No Deal, No Growth: US-Iran Standoff, Weak PMIs Drag GBP and EUR

8 min read

Share

A rare cocktail of Middle East conflict, a Fed transition, and stalling European growth. Weak UK and eurozone PMIs drag GBP and EUR. The dollar holds near a six-week high on stronger US data.

GBP: Contraction Meets a Cautious BoE

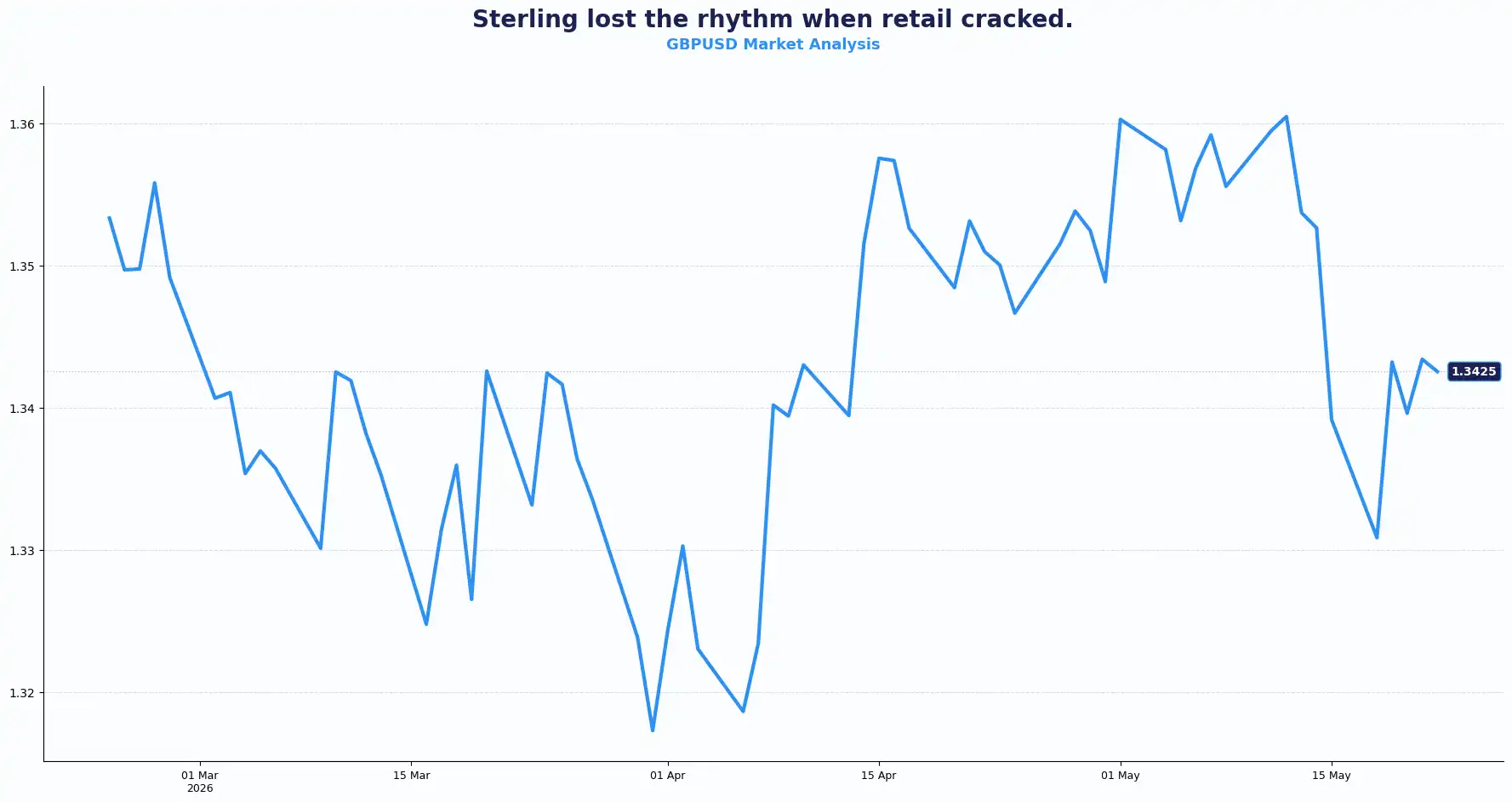

GBPUSD 1.3425 | EURGBP 0.8647

Sterling drifted lower after a sharp deterioration in UK retail activity, and softer PMI readings challenged the Bank of England’s (BoE) tightening narrative. The GBP/USD pair hovered near 1.3425 after slipping below the 1.3450 handle.

