A Beat for Sterling. A Warsh Day for the Dollar.

7 min read

Share

UK employment data defied expectations this morning. Unemployment rate dropped to 4.9% against a consensus of 5.2%, sparking a shift in BoE rate bets. Meanwhile, Washington and Tehran are pulling focus: Iran's ceasefire frays at the edges as Warsh steps into the Senate for the Fed's most consequential confirmation hearing in years. The kiwi quietly stole a beat of its own on sticky CPI. UK CPI lands tomorrow.

GBP: Sterling Bids Return on Cooling UK Jobless Rate

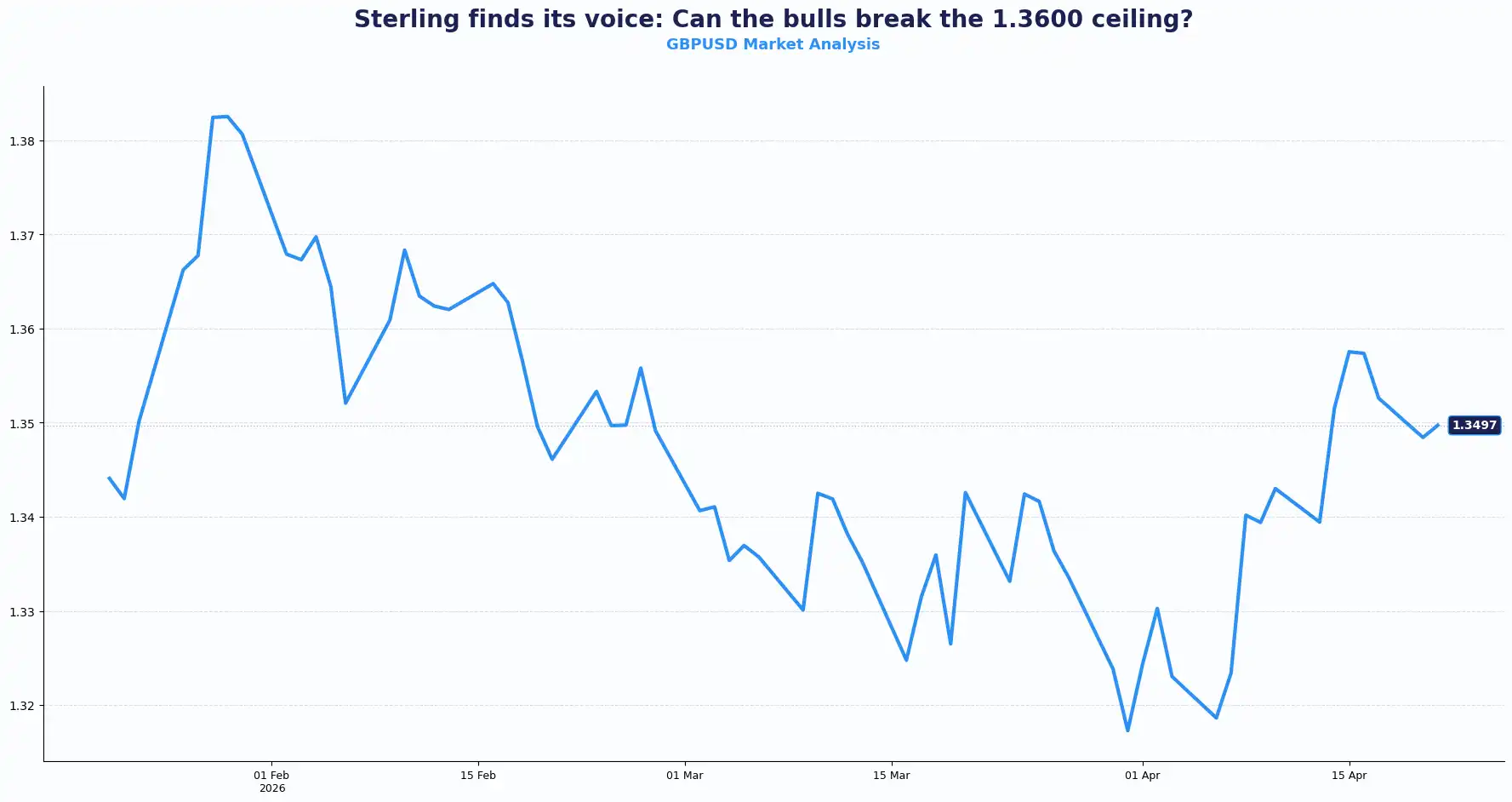

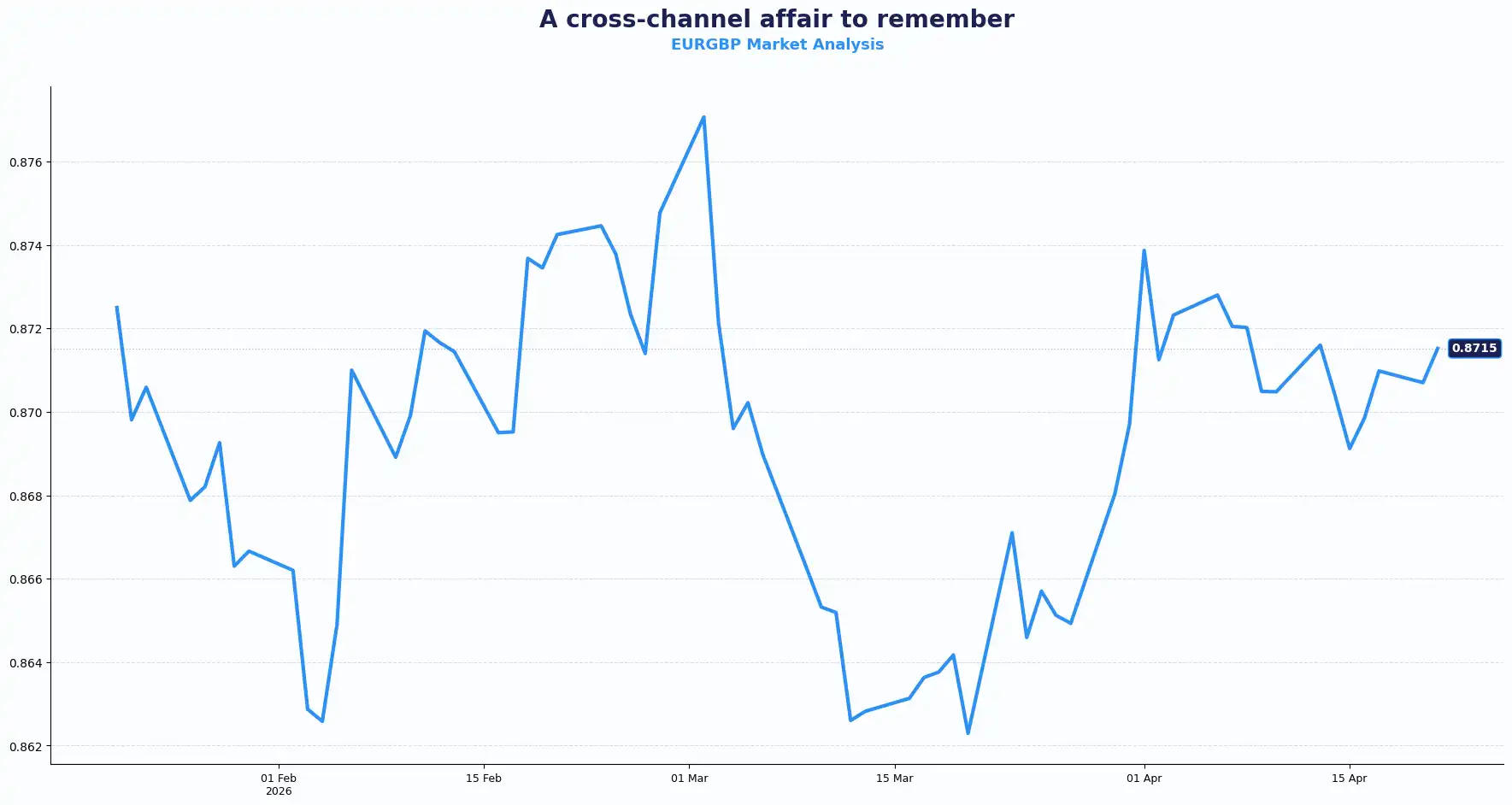

GBPUSD 1.3525 | EURGBP 0.8710

Sterling softened in Asian trading and held that dip into the European open, but the UK labour data released this morning shifts the picture considerably.

