Central Banks Cornered, PMIs Due, Oil at $100

6 min read

Share

Hormuz stays shut, two ships seized, oil above $100 and PMIs drop across all major blocs today. Sterling soft, euro slips, dollar firms. The energy shock puts central banks across the UK, eurozone and US under fresh pressure to rethink the rate cut timeline.

GBP: Sterling Weathers the Storm

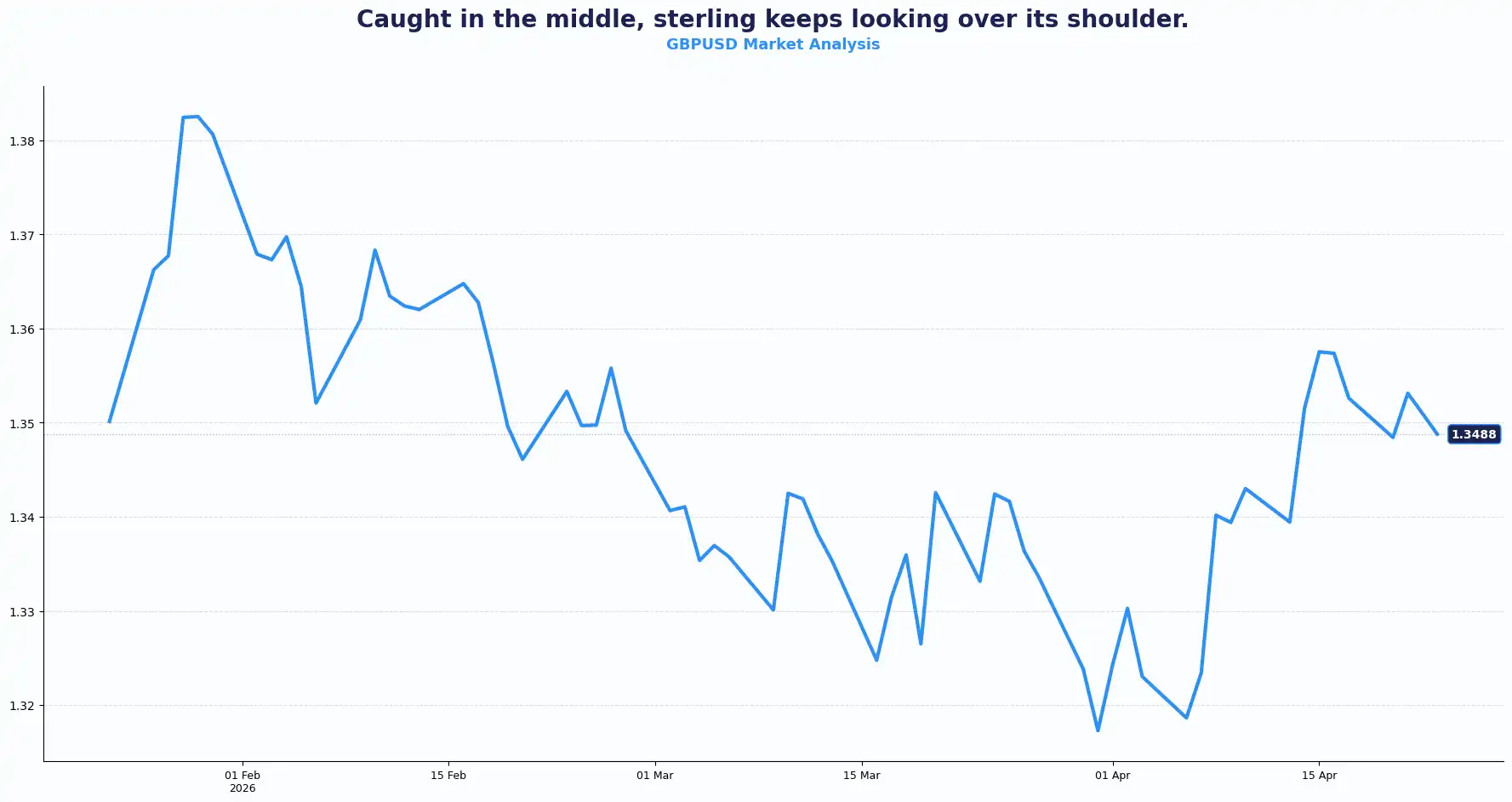

GBPUSD: 1.3491

Cable sits at 1.3491, down on the session, as the ceasefire extension between the US and Iran failed to deliver a roadmap for peace. This geopolitical deadlock keeps the Strait of Hormuz effectively closed. The resulting energy shock ripples through the British economy, leaving the currency vulnerable. High energy costs are now driving inflation forecasts higher, forcing money markets to price in at least one Bank of England (BoE) rate hike this year.

