Back to Square One: Australia Wipes Out 2025's Rate Cuts

8 min read

Share

Project Freedom stalls on day one as US and Iran exchange fresh Gulf strikes and the Strait stays shut. BoE, ECB and Fed members speak today on the back of last week's rate decisions. Safe-haven demand keeps the dollar steady. GBP and EUR on the back foot.

The RBA hikes to 4.35%. Three hikes in 2026 have fully unwound three cuts in 2025. Same number, heavier weight; sets the tone for everything that follows: Inflation is winning rounds it was supposed to have already lost, and central banks are not done fighting.

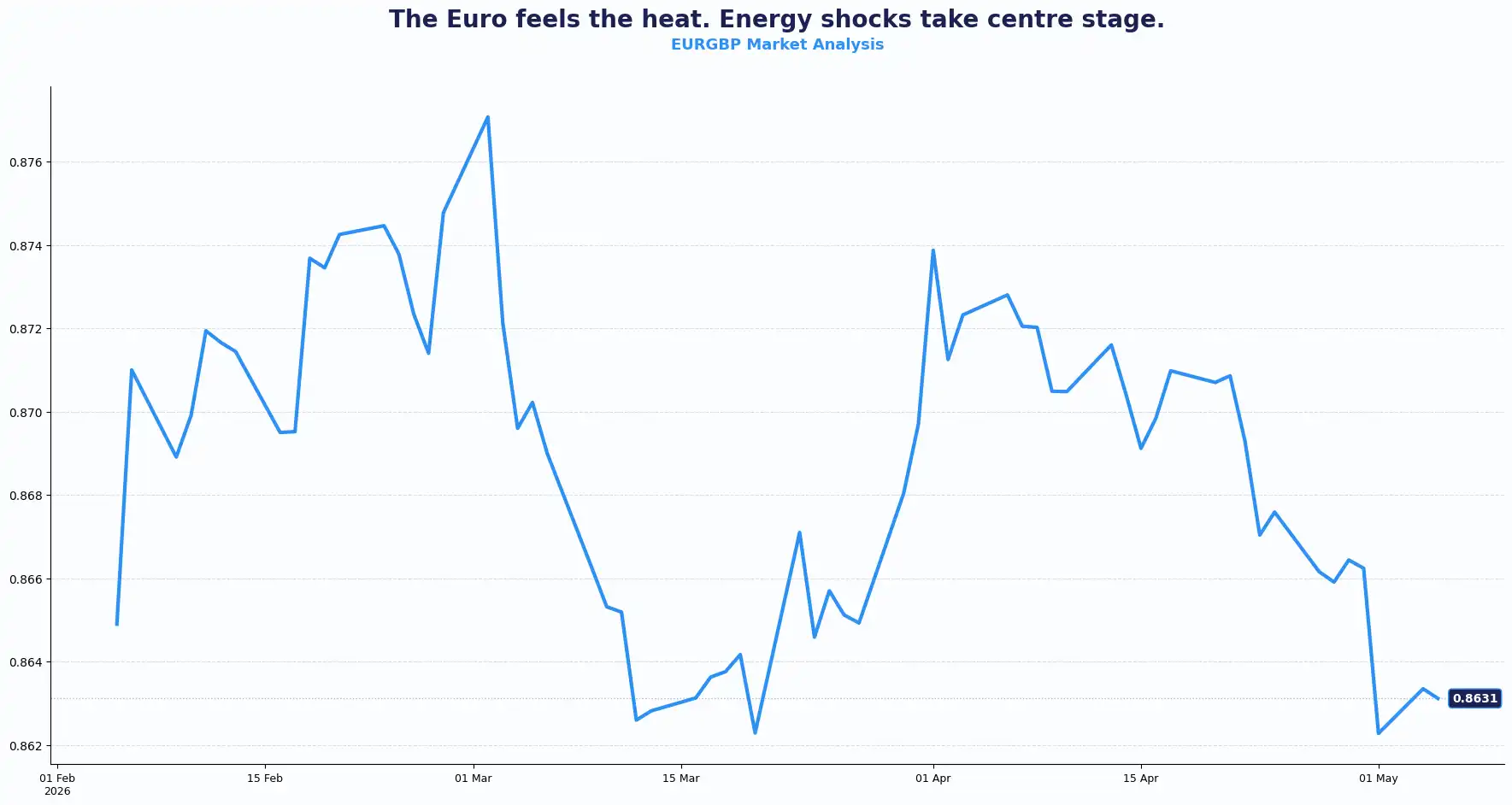

GBP: The Pound Balancing Inflation and Politics

GBPUSD: 1.3520 | EURGBP: 0.8640 | GBPAUD: 1.8941

GBP/USD trades near 1.3520 after easing from recent highs. Price holds above the 100-day EMA, keeping the broader upside structure intact, though pressure mounts.

