Starmer's Crisis Hits the Pound Amid Stalling Peace Talks

8 min read

Share

Oil climbs again as Iran ceasefire talks stall, Trump calling it "on life support" rattled FX and markets. Starmer's rebellion hits sterling hard. The euro softens on energy risk, the dollar holds its safe-haven bid, and all eyes turn to today's US CPI print as rate cut hopes continue to fade.

GBP: Sterling Feels the Heat

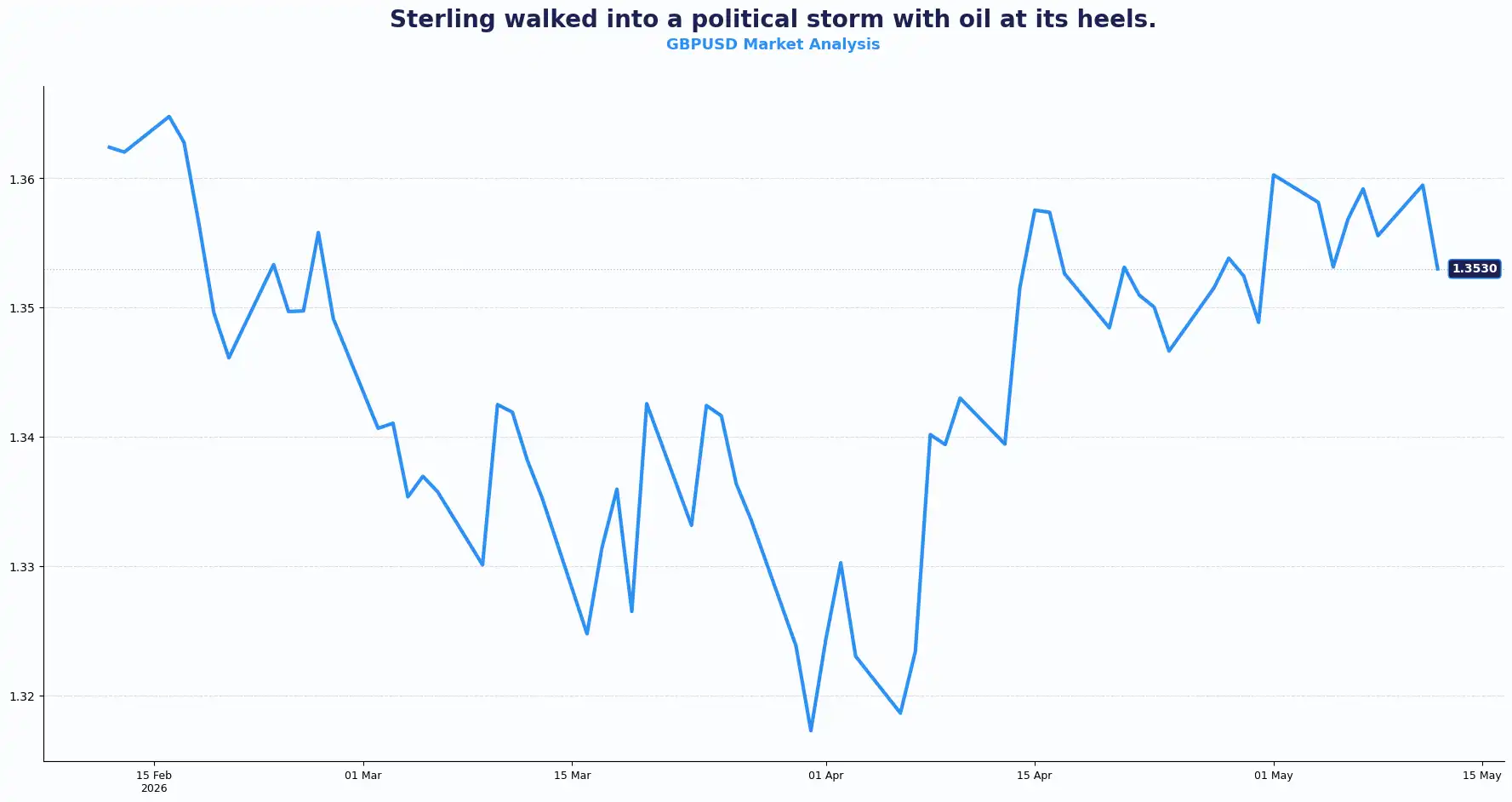

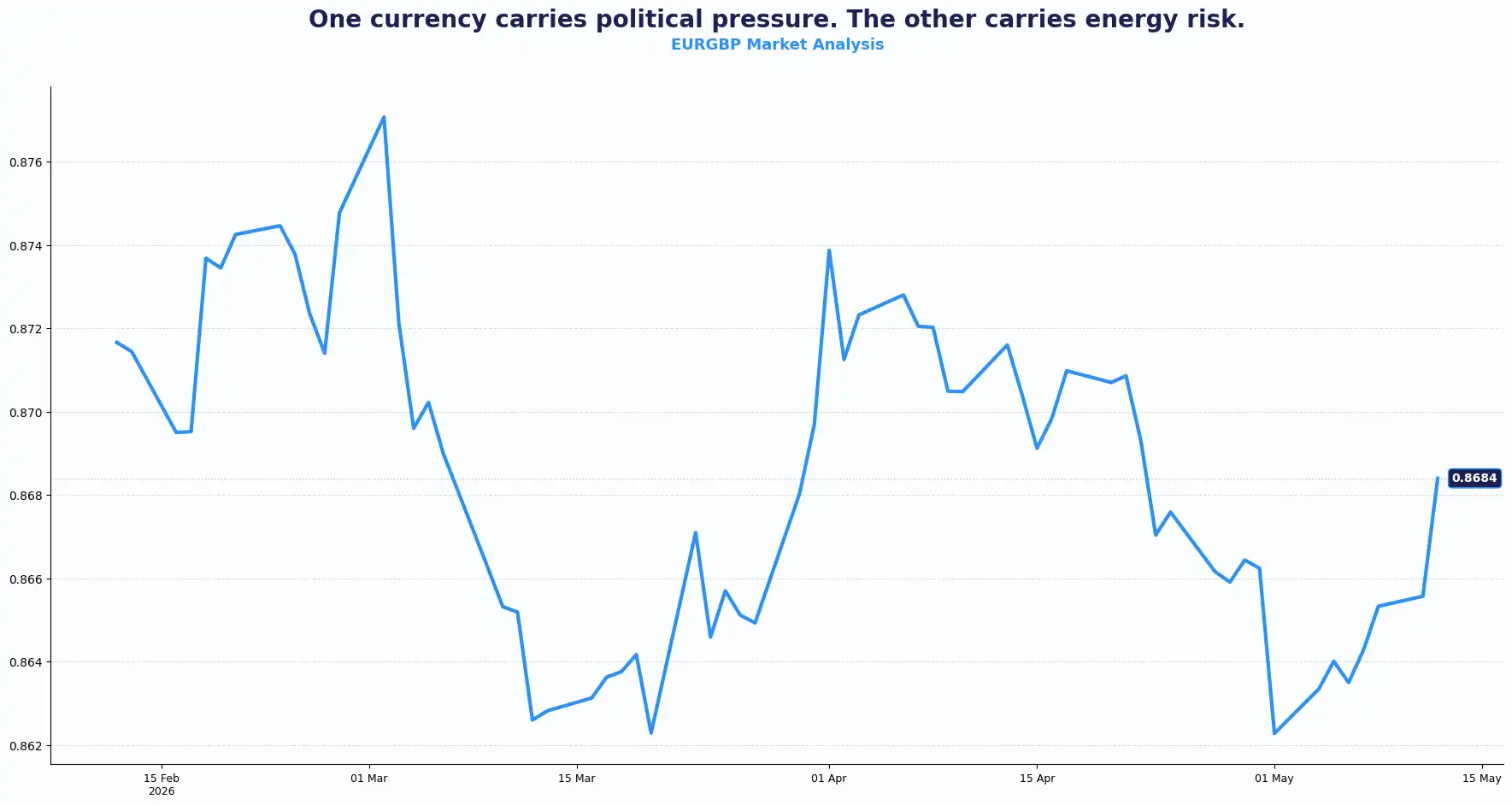

GBPUSD 1.3530 | EURGBP 0.8680

Sterling lost momentum as traders weighed rising oil prices against fresh political uncertainty in the UK. The political vacuum pushed GBPUSD to 1.3530 and saw EURGBP climb to 0.8680.

