UK GDP Treads Water, Pound Eyes the Cabinet

8 min read

Share

UK GDP grows 0.1% in May, services up, production and construction down. Burnham expected to enter No.10 Monday with cabinet speculation building. US PPI fell in June, a second consecutive cooling print this week, easing Fed hike bets. Oil prices have elevated as US-Iran strikes continue. The euro held firm while traders shifted their focus towards central banks and upcoming US data.

GBP: Sterling Holds Ground as Growth Fails to Spark Momentum

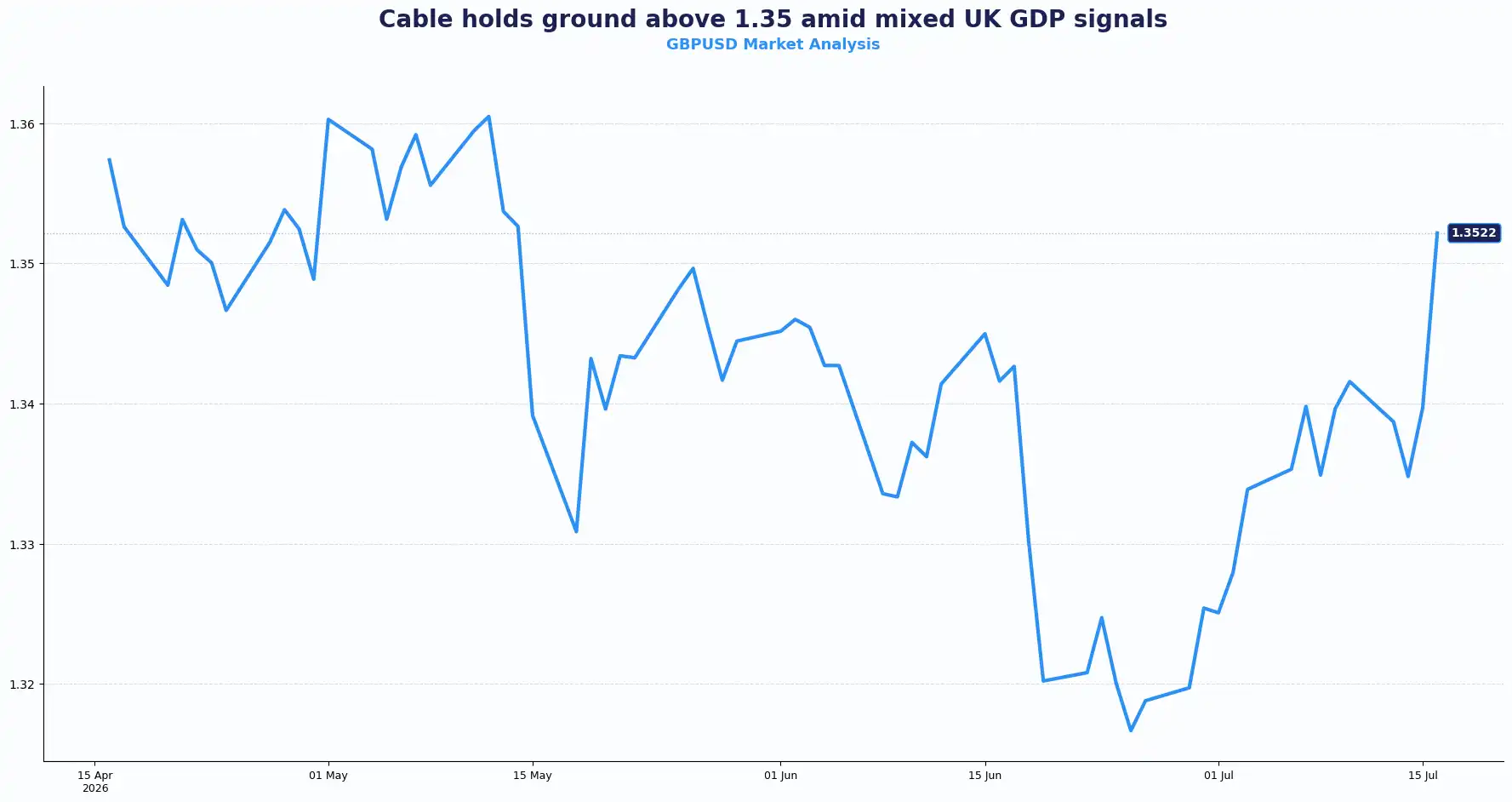

GBPUSD 1.3522

GBP/USD trades around 1.3530 in early European trade, down 0.06% on the day before trading near 1.3520. This morning's ONS release delivered exactly what the consensus expected. UK GDP grew 0.1% in May, recovering from April's 0.1% decline. Industrial production fell 0.5% on the month while manufacturing production edged 0.1% higher. The data moved the pound very little. Those releases did little to change expectations for Bank of England (BoE) policy.

The bigger influence came from abroad.

Renewed conflict in the Middle East and fresh disruption through the Strait of Hormuz pushed energy prices higher. Rising oil prices could feed back into inflation over the coming months. That backdrop has kept expectations for tighter BoE policy alive even as domestic growth slows.

Markets continue to price another BoE rate hike by November, with expectations for further tightening extending into next year. Investors also turned their attention towards the UK's political outlook ahead of the expected announcement of Andy Burnham as Prime Minister on 20 July, pushing the focus squarely onto his choice of finance minister given the UK's public finances. Traders are watching the cabinet composition closely; the fiscal stance of whoever takes the Treasury will carry real implications for gilt pricing and, by extension, the pound.

For sterling, the balance remains delicate. Softer growth limits upside momentum, while persistent inflation risks discourage expectations of rapid rate cuts. That combination has kept the pound broadly supported without providing a strong catalyst for a sustained move higher.

Upcoming US Retail Sales data may prove more influential for GBP/USD than this week's UK releases. A stronger US print could steady the dollar, while another softer reading may reopen room for sterling to recover.

Central bank expectations, energy prices and US data continue to shape sterling's direction, leaving currency moves sensitive to incoming headlines.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3580 and Support sits at 1.3480

