Trump Ends Iran Truce, Oil Soars, Dollar Holds Firm

10 min read

Share

Trump declared the US-Iran ceasefire over. The US military struck Iranian targets for a second straight day. Brent crossed $80. Fed hike bets jumped back into play. Sterling steadied above 1.34 on Burnham succession odds. Germany's trade surplus blew past forecast.

GBP: Sterling Above 1.34 as Succession Race Begins

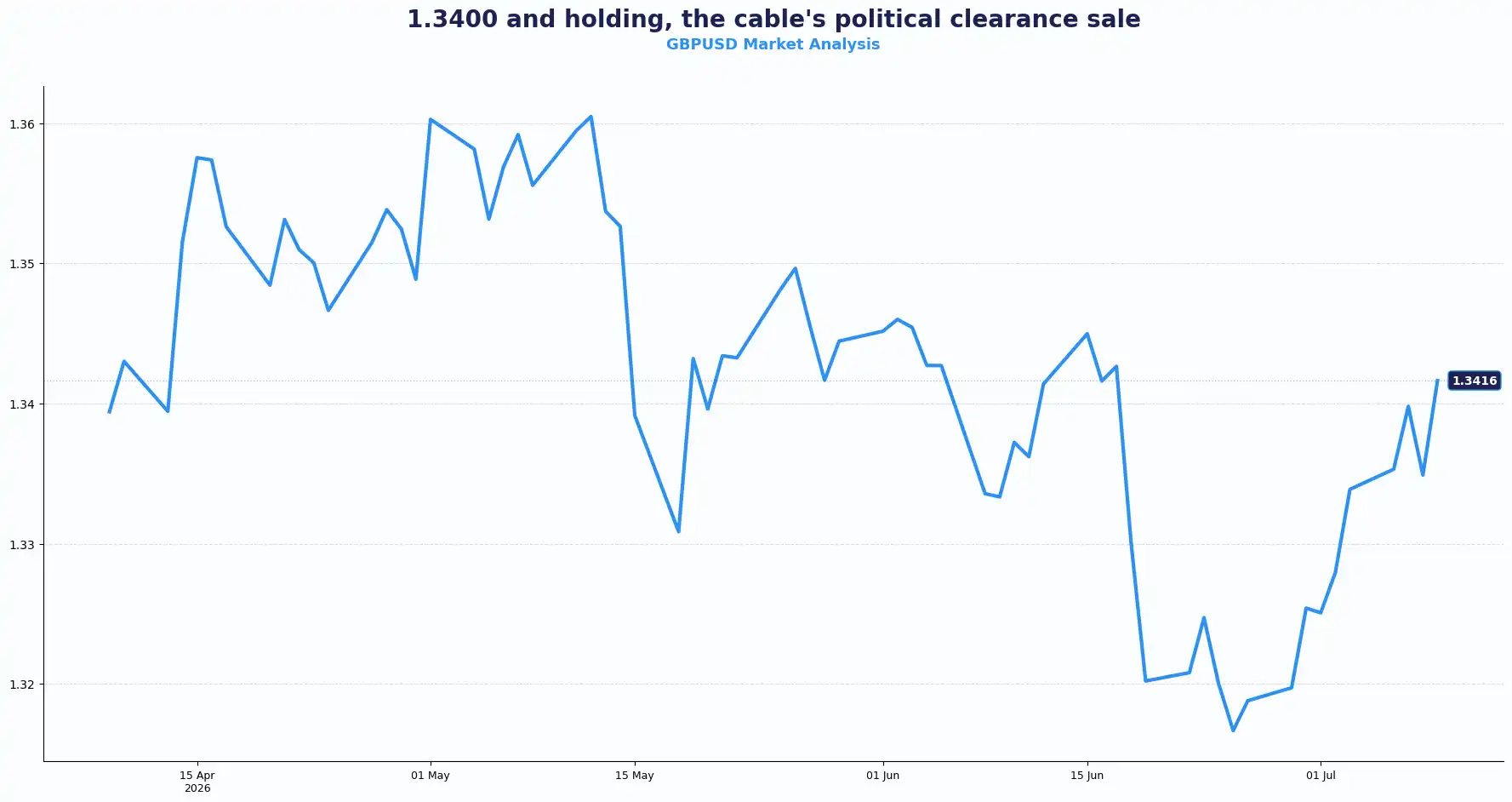

GBPUSD 1.3416 | EURGBP 0.8523

The pound holds a constructive tone above 1.3400, trading near 1.3395 during Asian hours. The domestic political picture has shifted decisively. Keir Starmer resigned in late June, and the Labour leadership nomination window opened today with Andy Burnham as the frontrunner. Burnham won the Makerfield by-election on 18 June, securing the parliamentary seat he needed to stand. Wes Streeting, widely seen as his main rival, endorsed him. Markets expect him to become prime minister with a 97% probability, with confirmation possible as early as 17 July if no opponent emerges. That reduction in political uncertainty has provided a meaningful lift to sterling.