Gilts faced a heavy selloff after Prime Minister Keir Starmer failed to silence a growing rebellion within the Labour Party. Three ministerial aides stepped down, and over 60 lawmakers now demand his resignation following bruising local election losses. Starmer addressed the party on Monday, telling doubters he would prove them wrong and reiterating his intention to stay. The market read it differently.

The pound softened. Political uncertainty of this kind does not sit well with a currency that already faces structural headwinds from elevated domestic inflation and a Bank of England (BoE) navigating a difficult path.

The key issue for sterling watchers is not just whether Starmer survives, but who comes next if he does not. His likely successors sit further to the left wing of the party, and that matters for spending expectations and fiscal credibility. The current backdrop might lack to provide a floor for the pound, pointing to both the political situation and seasonal factors, a prospect that leaves sterling vulnerable on a relative basis against G10 peers.

BoE MPC member Megan Green warns of persistent inflation. Greene warned that inflationary persistence had already begun to show before the Iran conflict intensified. She flagged that consumers are likely to feel the pinch of inflation once it clears 3.5%, the threshold that previously attracted attention, which sat at 4%. She also cautioned that waiting for second-round inflationary effects to materialise before acting risks a late policy response.

BoE faces a challenging situation, balancing inflation pressures that remain sticky while consumer demand and labour conditions continue to soften. Bond yields across the UK climbed as traders pushed back expectations for rate cuts. Sterling initially found support from higher yields, but political concerns quickly capped gains.

The pound also faces a seasonal headwind. Summer liquidity tends to thin out. Political headlines can therefore trigger sharper currency swings than usual. Energy costs, political noise and central bank uncertainty now pull sterling in different directions at once. Upcoming macro data on Thursday could provide a catalyst for Sterling ‘s near-term direction.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3640 and Support sits at 1.3520

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700 and Support sits at 0.8625

