Hot US Inflation and UK Gilt Spike Grip FX

8 min read

Share

US inflation runs hot, UK gilts spike to 2008 highs, Starmer's grip slips and Trump lands in Beijing. The dollar firms while geopolitical and domestic uncertainty bears down on sterling. US-Iran peace talks stall and FX pairs are feeling it.

GBP: Sterling Under Siege, Politics Meets Gilts

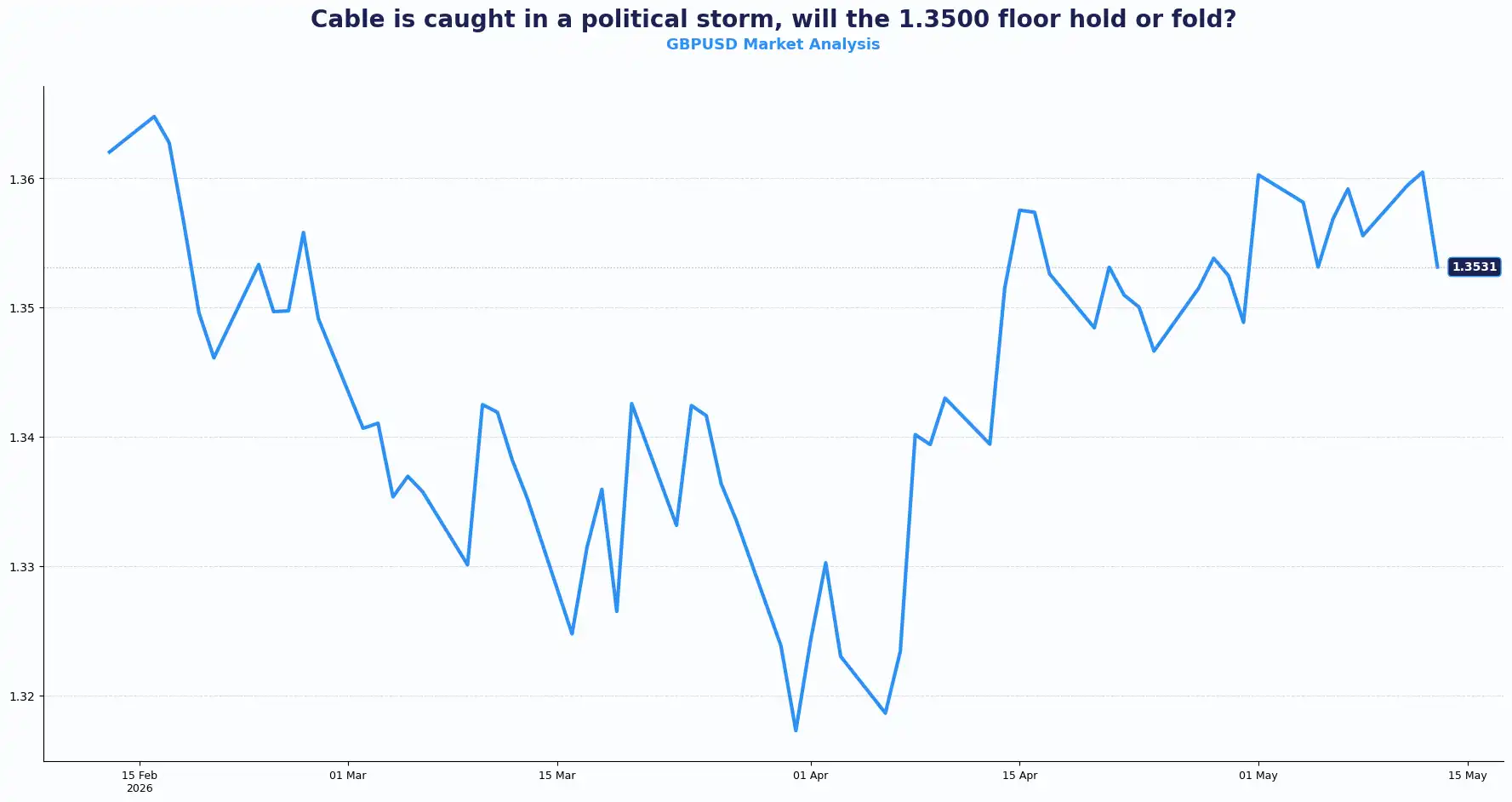

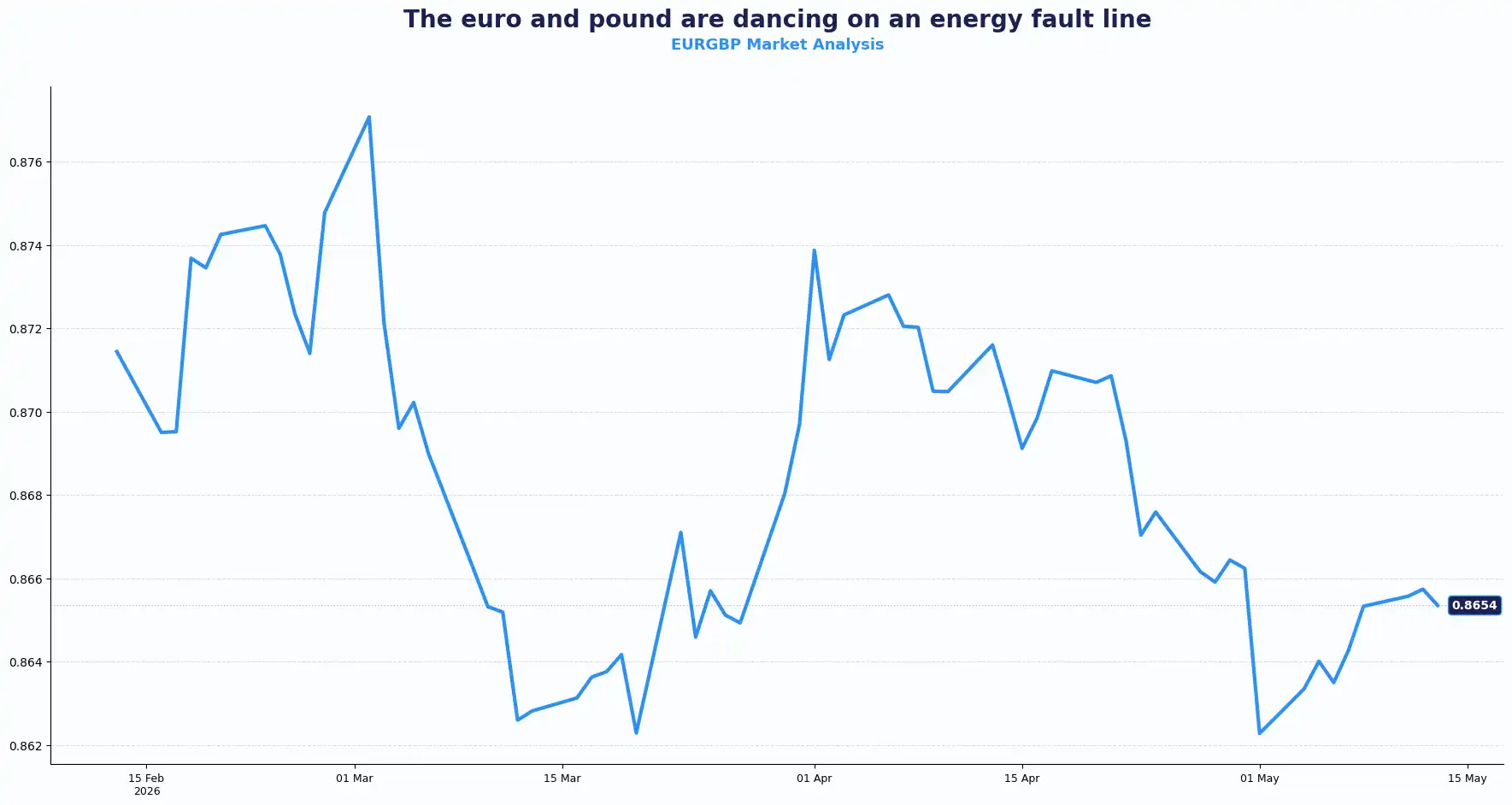

GBPUSD 1.3531 | EURGBP 0.8654

Sterling holds just above the $1.3500 psychological floor, but the grip is fragile.

