Dollar Dims as NFP Miss Steals the Fireworks

9 min read

Share

A 57,000 NFP print, less than half the forecast. The dollar posts its worst week since April as US desks close early for Independence Day. Sterling gained on Mann's hawkish pivot. The euro held near two-week highs despite cooler CPI trimming ECB hike bets. Liquidity thins into the close.

GBP: Sterling Gains Ground

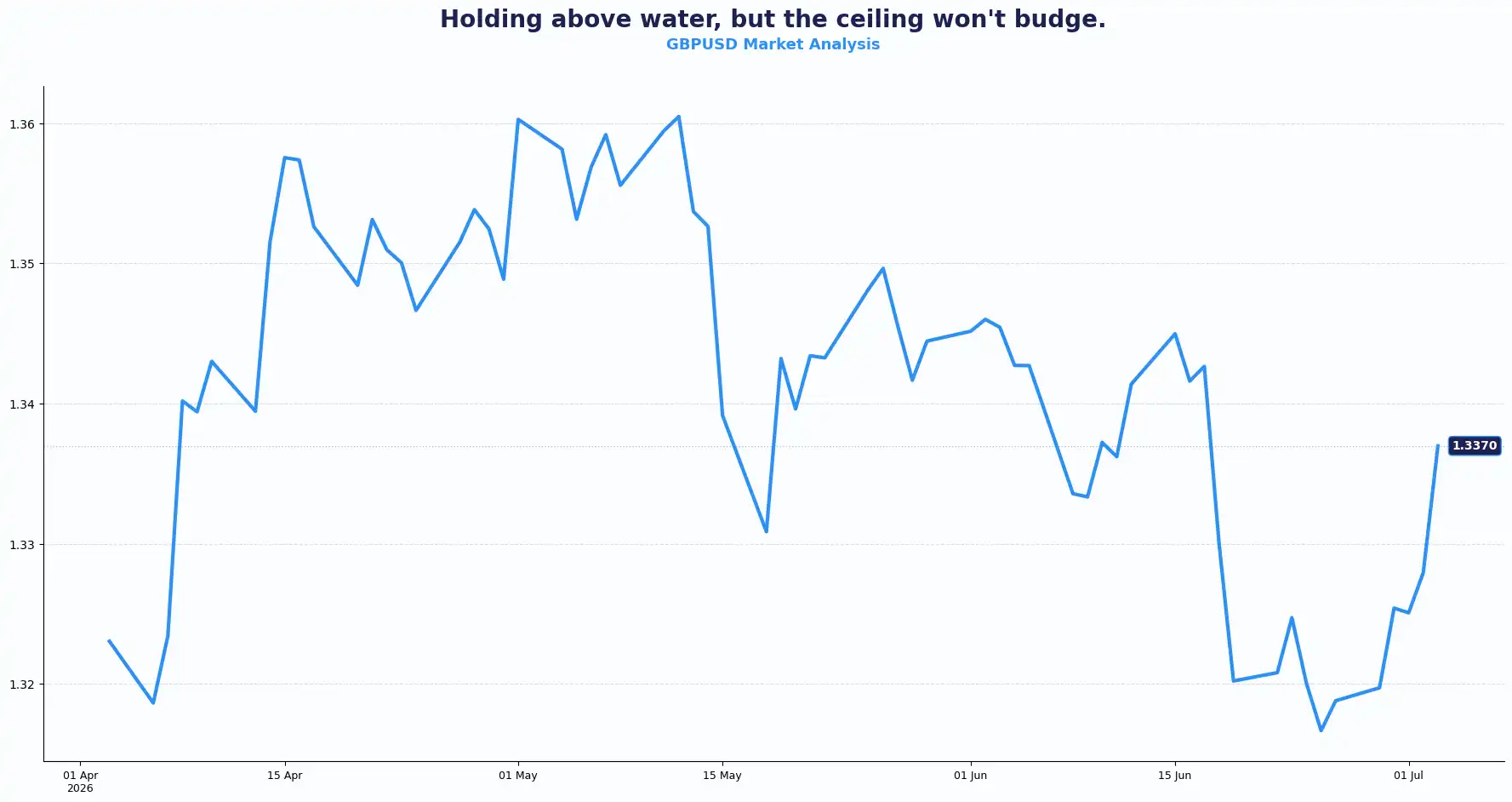