EUR: Oil Surge Keeps ECB Hike Bets Alive

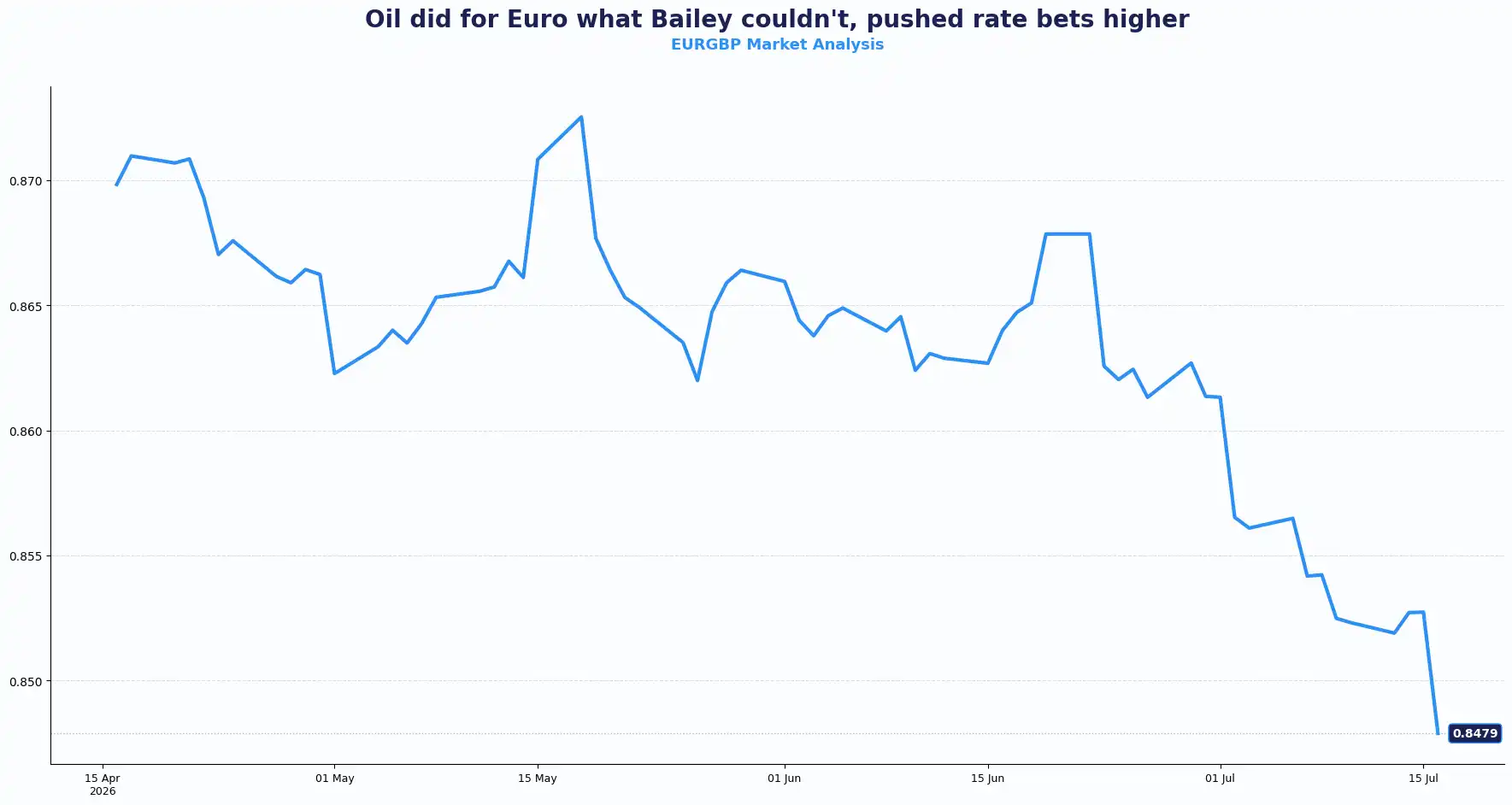

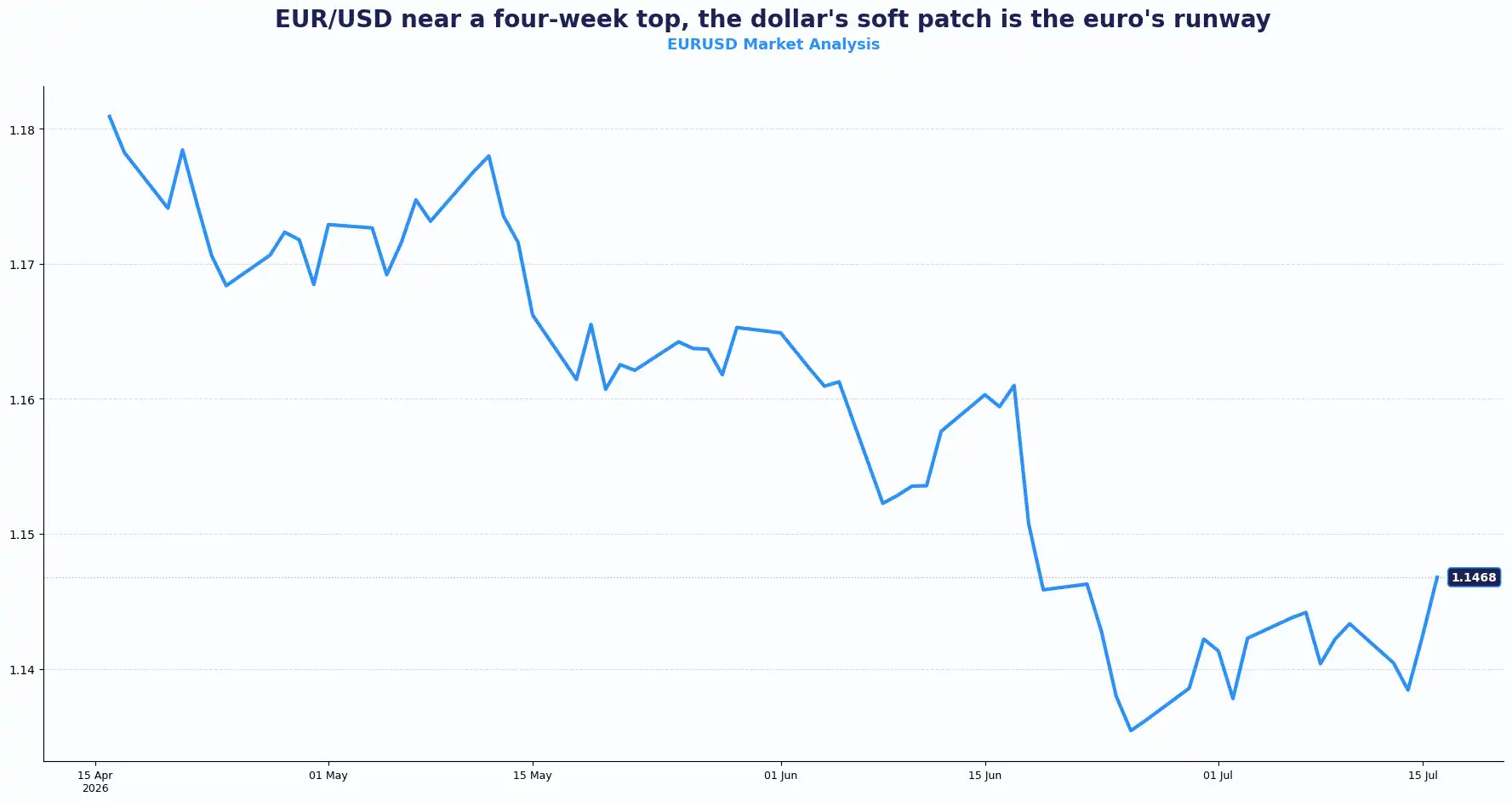

EURGBP 0.8479 | EURUSD 1.1468

EUR/GBP holds positive ground near 0.8475 in early European trade. The British pound softened against the euro following this morning's UK data, though the move is modest. Traders continue to ramp up bets on BoE and ECB rate hikes this year, with rising oil prices expected to feed through to inflation on both sides of the Channel.

EUR/USD extended its rebound and touched its highest level in about a month above 1.1480 on Wednesday. The pair consolidated around 1.1466 this morning. The dollar's softness, following a second consecutive cooling US inflation print, acts as the primary tailwind. ECB President Christine Lagarde continues to stress strict data-dependence. The ECB's June meeting account explicitly noted that the hike was neither a guaranteed sequence nor a guaranteed one-off. ECB Governing Council member Martin Kocher said on Wednesday that the central bank is prepared to implement monetary policy measures whenever necessary to achieve its 2% medium-term inflation target. Traders now price a 25bp ECB hike by September, with another move by year-end all but certain.

Even so, the euro's advance has lost momentum.

Fresh military escalation between the United States and Iran, alongside disruption in the Strait of Hormuz, lifted oil prices and revived concerns about imported inflation. Those developments offered the dollar fresh support as investors reassessed the inflation outlook, preventing EUR/USD from extending its rally.

Attention now shifts to US Retail Sales, Weekly Jobless Claims. Together with comments from Fed officials, those releases could shape expectations for Fed interest rates and determine whether the euro can hold its recent gains.

The euro continues to respond more to shifting US interest rate expectations than domestic developments. Inflation data, central bank guidance and geopolitical events continue to influence price direction across EUR/USD.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8510 and Support sits at 0.8440

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1500 and Support sits at 1.1420

USD: Two Cooling Prints, One Blockade

DXY 100.50

The dollar index (DXY) holds around 100.50 on Thursday morning. US June PPI fell 0.3% on the month, an unexpected downside print that compounds Tuesday's soft CPI reading. Two consecutive cooling inflation prints have driven front-end Treasury yields lower and kept dollar bulls on the defensive. The CME FedWatch Tool now shows the implied probability of a September Fed rate hike at 44%, down from 50% prior to the PPI release.

