War Premium Fades. Peace Talks and PMIs Take the Wheel.

7 min read

Share

US-Iran peace talks ease the war premium. Central bank minutes stay hawkish. Global PMIs land today. Sterling steadies, the dollar pauses and commodity FX loses ground.

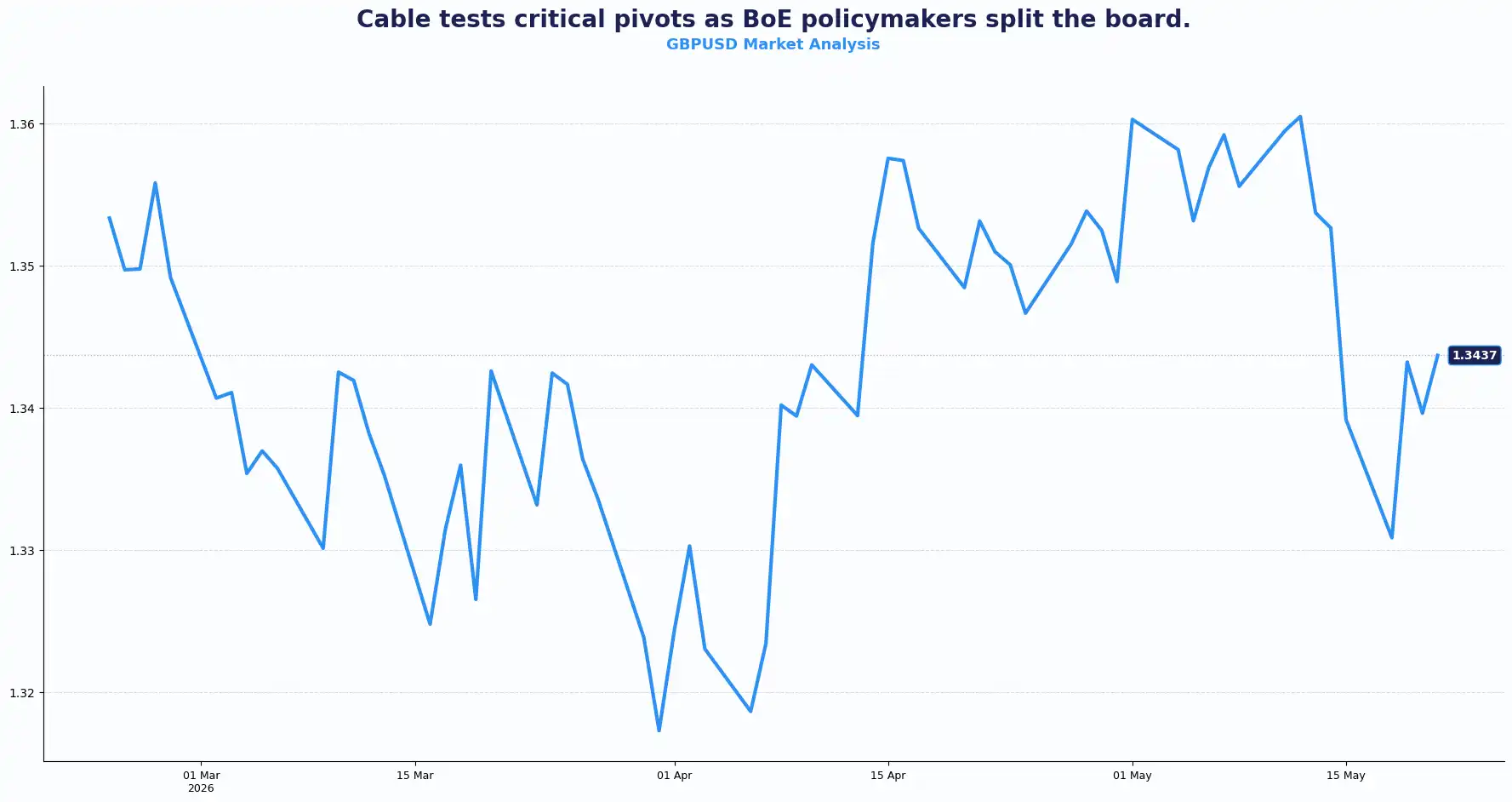

GBP: Sterling Holds Amid Conflicting Signals

GBPUSD 1.3437 | EURGBP 0.8653

Sterling trades at $1.3437, steady after Wednesday's softer-than-expected UK CPI reading pushed markets' rate-hike expectations back to December. The Bank of England's (BoE) own testimony reinforced the caution. BoE Governor Andrew Bailey confirmed that the Monetary Policy Committee (MPC) removed the prospect of two rate cuts from the table after the March meeting, reflecting a more watchful stance than a dovish outlook.

MPC member Catherine Mann noted firms tend to pass through higher prices from economic shocks, and warned that financial conditions have tightened considerably. Deputy Governor Sarah Breeden said the BoE is well placed to monitor secondary wage-price spirals. Swati Dhingra offered the counterpoint that even in a fairly severe scenario, there is probably enough tightness in the system to contain inflation, and food price inflation is unlikely to reach the scale seen in recent years, reflecting an intensely fractured front from the BoE. This domestic policy friction collides with an unyielding Federal Reserve (Fed), keeping the British currency trapped in a volatile holding pattern.

Today's S&P Global UK PMIs carry weight. Composite PMI consensus sits at 51.7. Manufacturing consensus is 53.0, and Services, which drive the UK economy, sits at 51.8. A miss on services would confirm the softness in inflation narrative and give the BoE cover to hold rates well into year-end. A beat reopens the question of timing.

The Iran situation adds a layer of noise. The dollar's safe-haven bid softened after Trump confirmed that US-Iran talks are in their final stages, giving sterling some breathing room. Oil pulling back from elevated levels eases imported inflation pressure, a constructive dynamic for the UK's external balance.

Tomorrow brings GfK Consumer Confidence for May, with consensus at -28, down from a prior reading of -25. UK Retail Sales data for April also drop. Two prints that could give a clearer read on whether the UK consumer is holding up or beginning to crack under the weight of higher rates.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3520 and Support sits at 1.3380, 1.3325

