It's BoE & ECB Day with Sterling at 3-Week Lows, Fading Euro

7 min read

Share

GBP and EUR drift into today's BoE and ECB decisions under pressure. Fed kept its rate unchanged alongside Powell's final meeting as chair, an 8-4 vote, the most divided vote since 1992. Energy prices near four-year highs is the common thread, forcing every central bank to weigh an inflation problem against a growth outlook. Geopolitics and macro data continue to affect the crosses.

GBP: Pound Slips Before BoE Call

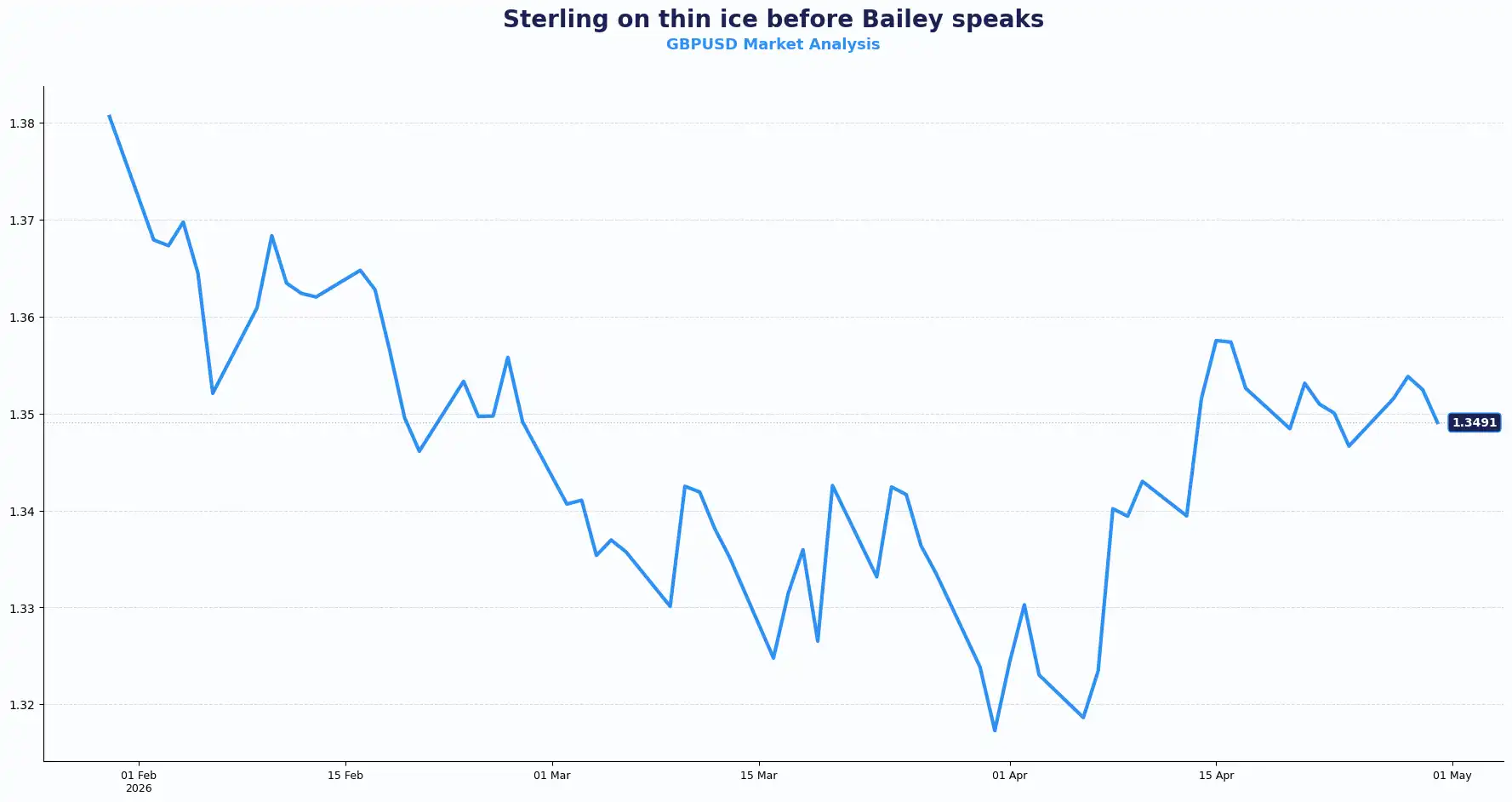

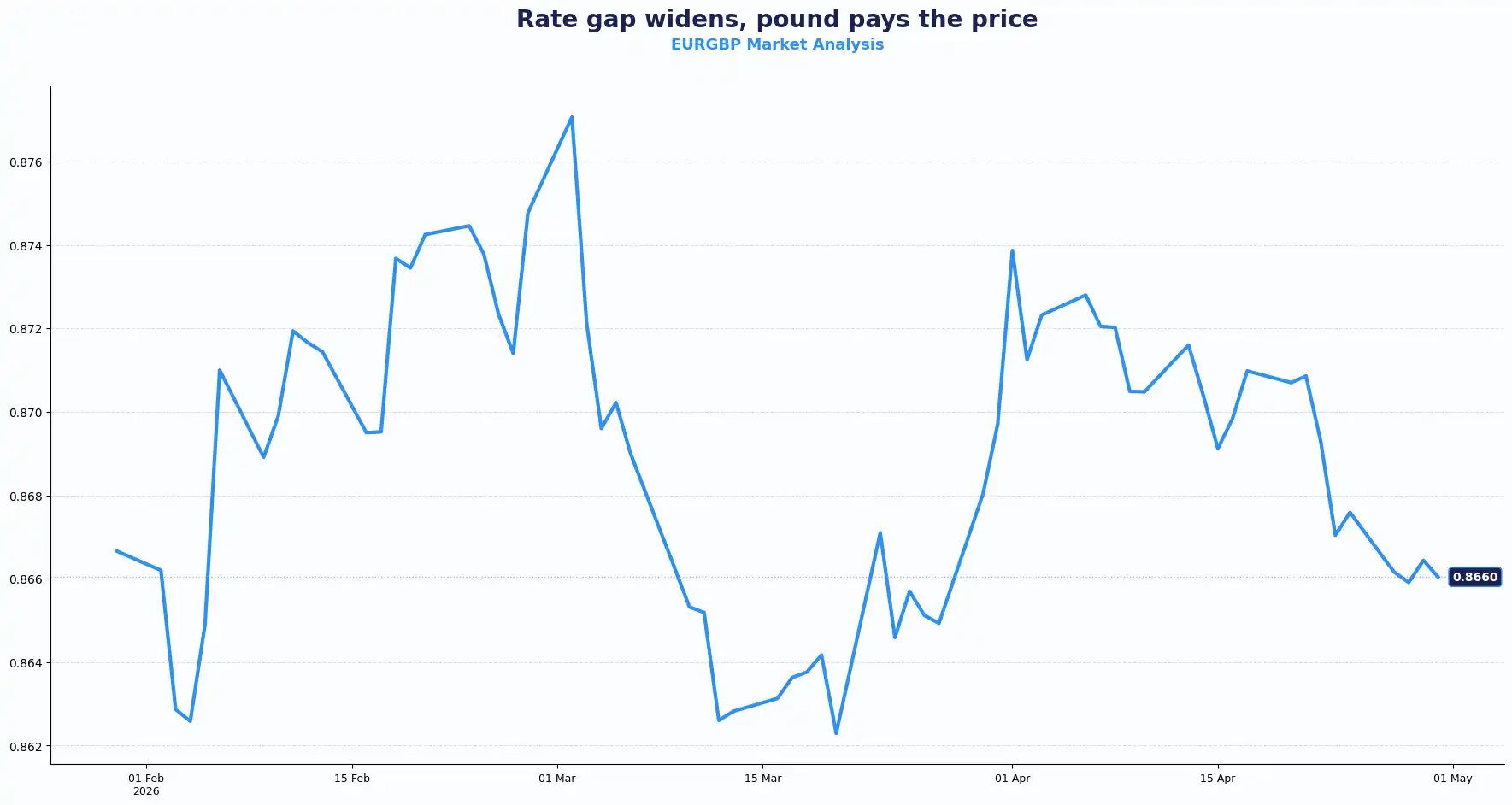

GBPUSD 1.3463 | EURGBP 0.8660

Sterling dropped 0.1% to $1.3463, touching its weakest level since early April, as investors position ahead of the Bank of England's (BoE) rate decision later today. Brent Crude is pushing past $113 a barrel after reports suggested the US is weighing further military action in Iran, adding to the pressure ahead of the bank decisions.

The BoE is expected to hold the Bank Rate at 3.75%. Governor Bailey's press conference and the MPC vote split. EUR/GBP is trading above levels implied by BoE-ECB rate differentials. Analysts typically attribute this to UK political uncertainty and elevated gilt yields after the energy shock.

We see a convergence of crises, with the BoE navigating growing inflationary pressures amid rising energy prices. Market anticipates three 25bps rate hikes this year. However, the Middle East conflict creates a structural impasse. The bank is likely to take a cautious stance by keeping the rates unchanged today, creating a divergence between the data and policy action.

With UK term premia rising and the Labour Party facing electoral headwinds, a risk premium has been embedded in sterling. That premium does not look likely to unwind quickly. The base case across desks is no change to bank rate today, but the probability of a hike has risen. The window for that move is flagged for late Q2 or early Q3 2026, contingent on how the MPC reads the incoming inflation data.