Energy shocks from the Strait of Hormuz closure have unleashed a global inflation flare. Crude prices have exceeded $100 a barrel since February. UK CPI sits at 3.1% projected for Q2, edging higher through Q4, above target, with the pathway back to 2% looking considerably less clean than it did six months ago.

The Bank of England (BoE) held its bank rate steady at 3.75% last week, with a unanimous vote, and the MPC suggested future rate hikes might prove necessary but currently avoids explicit pre-commitments. The BoE faces a difficult trade-off between curbing price growth and supporting a fragile economy. Governor Andrew Bailey highlights the risk of "forceful tightening" if energy price shocks continue to push inflation higher.

The hawkish framing suggests the BoE isn't cutting anytime soon. The divergence with the European Central Bank (ECB), which kept its deposit rate at 2.0% and faces deeper structural exposure to the energy shock, gives sterling a policy edge. The EUR/GBP trades near 0.8640. Eurozone growth faces a sharper drag from elevated energy costs than the UK, limiting the ECB's room to tighten aggressively even as inflation runs hot.

Several central bank speakers from the BoE, ECB, and Federal Reserve (Fed) are due for the session, following last week's meetings that saw a distinct hawkish tilt across the board.

The more immediate risk for sterling is domestic. Markets currently price the probability of Starmer leaving office at 66% before the end of 2026. A poor result could trigger a leadership challenge, though any formal contest is unlikely to arrive before the September party conference. A cabinet reshuffle post-Thursday looks probable regardless. Political noise of this kind rarely drives sustained GBP moves, but it adds a layer of near-term uncertainty that traders will price cautiously.

Wednesday brings the S&P Global Composite and Services PMIs for April, with consensus at 52 on both, unchanged from the prior print. A reading above 50 signals expansion in the services sector, which has historically been supportive of sterling. Match the consensus, and it's a non-event. A miss below 50 changes the conversation.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3610 and Support sits at 1.3515

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8670 and Support sits at 0.8600