The UK ILO unemployment rate was 4.9% (vs. 5.2% expected/prior), a strong beat. Employment change rose to 4.4% from 4.3%. The broadest measure of Britain’s labour market arrived firmer than anyone expected, and sterling attracted bids almost immediately on the release.

The case for sterling is not unambiguous, though. Average earnings, including bonus, came in at 3.8%, beating the consensus of 3.6%; wages are still running hot, which the Bank of England (BoE) cannot ignore. Avg. earnings excluding bonus printed at 3.6%, just above the 3.5% consensus. Higher wages slow the pace at which the BoE can consider cuts. That is structurally supportive for the pound.

On the other hand, the complication is the claimant count. March’s figure came in at 26.8k, well above the 21.4k consensus and above the prior 24.7k. A claimant count this elevated signals a deteriorating segment of the labour picture and typically leans GBP-bearish. It lands in direct tension with the unemployment beat. The net read: a resilient headline labour market, but stress building at the margins. Together, these data points give the BoE room to leave rates unchanged at its 30 April meeting. The lower jobless rate in particular supports that view.

All eyes now turn to Wednesday’s CPI release for March. Headline inflation is forecast to accelerate to 3.3% YoY from 3.0% in February, driven partly by higher energy prices. Core CPI consensus sits at 3.2% YoY, unchanged from prior. A hotter-than-expected CPI print would push back rate-cut expectations further and add genuine support to sterling; a miss, by contrast, would reopen the cut debate.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3600 and Support sits at 1.3450; Bias range-bound with upside pressure

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8750 and Support sits at 0.8650; Neutral bias

EUR: Sentiment Check Before the Blackout

EURUSD 1.1781

The euro softened in Asian trading. European equity futures pointed to a firmer open, pan-region futures up 0.3%, German DAX up 0.3%, and FTSE futures up 0.2%.

Today’s data focus is the ZEW Survey: Germany’s Current Situation and Economic Sentiment readings for Germany and the eurozone, all for April. The ZEW measures the gap between optimism and pessimism among institutional investors. A positive reading usually favours the euro and signals improving forward expectations for the economy.

March business surveys proved more resilient than feared. The question is whether April data holds that tone or whether escalating geopolitical risk has started to bite into confidence.

This is the last window of meaningful ECB commentary before the blackout period kicks in on Thursday. ECB speakers have been consistent in their message: the bank stands ready to act if required, but more data is needed. The market has already priced out a 30 April hike and now places roughly a 50% probability on a June hike. President Lagarde also speaks tomorrow, alongside eurozone consumer confidence for April; both events may either cement or soften that pricing.

Euro outlook hinges on rate expectations, incoming data, and ECB action ahead of clear evidence. Any hawkish surprise from ZEW today or Lagarde tomorrow could quickly push EUR/USD toward resistance.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1850 and Support sits at 1.1720; Bias - soft near-term

USD: Iran Talks, Intervention, and the Warsh Question

DXY 98.10

The dollar reversed earlier gains on Monday and finished the session with moderate losses. The US stock market closed in the red, while the Nasdaq snapped a 13-day winning streak, its longest since January 1992.

Two forces act simultaneously and cut in opposite directions.

The Iran situation. A ceasefire between the US and Iran has frayed. The US announced the seizure of an Iranian cargo ship; Tehran responded with vows of retaliation and initially said it would skip a second round of negotiations, though a senior official later indicated the country may yet send delegates to talks expected in Islamabad.

