Iran Strikes Lift the Dollar Ahead of FOMC Minutes

10 min read

Share

US airstrikes on Iran send safe-haven demands into the dollar. The euro holds above 1.1400 as ECB hawks flag inflation risk from Strait of Hormuz disruptions. The RBNZ hiked to 2.50%. Sterling softens as Burnham's leadership race opens. All eyes on Warsh's first FOMC Minutes today for the next policy signal.

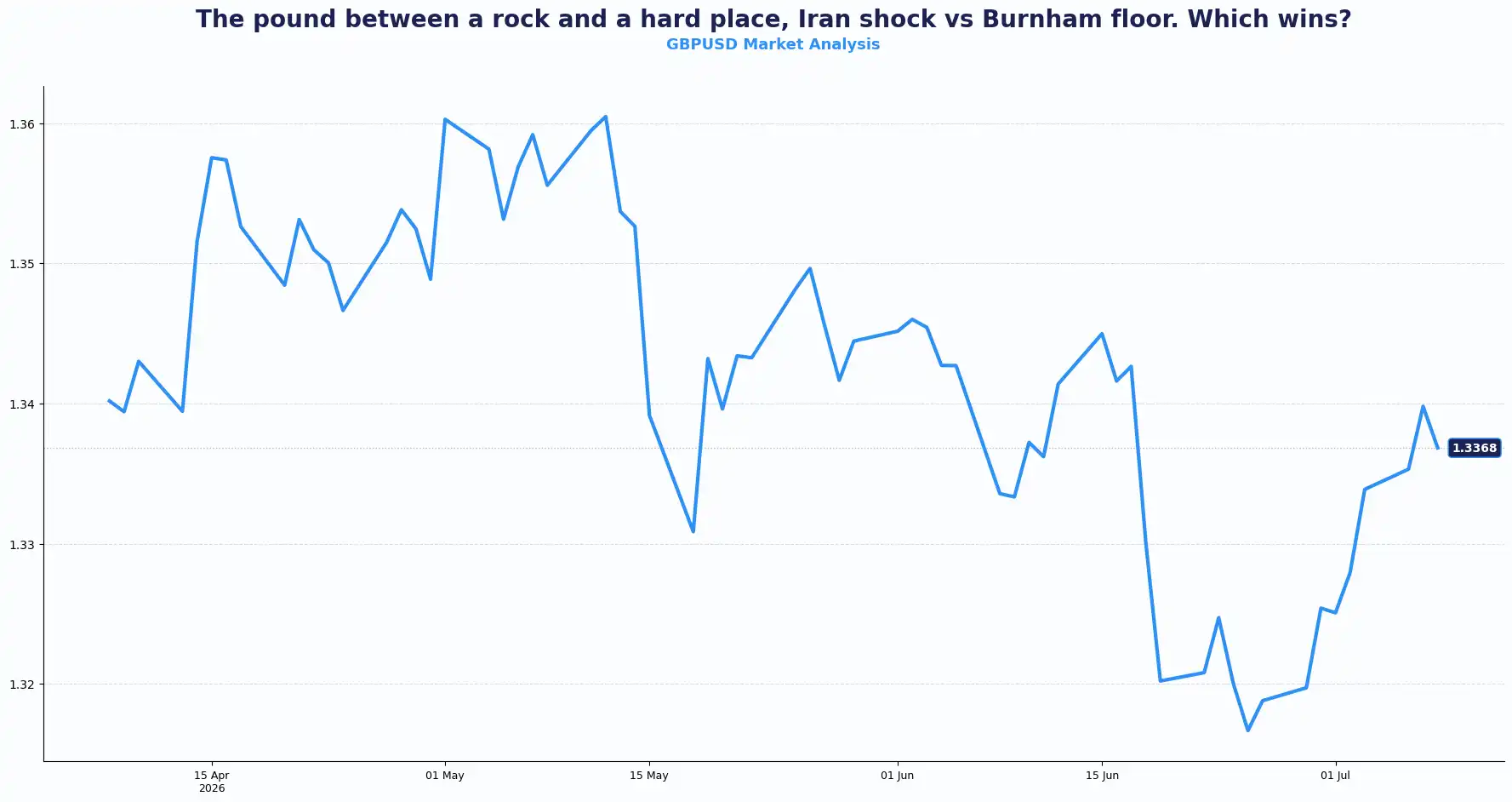

GBP: Sterling Gives Ground as Safe-Haven Demand Returns

GBPUSD 1.3368 | EURGBP 0.8549

The pound gave ground in Asian trade on Wednesday, slipping to 1.3350 against the dolla, Before trading near 1.3360. Fresh US strikes on Iran and renewed disruption concerns around the Strait of Hormuz pushed oil prices higher and revived demand for traditional safe-haven currencies. The same safe-haven demand flooded into the dollar while the sterling bore the brunt alongside other risk-sensitive currencies.

Higher oil prices also pushed global bond yields higher as traders reassessed inflation risks. That combination strengthened the dollar and weighed on sterling through the Asian session.

The move reflected global risk sentiment rather than any significant deterioration in UK fundamentals. Sterling had enjoyed a strong run over recent weeks as political uncertainty faded and investors reduced the domestic risk premium on UK assets, only to pause its support as geopolitical headlines dominated trading.