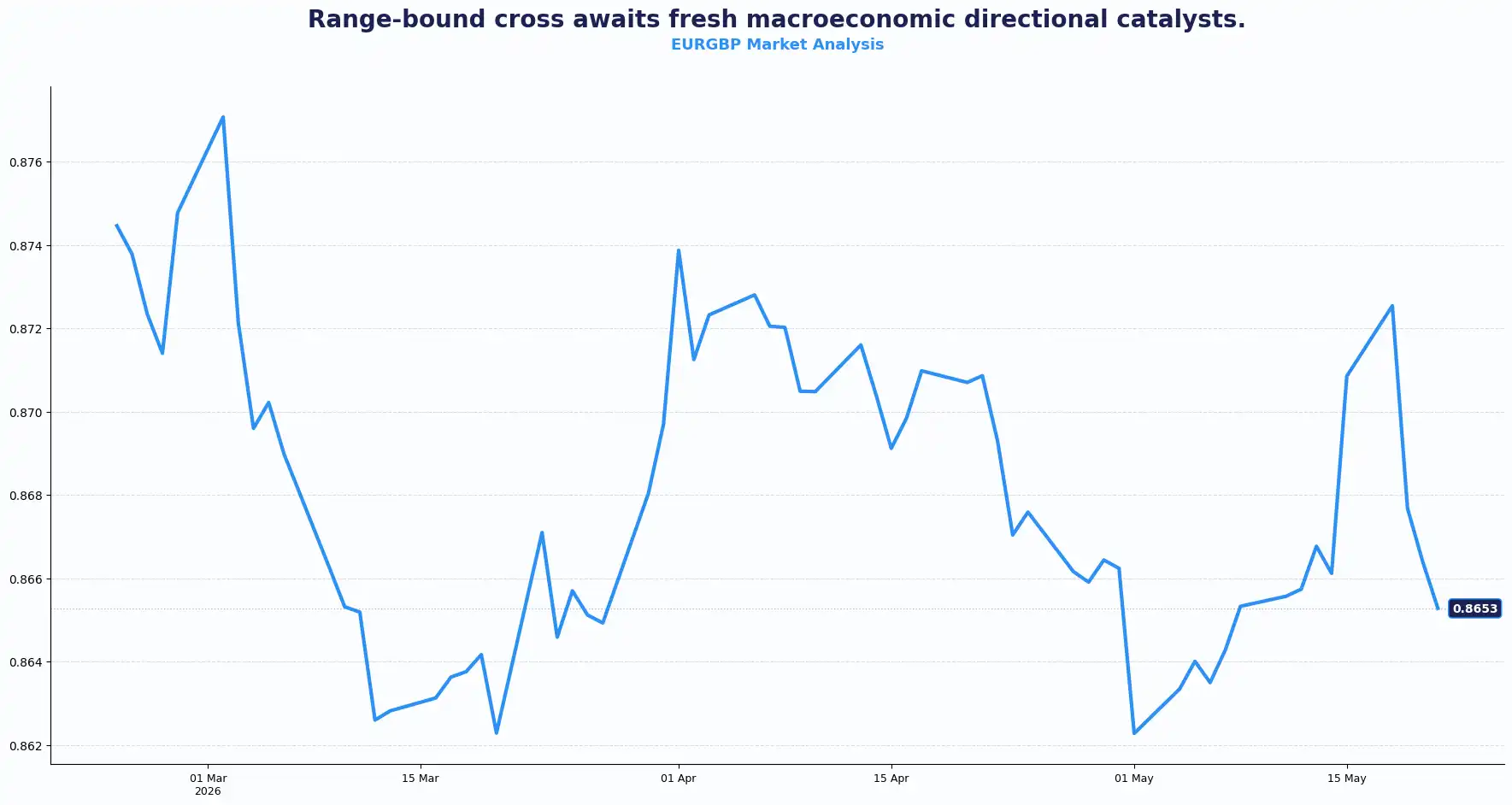

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8685, 0.8720 and Support sits at 0.8620, 0.8590

