Burnham's Fiscal Vow Steadies Pound as Dollar Surges

7 min read

Share

Sterling holds near $1.32 as Burnham commits to current fiscal rules, though it's still down ~1.7% this month. Dollar strength continues to dominate, pushing the euro to yearly lows, the yen to a 40-year low, and the Aussie and kiwi to multi-month lows. A firmer dollar kept pressure across major currencies ahead of key US labour data.

GBP: Fiscal Vow Buys the Pound Some Calm

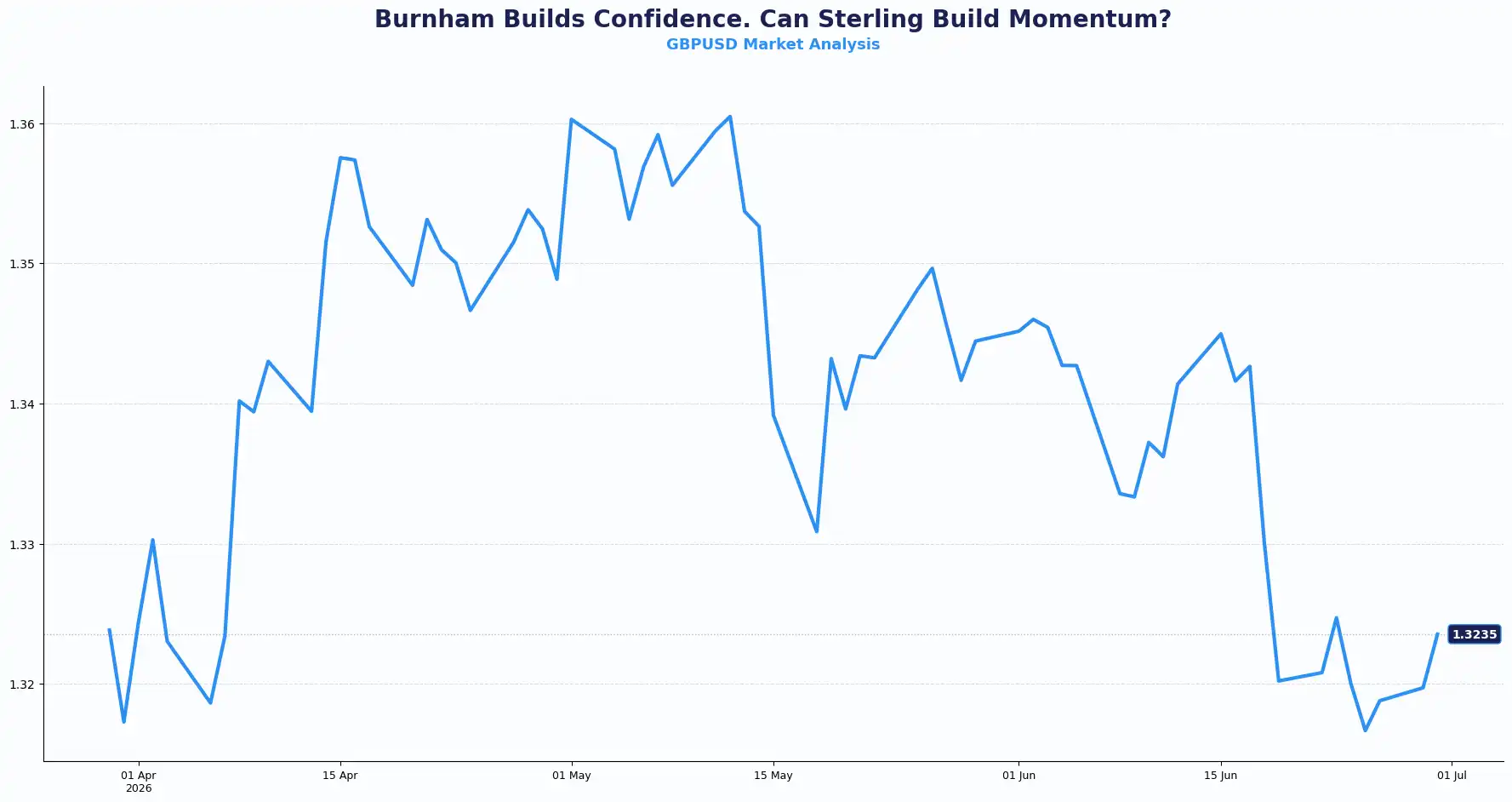

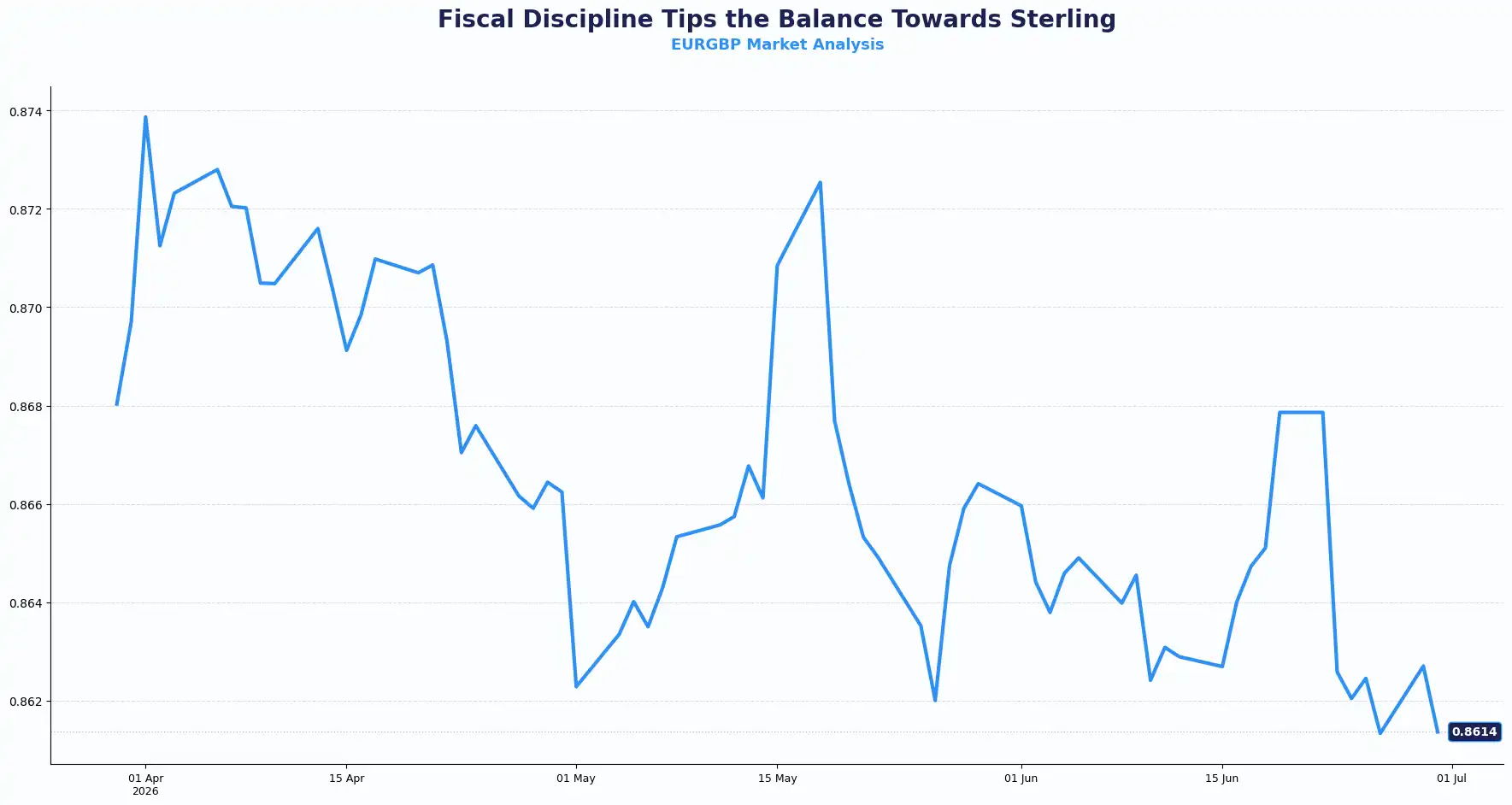

GBPUSD 1.3235 | EURGBP 0.8614

Sterling started the week on firmer footing after Andy Burnham signalled he would stick to the UK's existing fiscal rules if he becomes Britain's next prime minister. The move helped calm concerns over public borrowing, even as political uncertainty continues to dominate sentiment.