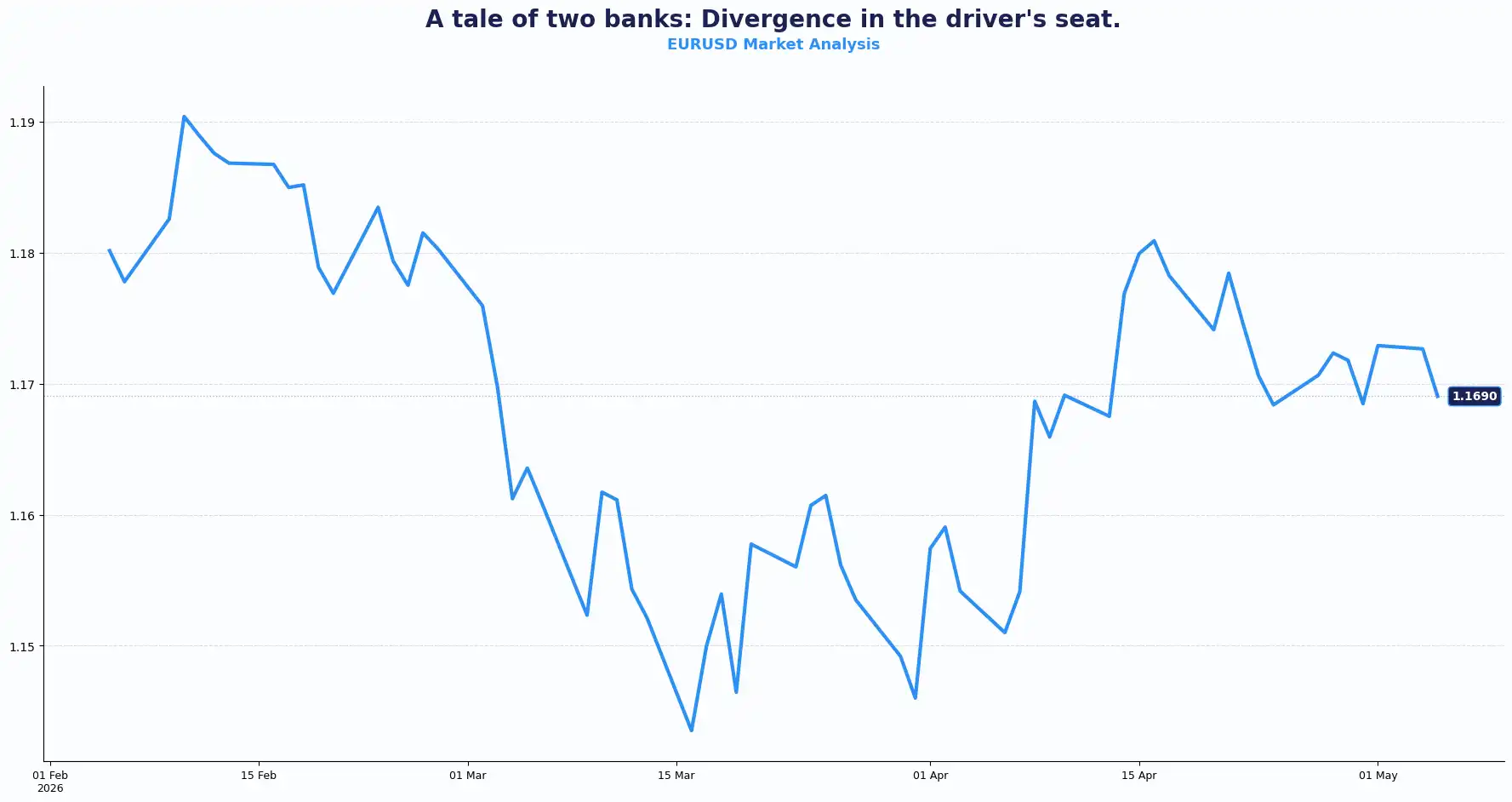

EUR: The Euro Grapples with Energy Exposure

EURUSD: 1.1679 | EURAUD: 1.6362

The euro continues to nurse overnight losses. The EUR/USD pair sits at 1.1679. Geopolitics in the Middle East dominate the price action. The euro struggles to maintain gains, reflecting the eurozone’s vulnerability to the energy supply crisis and renewed hostilities in the Gulf, which weigh on the single currency.

As one analyst put it: de-escalation in the Middle East is the single biggest upside catalyst for the euro right now. A durable ceasefire or reopening of the Strait would shift the calculus materially. Until then, the path of least resistance is sideways-to-lower.

The ECB held its deposit rate at 2.0% last week and signalled that the conflict is pushing near-term inflation higher, but with growth simultaneously under threat, the bank's hands are partly tied. Markets currently price in two rate hikes for both the BoE and ECB over the coming cycle, but the credibility of that path for the ECB is more in question.

Tomorrow brings the HCOB Composite and Services PMI data for Germany and the wider Eurozone. Traders also await the March Producer Price Index (PPI) figures. PPI from Eurostat measures price changes received by domestic producers across all processing stages – a high print is typically seen as EUR-positive, signalling inflationary pipeline pressure that could support a more hawkish ECB stance.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1720 and Support sits at 1.1650

USD: Dollar Safe-Haven Bid Holds Amid Escaling Gulf Tensions

DXY 98.55

The dollar firms as conflict in the Middle East spurs safe-haven demand. DXY, now at 98.55, reflects this flight.

President Trump's "Project Freedom", framed as a humanitarian passage operation, got off to a shaky start. The U.S. and Iran launched fresh strikes in the Gulf on Monday. Both nations struggle for control over the Strait of Hormuz. News of duelling maritime blockades and the stalling of Trump’s new Project has rattled investor sentiment and driven safe-haven flows back into the dollar, keeping risk appetite suppressed.

The dollar currently serves as the primary vehicle for capital preservation during geopolitical crises, as reflected in market sentiment. While investors initially hoped for a humanitarian resolution in the Gulf, the current stalemate suggests a prolonged period of tension. If escalation continues, oil prices will surge. This would weigh on risk assets. Brent futures currently trade at $112.92 per barrel.