The BoE confronts a genuine dilemma. While 90% of the market expects a rate hold this month, the persistent price pressures suggest the "higher for longer" narrative has fresh legs. Households, now accustomed to high prices, may demand higher wages to restore their purchasing power. However, a weakening labour market and falling vacancies could weigh on consumption. The BoE must now decide which of these risks poses the greater threat to stability.

Today's S&P Global PMIs - composite, manufacturing, and services for April- are the first hard read on how the energy shock filters into British business activity. Tomorrow, GfK consumer confidence for April and retail sales for March will add further insights. A miss on either print could sharpen sterling volatility. Popping the champagne requires two free hands; right now, one is firmly on the shoulder.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3550 and Support sits at 1.3400;

EUR: Euro Holds Ground but Loses Momentum

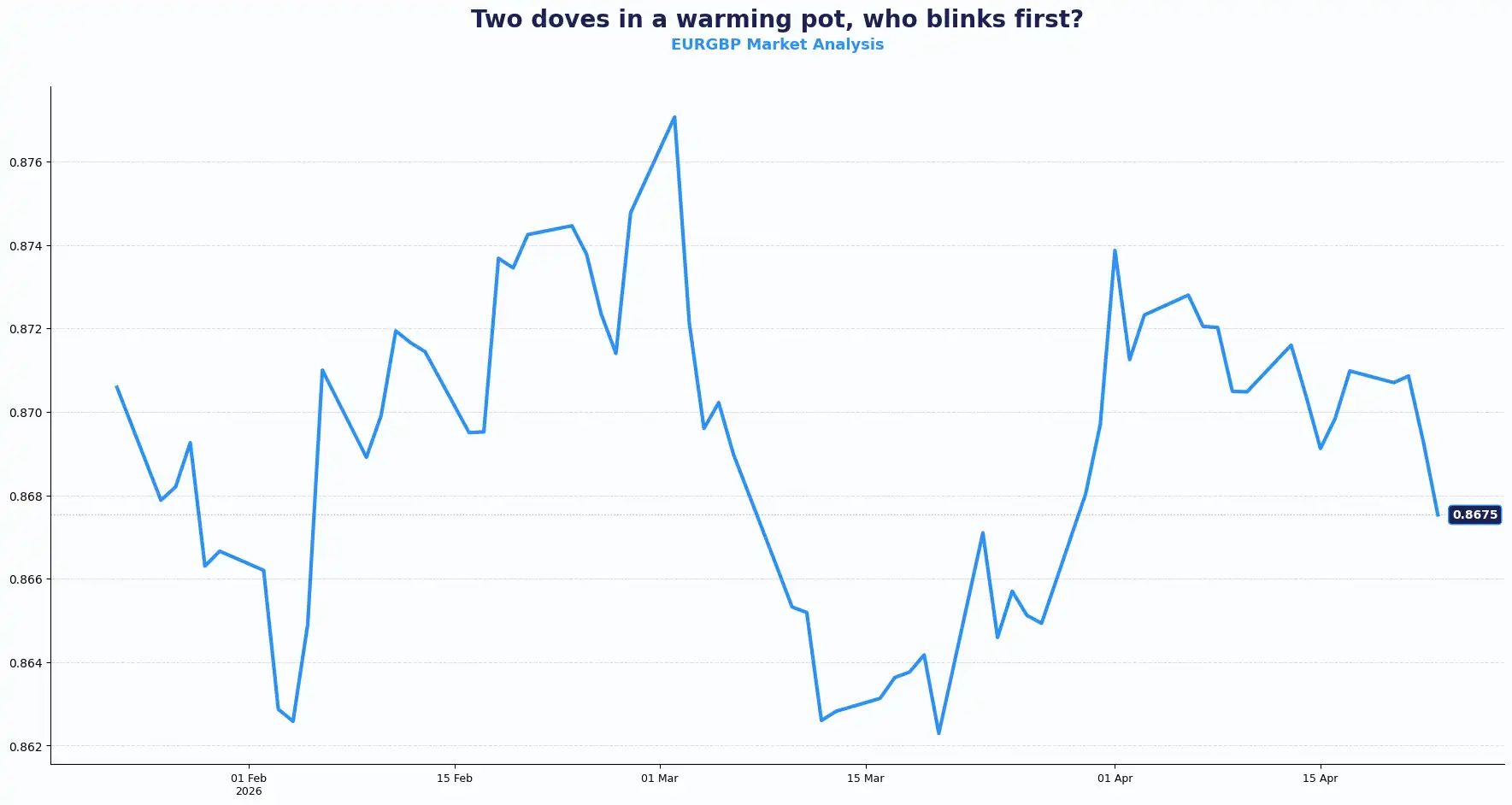

EURGBP: 0.8675 | EURUSD: 1.1704

The EUR/GBP pair is trading modestly higher at 0.8675 in early European trading. Hot UK inflation data acts as a ceiling; any sterling softness is limited by the expectation that the BoE will respond to inflation by tightening monetary policy more aggressively than the European Central Bank (ECB).

