The Hormuz Bill Is Finding Its Way to FX Markets

7 min read

Share

Hormuz stayed shut. The market stayed hopeful. Now, oil is at $110, gilts are at post-2008 highs. The G7 convenes in Paris today as Hormuz uncertainty deepens across FX.

GBP: The Political Storm Hitting Cable

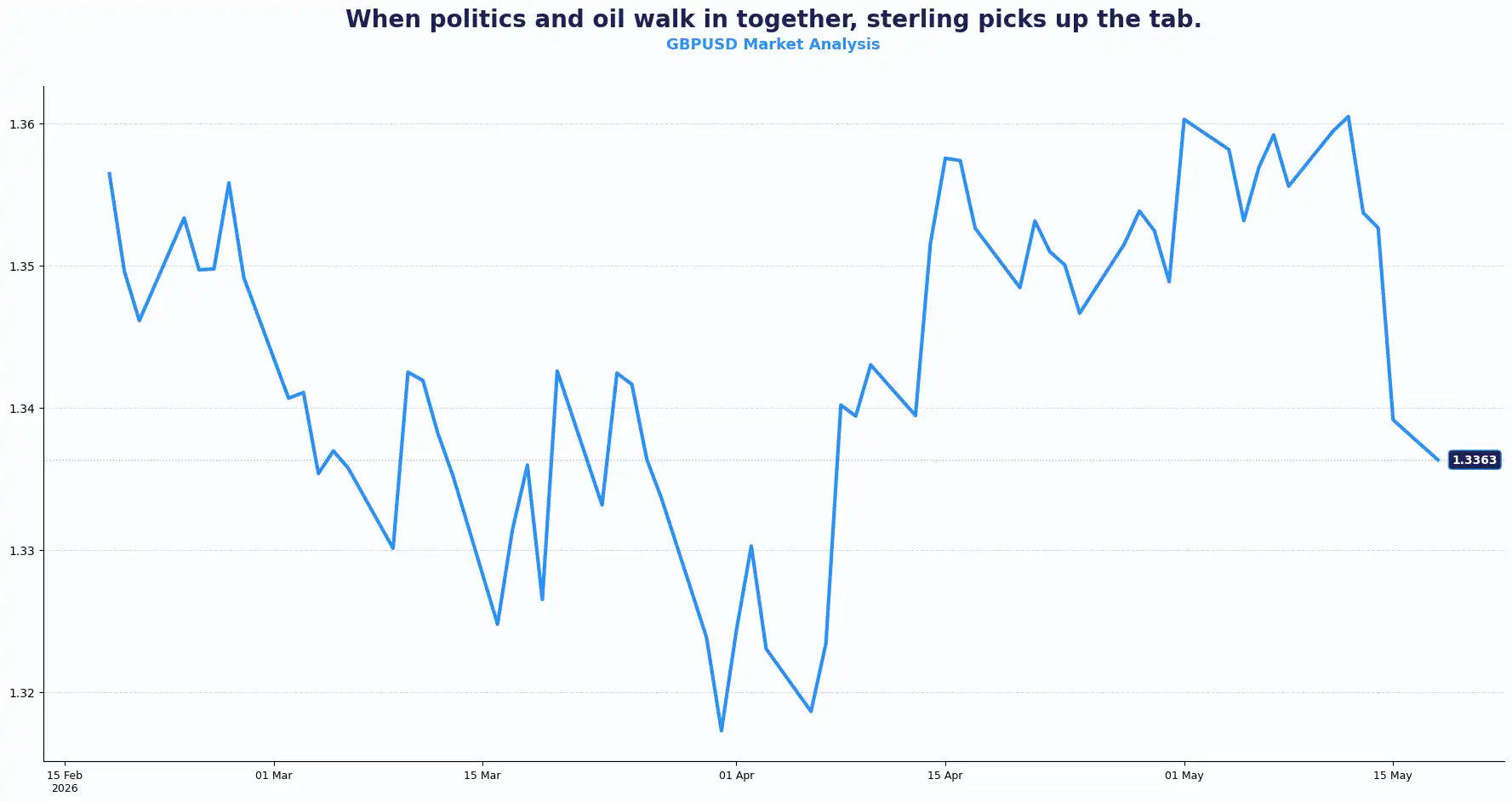

GBPUSD 1.3363 | EURGBP 0.8707

Sterling slid to $1.3311 last week, posting a sharp 2.3% decline as domestic political volatility collided with a brutal bond sell-off. In early European trading, the British pound traded near $1.3320.

A deep global bond rout accelerated on Monday morning. Spiralling energy prices fanned global inflation fears, pushing 10-year UK gilt yields up nearly 3% to 5.19%. This is the highest borrowing cost for the British government since the subprime crisis.

Fears of a sudden leadership change at Downing Street are reflecting this dramatic spike in gilt yields. Market speculation mounts that a managed exit for Prime Minister Keir Starmer will pave the way for Andy Burnham to take over, shifting the UK towards a looser fiscal regime. Bank of England (BoE) Deputy Governor Sarah Breeden highlighted this vulnerability, warning that political unpredictability damages the wider business climate. She cautioned that policymakers should not be "trigger happy" on interest rates. This domestic friction compounds a grim global backdrop; the ongoing closure of the Strait of Hormuz and fresh attacks in the United Arab Emirates threaten to keep crude above $110 a barrel, raising the prospect of a global recession if oil hits $150.

The broader risk-off environment, caused by the Strait closure, global bond selloffs, and surging oil prices, is negatively affecting all risk-sensitive currencies. The pound is particularly impacted because, as a current-account-deficit currency, it is more vulnerable in such conditions.