On the other hand, the UK political calendar introduces its own uncertainty. Nominations for the Labour leadership open on 9 July, with Greater Manchester Mayor Andy Burnham still viewed as the clear frontrunner to succeed outgoing Prime Minister Keir Starmer. Burnham is widely expected to take office by late July or August, depending on whether a contested vote proceeds. Expectations that a new government could be in place by around 20 July have helped calm domestic uncertainty. Investors have been pricing out domestic risk premium as his position consolidates his near-certain ascendancy to Downing Street has acted as a stabilising signal for sterling over recent weeks. That floor, however, only holds if the broader macro backdrop cooperates.

Sterling sits at a crossroads. Geopolitical pressure from the Middle East pushes Cable lower. Domestic political clarity around Burnham offers a partial offset. The combination suggests potential for elevated short-term volatility.

While geopolitical events continue to drive short-term price action, investors will also watch whether the next government can restore confidence in the UK's longer-term economic outlook.

The bigger driver, however, sits across the Atlantic. Rising oil prices have revived concerns that inflation could stay elevated for longer. That has pushed expectations for future Federal Reserve (Fed) policy slightly higher and strengthened the US dollar against most major currencies.

Current price swings reflect changing global sentiment rather than a material shift in the UK's economic outlook. As geopolitical headlines continue to move exchange rates, volatility across GBP pairs may stay elevated until clearer signals emerge from both policymakers and global risk events.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3470, 1.3450, 1.3400 and Support sits at 1.3320, 1.3275

