Two Holds. Two Hawks. One Softer Dollar

7 min read

Share

The BoE and ECB both kept bank rates unchanged. Both warned of hawkish signals. Sterling climbs on policy signals, euro steadies on ECB intent. Four major central banks flagged inflation risk in a single week. The dollar faces headwinds, navigating a path through tech earnings and yield divergence. Oil volatility and geopolitical uncertainty lingers beneath the surface, shaping global FX tone.

GBP: The BoE’s Active Hold

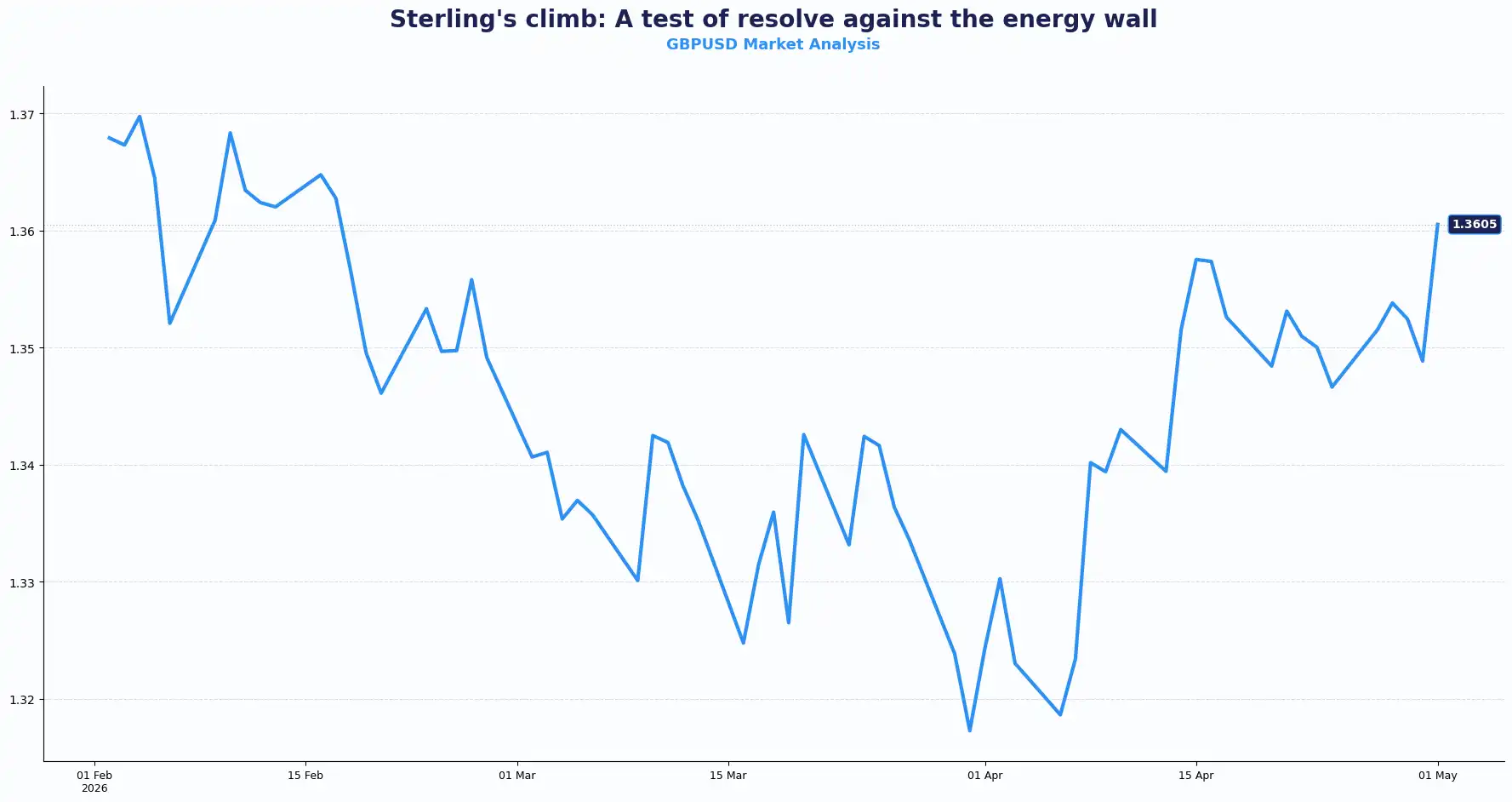

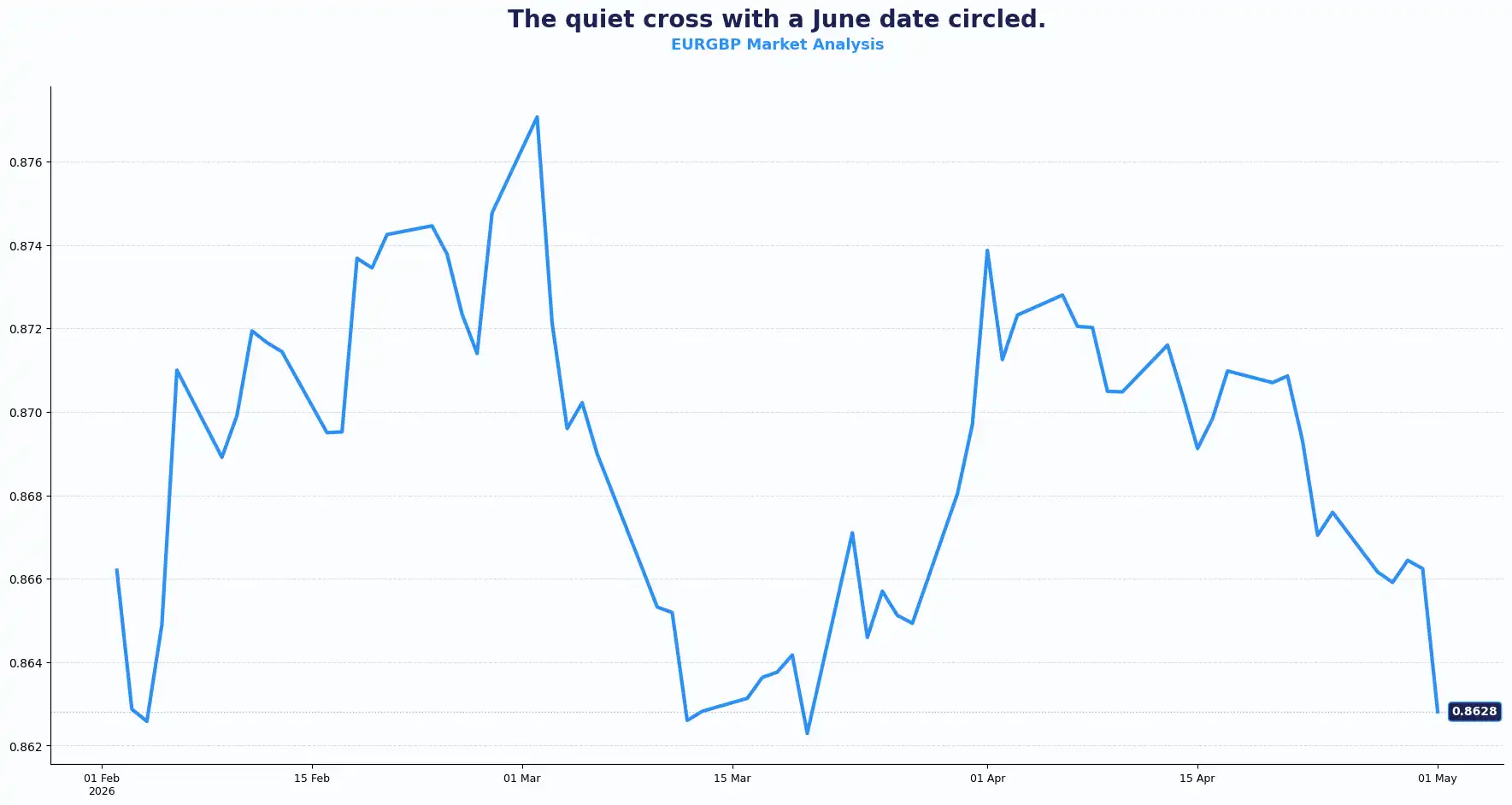

GBPUSD 1.3593 | EURGBP 0.8626

Cable approached near 10-week highs, testing 1.36 levels. Despite broader geopolitical concerns, the currency found support as the Bank of England (BoE) held its interest rate at 3.75% and adopted a hawkish tone.