UK retail sales for April fell 1.3% MoM, below the consensus of −0.6% and the prior reading of +0.7%. YoY sales came in flat at 0.0% against a forecast of +1.3%. Excluding fuel, April retail sales printed −0.4% MoM and +1.1% YoY. The miss was broad and hard to dismiss.

Despite the weak print, sterling is on track to gain 0.8% for the week, a partial recovery from last week's 2% sell-off driven by political turmoil.

The GfK Consumer Confidence Index for May landed at −23, beating a consensus of −28 and an April reading of −25, which itself had been the lowest since October 2023. GfK's Neil Bellamy flagged the uptick as unlikely to mark a sustained recovery. His read is that one month's relief does not make a trend.

The UK S&P Global PMIs for May told a sharper story. Manufacturing held at 53.7, in line with the prior period, but the composite collapsed to 48.5 from 52.6, and services fell to 47.9 from 52.7. Both composite and services dropped into contraction territory. British companies are reporting their most widespread drop in activity in over a year. A PMI below 50 signals declining activity, and the services sector is where the UK economy lives, so this matters.

This toxic combination of negative economic growth and persistent price pressures paralyses the Bank of England. The escalation of the US-Iran conflict has triggered a severe energy shock, driving input costs up and forcing a stark policy divergence.

BoE MPC Member Alan Taylor noted that the system has sufficient restrictiveness to cap inflation, viewing current interest rates as roughly 100 bps above the neutral level and approximately 50 bps above where he would have preferred in the absence of the Iran war. He acknowledged that under adverse scenarios, some hiking could be required, though he assessed second-round inflationary effects as less likely than in 2022. BoE Governor Andrew Bailey also spoke, delivering prepared remarks at the Cutler's Feast, but made no reference to current monetary policy and moved no needles.

However, the unexpected rise in the unemployment rate to 5.0% complicates matters. The central bank cannot easily raise rates to fight energy-driven inflation without worsening a deeper recession, yet it cannot cut rates while geopolitical escalations threaten a second wave of inflationary shocks next year.

PMI data points to a stalling UK economy, while an MPC member explicitly defends the current level of restriction and leaves the door open to further hikes. That policy contrast, tightening bias in the contracting services sector, is likely to shape the GBP outlook into next week.

The EUR/GBP pair sits subdued at 0.8647. Both currencies bear the weakness; sterling from disappointing retail sales figures and collapsing services PMIs, the euro from a faster and deeper contraction in eurozone activity. The euro's heavier fundamental damage keeps the pair's bias to the downside, but sterling's own soft data limits the move. It appears that neither side has a clean case to run.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3485, 1.3550 and Support sits at 1.3380, 1.3320

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8685, 0.8720 and Support sits at 0.8610, 0.8580