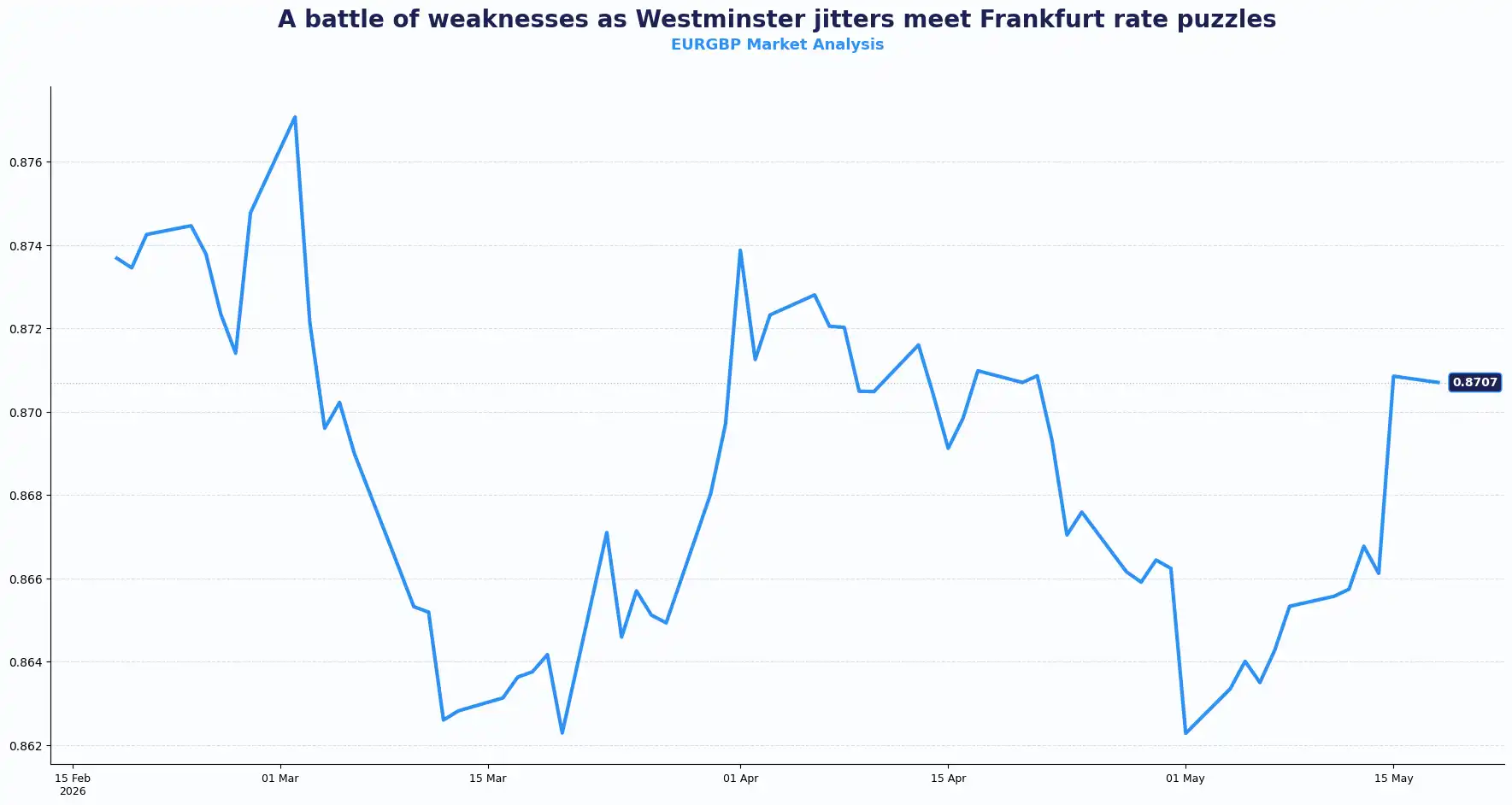

EUR/GBP held at 0.8707, tilted in favour of the euro as relative fiscal credibility favoured Frankfurt over Westminster.

The pound’s pressure stems from intertwined politics, gilt yields, and geopolitics. Investors are closely monitoring oil prices, UK leadership developments, and G7 discussions.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3400 and Support sits at 1.3280

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8780 and Support sits at 0.8700

