Hormuz Open. Hormuz Shut. Repeat. FX Trades the Strait.

8 min read

Share

The Strait swings open and shut. Oil jumps, the dollar steadies on the safe-haven bid, and cable holds 1.3500 as sterling faces geopolitical friction and a domestic political storm. A week of key data across GBP, EUR, and USD is about to test every level.

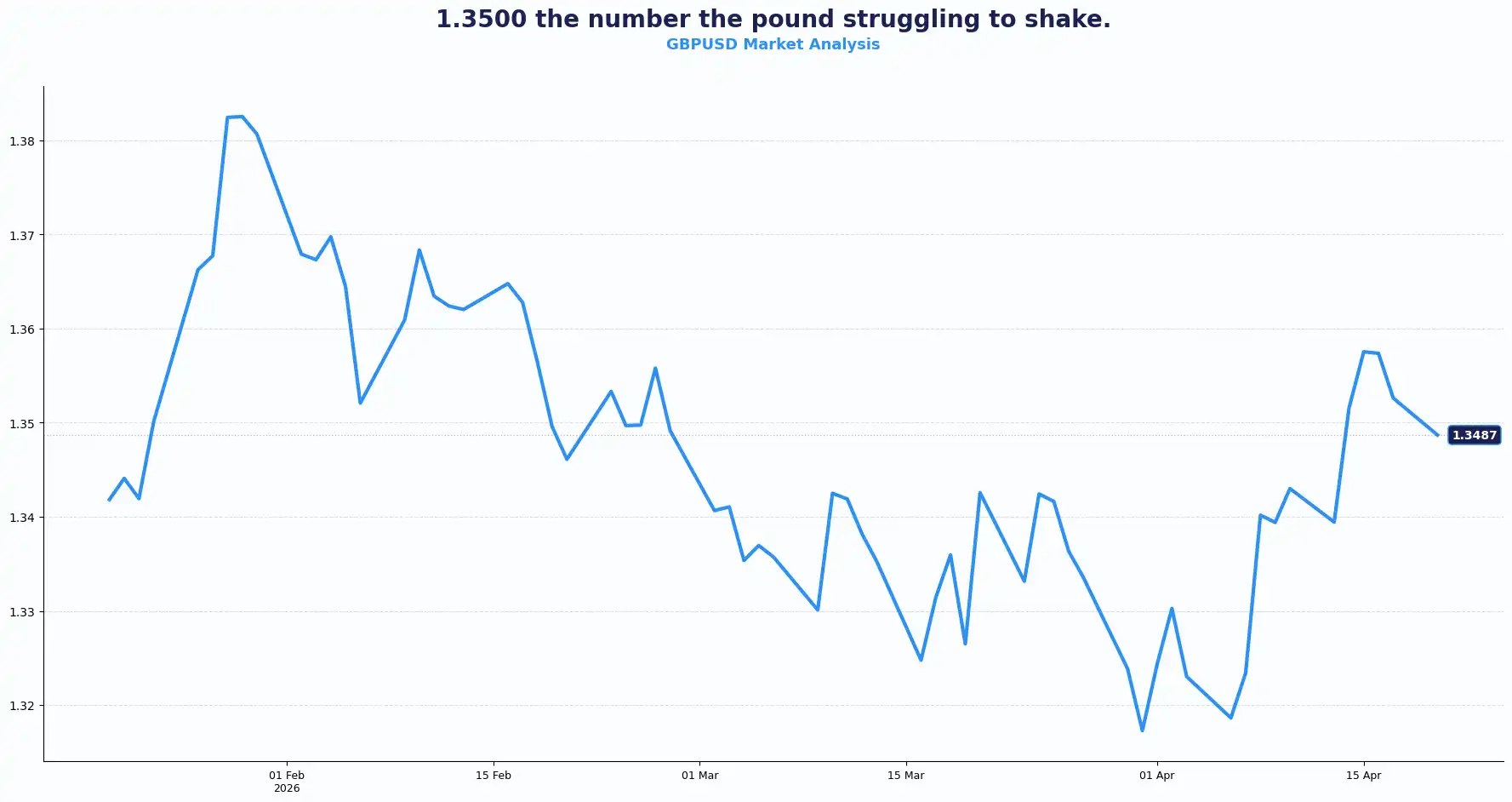

GBP: Pressure Builds Near 1.35

GBPUSD 1.3495 | EURGBP 0.8710

Sterling softened into the 1.3500 handle, as the Strait of Hormuz shut again over the weekend. Safe-haven flows drove demand for the dollar, and cable took the brunt.