ECB officials like Gediminas Simkus suggest an April rate hike is unlikely, but tightening later this year remains possible. Analysts see 25bp hikes in June and September as live ECB scenarios, driven by the same energy-inflation dynamic affecting the BoE. With both central banks on hold near-term but facing upward inflation pressure, the cross trades on nuance , specifically, which institution blinks first on forward guidance.

Flash PMI readings from both the eurozone and the UK today will be the cross's primary driver. Traders are watching for the services print, where the energy-cost pass-through typically shows up first in the survey data. The EUR/GBP pair has limited room to extend gains while UK inflation data stays elevated.

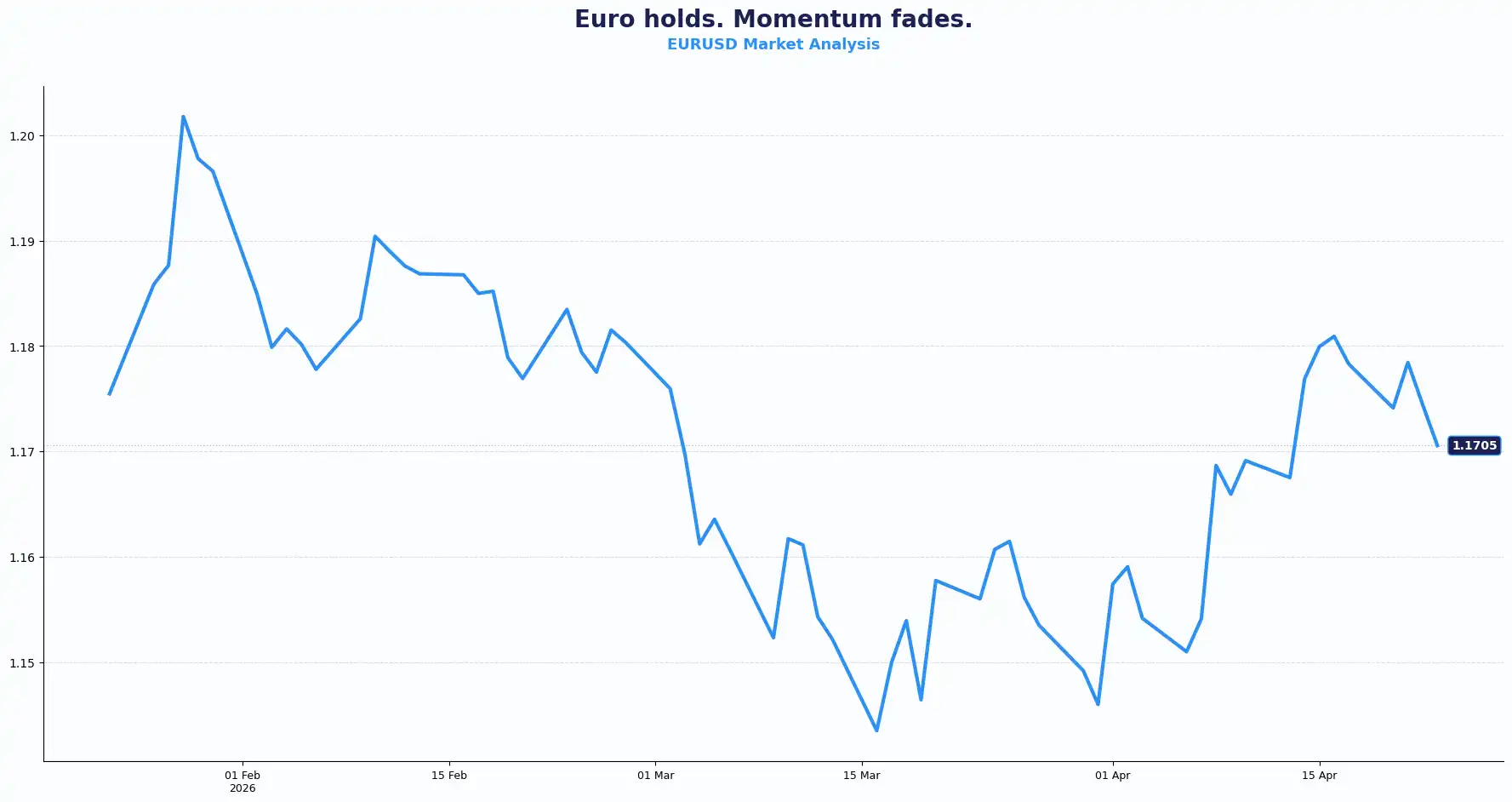

Turning to EUR/USD, the pair held gains above 1.1700 following the US-Iran news, yet it still eyes a 0.5% weekly decline, its first drop in a month. This stagnation reflects a darkening outlook for the bloc. The pair tracks an extended ceasefire with Iran that yields no sign of peace talks restarting, keeping energy prices elevated and the growth outlook under pressure.

Germany’s economy ministry recently cut growth forecasts for 2026 and 2027 while simultaneously raising inflation projections, a combination that narrows the ECB's room to pivot. This "stagflation lite" environment weighs heavily on sentiment, especially as governments sound the alarm over soaring energy costs.

European equities fall for a third straight session. Meanwhile, corporate earnings strike a cautious tone: consumer goods, travel, and mining firms all warn that the Middle East conflict is driving up input costs, disrupting supply chains, and damaging consumer confidence.

Today's HCOB flash PMIs, manufacturing, composite, and services for April ,give the first post-shock activity read for the eurozone. Tomorrow brings Germany's Ifo business climate and expectations for April. A deterioration in either print would reinforce the growth-versus-inflation bind the ECB already navigates. The single currency's hold above 1.1700 is notable given the backdrop.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8720 and Support sits at 0.8620;

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1750 and Support sits at 1.1650;

USD: Safe-Haven Bid Holds, Rate Cut Hopes Fade

DXY: 98.65

The dollar index (DXY) holds firm near 98.65, supported by intense safe-haven demand. The index eyes a 0.5% gain this week, reversing a two-week losing streak. As peace talks stall and oil prices surge back above $100 per barrel, the Federal Reserve (Fed) now looks likely to delay any planned rate cuts. The energy shock has reignited inflation, effectively wiping out previous market pricing for policy easing this year.