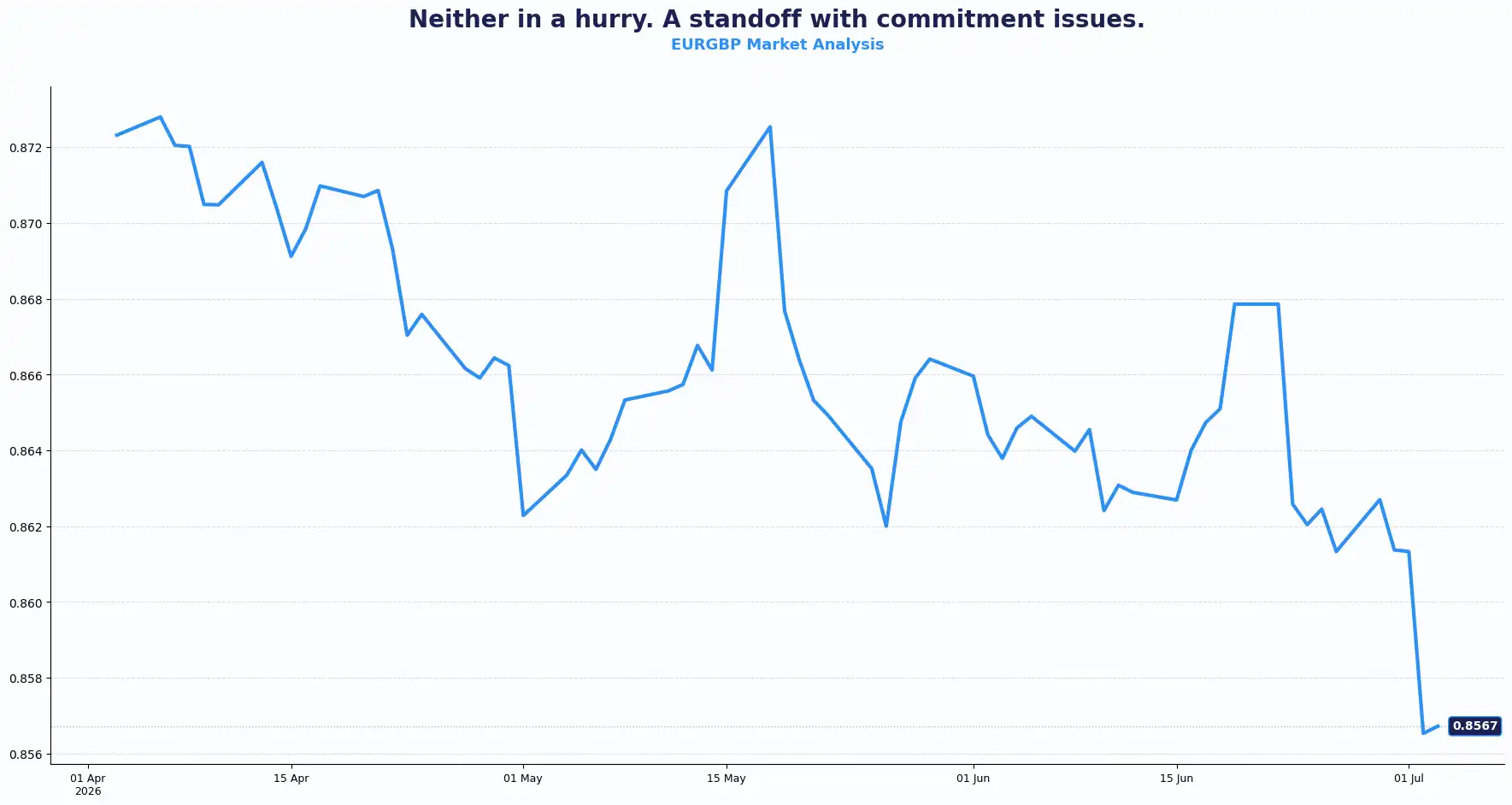

GBPUSD 1.3370 | EURGBP 0.8567

Sterling heads into the end of the week with fresh momentum, with GBP/USD touching 1.3370, a 1.2% weekly gain and marking a three-month-high. The cooling US labour market provided the catalyst, weighing on the dollar. At the same time, EUR/GBP eased towards 0.8567 as investors reassessed the outlook for UK interest rates.

