UK Inflation Dips. Geopolitics Keeps the Pressure On

7 min read

Share

Middle east conflict drives energy prices higher. The FED reprices hawkish. UK CPI beats to the downside, German PPI surprises higher. Volatility holds across FX and bonds.

GBP: Soft CPI Buys Time on a Ticking Clock

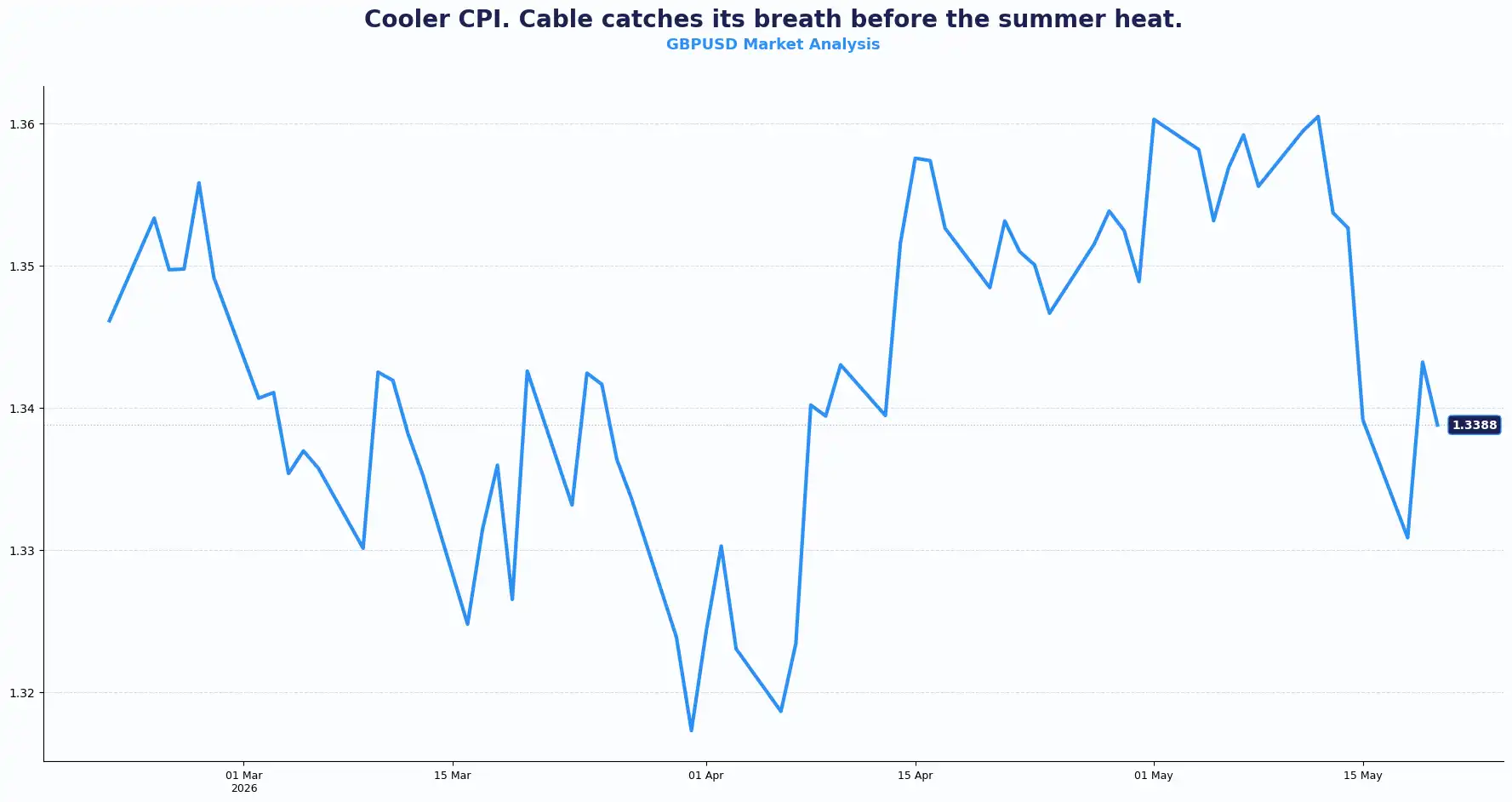