For the investors, geopolitical friction fuels a flight to safety. Shipping in the Gulf slowed to a crawl after Iran de facto closed the Strait of Hormuz. Although data confirms twenty vessels transited the chokepoint on Saturday; the seizure of an Iranian cargo ship by U.S. forces cast shadows over Tuesday’s ceasefire deadline. Oil prices jumped over 5% on the news, introducing a volatile variable for UK inflation. Brent crude futures rose to $95.2 a barrel and WTI climbed to $88.99.

The standoff creates a complex backdrop for the Bank of England (BoE). While Sarah Breeden warns that "vulnerabilities from past crises have not disappeared," the surge in energy costs could reignite domestic inflation. This divergence between geopolitical risk and sticky inflation may force the BoE to maintain a more hawkish stance than peers, even as economic growth currently stays fragile. The hawkish framing offers the pound some fundamental support even as short-term sentiment sours.

The domestic political picture complicates things further. UK Prime Minister Keir Starmer faces calls for resignation in Parliament on Monday over the handling of Peter Mandelson's appointment as US ambassador. Mandelson's known ties to convicted sex offender Jeffrey Epstein cost him his position last September. Historically, political noise of this nature does not tend to shift cable in a sustained way, but it could reduce investors' appetite for any fresh sterling positioning ahead of this week's data.

Investors are now looking ahead to Tuesday’s UK labour market figures. Consensus expects Avg. Earnings at 3.5% (excl. bonus) and 3.6% (incl. bonus) for February, on a three-month annualised basis. The Claimant count for March is expected to rise to 21,400, against a prior 24,700, a modest improvement. The ILO unemployment rate for the three months to February is expected to hold at 5.2%. A beat on “Earnings data” keeps BoE rate expectations supported; a miss and the pound might lose its structural argument fast.

Volatility clusters around macro risk and energy prices. As political pressure mounts on Prime Minister Keir Starmer regarding diplomatic appointments, domestic policy uncertainty may amplify currency swings. Sterling reflects both global risk tone and domestic pressure points.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3550, 1.3600 and Support sits at 1.3450, 1.3400

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8750, 0.8780 and Support sits at 0.8680, 0.8650

