Oil, Politics, and a CPI Surprise Pull FX Strings

7 min read

Share

Soft US Inflation cools dollar demand. Hormuz tensions lift oil and BoE and ECB hike bets. UK Domestic politics keeps the pound on edge, with Burnham likely to be the PM on 20 July. US PPI data drops today. Cable holds above 1.3400 and the EUR/USD pair testing 1.1430.

GBP: Sterling Standing Tall on a Shaky Floor

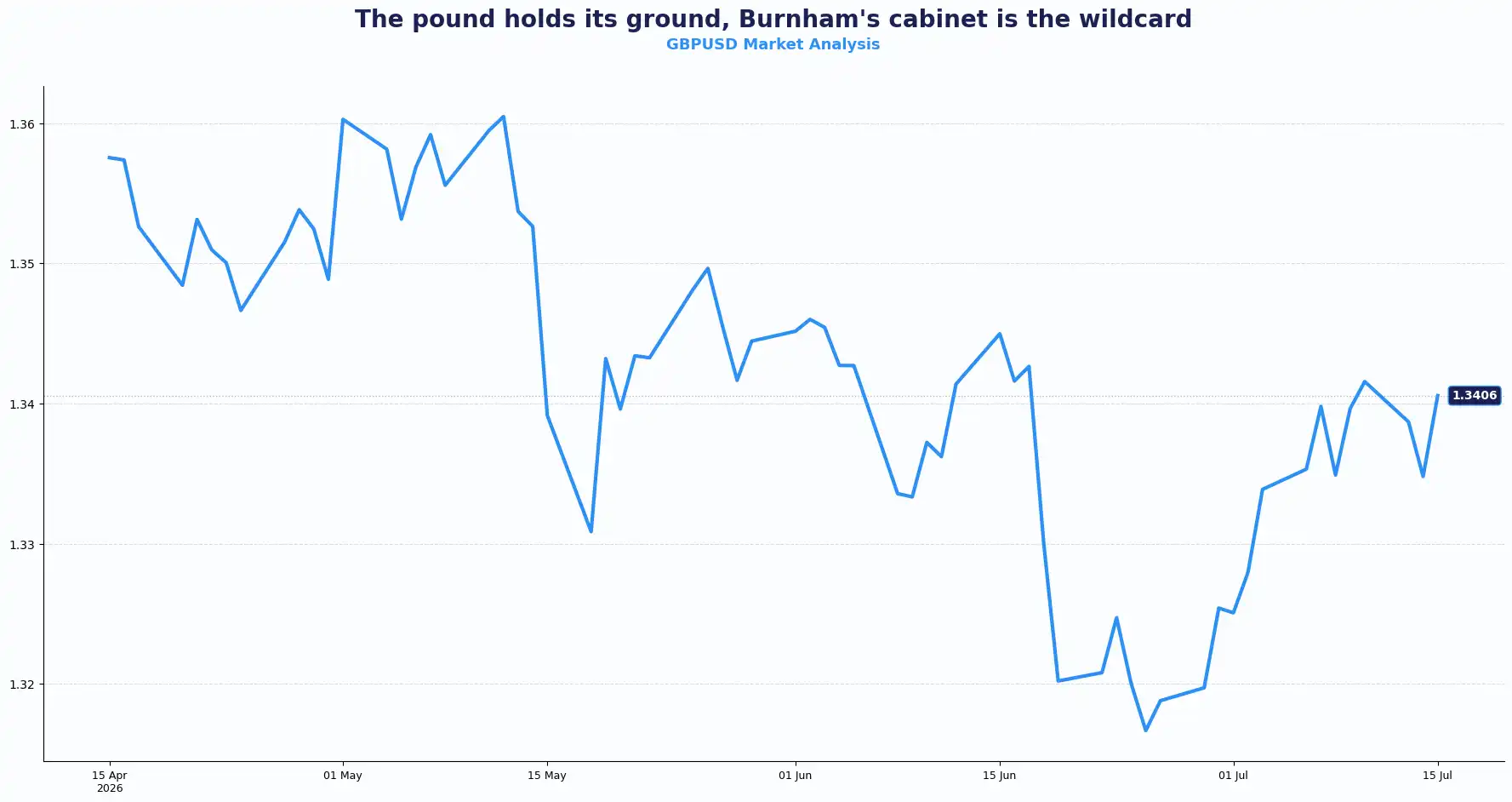

GBPUSD 1.3406

Cable pushed to 1.3414 in early European session on Wednesday, logging a second consecutive session of gains against a soft dollar. GBPUSD holds above 1.34. The immediate catalyst is yesterday's US CPI print: headline inflation slowed to 3.5% YoY in June, down sharply from May's 4.2% and well below the 3.8% consensus. The dollar shed ground across the board.