The interim US-Iran peace agreement reached last month has effectively unravelled. June's inflation data does not yet capture the economic impact of this latest military escalation. Iran's top negotiator, Mohammad Bagher Ghalibaf said that if Iran did not benefit from its memorandum of understanding with the United States, "We have no reason to adhere to such an understanding." That language keeps energy supply risk elevated and the inflation outlook genuinely uncertain beyond the June data window.

The US naval blockade of Iranian ports and the closure of the Strait of Hormuz support elevated crude oil prices. Higher oil prices fuel inflation concerns and revive hawkish Fed expectations, limiting dollar losses even as the data point the other way. Fed Chair Kevin Warsh also struck a balanced tone. He described recent inflation data as an imperfect guide to underlying price pressures and argued that artificial intelligence could lift productivity while also reshaping wages over time. His comments stopped short of endorsing a more aggressive policy path, leaving traders with little reason to price an immediate shift in Fed policy.

Attention now turns to this week’s US data. Stronger data could reinforce support for the dollar. Softer readings may renew pressure if inflation expectations stay contained.

The dollar now sits between two competing themes. Softer inflation weighs on interest rate expectations, while geopolitical risks continue to support safe-haven demand. That balance could keep volatility elevated as fresh economic data arrive.

Other Currencies:

USDJPY 162.16 | GBPJPY 219.40 | NZDUSD 0.5852 | AUDUSD 0.6995

Outside the major pairs, regional stories continued to drive individual currencies even as the dollar regained some stability.

The Australian dollar slipped back towards 0.6995 after Australia's Consumer Inflation Expectations fell in July. Lower inflation expectations reduced support for the Reserve Bank of Australia's policy outlook and left AUD/USD struggling to build on earlier gains.

The New Zealand dollar held close to 0.5850 after the Reserve Bank of New Zealand's recent rate increase continued to support demand for the Kiwi. Investors still expect further tightening this year, helping NZD/USD outperform several of its commodity-linked peers despite the steadier dollar.

The Japanese yen stayed under pressure, leaving USD/JPY above 162 and GBP/JPY near 219. Wide interest rate differentials continue to favour the dollar and sterling over the lower-yielding yen, although any increase in global risk aversion could revive demand for Japan's traditional safe-haven currency.

The South Korean won weakened after a sharp sell-off in semiconductor stocks weighed on investor sentiment. The Bank of Korea raised interest rates by 25 basis points to 2.75%, matching expectations as policymakers responded to domestic inflation pressures. Even so, weaker technology shares kept pressure on the won, leaving USD/KRW around 1,478.

The Indonesian rupiah also lost ground as higher oil prices increased import costs and raised concerns over the country's trade balance. Rising energy prices continue to present a headwind for net oil-importing economies across Asia.

Meanwhile, the Swiss franc surrendered some gains as geopolitical tensions increased demand for the dollar. Softer US inflation briefly supported the franc, but stronger safe-haven demand for the dollar and expectations that US interest rates could stay elevated helped stabilise USD/CHF.

Across the wider FX landscape, one theme connects every major currency. Inflation expectations now depend as much on geopolitical developments as economic data. Energy prices have become the bridge between those two forces, giving every headline from the Middle East the potential to influence central bank expectations and currency pricing.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3522 | Mild bullish bias |

| EUR/GBP | 0.8479 | Mild bullish EUR |

| EUR/USD | 1.1468 | Bullish |

| USD/JPY | 162.16 | Bearish (USD) |

| AUD/USD | 0.6995 | Mild bullish |

| NZD/USD | 0.5852 | Bullish |

| USD/CHF | 0.8060 | Bearish (USD) |

| GBP/JPY | 219.40 | Bullish |

| USD/KRW | 1,478.08 | Mixed / KRW volatile |

Market Lookahead

Thurs, July 16

- US Initial Jobless Claims

- US Retail Sales (Jun)

Fri, July 17

- Eurozone HICP (Jun) inflation figures

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.