BoE Governor Andrew Bailey was unambiguous: “This is an active hold, not a wait-and-see.” Inflation expectations have risen sharply. Energy disruption is lasting longer than curve pricing implies. The BoE suggests that policy tightening creates the necessary friction to counter energy-driven inflation. Chief Economist Huw Pill voted to hike 25 bps to 4.00% immediately - the lone dissenter, but a telling one.

Bailey's language on gas prices carried real weight. He said the market's forward curve for gas prices is too optimistic given how long it could take to restore supply. This divergence between market pricing and the central bank's assessment is where sterling's upside case lies. If energy disruption persists with the Strait of Hormuz still closed and Iran pledging "long and painful strikes" on US positions, there is little reason to expect otherwise; the Monetary Policy Committee (MPC) has signalled it stands ready to act with force.

The MPC minutes confirmed that CPI is projected to reach 3.6% in a worst-case scenario by Q4, with GDP growth still at 0.5-0.8% across all three scenarios modelled. No recession. Slower growth, but not contraction. The labour market, per Deputy Governor Dave Ramsden, is in a materially different position than in 2022. We are witnessing tighter monetary conditions today, meaning the starting point for any further action is already restrictive.

Market consensus now prices back-to-back hikes in June and July. The June MPC meeting on the 11th is the next rate decision.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3600, 1.3650 and Support sits at 1.3450

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8650 and Support sits at 0.8580

For EUR/GBP, the policy divergence between the BoE's conditional tightening bias and the European Central Bank’s (ECB) more cautious stance may draw investor attention as they track relative rate expectations. Given that the cross has historically responded to shifts in forward rate differentials, the current signals from both central banks suggest that this dynamic could continue to evolve.

