Peace whispers in Tehran, Intervention heat in Tokyo

6 min read

Share

Iran deal signals pause “Project Freedom” – risk assets rally, the dollar retreats. Sterling navigates BoE rate bets against local election risk. The euro holds firm above 1.17. The yen surges on suspected intervention for the second time in a week. Data flow thickens ahead of Friday's NFP.

GBP: Sterling Gathered by Political Clouds

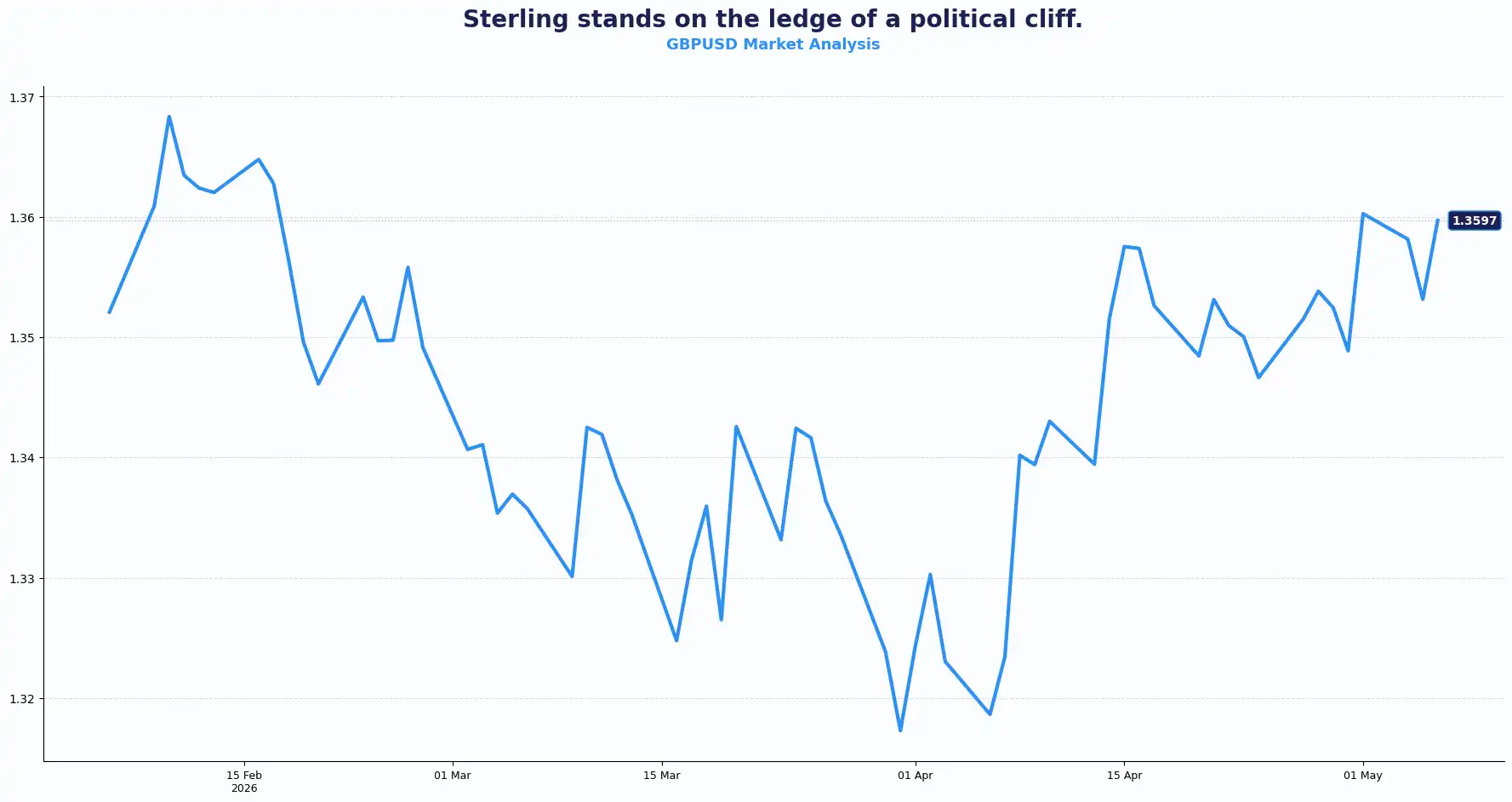

GBPUSD: 1.3588 | EURGBP: 0.8635

The dollar fell against most major currencies on Wednesday as the US signalled a possible deal with Iran. Sterling touched $1.3588, up 0.4% on the day, with the euro moving in tandem at $1.1736, while the EUR/GBP pair settled near 0.8635.

Sterling's strength since the start of the Middle East conflict is a BoE story. Before hostilities, the market priced cuts. It then swung sharply to pricing hikes, now reflecting at least two 25bps increases this year, with a meaningful probability of a third. This repricing has driven the pound to outperform most G10 peers.