The shift came after Bank of England (BoE) policymaker Catherine Mann adopted a noticeably firmer stance on inflation. Mann stated her view has shifted away from considering a rate reduction toward a longer hold, and potentially toward a tilt against inflation risk. She described the June hold as an "activist" decision, adding that tightening the bank rate could have made sense but that market rates had already tightened in nominal terms. Her forward guidance centred on energy price developments, profit margins, and 2027 wage negotiations as the key variables the BoE will be watching closely. Crucially, Mann placed greater weight on inflation persistence since the Iran conflict began, reinforcing the view that geopolitical commodity pressure is feeding into policy calculus. Markets have already priced in a 90% probability of a BoE hike before the year is out.

The domestic political backdrop adds another layer to sterling's positioning. Since Keir Starmer's resignation last week, Andy Burnham's early commitment to fiscal discipline has offered near-term support to the pound. Analysts note that any future budget seen to be relaxing fiscal rules in favour of higher public spending would likely challenge that support. GBP/USD is trading above 1.3350 but has not convincingly cleared the 100-day average. The 100-day moving average, currently at 1.3410, has so far capped upside. The initial support floor sits at 1.3300.

The BoE is widely expected to leave the Bank Rate unchanged at its next meeting. Even so, interest rate pricing continues to reflect expectations that policy could stay restrictive for longer than previously anticipated if inflation proves harder to bring back to target.

For now, sterling's strength reflects two forces working together. The BoE has adopted a more cautious approach to easing policy, while softer US economic data has eroded some support for the dollar. Together, those themes have helped lift the pound into the final trading session of the week.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3410, 1.3300 and Support sits at 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8600 and Support sits at 0.8530