GBP/USD traded around 1.3230, while EUR/GBP slipped towards 0.8600 as traders gave the pound modest support. Even so, sterling is still on course for its weakest monthly performance since March after the dollar's broad rally gathered pace through June.

Burnham's commitment to Labour's 2024 manifesto and existing borrowing limits removed one layer of uncertainty, but it didn't remove all of it. He's held off on naming any cabinet appointments until the leadership process concludes, leaving the market's real question unanswered: who takes the Treasury? That appointment will shape whether UK borrowing costs stay anchored or start drifting again.

Gilt yields have nearly doubled since the pandemic, and continued deficit spending makes a fresh round of spending commitments the last thing the budget needs. Investors had largely priced in Starmer's exit; speculative positioning data from the CFTC shows the largest net short against sterling since June 2015, suggesting the pair is primed to react sharply in either direction once the chancellor pick is announced. At his Manchester speech, Burnham promised Britain's "biggest rebalancing of power," covering social housing, regional control of utilities, and a cost-of-living push, while insisting he'd deliver it within "the discipline of our current fiscal rules." UK 10-year gilt yields dipped slightly as he spoke, a signal the market took the reassurance at face value, even as some commentators flagged the speech as light on detail.

EUR/GBP held in negative territory near 0.8605 on Tuesday despite stronger German retail sales, with the euro unable to capitalise on the data against a steadier pound. Traders are watching Germany's preliminary June HICP print and, again, who Burnham appoints to run the Treasury, the same appointment likely to set the tone for gilts and sterling through July.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3350, 1.3300 and Support sits at 1.3200, 1.3150

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8660, 0.8640 and Support sits at 0.8590, 0.8565