The BoE held policy last week but kept the door open to future rate hikes. But the backdrop is softening: UK economic data is showing signs of weakness, and rate hikes at this stage carry the risk of amplifying that weakness rather than simply cooling inflation.

Today brings the UK S&P Global composite and services PMI figures. With gilt yields at their highest since 1998, UK 30-year gilts traded as high as 5.78% on Tuesday, and 10-year yields topped 5.10%. The investors are closely watching every data release for cues.

The political dimension is harder to quantify but not to dismiss. Wednesday's local election results could pose a direct risk to sterling. A poor showing for Labour raises the probability of Keir Starmer's resignation. A potentially more left-wing successor would focus attention on public finances. The EUR/GBP pair, currently close to 0.86, could trend towards 0.89 if political conditions deteriorate.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3650 and Support sits at 1.3450

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700 and Support sits at 0.8550

EUR: Euro Data in the Crosshairs

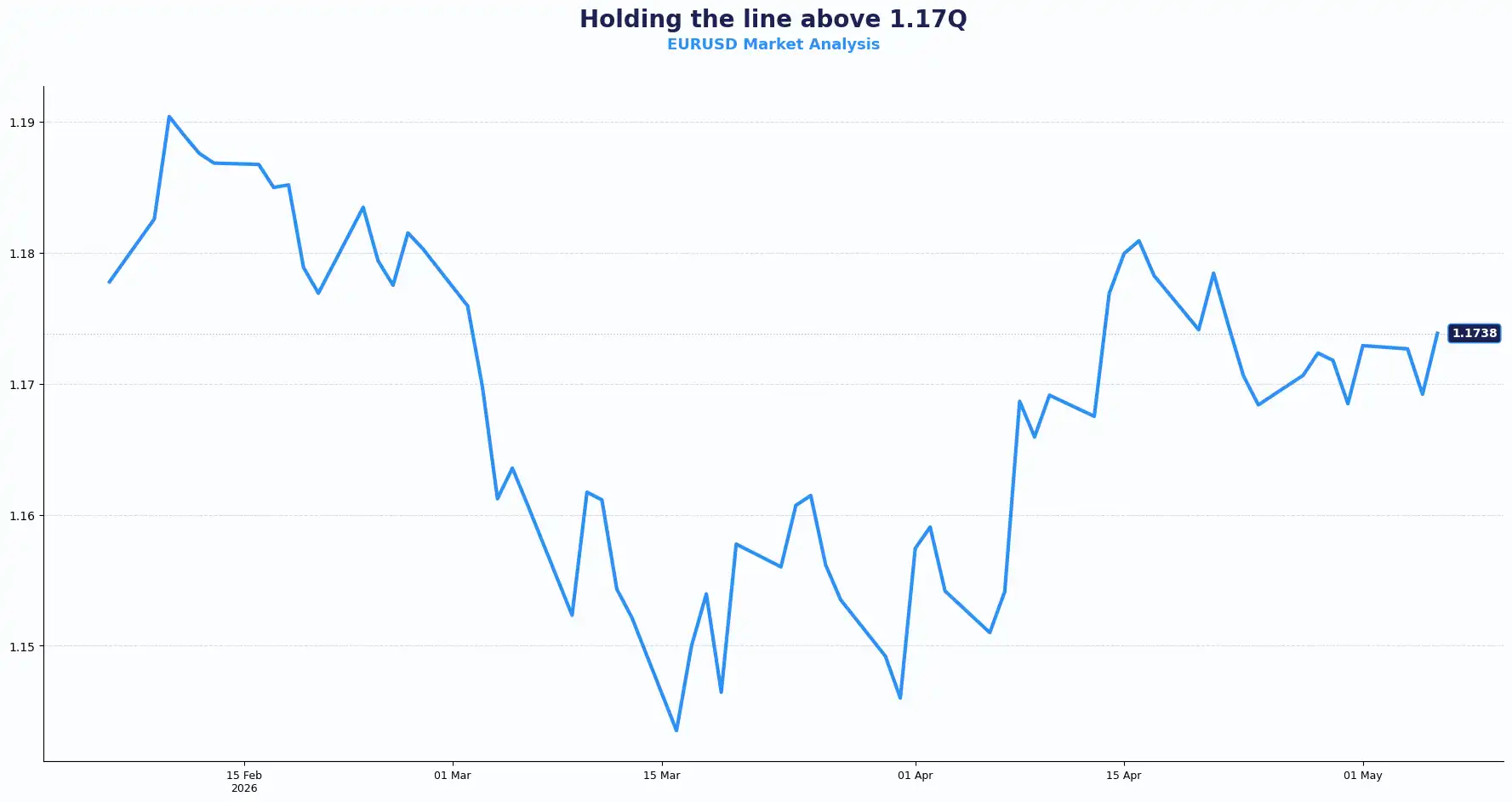

EURUSD: 1.1733

EUR/USD held firm above 1.1700 through early European trading on Wednesday. Improved risk sentiment is doing the heavy lifting, while the dollar's safe-haven bid is fading as optimism over the Iran deal takes hold.