EUR: Euro Slips as Energy Risk Returns

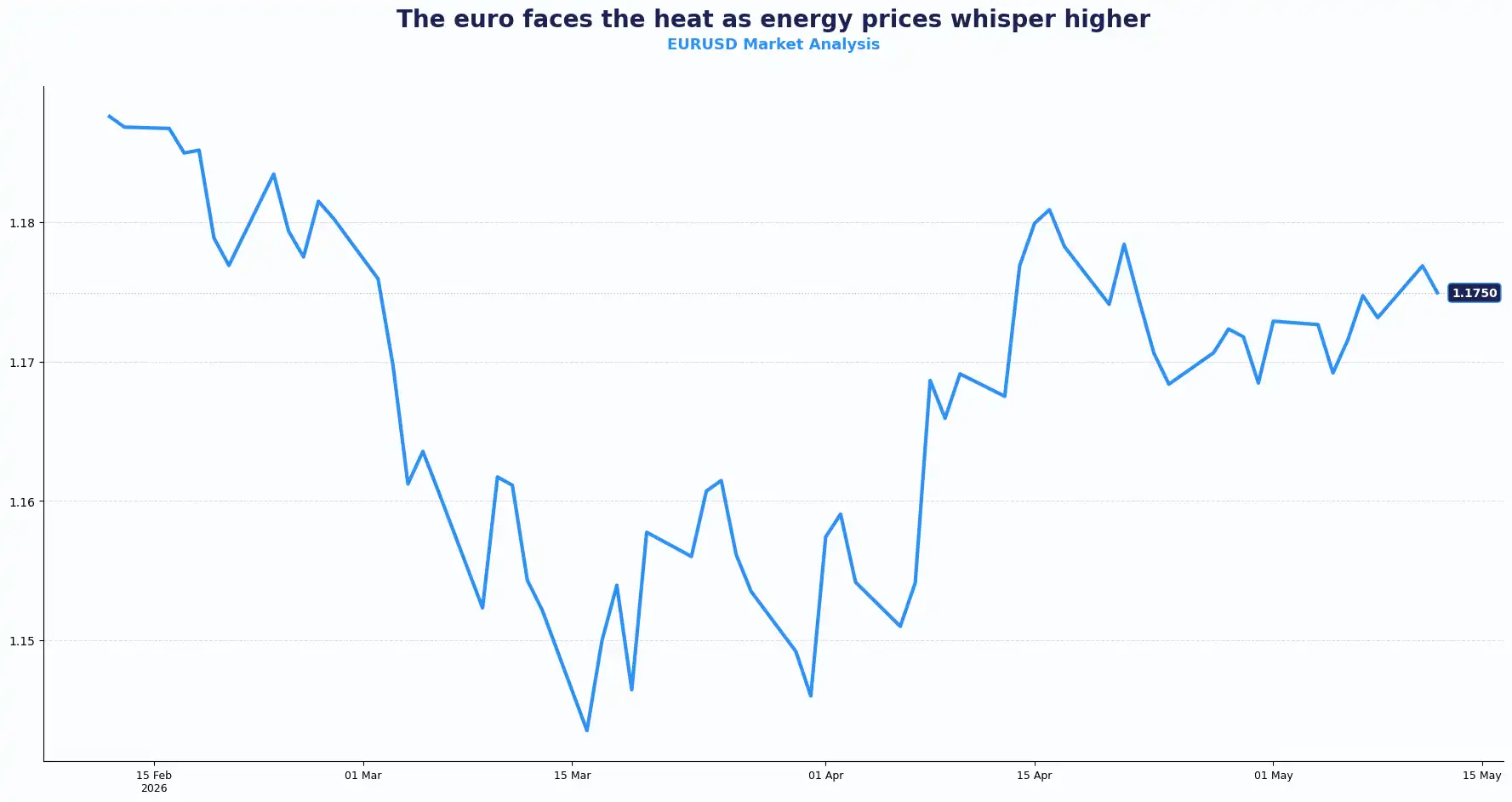

EURUSD 1.1750

The euro eased, with EUR/USD trading near 1.1750, as traders reassessed Europe’s vulnerability to higher energy prices. That said, the broader picture at the European Central Bank (ECB) gives the single currency more structural support than sterling can claim right now.

Eurozone rate pricing has shifted decisively. Markets are fully pricing two 25bps hikes across the ECB's next three meetings through to September and with roughly a 75% probability of a third by year-end, creating a stark contrast with the Federal Reserve’s hawkish pause.

Germany’s final April inflation data landed in line with forecasts. CPI printed at 0.6% MoM and 2.9% YoY. Harmonised inflation also held at 0.5% MoM and 2.9% YoY. There were no surprises, which in the current environment is a relative source of comfort. High HICP readings generally support the euro, but the looming supply shock from the Middle East complicates the ECB’s path.

But that steady reading brings a sharper question into focus. Europe is an energy-dependent region, and the Strait of Hormuz has been effectively closed for ten weeks now. The absence of an inflation shock so far does not mean the pressure is absent; it means it likely has not fully transmitted yet. European equity futures are pointing to a softer open, and the pan-European STOXX 600 is still trading roughly 4% below pre-war levels, lagging global peers that have recovered on the back of the AI rally.

The ZEW survey for Germany and the eurozone is due later today, offering a read on economic sentiment in May. Although ZEW sentiment surveys offer a glimpse into the current economic mood, tomorrow’s Eurozone GDP and industrial production data could provide better insights into growth. The divergence between the ECB and the Fed remains the primary driver for the EUR/USD pair.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1815 and Support sits at 1.1700

USD: Dollar Finds Support Ahead of CPI

DXY 98.16

The dollar index trades at 98.16, holding a modest bid as hopes for a Strait of Hormuz resolution fade once more.