The Labour Party's catastrophic local election performance last week, losing over 1,400 council seats to Reform UK and surrendering Wales for the first time in a generation, has pushed Prime Minister Keir Starmer to the political cliff edge. Four junior ministers have already quit. Cabinet support, however, is clearly split , with reports that Home Secretary Shabana Mahmood is among those pressing him to set a departure timetable.

Markets place the probability of Starmer facing a leadership election by September at 35%, with a further 25% chance of an orderly transition if he agrees to stand down by then. That would leave sterling pricing with a deeply uncomfortable political discount.

The succession question matters as much as the timing. Health Secretary Wes Streeting, a centrist, represents the softest landing for UK assets. Markets anticipate that he would likely loosen fiscal policy only modestly. A Burnham or Rayner premiership, both perceived as significantly more willing to expand borrowing, could put the long end of the gilt curve under further pressure.

UK borrowing costs already hit their highest level since 2008 on Tuesday. Consensus suggests 10-year gilts look increasingly likely to trade in a 5-5.25% range, with scope for a spike higher should a left-leaning successor emerge. Bear steepening, which is gaining traction, only adds to GBP's downside risk profile.

Eurozone exposure to the same Strait of Hormuz supply shock caps the upside in EUR/GBP for now, keeping the cross in a relatively contained range, though GBP's domestic political drag means the cross tilts marginally to the upside.

Tomorrow brings UK March GDP, preliminary Q1 GDP, Industrial Production, and Manufacturing Production. A miss on any of these in the current political climate will do the GBP no favours at all.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3600, 1.3675 and Support sits at 1.3500, 1.3450

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700, 0.8740 and Support sits at 0.8620, 0.8580