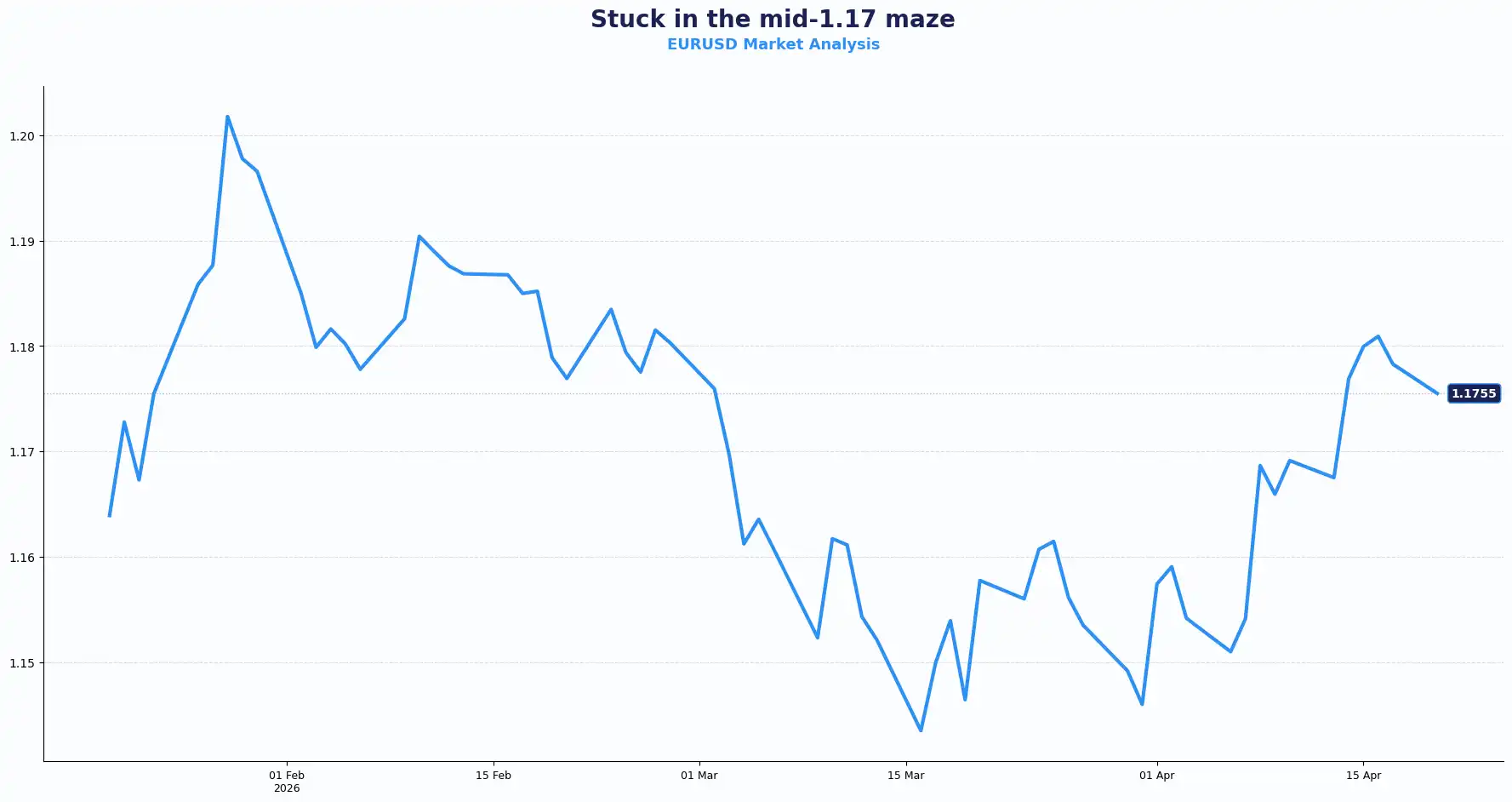

EUR: German PPI Surprises Amidst Diplomatic Doubt

EURUSD 1.1754

The euro drifted lower, trading just above the mid-1.1700s and maintaining a bearish bias as it trades below its 100-hour SMA. The pair found no obvious catalyst to reclaim lost ground, and thin volume on Monday left sentiment doing most of the driving.

European allies express growing concern that the U.S. negotiating team lacks the experience to secure a lasting agreement with Tehran. French and German bond futures fell as the market digested the prospect of a prolonged U.S.-Iran standoff, reversing Friday's rally as the initial ceasefire optimism unwound.

Germany’s PPI for March was released this morning, significantly beating expectations, coming in at 2.5% MoM, above the lower consensus. A 2.5% PPI reading is a loud signal for commodity inflation, which typically supports the euro by suggesting future interest rate hikes. However, the dollar's safe-haven allure currently caps any meaningful euro recovery. The ZEW Survey due tomorrow will provide the next litmus test for institutional sentiment across the Eurozone. April's reading will be the first to fully capture market sentiment post the Hormuz re-closure and renewed US-Iran tensions. A significant miss could accelerate the euro's retreat from the 1.18 handle.

The structural drag on the EUR/USD pair is the Fed divergence story. Diminishing expectations for a US Federal Reserve (Fed) rate cut support the dollar, and that dynamic caps rallies for the pair. Geopolitical risk adds a secondary headwind. The Hormuz standoff stokes risk aversion, and the dollar benefits more from safe-haven demand than the euro does.

The euro sits between softer inflation signals and external risk. Investors are watching EU sentiment data and Fed expectations for direction, with the near-term upside looking limited while geopolitical risk stays active.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1800, 1.1850 and Support sits at 1.1700, 1.1650

USD: Dollar Steadies as Risk Resets

DXY 98.33 | USDCAD 1.3702

The dollar steadied on Monday after selling off for the best part of a fortnight. The DXY sits at 98.33, down 1.5% through April on the back of rising hopes for a US-Iran peace deal. The index had rallied 2.3% in March when the conflict first broke out.