EUR: Consumer Strength Fails to Offset Dollar Heat

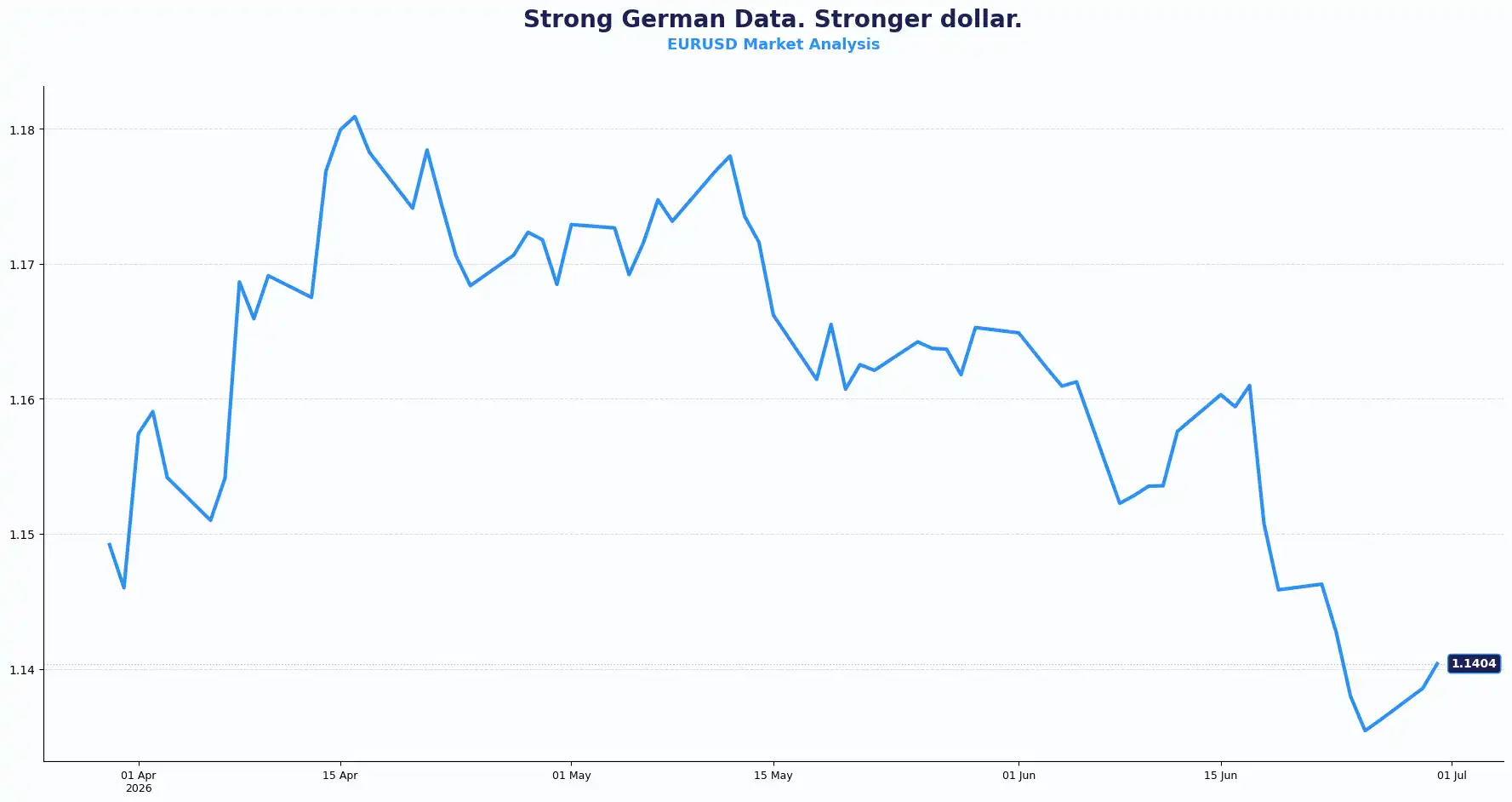

EURUSD 1.1404

EUR/USD slipped back towards 1.1385 on Tuesday, giving up Monday's gains and trading close to its lows for the year. The move came despite German retail sales jumping 1.8% year-on-year in May, comfortably ahead of the flat reading expected, and up 1.1% month-on-month against a forecast decline.

Strong German consumption data hasn't shifted the euro's trajectory because the bigger driver sits on the other side of the pair. The dollar is firming into a string of US employment releases, with the US JOLTS report due Tuesday and Thursday's NonFarm Payrolls figures another key event; consensus sits at 110K new jobs after May's 172K. That dollar pull is overwhelming what would, in a calmer week, be a euro-supportive surprise.

At the ECB's Sintra forum, Christine Lagarde struck a firmer tone, saying the central bank can lean on interest rates alone without reaching for unconventional tools, and warned that holding rates steady would have let inflation run above target into 2027 and 2028. Markets have nonetheless pared back expectations for further ECB hikes as energy prices ease; some economists expect the ECB is done with hikes for now, though some traders are still pricing a final quarter-point move to take the deposit rate to 2.50%.

Geopolitics added another layer to sentiment. Reports that US and Iranian negotiators could resume discussions in Doha helped keep oil prices close to pre-conflict levels. Lower energy prices generally support the eurozone economy by easing import costs, but that positive backdrop has yet to outweigh the dollar's strength.