EUR: The ECB Maintains Flexibility

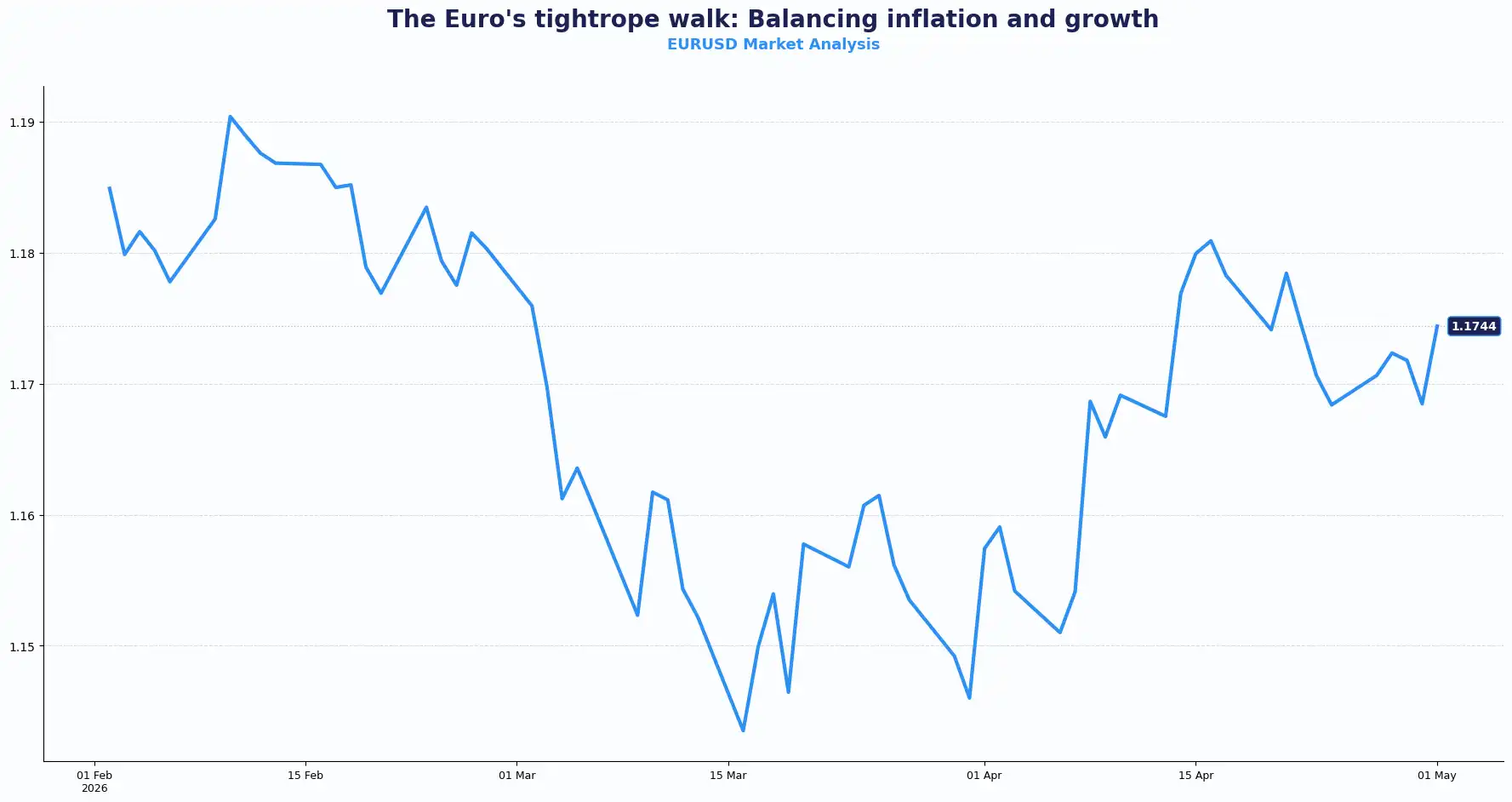

EURUSD 1.1726 | EURGBP 0.8626

EUR/USD edged up from a three-week trough of 1.1655 to 1.1726, following the ECB policy update. ECB unanimously held the rate at 2.00%, but the conversation in Frankfurt was far from unanimous on direction. Christine Lagarde avoided committing to a rigid rate path. She emphasised that data over the next six weeks will dictate the Governing Council's decisions. The market reaction stayed contained, reflecting the ECB’s focus on meeting-by-meeting adjustments.

ECB President Christine Lagarde confirmed the Governing Council debated a rate hike at this meeting. She declined to specify which scenario from the March meeting is now most likely, but acknowledged the ECB is moving away from its baseline. Short-term inflation expectations have moved up significantly. Upside risks to inflation and downside risks to growth have both intensified. Underlying inflation has changed little.

The ECB's next move, should it come, points to June, when the ECB will have updated projections and new scenario modelling. Lagarde described the approach as data-dependent and meeting-by-meeting. That is the language of a central bank that wants to act but needs political cover from the data.

Next week's eurozone data run matters for this reason. Germany and Eurozone HCOB PMI figures land on Wednesday, Eurozone Producer Price Index (PPI) data, and Eurozone retail sales on Thursday. Upside surprises could accelerate rate hike expectations. Downside surprises may test Lagarde's already careful messaging.

For EUR/USD and EUR/GBP, the sequence and magnitude of rate-hike expectations, relative to the Fed and the BoE, respectively, are the structural drivers investors are likely to track through next week's data. Incoming figures on consumer and producer prices, in particular, have historically influenced positioning ahead of ECB meetings.

USD: Narrow Rally, Tech Earnings and Yield Flux

DXY 98.20

The dollar index (DXY) softened to 98.20 in April. This drop follows a surge in March. The dollar index slid 1.76% as the U.S. economy displayed relative resilience to higher oil prices compared to the Eurozone and Japan. The reversal reflects the market's reassessment of the US economy's relative energy insulation.