EUR: Euro Balances Softer Inflation with Steady Growth

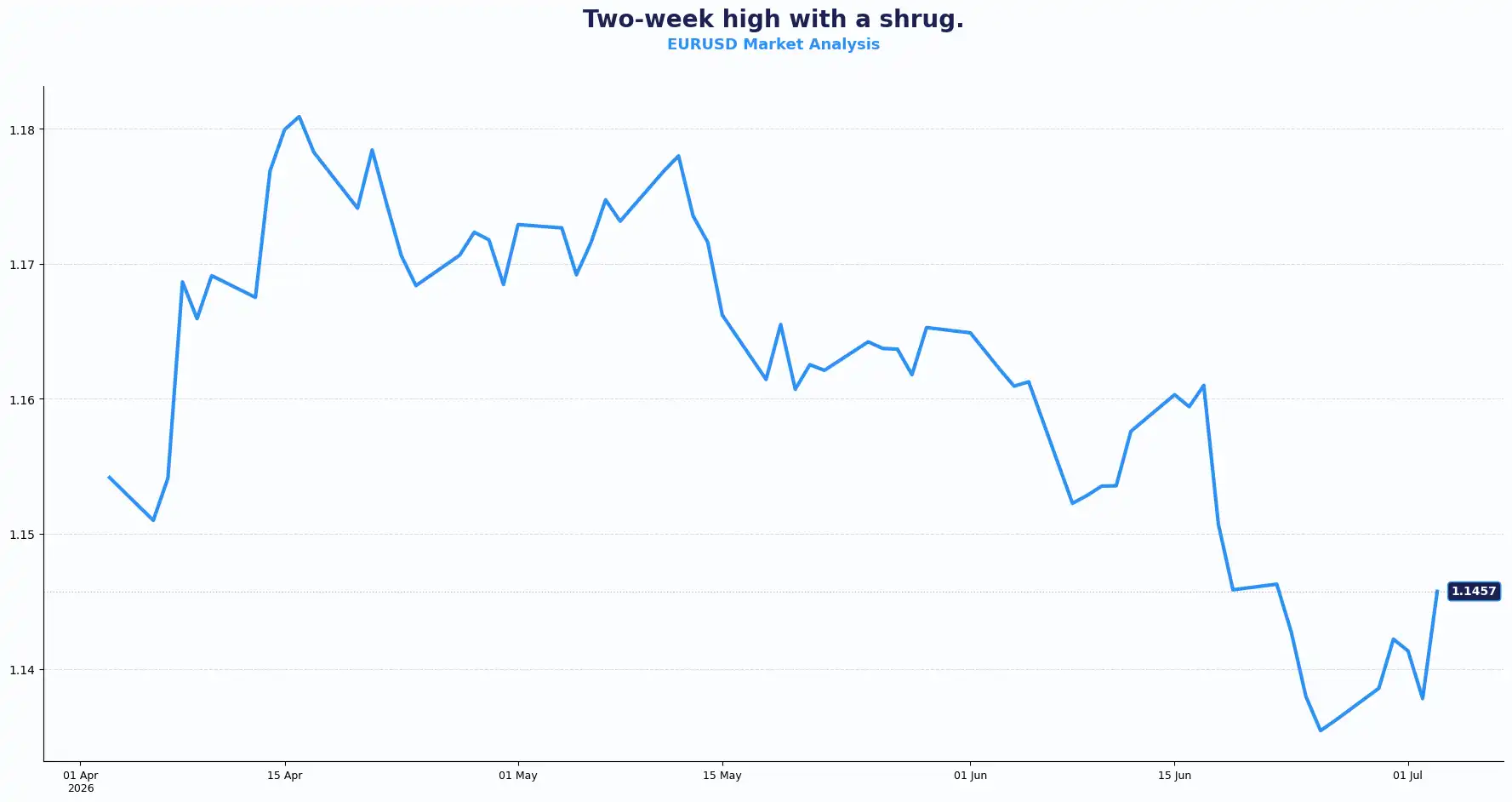

EURUSD 1.1457

The euro held close to 1.1457 against the dollar after earlier climbing to its strongest level in almost two weeks. Although gains eased slightly, the single currency still benefited from broad dollar weakness following the softer US employment report.

Recent Eurozone inflation figures have cooled expectations for another immediate European Central Bank (ECB) rate increase. Headline inflation slowed to 2.8% in June, while core inflation also eased, giving policymakers greater confidence that price pressures are moderating.

Even so, ECB Christine Lagarde struck a measured tone. She defended June's rate increase, said the Governing Council continues to monitor second-round inflation effects closely, and noted that national central banks still see sufficient evidence of economic growth to avoid lowering their forecasts.

Lagarde also acknowledged she "honestly doesn't know" whether the ECB will tighten again, a statement that, given her usual precision, reads more like a deliberate signal than an offhand comment. Her additional remark about potentially providing a "European voice" in the French presidential debate introduced a political dimension that the market noted, though she quickly added that her ECB term runs until October 2027 and her duty lies with the institution.

The combination presents a more balanced picture for the euro. Softer inflation reduces pressure for another rapid move higher in interest rates, but resilient economic activity also limits expectations for aggressive policy easing. Domestic inflation data argues for patience from the ECB, while broader dollar weakness provides near-term support for EUR/USD.

European equity futures also pointed to a firmer start, adding to the constructive tone across risk assets. Stronger sentiment tends to support higher-beta currencies against the dollar, although interest rate expectations continue to drive the largest moves across the major pairs.

From a technical perspective, 1.1500 remains the next key upside area for EUR/USD after buyers defended support around 1.1400. Whether the pair can establish itself above recent highs could depend less on Eurozone data and more on how expectations for Fed policy evolve following the latest US employment figures.

The EUR/USD upside bias is now capped by the resistance cluster near 1.1450. Softer inflation data has reduced the urgency for further ECB tightening, and Lagarde's openly uncertain guidance has trimmed the policy premium that had been supporting the euro through June. The pair looks to next week's data calendar to establish its next range.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1450-1.1454 and Support sits at 1.1420 1.1340

USD: A Soft Jobs Print Clips the Dollar's Wings

DXY 100.70

The US dollar heads towards its biggest weekly decline since April after June's labour report missed expectations and prompted traders to scale back expectations for another near-term Federal Reserve (Fed) rate increase. The dollar index (DXY) slipped to around 100.70, extending Thursday's losses and breaking a two-week run of gains.

The headline numbers told the story. The US economy added 57,000 jobs in June, well below expectations of around 115,000, while payroll figures for the previous two months were revised lower. Although the unemployment rate edged down to 4.2%, hiring momentum has slowed enough to shift the conversation away from another immediate rate increase.

That change quickly filtered through interest rate expectations. CME FedWatch pricing now points to roughly a 50% probability of a September rate hike, down sharply from around 65% before the employment report. Treasury yields also moved lower, with two-year yields giving back part of this week's earlier advance.

