Hot UK Wages, Cold UK Politics, One Very Flat Pound

6 min read

Share

Sterling buckles under political strain and mixed UK jobs data. Trump pauses a planned Iran strike, oil drops, bonds stabilise. The euro awaits a data test and the dollar outperforms. UK inflation lands tomorrow.

GBP: Good Data, Bad Politics

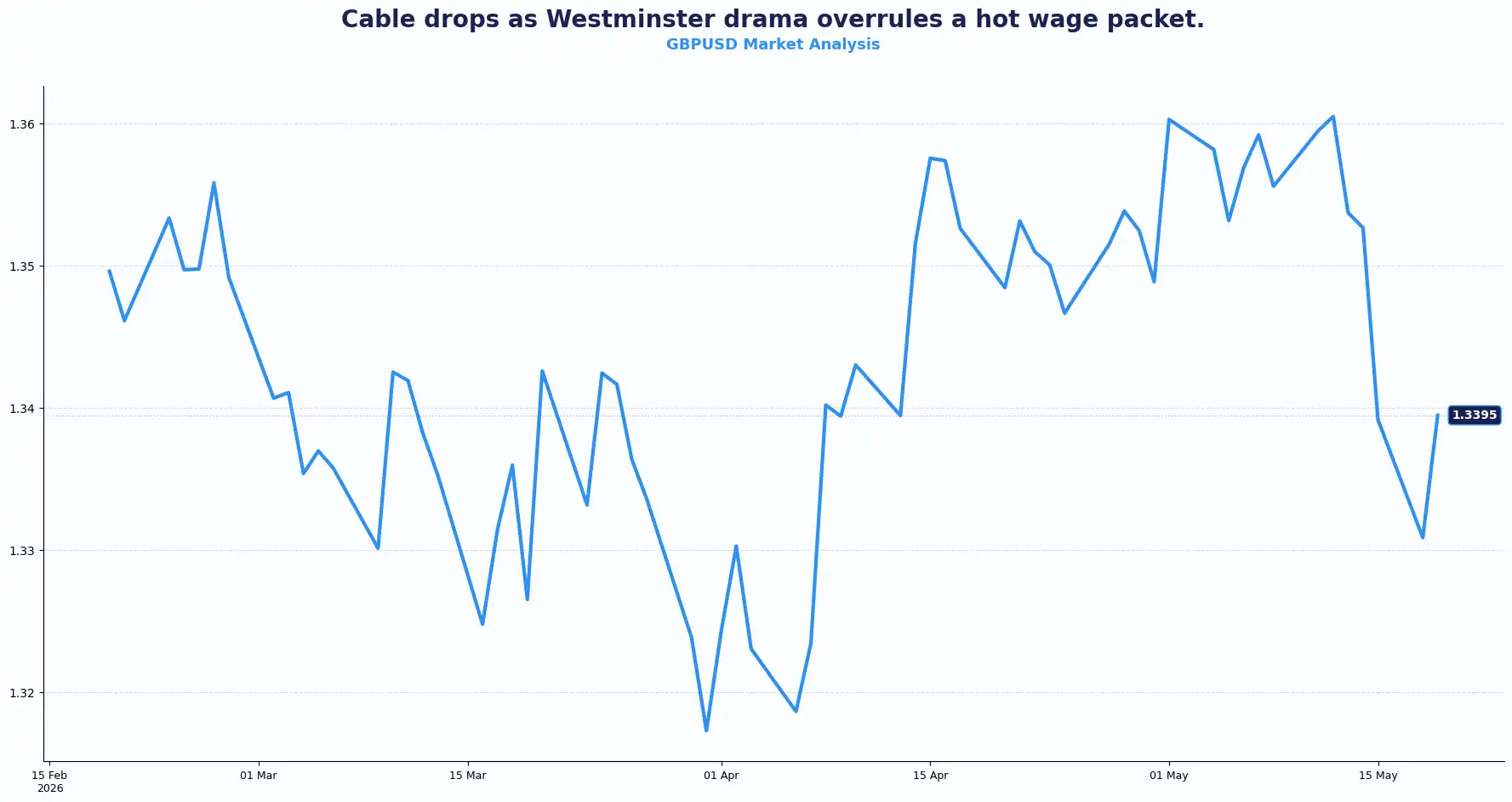

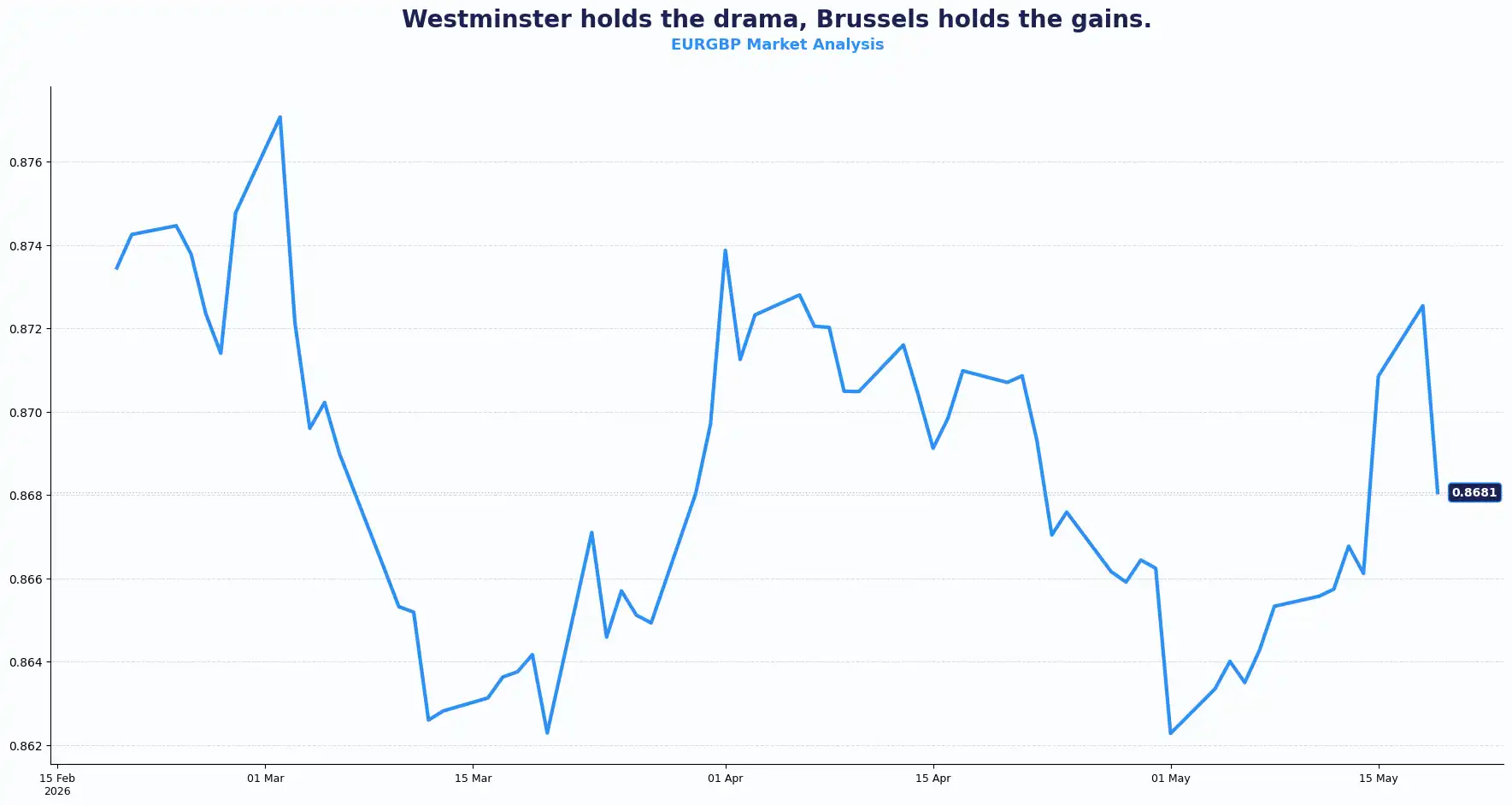

GBPUSD 1.3395 | EURGBP 0.8681

Cable trades at 1.3395. The EUR/GBP pair holds near 0.8681, ticking upwards after touching a one-month low in the prior session. UK average earnings, including bonuses, hit 4.1% against the 3.8% consensus. This headline beat normally drives a currency higher. Yet, the claimant count jumped by 26.5k, vastly outstripping the prior 4.9k expansion. The labour market is softening at the margins, even if wage pressures persist. This dual reality leaves Sterling stranded.

Employment change jumped to 148K for the three months to March, a sharp rebound from the prior 25K. That figure is strong by any measure. But the ILO unemployment rate ticked up to 5.0%, against a consensus of 4.9% and a prior of 4.9%, so the headline tells a slightly softer story than the internals.

