Dollar on the Back Foot as Peace Talks Revive

9 min read

Share

Dollar slips for a third straight session as US-Iran peace talks revive and safe-haven demand fades, easing the week's geopolitical premium. German CPI came in unchanged, removing any fresh pressure on the ECB ahead of its July meeting. Sterling holds above 1.34 on BoE hike bets and Burnham's near-certain path to Number 10. Yen stays the week's outlier near 40-year lows. Next week brings US CPI, another strong catalyst for the dollar and its crosses.

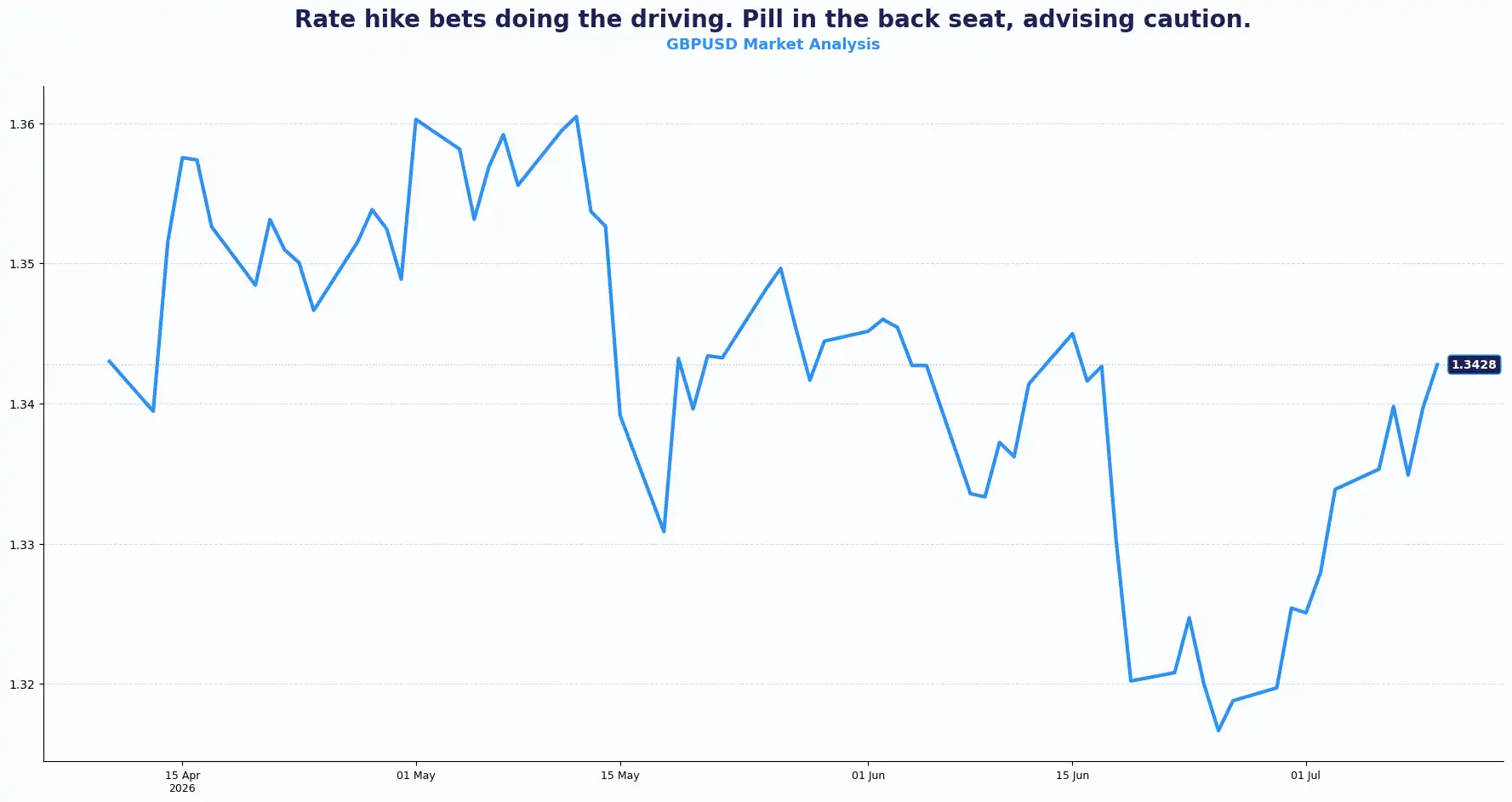

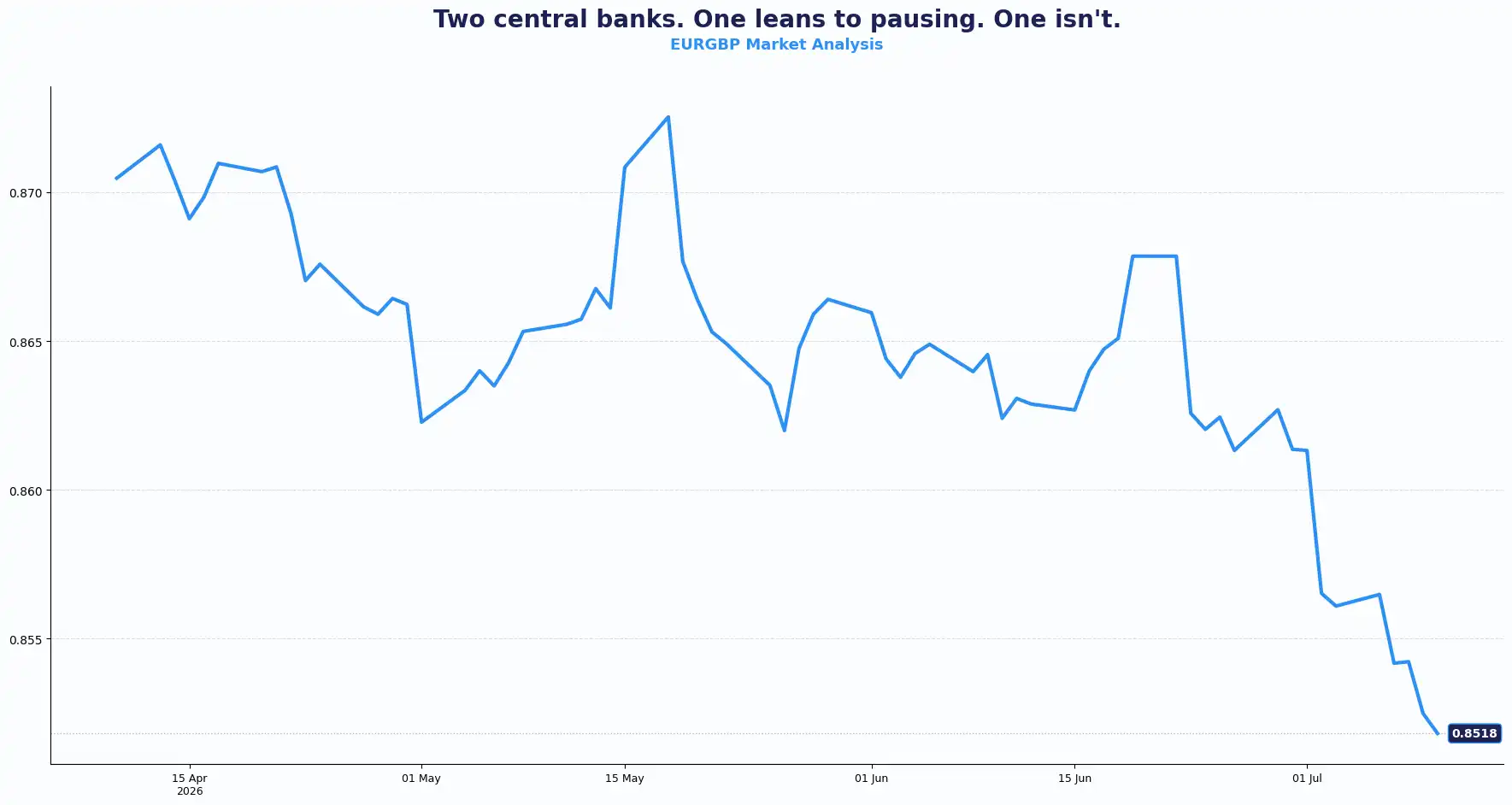

GBP: Sterling Finds Fresh Support as Rate Bets Build

GBPUSD 1.3428 | EURGBP 0.8518

The pound opened on Friday on a firmer footing and held near 1.3430 against the dollar. Investors continued to price in another Bank of England (BoE) rate increase later this year while political uncertainty eased following Labour's leadership transition.