The latest figures also followed weaker-than-expected private sector employment data earlier in the week, reinforcing signs that labour demand is beginning to cool. At the same time, easing energy prices and moderating inflation expectations have reduced pressure on the Fed to tighten policy again in the immediate term.

Fed Chair Kevin Warsh urged caution against placing too much weight on a single employment report, noting that payroll data often changes after subsequent revisions. Even so, the latest release has shifted attention towards incoming inflation and activity data rather than another immediate policy move.

The dollar's decline has supported most major currencies over recent sessions. Sterling and the euro both strengthened, while higher-beta currencies such as the Australian and New Zealand dollars also recovered ground.

The broader picture has not changed completely. US interest rates still sit well above many developed economies, which continues to offer underlying support for the dollar over the medium term. For now, however, softer economic data has interrupted that advantage and encouraged a period of consolidation.

Other Currencies: Yen, Aussie, and the EM Pressure Points

AUDUSD 0.6942 | NZDUSD 0.5717 | USDJPY 161.00 | GBPJPY 215.40 | USDCNH 6.7845 | USDIDR ~18000

Yen: Intervention Risk Stays Live

USD/JPY sat near 161.00 on Friday after a sharp 1% reversal in the previous session. Japanese Finance Minister Satsuki Katayama reiterated this week that authorities stand ready to intervene in the currency market at any time. Thursday's yen rebound came on reports suggesting Japan may abandon its habit of telegraphing intervention plans in advance, catching speculative short positions off guard. Japan and the US are reported to be in close communication on FX policy. The 162.83 level is flagged by analysts as the short-term top for USD/JPY, with thin holiday liquidity creating conditions that have historically suited intervention. GBP/JPY tracked the broader moves, printing at 215.40.

Australian Dollar: Hawkish RBA Minutes Provide a Floor

AUD/USD strengthened to $0.6942 and looks set to snap a four-week losing streak. The RBA's June meeting minutes struck a hawkish tone, with both CBA and ANZ interpreting persistent references to excess demand and capacity constraints as a signal the bank is not done tightening. Markets price a 15% chance of an August hike, with around 50% odds the tightening cycle has ended, but the minutes leave that picture deliberately open. Australia's composite PMI was revised up to 50.4 in June from an initial estimate of 49.8, with services returning to expansion at 50.5. The softer dollar also supported the move.

New Zealand Dollar

NZD/USD held at $0.5717, up 1.4% for the week, primarily tracking the broader dollar retreat rather than domestic catalysts.

Chinese Yuan

The offshore yuan (USD/CNH) edged to 6.7845 per dollar, on track for its first weekly gain in three weeks. June PMI data and high-frequency indicators point to an export-led recovery, while domestic demand and the property market stay soft. Credit and inflation data are the focus for the coming week. A Fed pause in the second half of this year is flagged by strategists as a potential headwind reduction for the yuan, alongside China's structurally large trade surplus.

Turkish Lira

High underlying domestic inflation keeps the lira structurally exposed, even as global disinflation continues. Analysis suggests that if Turkey's inflation problem is domestically driven and entrenched in expectations rather than imported, the Central Bank of the Republic of Türkiye cannot safely cut rates without putting the currency under renewed pressure. The lira is closely watching the CBRT's next signal.

Indonesian Rupiah

USD/IDR traded near 18,000 during Asian hours. Indonesia registered a surprise $1.61 billion trade deficit in May, its first since 2020 alongside a three-month inflation high of 3.34% in June. Analysis suggests that declining foreign exchange reserves could threaten Indonesia's sovereign credit rating.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3370 | Firm but capped |

| EUR/USD | 1.1457 | Soft bias below resistance |

| EUR/GBP | 0.8567 | Contained |

| AUD/USD | 0.6942 | Recovery mode |

| NZD/USD | 0.5717 | Supported |

| USD/JPY | 161.00 | Capped by intervention risk |

| GBP/JPY | 215.40 | Directional with USD/JPY |

| USD/IDR | ~18,000 | Under pressure |

| USD/CNH | 6.7845 | Slight recovery |

Market Lookahead

Mon, Jul 6

- Eurozone PPI, Retail Sales

- US ISM services PMI

- BoE Mann’s Speech

- Fed Waller Speech

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.