The weekend brought two developments that revived demand for havens. First, the Strait of Hormuz was opened for roughly 12 hours on Saturday, then closed again. Second, Iran confirmed it would not attend a second round of negotiations the US had hoped to convene before Tuesday's ceasefire expiry. The US seized an Iranian cargo ship over the weekend; Tehran's military command has vowed to retaliate. The market's reaction to all of this is cautiously orderly, yet currency moves remained measured relative to the oil shock. The interpretation holding sway is that both sides retain a commercial interest in reaching a deal and that the path to any agreement was never going to be linear.

The "higher-for-longer" narrative gained fresh legs as persistent inflation and Middle East tensions forced a rethink of the Fed's timing, with a diminishing prospect of near-term rate cuts. The dollar acts as the primary beneficiary of global anxiety.

Tuesday's US retail sales for March are the next key domestic data point. Consensus expects a 1.3% MoM rise, up from 0.6% in February. ADP's four-week employment average is also due Tuesday. A strong retail sales print could reinforce the Fed's patience and give the dollar a fresh floor.

The 10-year Treasury yield edged 2.2 basis points higher to 4.266% on Monday as bonds gave back Friday's ceasefire-driven rally. Analyst positioning data shows investors still hold a net short dollar bias, meaning the currency has further room to drop if the Middle East situation normalises materially. For now though, the noise keeps that trade on hold.

Canadian Prime Minister Mark Carney stated publicly that the close ties with the United States that were once a strength have become a weakness - a diplomatic signal of how far the geopolitical fracture has extended beyond the Middle East. The USD/CAD pair holds at 1.3702, with the loonie capped by both risk aversion and the broader dollar stabilisation.

Other Currencies: Mixed Moves Under Pressure

AUDUSD 0.7151 | NZDUSD 0.5874 | USDJPY 158.95 | GBPJPY 214.51

The yen weakened to 158.95 per dollar on Monday, nudging toward the 160.00 level that traders associate with potential intervention by Japanese authorities. The Bank of Japan holds its policy meeting later this month. Governor Kazuo Ueda declined to pre-commit to an April rate hike amid the uncertainty introduced by the war, but left hawkish signals at last week's IMF meetings, suggesting tighter policy could arrive by June. For now, 160.00 acts as the line in the sand.

The Aussie dollar fell 0.3% to 0.7151. The move reflects both the risk-off tone and a company-specific jolt: National Australia Bank (NAB), Australia's largest business lender, flagged a $500 million impairment charge, citing expectations that the war will drive up bad debts. NAB shares fell 3.6%. That kind of domestic financial stress amplifies risk aversion already present in the broader FX market.

The New Zealand dollar drifted to 0.5874, relatively contained given the backdrop.

In crypto, both Bitcoin and Ether declined on Monday. Historically sought after as alternatives to traditional haven assets, both fell in a session where the dollar and oil captured the safe-haven and risk premium simultaneously, leaving less room for digital assets.

As the "barometer of risk" distils into the number of ships passing through Hormuz, global supply chains remain sensitive. Assessing the impact of energy costs on currency pairs has become essential for navigating the current macro environment.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3495 | Bearish below 1.3550 |

| EURUSD | 1.1754 | Bearish below 1.1800 |

| EURGBP | 0.8710 | Bullish above 0.8680 |

| USDJPY | 158.95 | Bullish near intervention zone |

| USDCAD | 1.3702 | Range-bound with upside bias |

| AUDUSD | 0.7151 | Bearish under 0.7200 |

| NZDUSD | 0.5874 | Bearish under 0.5900 |

| GBPJPY | 214.51 | Bullish but stretched |

(as at the time of writing)

Market Lookahead

Mon, 20 April

- UK: Prime Minister Keir Starmer addresses Parliament

- Geopolitics: Monitoring U.S.-Iran negotiations as the ceasefire deadline approaches

Tue, 21 April

- UK: Unemployment Rate (Feb), Average Earnings Index

- Eurozone: ZEW Survey Economic Sentiment

- USA: Retail Sales (Mar)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.