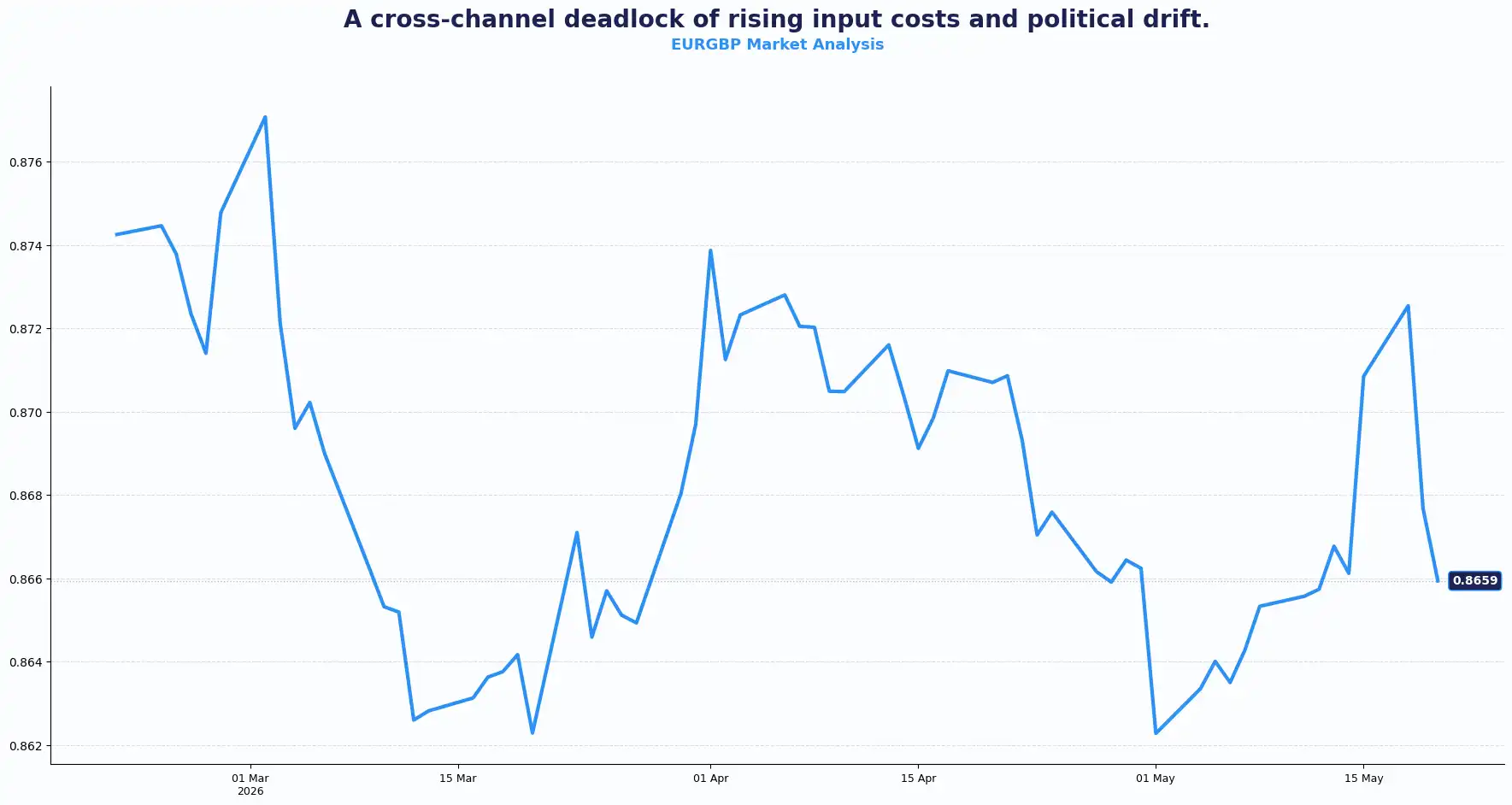

GBPUSD 1.3388 | EURGBP 0.8659

The GBP/USD pair traded at 1.3400 in the early European session, not far from the six-week low touched earlier this week. The pound took the day's CPI print in its stride, but the broader picture has sterling navigating a rather crowded set of headwinds.