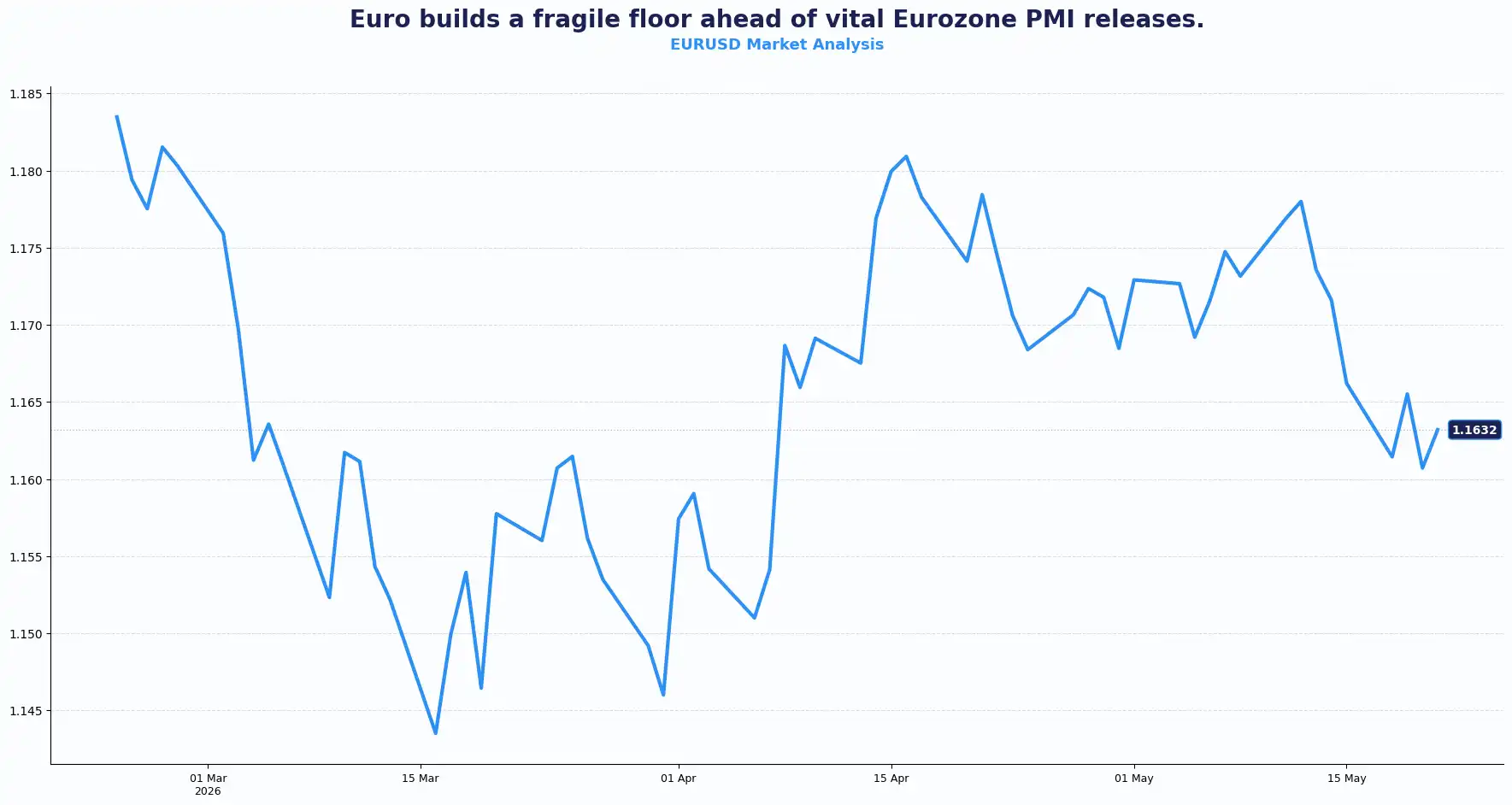

EUR: Euro Holds Above 1.1600 Before PMI Test

EURUSD 1.1632

The euro holds above $1.1600 after dipping to $1.1583 on Wednesday, its weakest level since early April. That low found support and bounced, but the structural picture is still complicated.

Markets locked into a tight range ahead of the Eurozone PMI figures from Hamburg Commercial Bank (HCOB) manufacturing flash index expected at 51.9, consensus for Services PMI sits at 47.7, consensus for Composite sits at 48.8. Services below 50 signals contraction, and the Eurozone services sector is contracting while manufacturing remains in expansion territory, creating a split picture that gives the ECB reason to proceed carefully.

Germany's HCOB readings are released alongside the Eurozone figures. Germany is the anchor of European output, and any material miss on German services will reinforce the divergence narrative between fiscal and monetary flexibility on the continent. Eurozone Consumer Confidence for May also prints today, projected at a deeply negative -20.8, signalling that confidence is not recovering and adding to the cautious tone.

ECB policymaker Olli Rehn added a pointed note earlier today, under adverse circumstances, it might be necessary to raise interest rates to maintain credibility. A June rate hike looks very likely. The question beyond June is less settled. Many policymakers prefer to wait for the September projections before committing to a follow-up step; this conditional approach keeps the EUR/USD pair range-bound rather than directional.

Tomorrow's calendar is loaded with Germany's Q1 GDP alongside the Eurogroup meeting and Germany’s IFO Business Climate and IFO Expectations indices. The IFO readings are among the most-watched German sentiment gauges; a beat could shift the narrative meaningfully in the euro's favour. A miss reinforces the contraction read already embedded in today's PMI consensus.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1675, 1.1720 and Support sits at 1.1580, 1.1525

USD: Greenback Softens, Hawkish Fed Minutes Keep Bid Alive

DXY 99.19

The US dollar index retreated to 99.182, backing away from its six-week peak of 99.472 hit on Wednesday. Optimism surrounding a potential Washington-Tehran peace deal triggered a reversal in safe-haven capital flows. This shift came after President Donald Trump announced that negotiations were entering their final stages.

