One Exit in London, One Hawkish Fed, One Closed Strait

7 min read

Share

Sterling hit a one-month low after a UK cabinet resignation deepened the political crisis around Keir Starmer. The dollar posted its sharpest weekly gain since March on resilient US data and a hawkish Fed repricing. The euro softened as oil hit $107. Meanwhile, In Geneva, Trump and Xi had their summit meeting and their conversation about the Strait of Hormuz, US oil sales, shifted crude, the yuan, and rate expectations all at once.

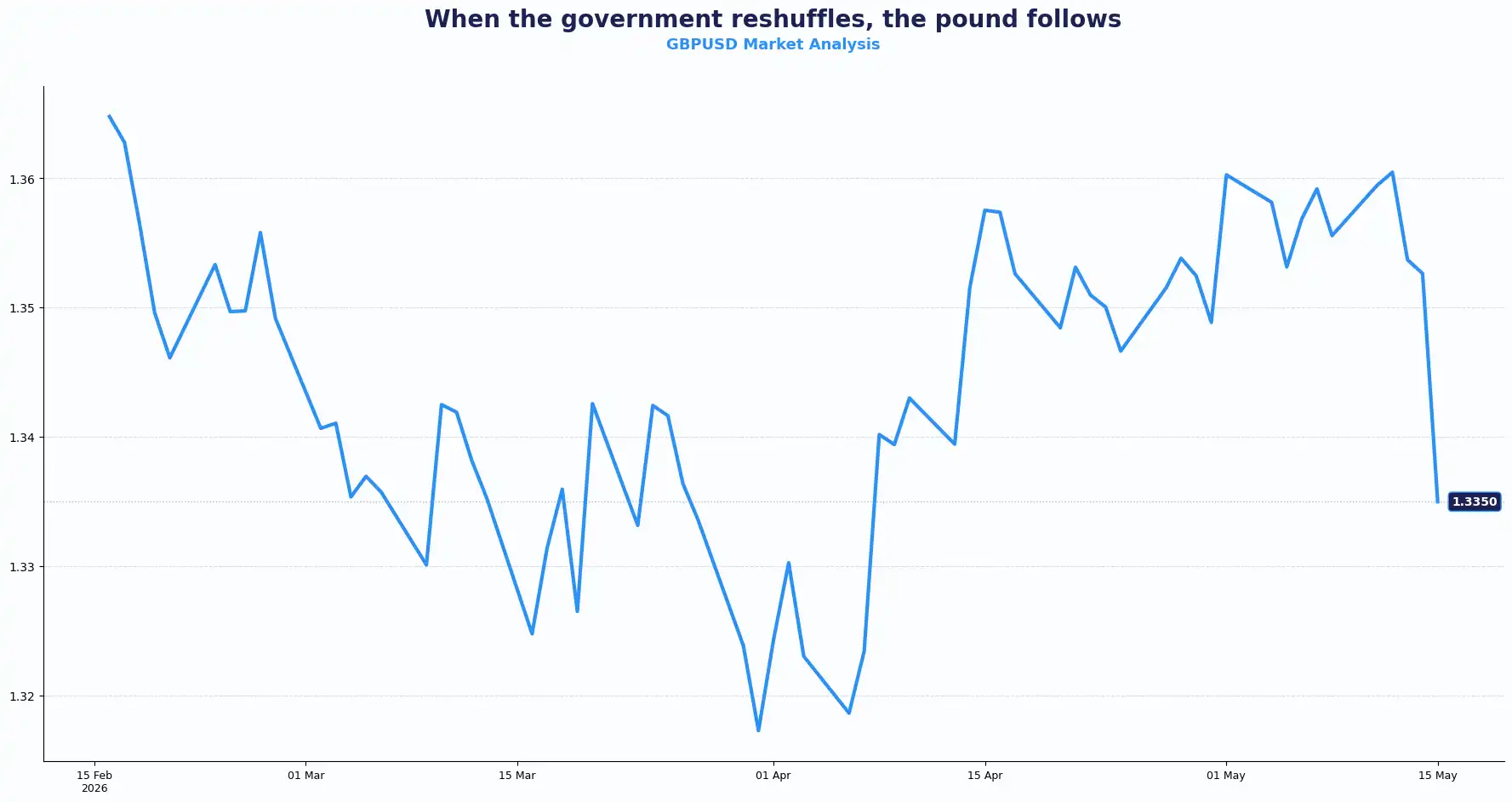

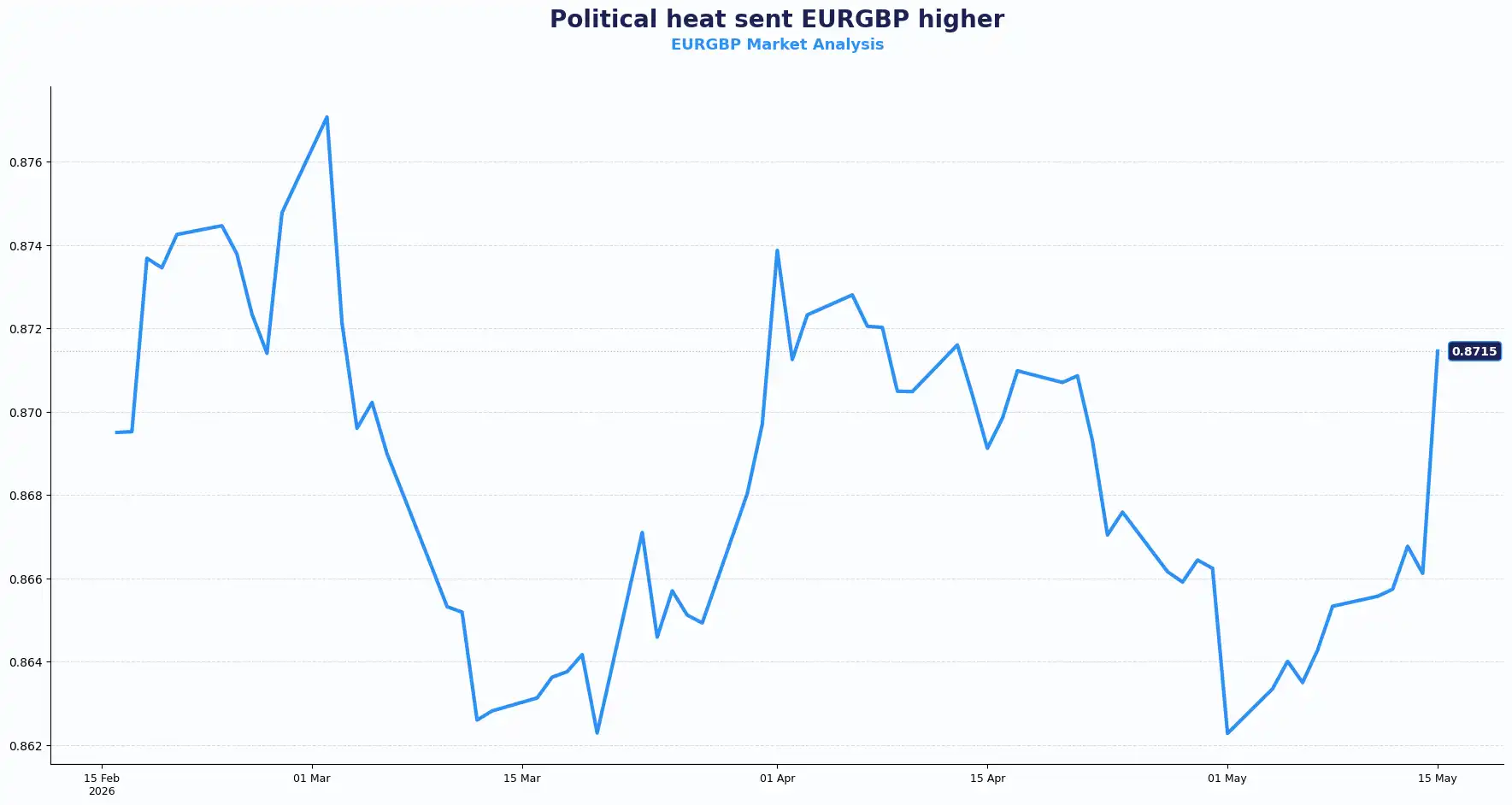

GBP: Starmer Crisis Is Turning Into Sterling's Crisis

GBPUSD 1.3357 | EURGBP 0.8719

Sterling hit a one-month low of $1.3357, falling 0.9% in a single session, its fourth consecutive daily decline. Against the euro, the pound slid to 87.19 pence per euro from 86.66. The UK political crisis sharpened after Health Secretary Wes Streeting resigned, followed by MP Josh Simons stepping aside to allow Manchester mayor Andy Burnham a clear run at parliament. Both moves signal an active challenge to Keir Starmer's leadership following the Labour Party’s heavy losses in last week's local elections.