UK headline CPI landed at 2.8% YoY in April, below the 3.0% consensus and down from 3.3% in March. Core CPI printed at 2.5%, cooling sharply from March's 3.1% MoM, CPI came in at 0.7%, also beneath the 0.9% forecast. On the face of it, that is good news for the Bank of England (BoE). Inflation is directionally lower and well off its recent highs. But the BoE's 2% target is still some distance away, and the read-through to policy is anything but straightforward.

The BoE's MPC cut rates at its last meeting in April. BoE Governor Andrew Bailey and fellow policymakers fronted the Treasury Committee today, fielding questions on that decision and the ongoing conflict in the Middle East. Deputy Governor Sarah Breeden flagged earlier this week that political uncertainty is actively weighing on the business environment, and cautioned against being trigger-happy on rates; signalling that the BoE prefers to watch and wait and this CPI print gives them the cover to do exactly that.

Producer prices told a more mixed story. PPI output came in at 1.4% MoM, flat on the prior reading. On an annual basis, however, the figure jumped to 4.0% against a prior of 3.0% a notable upside surprise. Core PPI output printed at 0.7% MoM and 2.4% YoY. Pipeline price pressures have not gone away. That asymmetry between softening consumer inflation and firming producer prices is worth taking note of.

The BoE now faces a difficult balancing act. Inflation cooled, but energy risks still shadow the second half of the year. Ofgem is to announce the next energy price cap at the end of this month. The revision, effective 1 July, could push household energy bills significantly higher. Consensus is that UK CPI will peak at 4% later this year. The disinflation move in today's data likely reflects a temporary lull rather than a durable trend. Q3 is where the pressure is likely to reflect again, with the risk of second-round effects feeding into wages and services inflation through the second half of the year.

Politics adds another layer. Labour party’s poor showing in the local elections has introduced a fresh wave of domestic uncertainty. Sterling has struggled to attract buyers in May against that backdrop and the combination of rising yields globally, geopolitical noise from the Middle East, and a fragile domestic picture has kept a lid on sterling conviction. Today's softer CPI may ease the urgency around the next BoE move, but it does not resolve the structural tensions surrounding the pound.

The EUR/GBP pair sat at 0.8659, reflecting the relative stability of both currencies within a narrow range whilst their respective central banks weighed their next steps.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3520 and Support sits at 1.3350, 1.3280

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8690, 0.8725 and Support sits at 0.8620, 0.8580