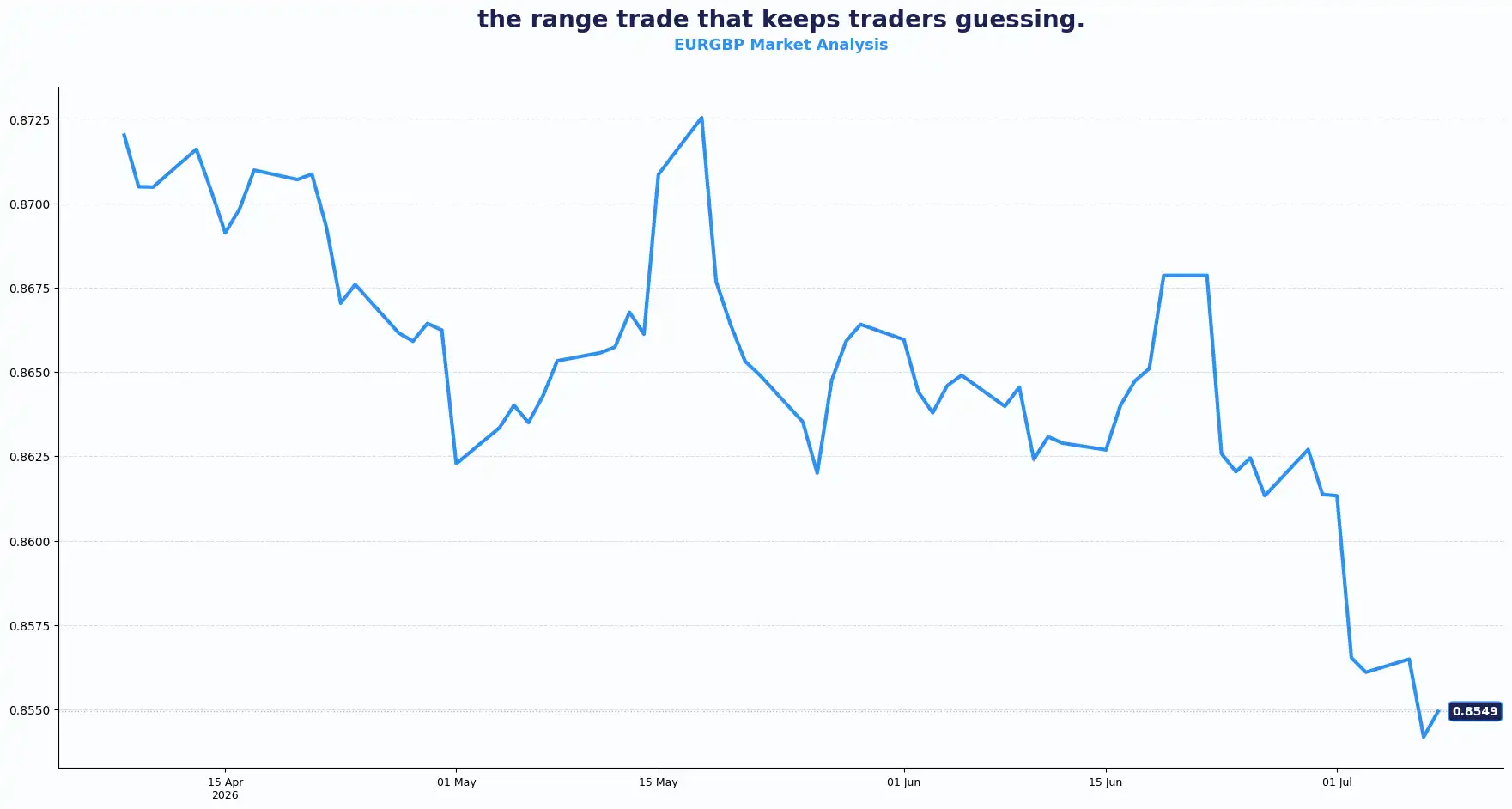

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8600, 0.8570 and Support sits at 0.8525, 0.8500