The FOMC minutes from the April 28-29 meeting confirmed what markets suspected. A vast majority of policymakers noted increased risk that inflation would take longer to return to the 2% target. Almost all flagged that the Iran war could persist and that energy and commodity prices could stay elevated even after a resolution. A growing number of officials wanted to eliminate the easing bias more than the dissent count suggested; hawkish sentiment dominated the room.

Oil and commodity supply chains will remain highly constrained even if the conflict concludes. Fed funds futures now price roughly 50% odds of a rate hike by December, completely reversing pre-war expectations of two rate cuts. That repricing is defining the dollar story.

US 10-year Treasury yields rose 1.9 basis points to 4.588%, resuming their climb after Wednesday's brief dip. US crude hovers near $99.50 per barrel. Brent settled near $106.00. The Fed is in a difficult position; elevated oil prices sustain inflationary pressures and limit its flexibility to cut rates. Any positive development on Iran that pulls oil lower gives the Fed cover to hold without hiking. Any deterioration in returns rates hikes bets to the front of the queue.

Today brings S&P Global US PMI flash estimates and initial jobless claims. The jobless claims print is particularly relevant to the FOMC minutes' note that the labour market appears stable. Any deterioration in claims could introduce dovish complexity into a currently hawkish narrative.

Three supertankers carrying 6 million barrels of oil crossed the Strait of Hormuz overnight, sending a constructive signal on supply flows and helping lift sentiment. President Trump confirmed his plans to speak with Taiwanese President Lai Ching-te, a move that introduces fresh China risk. Whether the sentiment around peace optimism holds through Trump's next announcement on Taiwan is a separate question.

Other Pairs: Yen Firms, Aussie Slides

AUDUSD 0.7128 | NZDUSD 0.5851 | USDJPY 159.00 | GBPJPY 213.19

The yen found some footing after Bank of Japan (BoJ) board member Junko Koeda said the central bank needs to continue raising rates, with underlying inflation already around the 2% target. The dollar eased from its eight-session run against the yen on Wednesday. The combination of BoJ hawkishness and Iran optimism, which reduced safe-haven demand, created the brief reversal. Japan's Nikkei jumped 3.6% after S&P Global's flash manufacturing PMI showed May expansion. Japanese exports jumped 14.8% annually in April, confounding stagflation concerns and reinforcing market expectations of a BoJ rate hike next month.

The Australian dollar fell after Australia's unemployment rate rose to 4.5%, above analyst expectations of 4.3% and the highest since 2021. The surprise prompted traders to pare back bets on Reserve Bank of Australia (RBA) rate tightening. The RBA's most pressing concern is still inflation, the labour market data complicates the picture but does not resolve it. Inflation pass-through from energy price shocks remains the variable the RBA is watching most closely. The kiwi dollar trades soft alongside broader risk sentiment adjustments and no domestic catalyst of note today. The currency seems to move with the dollar and the market's risk appetite.

Current Rate Table

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3437 | Bullish bias |

| EUR/USD | 1.1632 | Range-bound |

| EUR/GBP | 0.8653 | Mild bearish bias |

| AUD/USD | 0.7120 | Soft bearish bias |

| NZD/USD | 0.5860 | Neutral |

| USD/JPY | 159.01 | Bullish |

| GBP/JPY | 213.57 | Bullish |

Market Lookahead:

Thu, 21 May

- UK S&P Global PMI data

- Eurozone and German HCOB PMI releases

- US S&P Global PMI data

- US Initial Jobless Claims

- Eurozone Consumer Confidence

Fri, 22 May

- UK Retail Sales

- UK GfK Consumer Confidence

- Germany Q1 GDP

- Germany IFO Business Climate

- Eurogroup Meeting

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.