Sterling also strengthened against the euro, with EUR/GBP trading near 0.8520, as the policy outlook continued to favour the UK over the Eurozone.

Andy Burnham's route to Number 10 now looks near-certain. A substantial majority of Labour MPs, 322 of 403, backed him on the first day of the party's leadership contest to replace Keir Starmer. His formal installation as Prime Minister is expected on 20 July. Political continuity of that clarity has historically supported the pound in short-term price action.

On the rates front, markets now fully price in a 25-basis-point BoE hike for year-end, likely in December. Shifting expectations appear to have fed directly into sterling demand this week.

BoE’s Pill struck a measured tone on the UK's longer-term growth outlook. Pill warned that the economy's speed limit may be lower than previously assumed and acknowledged that policymakers may have overestimated the UK's growth trend. Pill also noted that inflation has been at or below the Bank's target for only three of the past 56 months.

Those comments reinforced a familiar theme. Structural growth may be slowing, but inflation remains stubborn enough to keep monetary policy restrictive.

GBP/USD has held above 1.3400 throughout the session. A softer dollar, retreating on fading safe-haven demand as US-Iran technical talks revive, is doing some of the heavy lifting here. Without that tailwind, sterling's progress above 1.3450 would face a more credible test.

External risks still deserve attention. Renewed tensions involving the US and Iran briefly revived demand for traditional safe havens earlier this week. Although diplomatic talks have eased some of that pressure, any fresh escalation could strengthen the dollar and temper sterling's advance against it.

EUR/GBP at 0.8519 reflects relative BoE-ECB policy divergence. With ECB pause expectations strengthening, the cross is likely to track BoE repricing as the dominant input for now.

Policy expectations continue to shape sterling more than short-term political headlines. The gap between UK and overseas interest rate expectations remains one of the main drivers for GBP crosses, leaving pricing highly sensitive to incoming inflation and labour data over the coming weeks.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3475, and Support sits at 1.3400, 1.3370

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8540, 0.8560 and Support sits at 0.8500, 0.8480

EUR: Euro Holds Ground as German Inflation Holds Steady

EURUSD 1.1443

The euro traded near 1.1450 against the dollar after Germany's latest inflation figures matched expectations and confirmed that price pressures continued to cool in June.

The data offered little surprise, leaving EUR/USD trapped within the range that has defined trading over the past two weeks.

Germany's final Harmonised Index of Consumer Prices showed inflation falling 0.2% MoM while annual inflation held at 2.4%, matching preliminary estimates.

The figures strengthened expectations that the European Central Bank will leave interest rates unchanged at its July meeting.

That outlook kept the euro supported but limited its ability to break above 1.1475, a level that has repeatedly capped recent rallies.

Energy prices also influenced sentiment. Oil rebounded after renewed concerns over supply disruption linked to tensions around the Strait of Hormuz. Higher energy costs tend to weigh more heavily on the Eurozone economy because of its dependence on imported energy, limiting broader euro gains.

The ECB appears closer to the end of its tightening cycle than the Bank of England (BoE). Inflation continues to ease across much of the bloc, giving policymakers greater scope to pause as they assess how previous rate increases are filtering through the economy.

That policy gap continues to shape relative performance across major euro pairs.

At the same time, uncertainty surrounding the Federal Reserve (Fed) has prevented the dollar from establishing a clear direction. That has left EUR/USD caught between diverging central bank expectations rather than a single dominant driver.

The euro continues to trade within established ranges as investors balance softer inflation with external risks, including energy prices and global policy expectations. Until either the ECB or the Federal Reserve delivers a stronger policy signal, range-bound trading is likely to remain the dominant theme.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1450, 1.1475 and Support sits at 1.1420 , 1.1405

USD: The Dollar Waits for Inflation to Break the Tie

DXY 100.77

The US dollar softened into the end of the week, with the Dollar Index (DXY) hovering around 100.77 after three consecutive sessions of losses. Even so, the index stayed on course for a broadly flat weekly finish as shifting geopolitical sentiment offset changing interest rate expectations.

Reports that the US and Iran will continue peace talks helped ease demand for traditional safe-haven assets after tensions flared earlier in the week. Oil prices also steadied from recent highs, easing immediate inflation concerns and reducing expectations that the Fed will need to tighten policy more aggressively.