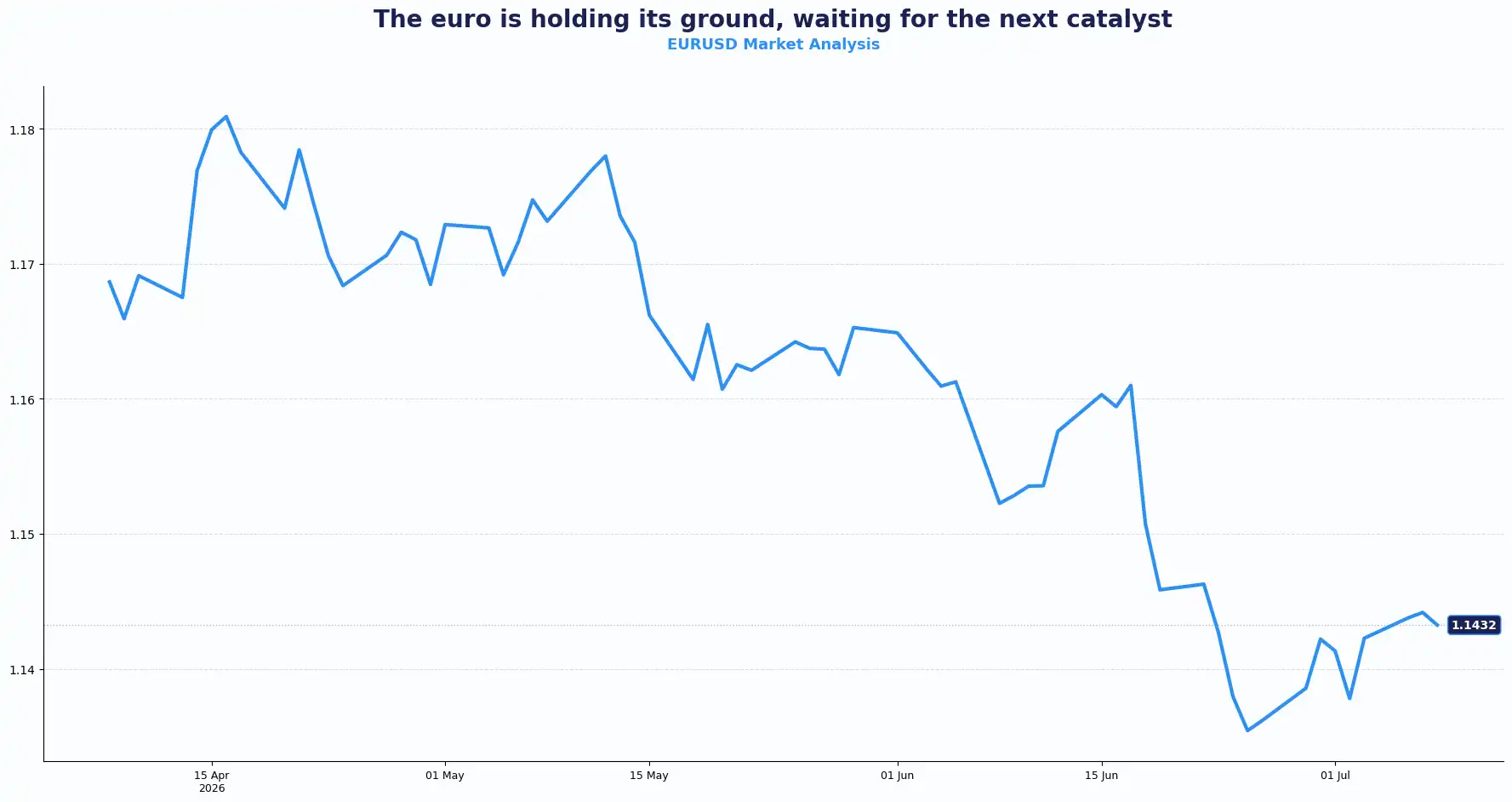

EUR: Euro Navigating Energy Inflation

EURUSD 1.1432

The euro traded near 1.1419 in the early Asian session, against the US dollar after giving back some of its recent rally. Price action has slowed following several weeks of gains, with traders now waiting for fresh direction from both the European Central Bank (ECB) and the Fed.

EUR/USD continues to hold above the important 1.1400 area, though buying interest has faded amid renewed geopolitical tensions that have boosted demand for the US dollar. The pair now sits in a broad consolidation range, with support developing around 1.1360 while resistance continues to build near 1.1450.

Attention now turns to the release of the latest FOMC minutes today, the first published under Chair Kevin Warsh. Investors hope the minutes will offer greater clarity on how policymakers view inflation risks following the recent rise in energy prices.

Oil has once again become the dominant variable. Fresh concerns over shipping through the Strait of Hormuz have lifted crude prices and increased expectations that energy costs could keep inflation elevated across advanced economies. That has complicated the outlook for central banks on both sides of the Atlantic.