Tehran’s seizure of two ships in the Strait of Hormuz on Wednesday reminded the world of the fragility of global trade. While the dollar saw a brief risk-on sell-off earlier this month, the return of geopolitical tension has restored its dominance. Whether financial markets are correctly pricing the likelihood that supply constraints persist is a question the dollar's stability will answer over the coming weeks. Investors find it difficult to embrace risk while a vital waterway remains blocked.

US weekly initial jobless claims and April PMIs print today. Both give clues on whether elevated energy costs filter through to the broader economy. The S&P 500 and the Nasdaq close at record highs despite the backdrop - corporate fundamentals, and consumer spending hold firm for now. Investors price in Hormuz reopening before lasting economic damage takes place. That assumption is tested each time Tehran acts in the Strait. The balance between resilience and risk defines near-term direction.

Global Ripple Effects

AUDUSD 0.7153 | NZDUSD 0.5888 | USDJPY 159.53 | GBPJPY 215.24

The Aussie dollar and Kiwi dollar both weakened as risk appetite evaporated. Meanwhile, the yen remained subdued near the 160 level, a clear line in the sand for Japanese authorities. Although Asian stocks tracked Wall Street higher on Thursday, the underlying anxiety regarding oil remains palpable. The Bank of Japan expects to keep rates steady next week, though a June hike remains a distinct possibility.

Against this backdrop, oil’s jump, even without a singular trigger, points to how sensitive positioning remains to geopolitical tail risk across the Asia-Pacific complex.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3491 | Soft |

| EUR/USD | 1.1704 | Holding |

| EUR/GBP | 0.8675 | Range-bound |

| AUD/USD | 0.7153 | Weak |

| NZD/USD | 0.5888 | Weak |

| USD/JPY | 159.53 | Elevated |

| GBP/JPY | 215.24 | Elevated |

| DXY | 98.64 | Firm |

Market Lookahead

Thu, 23 April

- UK S&P Global PMIs: Composite, Manufacturing, Services (April)

- Eurozone HCOB PMIs: Composite, Manufacturing, Services (April)

- US weekly initial jobless claims

- US S&P Global PMIs: Composite, Manufacturing, Services (April)

Fri, 24 April

- UK: GfK consumer confidence (April)

- UK retail sales (March)

- Germany IFO business climate & expectations (April)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.