EUR: Euro Slides as Growth Engine Slows Again

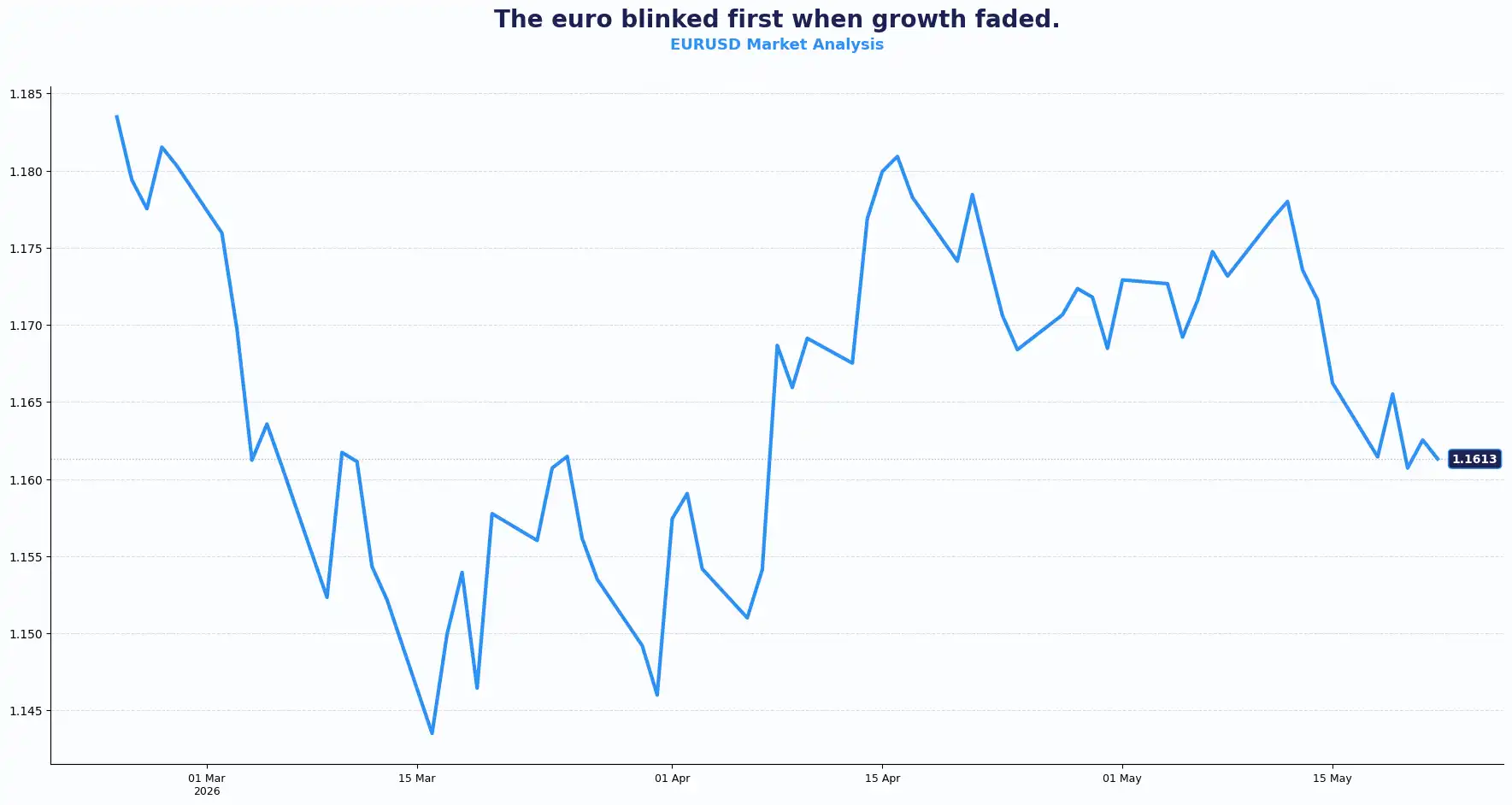

EUR/USD 1.1613

The Euro slipped to 1.1613 against the US dollar as macroeconomic indicators signalled a sharp economic contraction across the Eurozone, its fastest rate in more than two and a half years.

HCOB Eurozone PMIs for May confirmed the deterioration. Manufacturing came in at 51.4, below the prior of 52.2. Composite dropped to 47.5 from 48.8. Services fell to 46.4 from 47.6. All three moved southward, with composite and services deep in contraction. A conflict-driven surge in living costs hammered service demand and pushed input price inflation to a three-year-high.

Eurozone Consumer Confidence for May printed at −19, beating a consensus of −20.8 and a prior of −20.6, a marginal positive, though the broader backdrop limits how much weight it carries.

Germany provided the day's more constructive data. The GfK Consumer Climate Survey for June came in at −29.8. German GDP for Q1 printed at +0.3% QoQ, matching consensus and the prior. Year-on-year, German GDP came in at +0.4%, above the consensus of +0.3% and the previous +0.3%. German GDP delivers a modest beat, though it reflects Q1, before the full weight of May's conflict-driven energy shock landed on the Eurozone.

Eurogroup and Ecofin meetings run all day today, adding a political dimension to the session. Germany's IFO business climate and expectations data for May also lands today, a further read on how German business sentiment is holding up.