Today brings Germany's HCOB services PMI for April, forecast at 46.9, with the composite expected at 48.3, both unchanged from last month and both still below the 50 expansion threshold. The Eurozone-wide composite and services PMI follows. Consensus signals another month of contraction with no recovery in sight. The euro's resilience above 1.17 owes more to dollar weakness than eurozone economic strength; a distinction that sharpens considerably if the dollar finds a bid later this week.

Also, due today: Eurozone Producer Price Index (PPI) for March. Consensus puts the monthly reading at 3.3%, a sharp reversal from the prior month's -0.7%. The annual consensus stands at 1.8% against a prior of -3.0%. A reading in line or above consensus is typically associated with upward pressure on the EUR. Tomorrow brings Eurozone Retail Sales data for March.

The fundamental constraint on the EUR/USD pair currently remains the Iran conflict. Only a clear directional shift, de-escalation, or renewed escalation is likely to push the pair outside the range it has held for several weeks. Today's ADP employment data from the US presents the next test. Barring an outlier reading, it is unlikely to shift the dollar materially.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1800 and Support sits at 1.1650

USD: Dollar Slips as Risk Appetite Builds

DXY 98.09

The dollar eased broadly on Wednesday as Trump's "great progress" comments on a "final agreement" with Tehran triggered a risk-on rotation. Stocks rose. Oil slipped towards $100 per barrel on WTI. Safe-haven demand for the dollar softened.

Corporate earnings continue to prop up sentiment. AI-driven capital expenditure remains the dominant narrative for S&P 500 earnings growth, with the technology sector leading. Investors are looking through geopolitical risk and focusing on what they can see: robust top-line figures from Big Tech.

On the data side, yesterday's JOLTS report showed job openings at 6.9 million (4.1%), down from February's 6.92 million – a softer read. Today's ADP employment change figure follows. A strong print could give the dollar a modest boost. A weak print might just reinforce the case for caution. Friday brings the official NonFarm Payrolls report, which will carry the most weight this week, for Fed policy expectations. US S&P PMI services data showed that new orders fell in April 2026 for the first time since April 2024, likely due to the Middle East Conflict. Investors are focusing on these signals as the employment numbers land.

US initial jobless claims figures arrive on Thursday. The labour market picture remains the Fed's primary input. No clear direction in employment data is likely to emerge this week, but the sequence of releases could sharpen expectations heading into next month's policy meeting.

Eastern Shadows: The Yen and the Antipodeans

AUDUSD 0.7250 | NZDUSD 0.5951 | USDJPY 155.00 | GBPJPY 212.33

The USD/JPY pair slid sharply to 155.00, up nearly 2% to its strongest level since 26 February, after what looks like a second round of Japanese foreign exchange intervention in a week. The AUD/JPY pair dropped below 113.00 on the move.

Japanese Finance Minister Satsuki Katayama had already warned against speculative moves earlier in the week, citing a joint statement signed with the United States last year. "We will take decisive measures against speculative moves," Katayama told reporters at the Asian Development Bank's annual meeting in Uzbekistan. The Ministry of Finance was unavailable for comment during a local holiday.

The timing is telling. The Iran deal optimism gave the authorities cover, a moment of broader dollar weakness to add extra force to the yen's move. Whether the intervention holds through the end of the week remains the question.

The Aussie dollar printed a four-year high at $0.7250, buoyed by a third consecutive interest rate hike from the Reserve Bank of Australia (RBA) the previous day. The New Zealand dollar reached $0.5951, its highest in nearly two months. Both Antipodean currencies benefited from improved risk appetite and a softer dollar.

In other typically sought-after safe-haven assets, Gold rose 2.1% to $4,651.84. Bitcoin dipped 0.5% to $81,264.67. Ether fell 0.8% to $2,364.40.

Current Rate Table:

| Pair | Rate | Trend Bias |

|---|---|---|

| GBP/USD | 1.3588 | Bullish, stretched |

| EUR/USD | 1.1733 | Range-bound, Bullish Bias |

| EUR/GBP | 0.8635 | Flat |

| USD/JPY | 155.00 | Volatile, JPY bid |

| GBPJPY | 212.33 | Volatile |

| AUD/USD | 0.7250 | Uptrend intact |

| NZD/USD | 0.5951 | Uptrend building |

Market Lookahead

Wed, 06 May

- UK S&P Global Composite & Service PMI (Apr)

- Eurozone and Germany HCOB Composite and Services PMI (Apr)

- Eurozone Producer Price Index (Apr)

Thu, 07 May

- Germany factory orders (mar)

- Eurozone retail sales (mar)

- US Initial Jobless claims

Fri, 08 May

- German Industrial production & trade balance (Mar)

- US Unemployment rate, Average hourly earnings, NonFarm Payrolls (Apr)

Sat, 09 May

- China Trade balance and import exports CNY AND USD (Apr)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.