The succession uncertainty creates a fiscal vacuum at the worst possible moment. Traders now question the direction of UK fiscal policy heading into the autumn budget cycle; its ambiguity is weighing directly on gilt yields. The 10-year gilt yield pulled back four basis points to 5.026%, off the day's highs near 5.05%, but the political noise keeps sentiment fragile. Angela Rayner's HMRC clearance further broadened the field of leadership contenders.

At the Bank of England (BoE), the MPC sent two notably different signals in the same session. Chief Economist Huw Pill, who cast the sole vote to raise rates at the last meeting, made clear he sees risks of second-round inflation becoming entrenched. He noted that the disinflationary process had been stalling before the Iran conflict escalated, and he supports "a prompt but modest tightening" to head off persistent inflation. Deputy Governor Sarah Breeden took a cooler view. She described economic activity as "lacklustre" and argued the current energy shock is far less likely to generate the kind of wage-price spiral seen in 2022, given a looser labour market. Breeden sees no urgency to act in June or July. This stark policy divergence creates an unstable environment for sterling.

MPC member Catherine Mann added another layer, flagging that monetary policy needs to stay alert to the UK's debt position, a rare explicit reference to fiscal sustainability risk from inside the Bank.

The UK economy did expand in Q1 2026 at an annual rate of 1.1%, with March GDP rising 0.3%, both ahead of expectations. This resilience provides some floor to the pound. But with political leadership in flux, fiscal policy uncertain, and the MPC publicly divided, the balance of risks for sterling sits firmly to the downside.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450 and Support sits at 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8750 and Support sits at 0.8660