EUR: Euro Slips as Growth Concerns Build

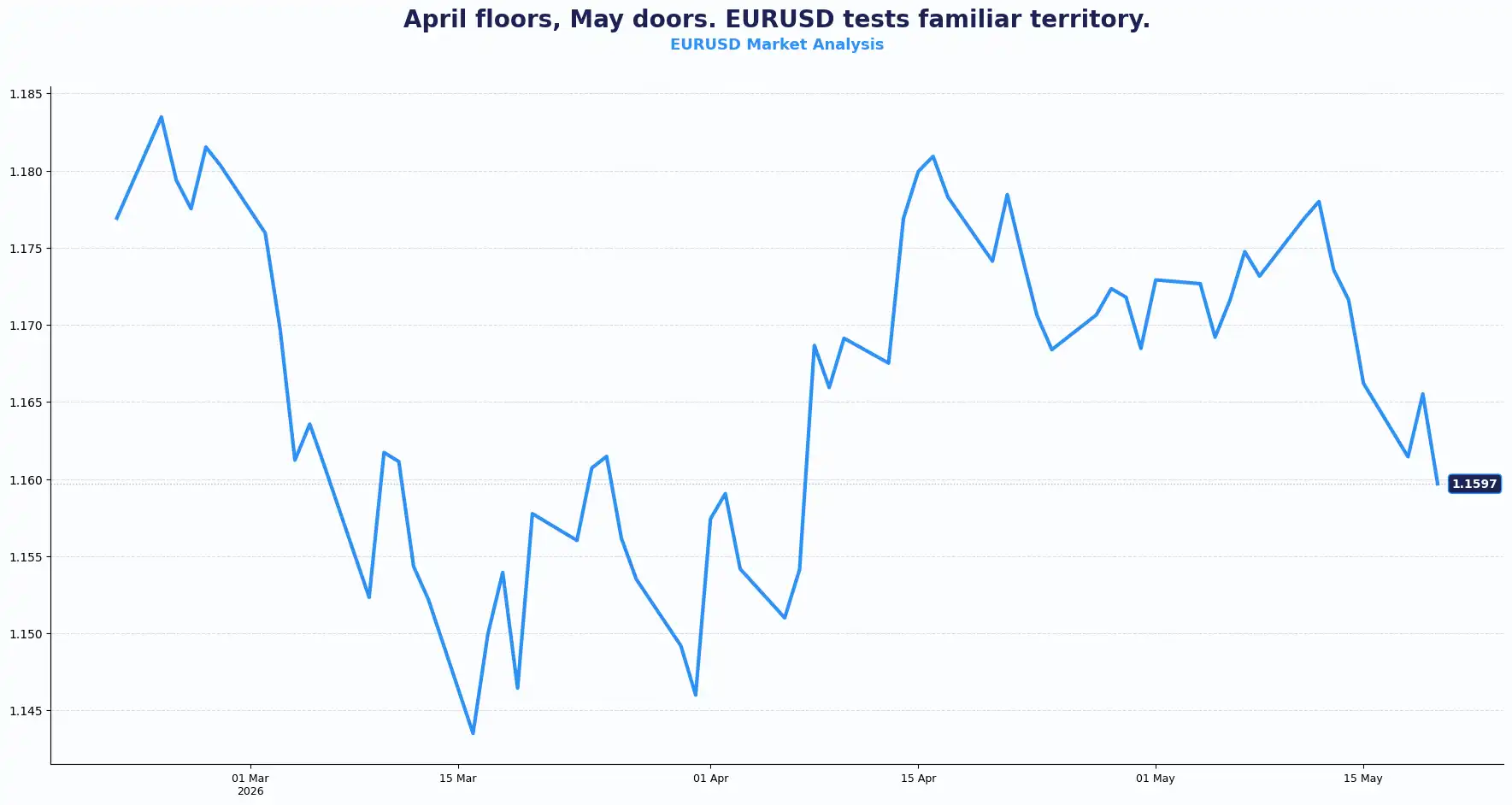

EURUSD 1.1597

The EUR/USD pair traded at 1.1597 in the early European session, touching its lowest level since early April. European equity futures pointed sharply lower, Euro Stoxx futures were off 0.7% as the global bond sell-off continued to weigh on risk appetite across the board.

German producer prices printed firmer than expected. PPI came in at 1.2% MoM versus a 1.0% consensus, and 1.7% YoY against a 1.5% forecast. Both beat estimates. The prior annual reading was -0.2%, so the year-on-year swing is significant and points to building upstream price pressures in the Eurozone's largest economy.

On the consumer side, the Eurozone's Harmonised Index of Consumer Prices for April is expected at 2.2% YoY, in line with the prior reading. The core HICP consensus also holds at 2.2% YoY, whilst the monthly reading is expected flat at 1.0%. Neither of those numbers argues for urgency at the European Central Bank (ECB), which has been among the more measured major central banks in this cycle.