Within the euro area, policymakers continue to acknowledge those inflation risks while balancing weaker economic growth. ECB member Fabio Panetta flagged that supply disruptions linked to the Middle East could keep inflation pressures alive for longer than expected. ECB Governor Isabel Schnabel reinforced the hawkish tone, noting that persistent energy shocks may require policymakers to stay cautious before considering any policy easing.

That backdrop has encouraged traders to trim expectations for near-term ECB rate cuts. While stronger oil prices could support inflation, they also risk slowing economic activity across the euro area. The ECB therefore faces an increasingly delicate balance between protecting growth and containing price pressures.

Attention will also shift towards this week's European data calendar. Two data points arrive this week that could further shape the trajectory. Germany releases its latest trade balance figures on Thursday, alongside an all-day Eurogroup meeting that could offer further insight into the region's fiscal priorities. Germany's June HICP inflation figures land on Friday. The consensus expects -0.2% MoM and 2.4% YoY, both unchanged from prior. A softer-than-expected print could give the ECB hawks pause. A surprise to the upside hardens the case for tightening.

Those data releases could help determine whether the euro breaks out of its current range or continues to consolidate ahead of the ECB's next policy meeting.

Against sterling, EUR/GBP traded around 0.8549, with both currencies largely responding to broader US dollar strength rather than domestic developments. Until geopolitical risks begin to ease, relative interest rate expectations and energy prices are likely to remain the primary drivers across the major European currency pairs.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1450, 1.1430 and Support sits at 1.1390, 1.1360

USD: Dollar Firms, Geopolitics Drive Sentiment ahead of FOMC

DXY: 101.34

The US dollar strengthened across most major currencies as investors sought safety after Washington launched a fresh round of strikes against Iran. Concerns over shipping through the Strait of Hormuz lifted oil prices and pushed the US Dollar Index (DXY) above 101, reversing part of last week's softer tone.

The shift came as traders reassessed the inflation outlook. Higher energy prices could slow the recent easing in inflation and influence the Fed's policy path over the coming months. That lifted US Treasury yields and gave the dollar broad support.

Attention now turns to the release of the June FOMC minutes. Traders will look for clues on how policymakers view inflation risks, labour market conditions and the balance between maintaining restrictive policy and supporting growth.

Recent US data have painted a mixed picture. The US trade deficit widened to $77.6 billion in May, its largest level since March 2025, highlighting continued strength in domestic demand alongside softer external trade. Even so, the latest geopolitical developments have overshadowed economic releases for now.

Interest rate expectations also shifted. Futures pricing now points to roughly a 50% probability of a September rate increase, slightly higher than earlier this week as investors factor in the inflationary effect of higher oil prices.

The next move for the dollar could depend on whether the Fed Minutes reinforce that view. Any indication that policymakers are prepared to keep interest rates higher for longer could extend the dollar's recent gains.

For now, geopolitical headlines continue to set the pace. Until tensions ease, shifts in oil prices and Treasury yields are likely to have a greater influence on the dollar than routine economic data.

Other Currencies: Regional Shifts

NZDUSD 0.5718 |AUDUSD 0.6943 | USDJPY 162.25 | GBPJPY 216.74

Renewed geopolitical uncertainty created a mixed picture across commodities and Asia-Pacific currencies. Safe-haven demand supported the US dollar, while central bank expectations and domestic data drove individual currency moves.

Japanese yen

The Japanese yen weakened towards 162.25 per US dollar, moving back towards multi-decade lows as the widening interest rate gap between Japan and the United States continued to favour the dollar.

Japan's heavy reliance on imported energy left the yen exposed after crude oil prices surged. Higher import costs could add further pressure to domestic inflation while weighing on household spending and business activity.

Markets also continued to question whether Japanese authorities would intervene to support the currency. Finance Minister Satsuki Katayama reiterated that officials stood ready to respond if necessary and confirmed ongoing dialogue with US counterparts. Even so, traders continue to view intervention as a tool that may smooth volatility rather than reverse the broader trend.