Hotter wages, combined with rising joblessness, create a complex backdrop for the Bank of England (BoE). The UK's deepening political crisis is weighing on the pound. Local election damage leaves Prime Minister Keir Starmer fighting for his political life. Gilt yields have risen sharply on the back of that uncertainty, and instead of drawing in foreign capital as higher yields usually do, stagnant UK growth and the energy price shock are keeping buyers away from the pound.

Starmer told staff at Labour headquarters, "I am focused on the job that I was asked to do." Whether markets take him at his word is another matter. The unfavourable political backdrop collides directly with gilt volatility, a combination that acts as a structural weight on sterling even when the underlying data supports it.

Tomorrow brings the UK CPI for April. Consensus sits at 0.9% MoM and 3.0% YoY, the prior reading was 3.3%. UK PPI and the Retail Price Index are also due. A hotter-than-expected CPI print would reinforce the BoE’s hold stance. Investors now price at least two rate hikes from the BoE, a full reversal from the two cuts that were priced before the Iran conflict began in late February.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3500 and Support sits at 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8730 and Support sits at 0.8620

EUR: The Euro Faces a Hawkish Wall

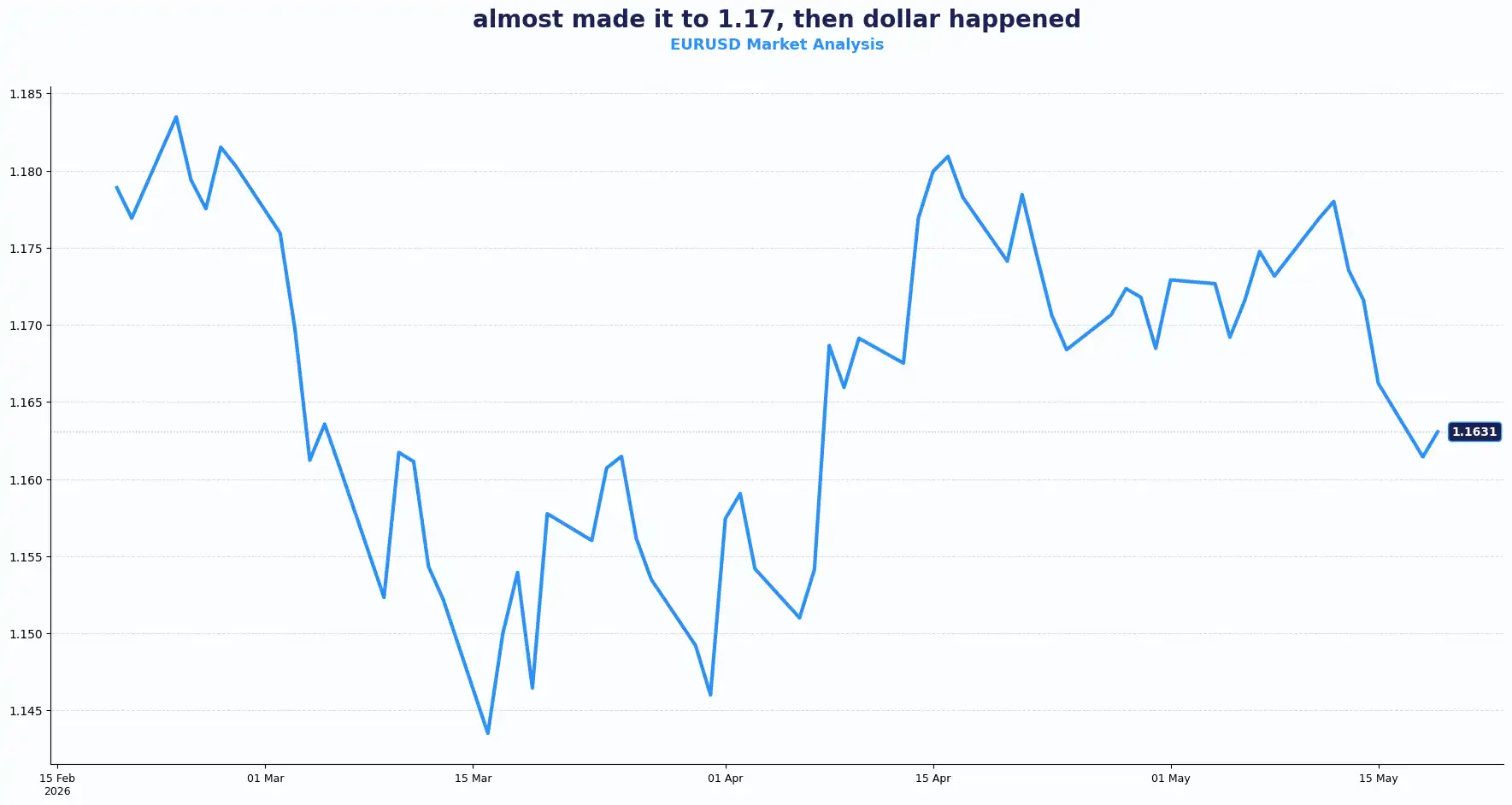

EURUSD 1.1631

The euro is trading on its back foot as the dollar reasserts itself. The EUR/USD pair trades near 1.1629. The pair faces selling pressure rooted in one core expectation that the Fed will not cut rates this year.