Rate holds alone might not anchor the single currency if inflation risks build. Volatility reflects shifting expectations across policy and geopolitics. With the geopolitical noise, the gap between rate expectations and the underlying inflation picture is a tension investors will be watching as Bailey takes the podium, parsing every word for the next direction.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3520 and Support sits at 1.3400

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700 and Support sits at 0.8620

EUR: Data Deficits Unease Ahead of ECB

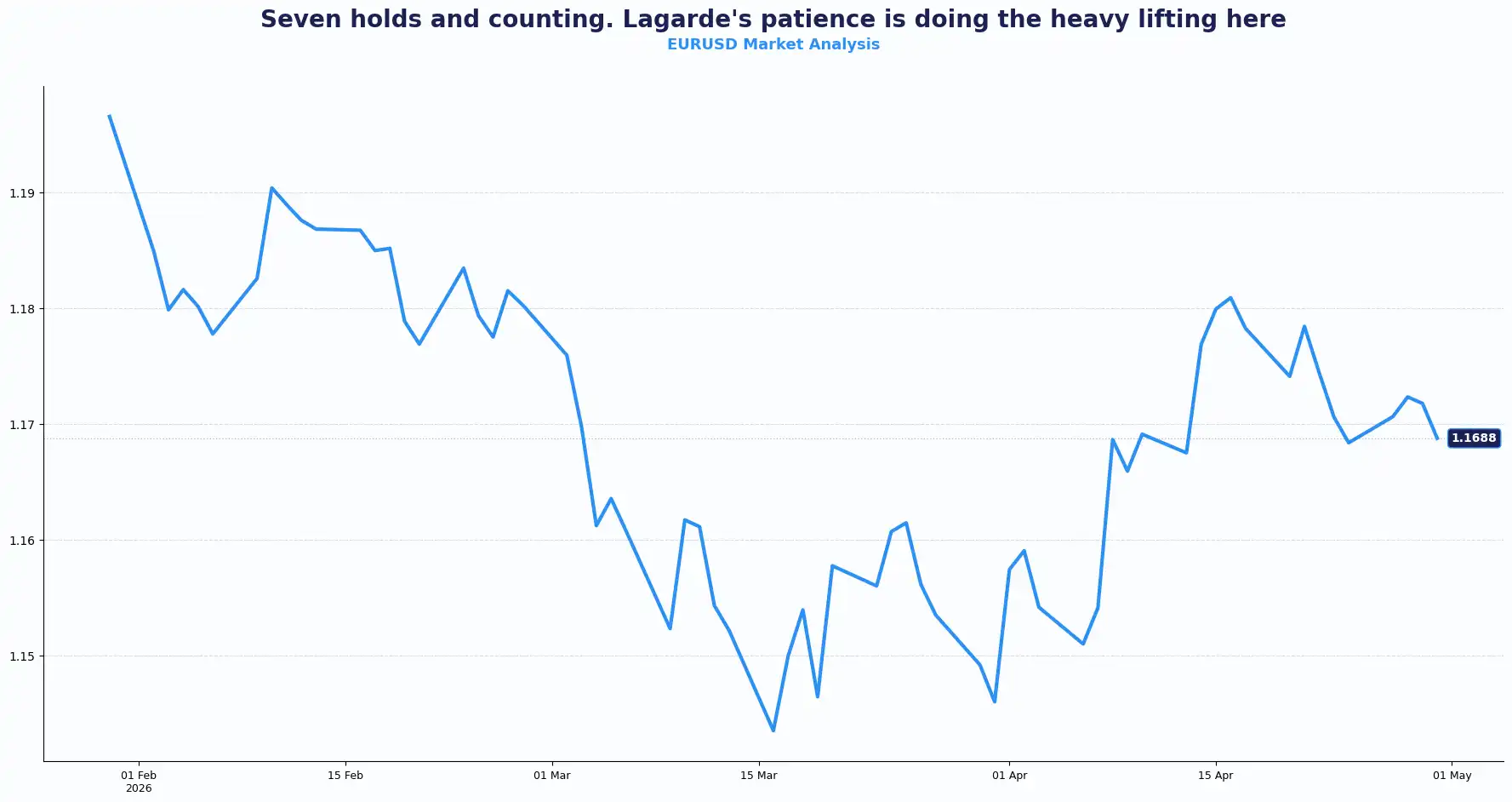

EURUSD 1.1663 | EURGBP 0.8660

The euro drifted to $1.1663 as the ECB prepares for its monetary policy meeting today. Markets expect the ECB to hold the deposit facility rate unchanged at 2.00% and the main refinancing rate at 2.15%, which would mark the seventh consecutive hold. Attention will centre on President Lagarde's guidance. The expectation is that she maintains flexibility, signalling that summer hikes remain a live possibility without committing to a timeline. The "wait and see" framing looks set to hold.