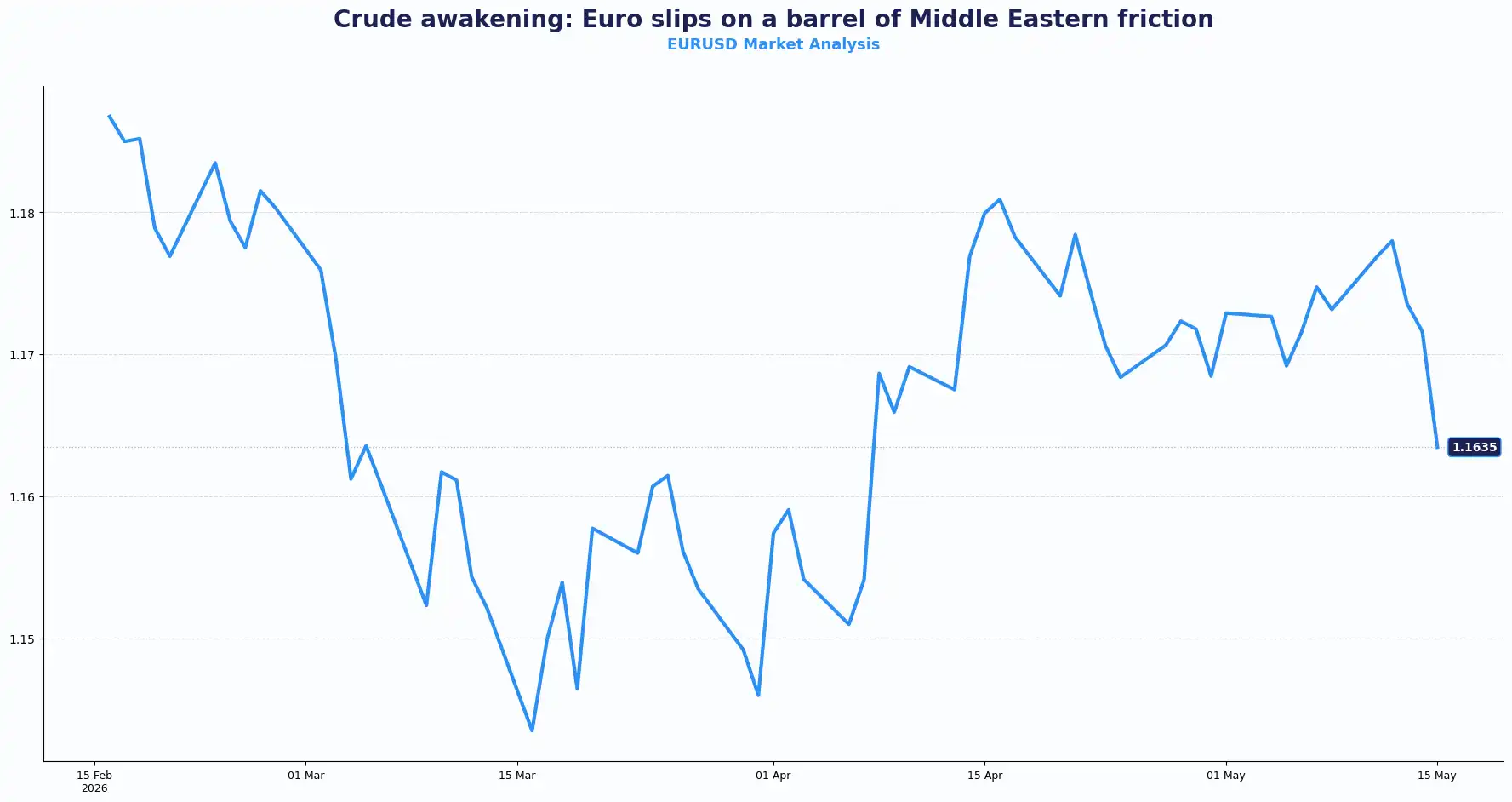

EUR: Euro Weakens as Severe Energy Shocks Intensify

EURUSD 1.1640

The EUR/USD pair fell to a one-month low, trading 0.15% lower at $1.1640 on the day and set to lose around 1.1% across the week. European equity futures dropped more than 1% ahead of the open, dragged lower alongside broader global risk-off sentiment. The move reflects less a eurozone-specific problem and more the euro's absorption of twin pressures: a stronger dollar and rising energy costs.

Geopolitical tensions and rising oil prices are dominating the price action. Brent Crude climbed 5.7% this week to $107 a barrel after fresh attacks on shipping in the Strait of Hormuz region, one vessel struck, another seized. The absence of any meaningful diplomatic progress to reopen the strait keeps energy prices elevated. Attacks on vessels spark profound supply. Higher energy costs present a severe headwind for the Eurozone economy, dampening productivity while stoking imported inflation.

The European Central Bank (ECB) faces a complex dilemma. Central bankers must address inflationary pressures without choking a fragile economic recovery. The energy crisis weakens the euro's structural support, driving capital toward higher-yielding assets across the Atlantic.