President Trump's comments that negotiations are progressing "relatively quickly" and are on track to yield better terms than previous agreements have kept sentiment from deteriorating sharply. Oil prices fell on those expectations, with Brent Crude settling near $95 per barrel on the prospect of talks reopening Gulf shipping through the Strait of Hormuz. Investors are cautiously hopeful but watching the ceasefire clock closely.

With peace talks uncertain, investors' attention has pivoted back to AI-linked equities, expecting growth to reassert itself. The overriding mood is wait-and-see.

The Warsh hearing. Kevin Warsh, Trump's nominee to lead the Federal Reserve, begins his confirmation hearing before the Senate Banking Committee today at 10am EDT (2pm GMT). His prepared remarks confirm he is "committed to ensuring that the conduct of monetary policy remains strictly independent," a direct response to sustained White House pressure on the Fed to cut rates faster.

Warsh has a well-known track record as a vocal critic of the Fed's balance sheet, which he has described as "bloated" and distortionary of asset prices. Any indication of how he defines the optimal balance sheet size will be watched closely. The tension between Warsh's stated independence and the administration's public stance on rates makes this hearing a genuine market event rather than procedural theatre.

Also landing today is the ADP Employment Change (four-week average) and March Retail Sales, with analysts forecasting a 1.4% MoM increase in the latter. A strong retail sales print could offer the dollar some structural support from the data side, even as Warsh and Iran dominate the headlines.

The dollar's structural position is caught in a longer-running debate. Escalating geopolitical risk in the Gulf has prompted senior Emirati officials to explore emergency liquidity options in dollars, including discussions with the US Treasury. Separately, Iran has continued oil exports to China outside the dollar system, with arrangements linked to yuan-denominated payments. These are not policy shifts yet, but they reflect a growing reassessment of dollar-denominated energy trade arrangements that have been in place for decades.

The dollar retains its structural dominance through deep, liquid financial markets, a robust legal framework, and full currency convertibility. Alternative currencies carry their own limitations: the yuan faces capital controls; the euro lacks unified fiscal backing. Reserve currency transitions unfold over decades, not quarters. However, the breadth of actors now exploring alternatives simultaneously and the infrastructure beginning to support those moves warrants attention.

Other Currencies: Kiwi Rises on Inflation

AUDUSD 0.7171 | NZDUSD 0.5914 | USDJPY 158.89 | GBPJPY 214.90 | GBPNZD 2.2866

The risk-sensitive Aussie dollar weakened to $0.7171 amid geopolitical uncertainty and a softer broader risk tone, weighing on commodity-linked currencies.

The Kiwi dollar gained ground, trading near $0.5914, after New Zealand's Q1 CPI held at 3.1% annually, above the Reserve Bank of New Zealand's (RBNZ) target range and above consensus. A sticky inflation print lifts the probability of further RBNZ rate hikes this year. The kiwi has a clear fundamental driver today where most others do not.

USD/JPY held steady at 158.89, hovering just below the 160 level that currency traders widely regard as the threshold for potential Bank of Japan (BoJ) intervention. BoJ is likely to hold rates at next week's meeting, with fading prospects of a near-term resolution to the Middle East conflict keeping Japan's economic and price outlook uncertain; this policy expectation supports continued USD/JPY elevation.

Divergence across central banks and inflation paths often leads to wider dispersion in currency performance and relative value moves.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3525 | Range / Bid |

| EURUSD | 1.1781 | Soft / Drift |

| EURGBP | 0.8710 | Stable |

| USDJPY | 158.89 | Uptrend |

| AUDUSD | 0.7171 | Soft |

| NZDUSD | 0.5914 | Firm |

| GBPNZD | 2.2866 | Supported uptrend |

| GBPJPY | 214.90 | Elevated |

(as at the time of writing)

Market Lookahead

Tue, 21 April

- Warsh Senate confirmation hearing

- US Retail Sales (March)

- ADP Employment change

- ZEW Germany + Eurozone Sentiment (April)

Wed, 22 April

- UK CPI (March), UK PPI & Retail Price Index (March)

- Eurozone Consumer Confidence (April)

- ECB Speeches

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.