The Federal Reserve's (Fed) hawkish shift on Wednesday closed the door on rate cut expectations. US 10-year Treasury yields closed the week up 8 basis points to 4.39%. The dollar's softness despite this reflects cross-currency dynamics: the BoE and ECB are now openly tightening or approaching hikes, compressing the Fed's relative advantage.

The Wall Street rally that cushioned sentiment this week has been notable for its narrowness. Gains concentrated in semiconductors, IT, and communications. Caterpillar's AI-driven data centre demand story added nearly 10%, while broader earnings upgrades outside that cluster remain sparse. Oil has pulled back from Brent's four-year peak, but that largely reflects contract roll dynamics rather than any fundamental easing of Strait of Hormuz disruption.

U.S. crude trades near 105.10 dollars a barrel. With Iran still blocking the Strait and demand for petrol, diesel, jet fuel and fertilisers outpacing available supply, price pressure is structural. Four major central banks this week explicitly flagged inflation risk.

Next week investors are watching US data releases for April, including the Unemployment rate, Average hourly earnings, and NonFarm Payrolls figures. Any upside surprise in wages reinforces the Fed's current stance and may give the dollar a firmer footing.

The interplay between US payroll strength and energy-driven inflation expectations has historically influenced dollar positioning relative to sterling and the euro. Investors are seen tracking the Fed's rate path alongside macro data ahead of the June policy window.

Yen Intervention and RBA Expectations

AUDUSD 0.7199 | NZDUSD 0.5894 | USDJPY 157.29 | GBPJPY 213.77

Japanese authorities intervened on Thursday, selling dollars for yen in what markets anticipated was a formal intervention; the first yen-buying move in two years. The initial move sent the pair down five yen to 155.50. Buyers returned by Friday, pushing USD/JPY to 157.29.

The arithmetic here is uncomfortable for Tokyo. Japan imports all of its oil. A widening trade deficit from sustained high crude prices undermines the effectiveness of the intervention, and the structural outflows that push USD/JPY higher are intensifying rather than easing. The 160.00 level appears to be the line Tokyo is defending, but the cost could run to tens of billions of dollars based on historical precedent. Whether the intervention holds depends as much on Brent's trajectory as on the Bank of Japan's (BoJ) resolve.

The Aussie dollar touched near a four-year high at 0.7202, above the 0.72 threshold for the first time since June 2022. The Reserve Bank of Australia (RBA) meets next Tuesday, with market consensus pricing a 25 basis point hike to 4.35% from 4.10%. That hike, if delivered, could consolidate AUD's recent outperformance.

The New Zealand dollar slipped modestly to 0.5894. GBP/JPY extended gains to 213.77.

Oil prices and energy shocks remain the central thread at the moment, shaping inflation, trade balances, and policy responses across regions.

Commodity-linked currencies and intervention-sensitive pairs often react to shifts in energy pricing and policy expectations. These dynamics can influence cross-asset correlations.

Current Rate Table:

| Pair | Rate | Trend Bias |

|---|---|---|

| GBPUSD | 1.3593 | Uptrend |

| EURUSD | 1.1726 | Range |

| EURGBP | 0.8626 | Downtrend |

| USDJPY | 157.29 | Uptrend |

| AUDUSD | 0.7199 | Uptrend |

| NZDUSD | 0.5894 | Range |

| GBPJPY | 213.77 | Uptrend |

Market Lookahead

Mon, 04 May

- Germany HCOB Manufacturing PMI (APR)

- Australia’s S&P GLobal PMI

Tue, 05 May

- RBA Interest rate decision

- US JOLTS job openings , US ISM Services PMI (Apr)

Wed, 06 May

- Eurozone and Germany HCOB Composite and Services PMI (Apr)

- Eurozone Producer Price Index (Apr)

Thu, 07 May

- Germany factory orders (mar)

- Eurozone retail sales (mar)

- US Initial Jobless claims

Fri, 08 May

- German Industrial production & trade balance (Mar)

- US Unemployment rate, Average hourly earnings, NonFarm Payrolls (Apr)

Sat, 09 May

- China Trade balance and import exports CNY AND USD (Apr)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.