The dollar's near-term dynamic is binary. A stalemate or escalation keeps it supported. Any credible peace signal or Strait reopening would see risk appetite recover sharply, and the dollar sell off. For now, that trade remains asymmetric in the dollar's favour.

Geopolitics aside, the fundamental domestic backdrop is also supportive. S&P 500 earnings have been strong: 83% of reporting companies beat EPS estimates, 78.2% beat revenue, with AI-driven tech spending continuing to do the heavy lifting.

The Fed held its rate at the top of the 3.50-3.75% range last week, keeping rates on hold amid energy-driven inflation that complicates the path to cuts. Friday's US NonFarm Payrolls report for April will be the week's most closely watched data. Today also brings the US JOLTS job openings for March.

Pacific Ripples and Asian Dynamics

AUDUSD 0.7149 | NZDUSD 0.5863 | USDJPY 157.28 | GBPJPY 212.64

The Reserve Bank of Australia (RBA) raised the cash rate by 25 bps to 4.35% this morning in an 8-1 board vote; the third straight hike of 2026, effectively reversing all three cuts made in 2025. RBA Governor Michele Bullock acknowledged the hikes are "hurting mortgage holders immensely," but stressed the board will do what is necessary to restore price stability. Headline inflation hit 4.6% in the year to March, and updated RBA forecasts point to further near-term pressure before any easing.

The updated RBA forecasts are striking: GDP growth is projected at 1.9% in Q2 2026, declining to 1.3% by Q2 2027. Unemployment rising from 4.2% now to 4.7% by Q2 2028. Trimmed mean inflation peaking at 3.8% in Q2, only reaching a target of 2.5% by mid-2028. The board's baseline assumes the Strait of Hormuz conflict resolves relatively soon but warned explicitly that a longer closure would force further hikes. Westpac is the outlier in forecasting two more 25bp hikes in 2026, which would bring the cash rate to 4.85%, a level not seen since 2008.

The AUD/USD pair fell on the announcement despite the hike, a classic "sell the news" after the decision was widely anticipated. The pair now sits near the 0.7149 level. Investor attention now turns to Bullock's press conference tone and whether the board signals any pause.

Governments across Asia are scrambling to secure alternative fuel sources as the energy shock drags on, adding pressure to regional currencies and growth outlooks.

The yen at 157.28 per dollar sits near its two-month high, a product of suspected intervention by Japanese authorities. But the structural pressure on the yen remains intact: Japan's ultra-low rates, a wide yield differential with developed-market peers, and mounting fiscal strain all point in the same direction. Suspected intervention has recalibrated the near-term range; it has not resolved the underlying dynamic.

USD/JPY volatility in a 155-160 range looks probable near-term, with authorities likely to lean against a clean break above 160 rather than engineer a durable reversal. Oil is the key variable; if Brent stays elevated or moves higher, yen pressure will build again.

Geopolitical instability and central bank shifts create a high-stakes environment.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3520 | Bullish bias above 1.3515 |

| EUR/GBP | 0.8640 | Range-bound, slight upside |

| GBP/AUD | 1.8941 | Supported, mild uptrend |

| EUR/USD | 1.1679 | Soft, downside pressure |

| EUR/AUD | 1.6362 | Stable, range-bound |

| AUD/USD | 0.7149 | Weak bias, pressured |

| NZD/USD | 0.5863 | Soft, risk-sensitive |

| USD/JPY | 157.28 | Volatile, upward bias |

| GBP/JPY | 212.64 | Strong, follows USD/JPY |

Market Lookahead

Tue, 05 May

- US JOLTS job openings, US ISM Services PMI (Apr)

Wed, 06 May

- UK S&P Global Composite & Service PMI (Apr)

- Eurozone and Germany HCOB Composite and Services PMI (Apr)

- Eurozone Producer Price Index (Apr)

Thu, 07 May

- Germany factory orders (mar)

- Eurozone retail sales (mar)

- US Initial Jobless claims

Fri, 08 May

- German Industrial production & trade balance (Mar)

- US Unemployment rate, Average hourly earnings, NonFarm Payrolls (Apr)

Sat, 09 May

- China Trade balance and import exports CNY AND USD (Apr)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.