The cross’s near-term direction ties closely to two catalysts due this week. FOMC minutes from the April policy meeting drop tomorrow, and investors will scrutinise the language around inflation persistence and the threshold for rate cuts. Flash Eurozone PMI data is due on Thursday, providing the first read on May's private-sector activity. Both releases carry the potential to reprice the EUR/USD pair in either direction.

On the European side, Germany's Producer Price Index data arrives tomorrow. The Eurozone Harmonised Index of Consumer Prices (HICP) for April is also due; the core HICP consensus sits at 2.2%, with headline HICP expected at 1.0% MoM in line with the prior reading. No surprise in those numbers would give the ECB little reason to shift tone.

The European Central Bank (ECB) retains a relatively hawkish stance. Energy price pressures from the Iran conflict continue to complicate the inflation picture across the eurozone. G7 finance ministers meeting in Paris acknowledged mounting concerns about public debt and bond market volatility, a reminder that the macro backdrop for European assets is not straightforwardly supportive of the euro either.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1720 and Support sits at 1.1550

USD: Dollar Holds Course as the Iran Narrative Shifts

DXY 99.19

The dollar index (DXY) holds at 99.19. Safe-haven demand has underpinned the dollar since the Iran conflict began in late February, and that dynamic has not changed, even as oil prices ease on Trump's latest commentary.

President Trump confirmed on Monday that he paused a planned strike on Iran to allow negotiations on a nuclear deal, after Tehran submitted a new peace proposal to Washington. He said there was "a very good chance" the US and Iran could reach an agreement. Brent Crude fell nearly 2% to $109.94 per barrel, and WTI dropped 1.54% to $106.99. Both remain over 50% above pre-war levels.

The fall in oil prices eased pressure on global bonds. The benchmark 10-year US Treasury yield pulled back from a more than one-year high to 4.6034% in Asian trade, with the two-year yield edging down to 4.0674%. Japanese government bond yields, which hit record highs in the prior session, also retreated across the curve.

Until ships pass safely through the Strait of Hormuz and traffic numbers show a genuine recovery, the market is treating diplomatic commentary from both sides as noise rather than signal. The inflation risk from an energy price shock, particularly for energy-import-heavy economies like the UK, has not gone away.

Investors now price in rate hikes from major central banks this year, expecting policymakers to face renewed inflationary pressure from higher-for-longer energy prices. That represents a complete reversal of the easing cycle that traders had priced in before late February. FOMC minutes tomorrow will be the next major test of the dollar's composure.

Yen & the Antipodeans Tread Water

AUDUSD 0.7128 | NZDUSD 0.5851 | USDJPY 159.00 | GBPJPY 213.19

The USD/JPY pair trades at 159.00. The GBP/JPY pair sits at 213.19, reflecting the combined weight of a soft pound and a yen that lacks the policy support to strengthen meaningfully despite near-record JGB yields. The BoJ's path remains constrained, and any aggressive yen defense through rate action risks destabilising a fragile domestic bond market.

The AUD/USD pair holds near 0.7128. The NZD/USD pair trades at 0.5851. Both antipodean currencies track global risk sentiment closely, and the softening prices in oil give them modest breathing room, though neither pair shows a compelling directional catalyst in today's early European session.

Current Rate Table:

| Pair | Last | Trend |

|---|---|---|

| GBP/USD | 1.3395 | Bearish |

| EUR/GBP | 1.1631 | Bullish |

| EUR/USD | 0.8681 | Bearish |

| AUD/USD | 0.7128 | Neutral |

| NZD/USD | 0.5851 | Bearish |

| USD/JPY | 159.00 | Bullish |

| GBP/JPY | 213.19 | Bearish |

Market Lookahead:

Wed, 20 May

- UK: Consumer Price Index (April)

- UK: Producer Price Index & Retail Price Index (April)

- Eurozone: Core Harmonised Index of Consumer Prices (April)

- USA: FOMC Minutes (April Policy Meeting).

Thu, 21 May

- Eurozone & USA: Preliminary Private Sector Purchasing Managers' Index (PMI) (May).

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.