Fed expectations shifted again. According to CME FedWatch, the probability of a 25-basis-point rate increase in July eased to around 24.6%, down from 31% the previous day. Expectations for a September move also dropped lower, although traders still see a reasonable chance of another rate increase before year-end.

Fed officials continued to send mixed signals. New York Fed President John Williams said demand linked to artificial intelligence remains one of the inflation drivers he is watching closely. At the same time, Fed Chair Kevin Warsh announced five policy review task forces, signalling that the central bank is assessing its approach to monetary policy over the longer term rather than signalling an immediate policy shift.

Attention now turns to next week's US Consumer Price Index (CPI). Markets expect core inflation to hold at 2.9% YoY.

The dollar currently sits between two competing forces. Softer geopolitical tensions have reduced safe-haven demand, while inflation has stayed firm enough to keep further Fed tightening on the table.

That balance explains why the dollar has struggled to establish a clear trend despite several days of weakness. Incoming inflation data will likely determine whether policy expectations move towards another rate increase or shift back towards a more patient stance.

A stronger CPI reading could support the dollar across the board. A softer print could narrow interest rate expectations and offer room for higher-beta currencies to extend recent gains.

The next inflation print could reshape expectations across major currency pairs. With policy pricing still evolving, the dollar is likely to stay at the centre of global FX sentiment over the coming week.

Other currencies:

USDJPY 161.52 | GBPJPY 216.90 | NZDUSD 0.5770 | AUDUSD 0.6949

The yen strengthened toward 161 per dollar on Friday, pulling back most of its losses from earlier in the week. Finance Minister Satsuki Katayama said the government would encourage domestic pension funds to increase their allocations to Japanese financial assets. That policy signal carried weight: structural domestic demand for yen-denominated assets, if it materialises, changes the currency's medium-term supply picture.

Japan's June producer prices rose 7.1% year-on-year, the sharpest annual increase since March 2023. The dual pressure of Middle East supply disruption and the yen's sustained depreciation is showing up directly in input costs. The BoJ's policy path will be watching this data point.

The partial retreat in oil prices on Thursday, tied to the resumption of US-Iran negotiations, provided additional yen support by reducing the inflation-from-energy channel that has complicated the BoJ's position. Intervention data due later this month might offer insight into whether Japanese authorities have been actively managing recent sharp but short-lived yen rallies.

The New Zealand dollar hit a three-week high on Friday, driven by reinforced rate hike expectations. The kiwi led the antipodean space as its higher-beta, rate-sensitive profile drew interest in a week where the dollar softened.

The Australian dollar rose to approximately 0.695 but tracked toward a flat weekly close. The RBA is expected to hold rates at 4.35% in August. Pricing still attributes roughly a 60% probability to one further hike later in the year, contingent on oil price developments and upcoming employment and inflation data.

The offshore yuan gained as much as 6.7785 per dollar, its sharpest single-session move in nearly a month. The People's Bank of China set the daily fixing at 6.7989 per dollar, below 6.80 for the first time since 2023. The PBOC has been guiding the yuan softer than market expectations since late last year, but the gap between official fixing and market forecasts has narrowed from more than 500 pips at times last month. The yuan is up 0.1% against the dollar this month and 3.1% YTD. Central bank guidance continues to carry significant weight for the yuan. Currency performance is likely to reflect policy signalling as much as economic data over the coming weeks.

The Canadian dollar has entered a consolidation phase against the US dollar. The Bank of Canada is expected to hold policy unchanged at its 15 July meeting. June unemployment is expected to print at 6.6%.

The Swiss franc gave back modest early gains against the dollar. Tuesday's US CPI could be the next meaningful input for the pair.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3428 | Bullish above 1.3400 |

| EUR/USD | 1.1443 | Range-bound |

| EUR/GBP | 0.8518 | Consolidating |

| USD/JPY | 161.52 | Yen recovery in play |

| GBP/JPY | 216.90 | Elevated; yen sensitivity |

| AUD/USD | 0.6949 | Flat weekly close |

| NZD/USD | 0.5770 | Bullish; 3-week high |

Market Lookahead

Tue, July 14

- UK BRC Retail sales (Jun)

- China’ Trade Balance (Jun)

- US Consumer Price Index (CPI) (Jun)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.