EUR: Euro Holds Firm Before GDP Data

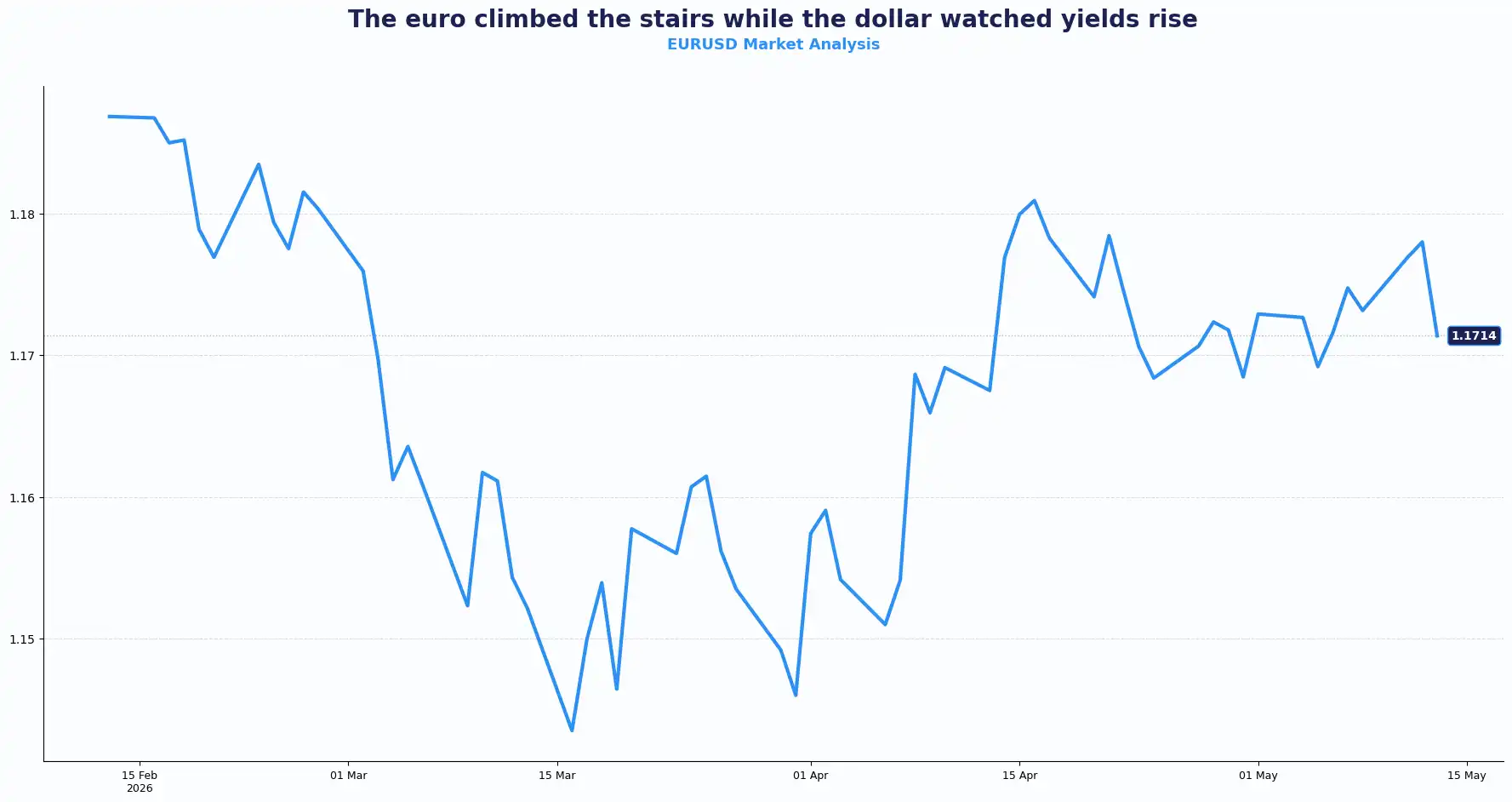

EUR/USD 1.1714

The euro holds in familiar territory mid-session, with pan-European futures nudging higher: Euro Stoxx futures up 0.6%, DAX futures up 0.4%, and FTSE futures up 0.5%, signalling a cautious but constructive tone at the open.

The Eurozone's structural vulnerability to the Middle East supply shock is currently the main constraint on the EUR/USD pair’s upside. With the Strait of Hormuz still effectively closed following US and Israeli strikes on Iran in late February, and Brent settling near $108/bbl, European energy import costs are rising sharply. The ECB now faces a familiar and uncomfortable bind: energy-driven inflation stalling disinflation progress, while growth signals stay uninspiring.

Wednesday's Eurozone Q1 GDP print is the session's key data release. Consensus looks for +0.1% QoQ and +0.8% YoY, a technically positive but underwhelming set of numbers. Preliminary Q1 employment change data drops alongside it. March Industrial Production rounds out today’s data release schedule.

ECB Governing Council member Joachim Nagel pushed back against the idea of central bank silence, noting that monetary policy does not require policymakers to remain silent. The comment carries some weight given market speculation around the ECB's next move, though the energy shock has substantially narrowed its room to cut.

The EUR/USD pair’s upside remains capped by the energy import drag, the prospect of sluggish Eurozone growth, and a dollar finding firm footing amid rate-hike repricing. A beat on the Eurozone’s GDP figures tomorrow could provide a modest lift. A miss, against this energy backdrop, would weigh on the euro.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1780, 1.1830 and Support sits at 1.1700, 1.1640

USD: Hotter CPI, New Fed Chair, Trump Lands in Beijing

DXY 98.31 | USDCNY 6.79

The dollar seems to be off to a good start on Wednesday, reigning as the ultimate safe haven for markets. With the Middle East mired in stalemate, Donald Trump heads to Beijing to meet Xi Jinping, seeking a deal to "open up China." This geopolitical theatre, combined with a scorching US CPI print, has fundamentally shifted the Fed’s trajectory.

April’s US CPI landed at +3.8% YoY in line with expectations on the headline, but the core print surprised to the upside at +2.8% YoY v/s +2.7% expected, and +0.4% MoM v/s +0.3% expected. Chicago Fed President Goolsbee did not dress it up: "CPI was worse than what we were expecting today and definitely worse than what it should be." The services component, he added, was "unexpectedly disappointing," and the Fed cannot lower mortgage rates until the inflation beast is tamed.

The oil shock doesn't seem to be going anywhere, yet. Brent has been above $100 since late February, following US and Israeli strikes on Iran, which is the primary driver of inflation. The effective closure of the Strait of Hormuz pushed energy prices sharply higher, embedding them in a monthly CPI print that is now running at its hottest pace since May 2023. Goolsbee also flagged that “once the war ends, oil should fall back as fast as it rose, but until then, both sides of the Fed's mandate are moving in the wrong direction.”