For now, the euro continues to trade in the shadow of US policy expectations. Strong domestic data can provide temporary support, but traders appear unwilling to challenge the dollar until they have clearer evidence that the Fed's tightening cycle has peaked.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1460, 1.1420 and Support sits at 1.1350, 1.1300

USD: Strength Builds Into a Big Data Week

DXY 101.37

The dollar index sits at 101.37, recovering overnight losses and on track for a 1.4% rise this quarter, building on a 1.6% gain in Q1. Data shows investors have built dollar-strength bets at their fastest pace on record for the first half of the year.

That positioning is doing real work against every other major currency right now. The market also digested a Supreme Court ruling blocking President Trump from removing Fed Governor Lisa Cook, which eased some concern around the central bank's independence, a factor that had been quietly weighing on dollar sentiment. New Fed Chair Kevin Warsh speaks Wednesday at the ECB's Sintra gathering, and his tone will matter more than the data this week given how stretched dollar positioning already is.

The broader market view has shifted from asking whether the dollar can hold its gains to asking what continued dollar strength means for risk assets more broadly: current levels broadly match underlying fundamentals, which makes a sustained extra leg higher less likely from here, and some of the hawkish rate repricing may already be overdone.

Geopolitical risk hasn't gone away either. Iranian and US negotiating teams are due in Doha this week, but Iran says no meeting is confirmed, and weekend missile exchanges tested the ceasefire, keeping sentiment fragile even as headline risk appetite holds up.

Tuesday's JOLTS Job Openings report begins a run of labour data before Thursday's Non-Farm Payrolls release. Any surprise in either direction could reshape interest rate expectations and drive the dollar's next move.

The dollar still draws support from higher yields and resilient economic data. That combination continues to set the tone across the major currency pairs.

Others: Aussie, Kiwi and Yen All Buckle Under Dollar Strength

AUDUSD 0.6867 | NZDUSD 0.5643 | USDJPY 162.23 | GBPJPY 214.70

AUD/USD fell 0.3% to $0.6867, its lowest in three months and edging toward the March trough of $0.6834. NZD/USD eased to $0.5643, a fresh 2026 low, having now fallen in nine of the last ten sessions. USD/JPY broke above 162 to hit 162.23, a 40-year high for the pair.

The Reserve Bank of Australia's June minutes flagged continued upside inflation risk and a readiness to hike again, but Brent Crude has dropped 13% since that meeting, easing one of the central bank's main inflation worries and shifting the balance of risk toward growth. Markets now price just a 15% chance of an August hike and a 60% chance the RBA is done tightening altogether, with a first cut pencilled in for late 2027.

For the kiwi, sustained dollar strength is doing most of the damage, with bears now eyeing the $0.5581 support level.

The yen's story is structural rather than cyclical: a wide rate gap with the US has driven four straight quarters of decline, the longest such stretch in four years. Japan's Finance Minister Satsuki Katayama repeated that authorities stand ready to act, a notably calmer tone than prior intervention warnings, suggesting Tokyo isn't at the panic point yet. Even so, implying any intervention could slow rather than reverse the broader uptrend.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3235 | Bearish |

| EUR/GBP | 0.8614 | Bearish |

| EUR/USD | 1.1404 | Bearish |

| USD/JPY | 162.23 | Bullish |

| GBP/JPY | 214.70 | Bullish |

| AUD/USD | 0.6867 | Bearish |

| NZD/USD | 0.5643 | Bearish |

Market Lookahead

Tue, June 30

- UK GDP Q1

- Germany’s Consumer Price Index (CPI) (Jun)

- Germany’s Unemployment Rate (May)

- US Consumer Confidence (Jun)

Wed, July 1

- Eurozone Harmonised Index of Consumer Prices (Jun)

- US ISM Manufacturing PMI (Jun)

- ECB President Lagarde Speech

Thurs, July 2

- US Nonfarm Payrolls (Jun)

- US Unemployment rate (Jun)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.