The Bank of England's (BoE) communication has become a key support factor for the pound. Governor Andrew Bailey has argued that tighter financial conditions have already delivered part of the required policy tightening. That approach reduces pressure for aggressive rate increases while keeping inflation credibility intact.

Compared with the ECB, the BoE has shown more willingness to look through temporary supply shocks. Investors appear comfortable with that trade-off for now. The result is a pound that has proved more resilient than many expected amid political noise and uneven UK growth data.

For GBP/USD specifically, geopolitical cross-currents constrain the upside. Hawkish FOMC minutes released Wednesday, the first under new Fed Chair Kevin Warsh, and a sharp escalation in US-Iran hostilities sent safe-haven dollar demand higher. Brent Crude jumped over 5% after President Trump declared the interim Iran ceasefire agreement "over", following fresh US strikes on Iran. Higher oil prices fuel US inflation expectations, which in turn boost Fed-hike bets, supporting the dollar and capping the cable rally.

Sterling's political discount is unwinding. Sterling has held its ground despite geopolitical stress and shifting Fed expectations. The succession of Starmer to Burnham, a frontrunner with strong regional governing credentials and market-calming fiscal commitments, reduces one of the key overhangs on the pound in recent weeks. The pair's constructive bias above 1.3400 reflects that repricing. The opposing force is the US dollar, which finds fresh support each time the Middle East conflict intensifies. GBP/USD is caught between two competing narratives for now.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3500, and Support sits at 1.3350, 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8550, 0.8580 and Support sits at 0.8470, 0.8500

EUR: Euro Holds Above 1.1400 as Germany Beats on Trade

EURUSD 1.1438

EUR/USD trades with a positive bias above 1.1400, last seen around 1.1426–1.1431 during Asian hours. The pair held above the 1.14 level after Germany reported a much stronger-than-expected trade surplus. Germany's May trade balance landed at €19.1 billion, decisively above the consensus estimate of €14.8 billion and well clear of April's €14.7 billion reading.

This is a meaningful beat as Germany's export engine still carries significant weight for the euro. A surplus of this size points to robust export demand for German goods and confirms that Europe's industrial engine is outperforming expectations despite a softer global backdrop,at least on the external balance front. European equity futures pointed higher by around 1%, with US futures adding a modest 0.2%.

The trade data arrived ahead of Germany's June HICP inflation figures, due tomorrow. The Harmonised Index of Consumer Prices (HICP) measures German inflation on a methodology standardised across the European Union, making it a direct input into ECB policymaking. A higher-than-expected reading would likely be read as euro-supportive; a softer print could rekindle downside pressure on ECB rate expectations following the unexpected fall in eurozone-wide inflation in recent weeks. ECB rate-hike bets have come under downward pressure in the wake of that inflation surprise. Traders now look to the release of the ECB's June monetary policy meeting accounts alongside US weekly initial jobless claims for fresh direction.

The EUR/USD pair's gain faces structural limits on two fronts. The escalation in US-Iran tensions pushes oil higher and adds inflationary risk in the US, reinforcing the case for the Fed to hold or hike rates and boosting the dollar relative to the euro. Second, ECB rate expectations have softened following the eurozone inflation undershoot, removing one of the structural tailwinds that drove EUR/USD higher through late spring.

The strong German trade surplus is the standout data point of the European session. It underscores the resilience of Germany's export sector even against a backdrop of Middle East conflict and global cost pressures. EUR/USD holds its constructive bias above 1.1400, but the pair's upside likely hinges on whether Thursday's German HICP confirms or undermines the optimism generated by the trade data. ECB meeting accounts and US jobless claims data later today provide the next test.

The common thread between sterling and the euro is policy divergence.

Neither currency is rallying because central banks are turning aggressively hawkish. Instead, both are benefiting from a dollar that cannot decide whether oil-driven inflation risks or softer Fed expectations will dominate.

That tension has kept GBP/USD above 1.34 and EUR/USD above 1.14, while leaving both pairs sensitive to every shift in energy prices, Treasury yields and central-bank commentary.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1460, 1.1500 and Support sits at 1.1380, 1.1340

USD: Dollar Holds Firm as Oil Surge Clouds the Fed Outlook

DXY 100.92

The US Dollar Index (DXY) traded around 100.92, holding just below 101.00. The Fed minutes failed to deliver a decisive hawkish surprise, which kept the dollar under pressure early in the session. Fresh US-Iran tensions and a sharp rise in oil prices quickly limited those losses.

On one side, the June FOMC minutes showed policymakers still divided on the next rate move. On the other hand, rising oil prices have revived inflation concerns and prompted investors to reassess how long interest rates may stay elevated.

After President Trump declared the Iran ceasefire agreement "over" ahead of the NATO summit in Turkey, following fresh US military strikes on Iranian targets for a second consecutive day. Iranian Speaker Mohammad Bagher Ghalibaf warned that any further US action would trigger immediate retaliation.

US 10-year and 30-year Treasury yields hit seven-week highs as the oil spike revived inflation expectations and pushed up rate-hike bets. CME FedWatch now prices approximately an 87% probability of at least one Fed rate hike in 2026, up from around 38 basis points of expected tightening priced prior to this week's events.