EUR: Euro Cracks Under Global Risk Aversion

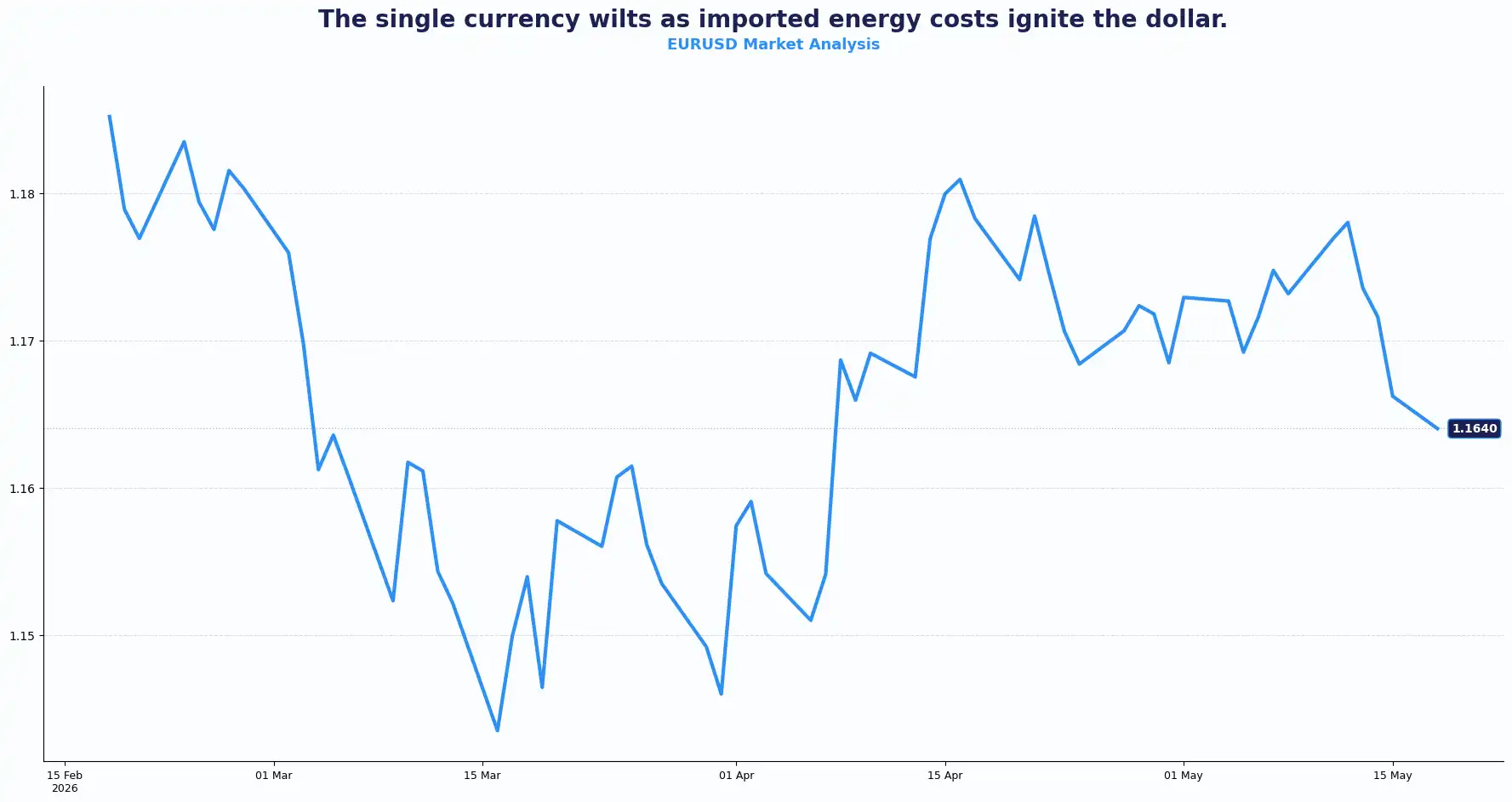

EURUSD 1.1640

The euro depreciated to 1.1640 against the dollar. This level follows a 1.4% loss across the previous five trading sessions. Aggressive safe-haven bidding lifted the dollar across the board on Monday morning. Equities slid globally while fixed-income assets buckled under pressure, as the prospect of extended maritime blockades in the Middle East drained global crude inventories.

This breakdown reflects a stark energy deficit. The US operates as a net energy exporter, securing a structural advantage over continental Europe, which absorbs the full brunt of imported inflation. Although 85% of economists expect the European Central Bank (ECB) to raise its deposit rate by 25 bps to 2.25% in June, these hawkish expectations cannot yet counteract the broader flight to safety.

The shift in ECB pricing provides a counterweight to the dollar bid. Risk aversion drove broad USD demand, but the EUR/USD pair stayed relatively contained compared to sterling, in part because the eurozone does not face the same political uncertainty premium.

The risk, as several analysts noted, is asymmetric: if the Strait of Hormuz closure extends through year-end and recession scenarios unfold, eurozone inflation could approach 10%, and rates would revisit recent peaks. At that point, ECB hikes become stagflationary rather than stabilising and the EUR/USD pair faces a more structurally challenging outlook.