Traders are pricing in less aggressive tightening from both the ECB and the BoE relative to what the Federal Reserve (Fed) may need to deliver. That divergence in rate expectations is one of the cleaner explanations for why the dollar continues to draw relative support even as geopolitical and fiscal concerns circle it. The euro, caught between its own domestic data flow and the pull of a repricing Fed, is finding it difficult to hold altitude. Brent Crude holding above $110 a barrel, off 0.5% on the day but elevated, adds an inflationary layer to Eurozone data watchers' concerns for the months ahead.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1640, 1.1700 and Support sits at 1.1550, 1.1490

USD: Dollar Holds Its Ground Amid Surging Yields

DXY 99.19

The dollar Index (DXY) was at 99.35. The index gained more than 1% in May, driven by a combination of safe-haven demand and a sharp shift in Fed rate expectations, from two cuts priced before the conflict to traders now assigning over a 50% chance of a hike by December, according to CME FedWatch data.

The 10-year US Treasury yield hit a 16-month high of 4.687% overnight. The 30-year climbed to 5.198% , levels not seen since 2007. Asian equities extended their losing streak into Wednesday's session as higher yields eroded the case for risk assets, whilst Nvidia earnings drew focus as markets looked to one of the few structural narratives capable of offsetting the rate pressure.

In Washington, incoming Fed Chair Kevin Warsh faces questions about monetary policy direction and central bank independence. Markets await the minutes from the Fed's April meeting for more detail on how many policymakers have hardened their stance since then. The expectation, widely held, is that the minutes read hawkish.

The geopolitical backdrop intensifies the dollar's role as a safe haven. President Trump said the United States may strike on Iran again, though he left open the possibility of a negotiated deal. The Strait of Hormuz disruption is feeding directly into energy prices and inflation expectations. Xi Jinping meeting Vladimir Putin in Beijing, less than a week after Trump's visit to the region, adds further complexity to the diplomatic backdrop that markets are trying to price.

The core point is this - investors are returning to fundamentals. What inflation is doing, what that means for bond yields, and what that implies for the Fed, that is the frame that governs risk appetite right now. The dollar sits well within that frame.

JPY, AUD, NZD: Yield Pressure Bites Across the Board

AUDUSD 0.7128 | NZDUSD 0.5851 | USDJPY 159.00 | GBPJPY 213.19

The USD/JPY pair held near 158.96, keeping the yen inside the zone that has previously triggered Bank of Japan intervention (BoJ). US Treasury Secretary Scott Bessent's comments about clearing political hurdles for the BoJ to hike rates next month provided a degree of support. But unless US Treasury yields and the broad dollar ease, official intervention, should it come, is more likely to slow the move than reverse it.

GBPJPY sat at 212.84 reflecting the dollar's broad strength against both currencies. The Australian dollar traded at 0.7102 and the New Zealand dollar at 0.5830, both near five-week lows. The Aussie functions as one of the cleaner real-time barometers of global risk appetite, and its subdued performance signals that markets are not yet comfortable stepping back into risk. Emerging market currencies are feeling the strain too. The Indian rupee and Indonesian rupiah both hit record lows on Wednesday, casualties of the broader repricing of US rate expectations and the flight to dollar assets.

Current Rate Table:

| Pair | Spot Rate | Trend |

|---|---|---|

| GBPUSD | 1.3388 | Bearish near-term |

| EURGBP | 0.8659 | Bullish |

| EURUSD | 1.1597 | Bearish near-term |

| AUDUSD | 0.7102 | Bearish |

| NZDUSD | 0.5830 | Bearish |

| USDJPY | 158.96 | Bullish |

| GBPJPY | 212.84 | Bullish |

Market Lookahead:

Wed, 20 May

- Eurozone: Core Harmonised Index of Consumer Prices (April)

- USA: FOMC Minutes (April Policy Meeting).

Thu, 21 May

- Eurozone, UK & USA: Preliminary Private Sector Purchasing Managers' Index (PMI) (May).

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.