The June FOMC minutes, first produced under Chair Kevin Warsh, confirmed what the June dot plot had signalled: a deeply divided committee. The vote to hold the federal funds rate at 3.50%-3.75% was unanimous. But the internal debate was not. A handful of participants saw an immediate case for hiking and agreed to hold only reluctantly. The broader committee split into two camps: one favouring rates at or slightly below the current range by year-end, the other concluding rates need to go higher. Nine of the 18 policymakers who submitted projections pencilled in at least one hike before year-end; a reversal from March's cut-leaning median. Consumer prices rose 4.2% year-on-year in May, a three-year high. Warsh himself declined to submit a projection, consistent with his stated intention to end forward guidance. The message the committee agreed on was unambiguous: "The Committee will deliver price stability." No qualifiers. The brevity of that sentence drew as much attention as the minutes themselves.

The oil-inflation feedback loop is the most consequential second-order effect of the current escalation in the Middle East. Higher energy prices raise the near-term inflation outlook. A higher inflation outlook raises the probability of a Fed hike. A higher probability of a Fed hike supports the dollar. That chain of causality is intact and active.

Dollar crosses into this session with dual support from geopolitical risk premium and a Fed that has signalled it is not done tightening. The DXY holding just below 101.00 reflects a market that is cautious about committing to a sustained breakout; there is still division on the FOMC but equally reluctant to sell the dollar while oil surges and safe-haven flows persist. The next FOMC meeting is scheduled for 28-29 July.

The dollar is no longer reacting to Fed commentary alone. Energy prices, geopolitical headlines and bond yields are moving together. That combination has increased volatility across major currency pairs and could continue to influence pricing until inflation expectations stabilise.

Other Currencies:

USDJPY 162.37 | GBPJPY 217.66 | NZDUSD 0.5725 | AUDUSD 0.6936

Yen Faces Renewed Pressure

The Japanese yen stayed under pressure as higher oil prices added another challenge for Japan's import-dependent economy. Rising crude prices increase import costs, widen trade pressures and weigh on the yen. The wider yield gap between the US and Japan has encouraged investors to favour the dollar over the yen.

Traders also noted the absence of any fresh intervention by Japanese authorities despite the yen trading near multi-decade lows. Attention has now shifted towards official intervention data later this month for further clues on Tokyo's actions.

Australian Dollar Holds Steady

The Australian dollar traded in a relatively narrow range. China's June CPI came in softer than expected, slowing from prior figures, a reminder that China's domestic demand recovery remains uneven. Under normal circumstances, that would pressure the Australian dollar because of Australia's close trade links with China. However, stronger commodity prices provided support and helped offset some of that weakness. The result was a balanced session with neither buyers nor sellers taking firm control.

Kiwi Extends Gains

The New Zealand dollar outperformed many of its peers. The Reserve Bank of New Zealand's recent hawkish stance continued to underpin the currency, while New Zealand's manufacturing sector expanded at its fastest pace in five years. Businesses reported stronger sales, fuller order books and improving confidence despite ongoing geopolitical tensions. Those factors helped the kiwi maintain its recent momentum against the dollar.

Canadian Dollar Draws Support from Oil

The Canadian dollar found support as crude oil prices continued to climb. Canada benefits from higher energy prices because oil exports make up a significant share of the country's external trade. At the same time, expectations that the Bank of Canada could maintain a relatively firm policy stance also supported the currency.

Swiss Franc Finds Defensive Demand

The Swiss franc strengthened modestly as investors sought traditional defensive currencies amid renewed tensions in the Middle East. While the dollar attracted most safe-haven flows, the franc also benefited from broader risk aversion and uncertainty surrounding the Fed's policy outlook.

Yuan Stabilises After Stronger PBOC Fixing

China's yuan recovered from recent weakness after the People's Bank of China set its strongest daily reference rate in almost three years. The central bank also reiterated its commitment to maintaining an accommodative monetary policy while supporting domestic consumption. Those signals helped steady sentiment, although concerns around uneven domestic demand continue to limit stronger gains.

The story across the major currencies comes back to one question.

Will higher oil prices prove temporary, or will they feed into inflation for long enough to influence central bank policy?

For now, sterling draws support from improving domestic confidence. The euro benefits from stronger economic data. The dollar gains backing from geopolitical uncertainty and higher bond yields. Commodity-linked currencies are taking their cues from energy prices, while the yen continues to struggle against widening interest rate differentials. Incoming inflation data and central bank communication are likely to determine whether today's moves develop into broader trends or fade as geopolitical tensions ease.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3416 | Bullish bias above 1.3400 |

| EUR/USD | 1.1438 | Positive bias above 1.1400 |

| EUR/GBP | 0.8523 | Consolidating |

| AUD/USD | 0.6936 | Steady |

| NZD/USD | 0.5725 | Bullish post-hike |

| USD/JPY | 162.37 | Bullish / near 40-yr high |

| GBP/JPY | 217.66 | Bullish |

Market Lookahead

Fri, July 10

- Germany’s HICP (Jun) inflation

Speeches from BoE, ECB and Fed members through the week

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.