The data backdrop complicates the picture heading in. German retail sales fell 2.0% MoM in March against a consensus of -0.1% and a prior reading of -0.6%. Germany's Q1 GDP came in at 0.3% QoQ and 0.3% YoY, broadly in line with previous figures and forecasts. The Eurozone flash April HICP is expected to print at 2.9% YoY, up from 2.6%, driven by higher energy prices. Core inflation is forecast to ease slightly to 2.2% YoY. Preliminary Q1 GDP figures for the eurozone are also due today.

The gulf between macro fear and micro euphoria has the euro currently lacking momentum. The energy crisis is feeding into transport costs and corporate margins, which are in turn feeding through to headline inflation, but core readings suggest the pass-through is a first-round effect for now. That is precisely the argument underpinning the ECB's anticipated stance today. Whether EUR/GBP continues to price in a sterling discount larger than rate differentials alone would justify the theme tracking across Q2, and Lagarde's tone this afternoon will either widen or narrow that conversation.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1720 and Support sits at 1.1600

USD: Dollar Climbs After the Fed's Most Divided Vote Since 1992

DXY 99.02 | USDJPY 160.55

The dollar climbed to its highest level in more than two weeks after yesterday's Fed decision. The dollar index (DXY) trades around 99.02. The Fed held the federal funds rate in the 3.50-3.75% target range, but the 8-4 vote was the most divided since 1992.

Three regional presidents dissented over language, pointing to an easing bias, arguing that guidance is no longer appropriate given elevated inflation and the uncertainty surrounding oil supply through the Strait of Hormuz.

Chair Powell, in what was almost certainly his final meeting as chair, described policy as being "in a good place" and said the Fed would wait and see how conditions evolve. He confirmed he would stay on as a Fed governor, stepping into the seat vacated by Stephen Miran, a Trump loyalist who voted for a rate cut. Some analysts note Powell may align with the hawkish wing of the board to resist pressure from incoming chair Kevin Warsh and the White House to cut rates.

The hawkish lean sent two-year and ten-year Treasury yields to their highest since the end of March. The dollar gained broadly, topping 160 yen for the first time during this episode of the conflict.

Today's data slate includes the first estimate of US Q1 GDP, with consensus at 2.3% annualised against a prior reading of -0.5%, alongside core PCE, personal spending figures for March, and initial jobless claims. Friday brings the ISM Manufacturing PMI for April. The BEA's first GDP estimate typically carries the most market weight; subsequent revisions tend not to move the needle.

The dollar is on course for a 0.8% loss in April despite the recent bid, having given back gains made on optimism over a potential resolution to the Iran conflict earlier in the month.

Other Currencies: Yen Breaks 160, Antipodeans Hold Steady

AUDUSD 0.7121 | NZDUSD 0.5831 | GBPJPY 216.22

The yen has broken above 160 per dollar, sharpening intervention risk. The Japanese currency has lost more than 2% since the conflict began on 28 February, and short yen positioning has reached its highest level in nearly two years. Japan's energy import exposure and the current impasse in the Middle East make the Ministry of Finance reluctant to deploy intervention reserves too early. Tokyo CPI for April is due tomorrow, providing a read on inflation.

The Aussie holds at $0.7121 and the New Zealand dollar at $0.5831, both broadly steady. Brent Crude's move towards four-year highs adds upside risk to inflation forecasts across commodity-importing economies. A short-lived oil spike is one thing. A sustained Hormuz disruption could change cost structures, transport margins, and central bank reaction functions in ways that are harder to look through, and with the BoE and ECB still to speak today, that calculus sits front and centre.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBPUSD | 1.3463 | Bearish bias |

| EURUSD | 1.1663 | Soft |

| EURGBP | 0.8660 | Bullish |

| USDJPY | 160.55 | Bullish |

| GBPJPY | 216.22 | Elevated |

| AUDUSD | 0.7121 | Rangebound |

| NZDUSD | 0.5831 | Rangebound |

Market Lookahead

Thu, 30 April

- BoE Bank Rate decision

- ECB Rate on deposit facility

- US CPI and Q1 GDP

Fri, 01 May

- US ISM Manufacturing PMI

- Tokyo CPI (APR)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. Forward contracts can help businesses manage foreign exchange exposure by providing greater certainty over future exchange rates, although they may also mean that businesses do not benefit from favourable exchange-rate movements. Businesses should consider their individual circumstances and speak with their dealer to understand how forward contracts may support their specific foreign exchange requirements. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.