EUR/USD now trades in the low 1.16s as investors price a higher probability of a Fed rate hike by year-end and judge the European Central Bank's (ECB) room to manoeuvre as more constrained than the Fed's. Higher oil and gas prices hit the Eurozone economy structurally harder than the US economy, reflecting the asymmetry in the ECB's ability to respond to inflation. Markets still expect the ECB to hike 25bps in June.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1665, 1.1720 and Support sits at 1.1570, 1.1500

USD: Iran Uncertainty Keeps a Bid Tone

DXY 99.22

The dollar holds near a six-week peak, strengthened toward 99.22 as investors rewarded American economic resilience. Overnight volatility was high with conflicting signals on a US-Iran peace deal whipsawing prices, but moves in currency pairs remained largely contained in the Asian session as participants awaited clarity.

Washington and Tehran remain apart on Iran's uranium stockpile and control of the Strait of Hormuz. US Secretary of State Marco Rubio noted "some good signs" in talks, which gave the dollar a modest headwind, but the broader bid tone held. Six weeks into the ceasefire, conviction around a near-term resolution appears to remain thin. Market sentiment suggests expectations of a path to resolution are likely to require a more forceful US posture, a dynamic that could support the dollar's haven demand.

US S&P Global PMIs for May showed manufacturing at 55.3, up from a prior of 54.5 and a four-year high. The composite came in at 51.7, matching the prior. Services printed at 50.9, marginally above a prior of 51.0. All three remain above 50. The contrast with UK and eurozone PMIs is stark, reflecting that the US economy is expanding while its peers are contracting.

US initial jobless claims fell last week. Unadjusted weekly claims came in at 185,625, down 5,826 from the prior week. The insured unemployment rate two weeks prior was held at 1.1%, unchanged. Labour market resilience gives the Federal Reserve (Fed) space to focus on the inflation side of its dual mandate, which is precisely what it appears to be doing.

Today, President Trump hosts the swearing-in of Kevin Warsh as Fed Chair at 11:00am ET. The Jerome Powell era formally concludes. Warsh chairs his first FOMC meeting on 16–17 June. Market expectations suggest the rate cuts are not on the table at that meeting. Fed officials, including Richmond Fed President Tom Barkin and Philadelphia Fed President Anna Paulson, have both described current policy as "well-positioned" and "appropriately positioned" respectively. Their language signals no urgency to move in either direction, but an increasing willingness to consider rate hikes should inflation fail to subside. The funds rate target range remains at 3.50%-3.75%, unchanged since the April 28–29 FOMC meeting.

The combination of a hawkish Fed transition and defensive safe-haven flows establishes a strong structural floor for the US dollar.

Other Currencies: Yen Soft, Emerging Asia Under Pressure

AUDUSD 0.7145 | NZDUSD 0.5876 | USDJPY 159.08 | GBPJPY 213.64

The yen holds on the weaker side of 159 per dollar. Japan's core inflation slowed to a four-year low in April, complicating the Bank of Japan's (BoJ’s) rate-hike path. Japanese authorities have intervened recently, but the yen has since given back more than half its post-intervention gains. Intervention risk is building; officials have signalled no hard ceiling on the frequency or scale of action.

The Australian dollar fell 0.1% to 0.7142. The New Zealand dollar trades at 0.5875. Both currencies are under pressure from a stronger dollar and persistently elevated oil prices.

Emerging Asian currencies are under severe strain from the global energy shock. Indonesia announced that, from 1 June, all natural resources exporters must hold 100% of export revenues in state-owned banks. The rupiah has been under sustained pressure, and the policy targets the onshore dollar supply directly. Policymakers across Asia now face rising pressure as imported inflation and dollar funding costs rise together.

Current Table:

| Pair | Spot | Trend Bias |

|---|---|---|

| GBP/USD | 1.3425 | Bearish below 1.3450 |

| EUR/USD | 1.1613 | Soft below 1.1650 |

| EUR/GBP | 0.8647 | Rangebound |

| USD/JPY | 159.08 | Bullish |

| GBP/JPY | 213.64 | Volatile bullish bias |

| AUD/USD | 0.7145 | Soft |

| NZD/USD | 0.5876 | Soft |

Market Lookahead

Tue, 26 May

- US Consumer Confidence for May

Wed, 27 May

- Australia CPI for April

- New Zealand RBNZ Interest Rate Decision and Monetary Policy Review

- US ADP Employment Change

Thu, 28 May

- Eurozone Business Climate and Consumer Confidence

- ECB Monetary Policy Meeting Accounts

- US Durable Goods Orders

- US Q1 GDP Revision

- US Core PCE Inflation

Fri, 29 May

- Germany Unemployment Change

- Germany CPI and Harmonised Inflation Data for May

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.