President Trump described the ceasefire with Iran as "on life support" after Tehran's response to the U.S. peace proposal made it clear the two sides remain far apart on nuclear development. The ceasefire that has been in place since 7 April has done enough to stabilise investor sentiment at the margin, but the lack of diplomatic progress is beginning to register, particularly in bond markets and oil prices. Bond yields rose across the globe, led by the gilt selloff described above. Ten-year Treasury yields hold around 4.42%.

Oil prices crept higher, fanning inflation fears just as the U.S. prepares to release its April CPI report. Headline inflation is expected to hit a hot 3.7% YoY, cementing the view that the Fed might end up keeping rates higher for longer.

The shift in sentiment is profound. Before the Iran war, investors expected two rate cuts this year; they have now priced those out entirely. Any upside surprise in core inflation, potentially driven by energy price spillover into airfares and food, will likely propel the dollar further and potentially open the discussion around hikes, a scenario that was not on the table six months ago.

Also due today is the U.S. monthly budget statement for April. The consensus sits at a surplus of $157.2 billion, a sharp swing from March's $164 billion deficit. A surplus reading has historically supported the dollar at the margin.

Treasury Secretary Scott Bessent is in Asia, meeting with officials in Japan and South Korea. His Japanese counterpart noted strong coordination on recent market moves, including exchange rates, though stopped short of explicitly endorsing currency intervention. The dollar trades at 157.10 against the yen, not far from levels that have previously attracted verbal pushback from Tokyo.

Trump's visit to China is scheduled for Wednesday. Expectations are deliberately low. The consensus view is that a successful outcome looks like no new tariffs, no new export controls, and perhaps a handful of symbolic trade gestures; agricultural purchases, aircraft orders, or signals on rare earths. Anything more would be a genuine surprise. Stability over progress is the baseline.

The Chinese yuan firmed slightly to 6.791 per dollar, its strongest level since February 2023. Beyond any tactical catalyst from this week's summit, there is a structural case for yuan appreciation that several analysts argue extends well past the diplomatic optics.

Antipodeans and the Yen, Watching and Waiting

AUDUSD 0.7223 | NZDUSD 0.5948 | USDJPY 157.10 | GBPJPY 213.46

The Australian and New Zealand dollars retreated as Gulf uncertainty weighed on risk appetite. The Aussie dipped to 0.7223, while the kiwi fell to 0.5948.

Both currencies eased as Gulf war uncertainty persisted, but the underlying picture for the Antipodeans is not straightforwardly bearish. When signs of diplomatic dialogue surface, risk-on flows have lifted both the Aussie, in particular, which has been testing the top of its recent range against the dollar. There is a broad view in the market that many participants are waiting for the current crisis to resolve before rotating out of the dollar more decisively.

The Aussie acts as a barometer for global risk. While stability reports occasionally buoy the currency, the lack of progress in Washington-Tehran negotiations keeps a lid on gains.

Japan's ten-year government bond yield rose to a 29-year high of 2.54% ahead of an auction later today. The Bank of Japan's April meeting summary reinforced a hawkish tilt among board members, keeping the door open to a June rate hike.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3530 | Soft bearish |

| EUR/GBP | 0.8680 | Bullish EUR |

| EUR/USD | 1.1750 | Mild bearish |

| GBP/AUD | 1.8778 | Bearish GBP |

| AUD/USD | 0.7223 | Bullish AUD |

| NZD/USD | 0.5948 | Neutral-bullish |

| USD/JPY | 157.10 | Bullish USD |

| GBP/JPY | 213.46 | Volatile bullish |

| USD/CNH | 6.7910 | Bearish USD |

Market Lookahead

Tue, 12 May

- Germany & Eurozone ZEW Survey - Current Situation & Economic Sentiment

- Australia's Budget Release

- US Consumer Price Index (Apr)

- US Monthly Budget Statement (Apr)

Wed, 13 May

- Eurozone Employment Change data

- Eurozone Gross Domestic Product Q1

- Eurozone Industrial Production s.a. (Mar)

- US Producer Price Index (Apr)

Thu, 14 May

- UK’s Gross Domestic Product Q1

- UK Industrial Production s.a. (Mar)

- US Retail Sales

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.