Australian dollar

The Australian dollar traded around 0.6943, close to three-month lows as weaker global risk appetite offset resilient domestic fundamentals.

RBA Assistant Governor Sarah Hunter acknowledged that higher oil prices had weighed on business and consumer confidence, but said the Australian economy remained resilient. She also reiterated that the RBA stands ready to respond if inflation deviates from the target.

Interest rate expectations have eased slightly following three increases earlier this year. Current pricing suggests the RBA is likely to leave rates unchanged in August, while expectations for another increase later in the year have moderated.

China's latest inflation data, due on Thursday, could also influence the Australian dollar given Australia's close trade links with the Chinese economy.

New Zealand dollar

The New Zealand dollar outperformed many of its peers after the Reserve Bank of New Zealand (RBNZ) raised the Official Cash Rate (OCR) to 2.50%, matching expectations.

The initial move higher reflected the rate increase itself, although the central bank's guidance attracted greater attention. Policymakers signalled that inflation uncertainty had increased and suggested that further policy tightening could still be required if price pressures proved more persistent.

Governor Christian Hawkesby noted that inflation may already have peaked but stressed that the neutral interest rate remains uncertain. Officials continue to assess incoming data before determining the pace of future policy changes.

The more hawkish tone offered short-term support for the kiwi after several weeks of weakness against the US dollar.

Canadian dollar

The Canadian dollar lost ground as broad US dollar strength outweighed support from higher crude oil prices.

USD/CAD edged higher as investors favoured the dollar amid developments in the Middle East. Under normal conditions, stronger oil prices often benefit the Canadian dollar given Canada's position as a major energy exporter. This week, however, demand for safe-haven assets proved stronger.

Chinese yuan

The Chinese yuan traded within a relatively narrow range against the US dollar despite broader strength in the Greenback.

Attention shifted towards Thursday's inflation figures and developments in China's energy sector after authorities eased July fuel export restrictions. The decision allows refiners to resume exports following several months of disruption and may help stabilise regional fuel supplies if current policy continues.

Swiss franc

The Swiss franc softened against the US dollar as investors continued to favour the Greenback during the latest bout of geopolitical uncertainty.

USD/CHF traded near 0.8090, extending its recent advance as rising global bond yields and stronger demand for US assets outweighed the franc's traditional safe-haven appeal.

Switzerland's 10-year government bond yield also rose alongside global borrowing costs, as investors reassessed inflation risks amid rising energy prices.

Indonesian rupiah

The Indonesian rupiah stayed under pressure after June consumer confidence fell to 117.8, down from 120.9 in May.

The softer reading added to existing pressure from a stronger US dollar, leaving USD/IDR higher ahead of the latest FOMC Minutes.

The common thread across the major currency pairs is no longer domestic data. Geopolitical developments have once again taken the lead, with oil prices, inflation expectations, and interest rate pricing driving moves across the FX landscape.

That focus could shift quickly once the FOMC Minutes are released. If policymakers signal greater concern over inflation risks linked to higher energy prices, interest rate expectations may adjust again. If the tone proves more balanced, attention could return to domestic economic data and central bank guidance.

For now, price action continues to reflect a cautious global backdrop. Currency movements remain closely tied to incoming geopolitical headlines, making cross-asset sentiment just as important as scheduled economic releases.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3368 | Bearish |

| EUR/USD | 1.1432 | Neutral to Bullish, range |

| EUR/GBP | 0.8549 | Range-bound |

| USD/JPY | 162.25 | Bullish |

| GBP/JPY | 216.74 | Range-bound |

| AUD/USD | 0.6943 | Bearish |

| NZD/USD | 0.5718 | Neutral |

| USD/CHF | 0.8090 | Bullish |

| USD/CAD | 1.1461 | Bullish |

Market Lookahead

Wed, July 8

- FOMC Minutes

Thurs, July 9

- Germany’s Trade Balance

Fri, July 10

- Germany’s HICP (Jun) inflation

Speeches from BoE, ECB and Fed members through the week

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.