For now, the ECB's hawkish stance is cushioning the blow and providing a relative anchor. Investors are weighing central bank narratives and macroeconomic signals to assess risk sentiment.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1700 and Support sits at 1.1580

USD: Dollar Strength Extends

DXY 99.31

The dollar index (DXY) advanced firmly to 99.31, capitalising on a sharp global sell-off that sent benchmark 10-year US Treasury yields surging to 4.6310%. Several drivers are reinforcing each other. The shorter-term two-year yield kept pace, rising to 4.1020% to reach its highest level since February 2025. This parallel surge across the spectrum shows that conditions favour a prolonged dollar rally this week. Risk aversion lifts the dollar, making it the world's most liquid currency. And the US, as a net energy exporter, holds a structural advantage over Europe and Asia when oil prices spike.

The Fed's outlook matters here, too. CME FedWatch data showed a probability of a Fed rate hike of over 50% by December. Fed minutes due Wednesday, alongside flash PMI data, could clarify how much internal pressure exists for a shift to neutral, and how seriously the committee weighs persistent inflation against growth risks.

New Fed Chair Kevin Warsh attends the G7 meeting in Paris today, his first major international forum. Analysts are watching closely for signals on how he will balance his traditional inflation discipline with external political pressures for lower borrowing costs, whether he aligns with Trump's preference for lower rates or leans hawkish amid current inflation dynamics.

USD/CNH weakened to 6.8150 as offshore yuan softened following the Trump-Xi summit, which produced no major breakthroughs. China's April growth data was also disappointing, adding downward pressure.

Global Crosses: Yen Intervention Alerts and Antipodean Slump

AUDUSD 0.7171 | NZDUSD 0.5869 | USDJPY 158.54 | GBPJPY 211.74

The Japanese yen weakened to 158.97 against the dollar, matching its lowest level since late April and prompting currency authorities to put on high alert for immediate direct intervention. In contrast, the risk-sensitive Australian dollar fell 0.2% to $0.7132 after poor infrastructure and retail data from China, whilst the New Zealand dollar stabilized flatly at $0.5837. Both currencies function as risk proxies and sold off alongside equities.

Geopolitical escalation directly penalises net energy importers. Japan faces an expanding fiscal burden, with government sources confirming a new debt issuance to fund an emergency budget aimed at softening the impact of the Middle East energy shock. Concurrently, broader risk appetite faces a major test as drone strikes in the Gulf overshadow corporate earnings optimism.

GBP/JPY sat at 211.75, dragged by both sterling weakness and yen softness. The cross reflects two vulnerable currencies in a risk-off world.

The Strait of Hormuz is acting as the fulcrum. During normal times, the waterway handles roughly 20% of the world's oil trade. Current throughput is a fraction of that. Market analysts have estimated that, at current levels, 1 billion barrels of Crude would have been lost by the end of May. Brent Crude rose on Monday to breach $110 per barrel following a drone attack on a UAE nuclear facility.

G7 finance ministers and central bankers convene in Paris today and tomorrow. The agenda: Hormuz, critical raw material supply chains, and how to manage an inflation shock that may be arriving like an uninvited guest. Every major theme currently traces back to a single waterway that the market assumed would reopen sooner, but it still remains effectively shut.

The dollar gains 0.5% to 1% for every 10% rise in oil prices, a structural advantage that is underpinning the dollar's bid in this environment. Europe and Asia are absorbing higher energy costs with no offsetting export windfall. This asymmetry is currently being reflected in the FX markets.

Current Rate Table:

| Pair | Last | Trend |

|---|---|---|

| GBP/USD | 1.3363 | Bearish |

| EUR/USD | 1.1640 | Bearish |

| EUR/GBP | 0.8707 | Bearish |

| AUD/USD | 0.7131 | Neutral |

| NZD/USD | 0.5838 | Neutral |

| USD/JPY | 158.97 | Bullish |

| GBP/JPY | 211.75 | Bearish |

Market Lookahead

Mon, 18 May

- G7 Finance Ministers and Central Bankers Meeting

Tue, 19 May

- UK - Avg. Earnings, Claimant Count Change & Rate (Apr) , ILO Unemployment Rate, Employment Change

- Canada’s CPI

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.