The Trump-Xi summit in Geneva provided marginal support. Both leaders expressed a shared desire to reopen the Strait of Hormuz, and China signalled interest in purchasing US oil as an alternative to Middle Eastern supply. Markets read the outcome as broadly constructive but short of any concrete commitment, hence the muted price reaction.

NVIDIA's 4% surge after market hours pulled US equities to record highs. US outperformance, combined with the dollar's momentum, has kept a lid on any euro recovery.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1700 and Support sits at 1.1660

USD: Dollar Rally Gains Pace on Fed Repricing

DXY 99.10

The dollar index climbed to a one-month high, up roughly 1.2% across the week, its sharpest weekly gain since early March. US Treasury yields scaled 11-month highs as rate-hike expectations reset materially higher. Investors now price close to a 40% probability of a Fed rate increase in December 2026, up from 22.5% just one week ago, according to the CME FedWatch tool.

US retail sales rose 0.5% in April, matching consensus after a strong March. Weekly jobless claims ticked up by 12,000 to 211,000, slightly above the 205,000 estimate but consistent with a stable labour market. US consumers are spending at a pace that continues to defy survey pessimism; they are telling pollsters they are more cautious, but they are not walking the talk.

Kansas City Fed President Jeffrey Schmid described inflation as the biggest risk facing an economy he called "remarkably resilient." Meanwhile, Fed Governor Stephen Miran, a consistent advocate for rate cuts, announced he will resign ahead of Kevin Warsh's swearing-in as the next Fed Chair, a procedural step to create a vacancy on the seven-member board. The succession move reinforces a hawkish institutional pivot at the top of the Fed.

With US CPI market forecasts revised higher again for 2026 and risks still skewed to the upside, the base case has shifted. An extended pause through the rest of 2026 now precedes any expected resumption of easing in 2027.

The onshore yuan pulled back from its strongest level against the dollar in over three years, trading at 6.7953 per dollar. Offshore, the USD/CNH dipped marginally to 6.7961. The brief positive signal from a Saudi-Iran non-aggression pact float caused a short-lived dip in crude and the dollar before both resumed their trends.

Commodity Currencies Retreat Amid Dollar Strength

AUDUSD 0.7171 | NZDUSD 0.5869 | USDJPY 158.54 | GBPJPY 211.74

The yen held on the weaker side of 158 per dollar despite Japanese producer prices rising sharply, data that strengthens the case for the Bank of Japan (BoJ) to raise rates as early as June. The USD/JPY pair at 158.54 reflects the yen's continued vulnerability to broad dollar strength, even when domestic inflation data points to a hawkish stance.

The Australian dollar retreated 0.4% to $0.7171, backing away from a recent four-year peak. The New Zealand dollar fell 0.55% to $0.5869. Both antipodean currencies absorbed the global dollar bid without a specific domestic catalyst.

GBPJPY at 211.74 captures the compound effect, sterling weakness meets yen softness. Political risk in London continues to generate downward pressure on this cross.

Aggressive dollar accumulation overpowers G10 indicators. Typically, strong commodity prices cannot withstand the allure of soaring US yields. This is when we see global capital migrate toward liquid dollar assets, leaving risk-sensitive currencies exposed to downside pressure. This realignment alters transactional behavior.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBPUSD | 1.3357 | Bearish |

| EURGBP | 0.8719 | Bullish |

| EURUSD | 1.1640 | Bearish |

| USDJPY | 158.54 | Bullish |

| AUDUSD | 0.7171 | Bearish |

| NZDUSD | 0.5869 | Bearish |

| GBPJPY | 211.74 | Volatile |

| DXY | 99.10 | Bullish |

Market Lookahead

Fri, 15 May

- German Industrial production (Mar)

Mon, 18 May

- CNY - Industrial Production (Apr)

- CNY - Retail Sales (Apr)

Tue, 19 May

- UK - Avg. Earnings, Claimant Count Change & Rate (Apr) , ILO Unemployment Rate, Employment Change

- Canada’s CPI

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.