigh on growth in other countries.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3521 | Range-high |

| EURGBP | 0.8715 | Sideways |

| EURUSD | 1.1783 | Range-high |

| USDJPY | 159.48 | Uptrend |

| GBPJPY | 215.63 | Uptrend |

| AUDUSD | 0.7169 | Strong bid |

| NZDUSD | 0.5888 | Steady |

(as at the time of writing)

Market Lookahead

Mon, 20 April

- Germany PPI (March)

Tue, 21 April

- UK Average Earnings (Feb, 3M/YR)

- UK Claimant Count (March)

- UK Employment Change (3M Feb)

- UK ILO Unemployment Rate (3M Feb)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.