The Fed’s rate path has repriced dramatically. Investors have priced out cuts entirely for 2026. Probability of at least a 25bp rate hike at the December FOMC has risen to over 35%, up from below 22% earlier in the week. Treasury yields have surged; both two year and ten-year yields climbed.

Wednesday also delivered a historic institutional shift. The Senate confirmed Kevin Warsh to the Fed's Board of Governors in a 51-45 vote. Warsh, who served on the Fed from 2006 to 2011 and built a reputation as an inflation hawk, stated his intention of "regime change" at the Fed, tightening coordination with Treasury, pursuing balance sheet reduction, and adding an institutional uncertainty premium to rate pricing on top of the existing inflation shock.

Atlanta Fed interim president Venable struck a careful balance, saying now is neither the time to cut nor the time to hike: "best to wait and see." But with inflation heading in the wrong direction and the Middle East conflict showing no sign of resolution, the patience of even the most measured voices at the Fed will be tested.

On diplomacy, Trump departed for Beijing on Wednesday, the first US presidential visit to China since Trump's own 2017 trip. He arrived accompanied by a cohort of corporate leaders, Nvidia CEO Jensen Huang among the last-minute additions to the delegation. The agenda centres on trade détente, rare-earth export curbs, and, inevitably, Iran, though Trump told reporters at the departure ropeline that he does not think he needs Beijing's help with Tehran. Analysts broadly expect the bar for "success" to be low: a continuation of the trade truce and a broadly functional bilateral tone should be sufficient to count as a win for both sides. USD/CNH traded around 6.79, near its strongest since February 2023, reflecting cautious optimism ahead of the summit.

US PPI for April is also due later today. Consensus looks for headline +4.9% YoY (versus +4.0% in March) and core +4.3% YoY (versus +3.8% prior). A hotter print could reinforce rate-hike expectations at the Fed and add further support to the dollar.

Asia & Other Pairs

USDJPY 157.70 | GBPJPY 213.59 | AUDUSD 0.7238 | NZDUSD 0.5944

The yen steadied around $157.70 after Tuesday's sudden spike, which stoked speculation of a "rate check" by Japanese authorities, an action that typically precedes intervention. US Treasury Secretary Scott Bessent added verbal support, reiterating that both Washington and Tokyo view excess currency volatility as undesirable. The comment offered Tokyo implicit backing for its recent round of intervention. With the USD/JPY pair holding above 155, Japanese authorities will continue to watch closely.

The Australian dollar held near $0.7238 and the New Zealand dollar around $0.5954, both broadly flat. The AUD's near-term trajectory depends heavily on risk appetite, and right now, hot US inflation, elevated oil, and geopolitical overhang are headwinds for risk-sensitive currencies.

In Seoul, Korean shares told a dramatic intraday story. The KOSPI fell as much as 3.2% after a renowned electronics company failed to reach a pay deal with its South Korean labour union. Over 50,000 workers now threaten a full strike with consequences for AI chip and semiconductor production. For the broader AI spending narrative, where big tech's seemingly price-insensitive capex has been a key growth driver, any disruption to chip supply chains carries real macro implications and inflation. If AI companies continue spending aggressively regardless of cost, input price pressure works both ways.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3531 | Bearish below 1.3600 |

| EUR/GBP | 0.8654 | Bullish above 0.8620 |

| EUR/USD | 1.1714 | Bullish above 1.1700 |

| USD/JPY | 157.70 | Bullish above 156.80 |

| GBP/JPY | 213.59 | Volatile bullish |

| AUD/USD | 0.7238 | Neutral bullish |

| NZD/USD | 0.5944 | Neutral |

| USD/CNY | 6.79 | Strong |

Market Lookahead

Wed, 13 May

- Eurozone Employment Change data

- Eurozone Gross Domestic Product Q1

- Eurozone Industrial Production s.a. (Mar)

- US Producer Price Index (Apr)

Thu, 14 May

- UK’s Gross Domestic Product Q1

- UK Industrial Production s.a. (Mar)

- US Retail Sales

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.