Energy prices feed directly into UK inflation expectations, and the renewed disruption in the Strait of Hormuz, with the IRGC confirming strikes on US Fifth Fleet facilities in Bahrain overnight, has put oil back on the boil, keeping BoE rate-hike expectations elevated. The market now prices a 25bp hike in September, with a second move before year-end all but locked in. Hawkish BoE pricing is a near-term pillar under the pound. The structural question is whether the UK economy can absorb two hikes without cracking.

Overlaying all of this is a domestic political transition. Andy Burnham is set to enter Downing Street on 20 July. His cabinet picks will matter. Markets have pointed to Ed Miliband for Chancellor, though reports suggest that Burnham's own advisers are divided over whether to make the appointment. Miliband's reputation as fiscally expansive means the gilts market would likely respond to his appointment with some pressure on UK borrowing costs, which could pull the pound in opposite directions. Higher yields are supportive in isolation, but fiscal credibility risk could cap the upside.

The policy landscape across the next two weeks combines a new prime minister, live Hormuz tensions, and today's US PPI release, all of which have the capacity to shift the GBP/USD pair by meaningful amounts in the near term.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3480 and Support sits at 1.3350

EUR: Euro Holds Firm as Inflation Risks Return

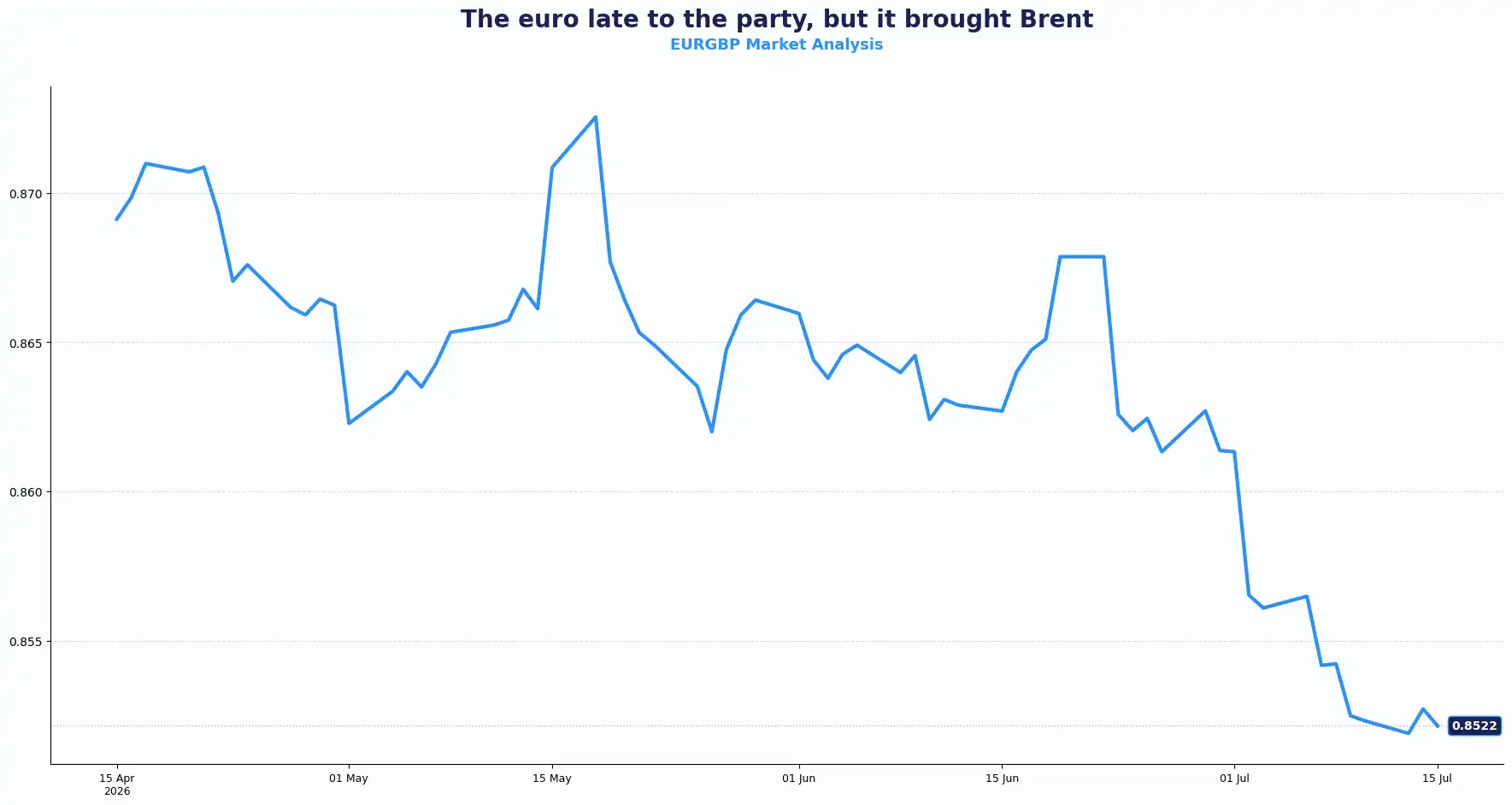

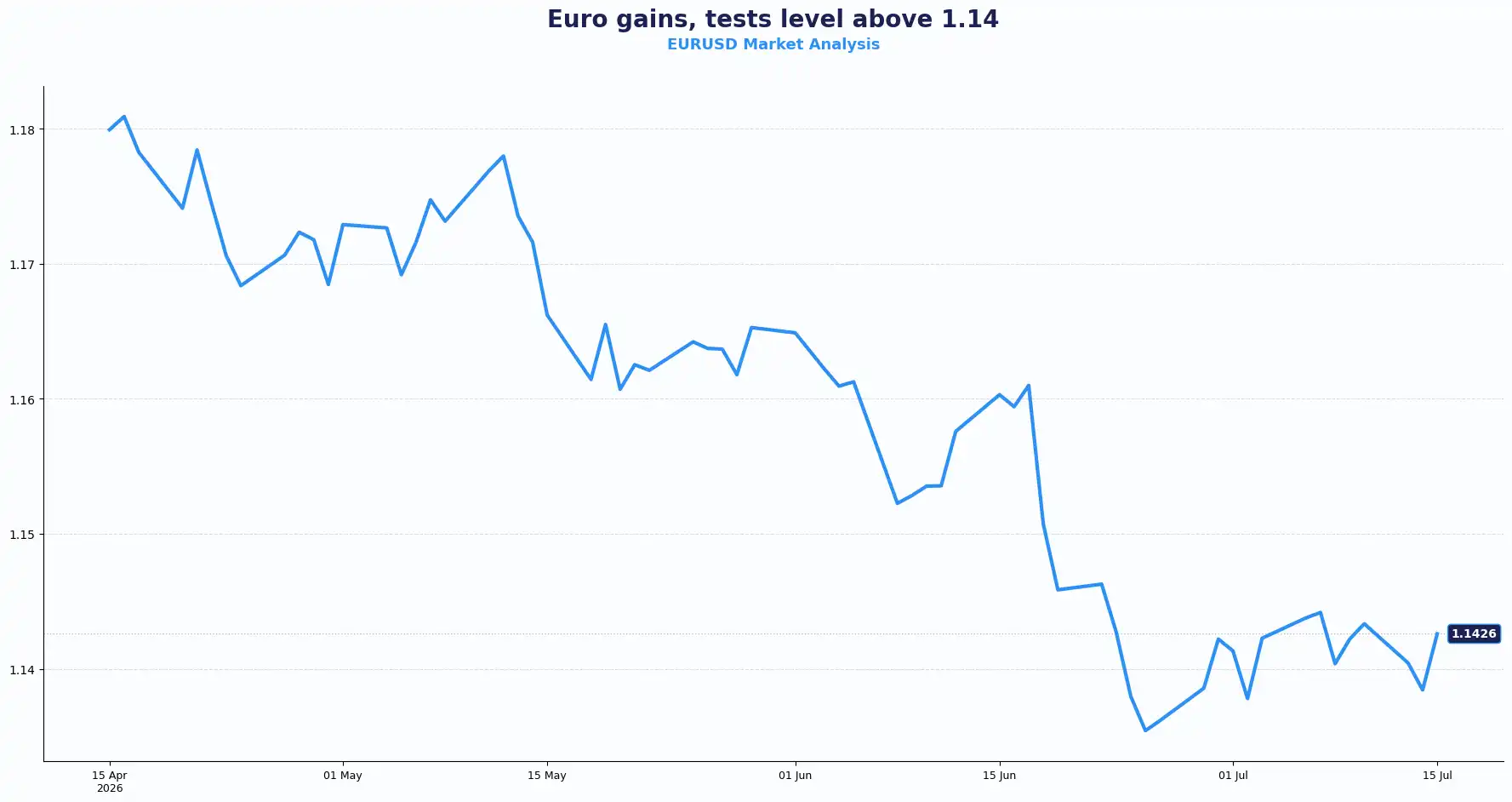

EURGBP 0.8522 | EURUSD 1.1426

EUR/GBP gained ground to around 0.8535 in Wednesday's early European session before trading near 0.8520. The surge in oil costs has reignited Eurozone inflation concerns and pushed traders to advance their ECB rate-hike timeline. Market expectations now reflect a 25bp ECB hike in September, with another before year-end all but certain.

ECB Governing Council member Martin Kocher said on Wednesday that the central bank is prepared to act on monetary policy whenever necessary to hit its 2% medium-term inflation target. That stance is consistent with ECB President Christine Lagarde's emphasis on strict data dependence and with the ECB's June decision meeting minutes, which explicitly noted that the hike was neither a guaranteed sequence nor a guaranteed one-off. Other ECB Council members are due to speak later today, and their remarks on oil pass-through risk could shift EUR pricing at the margin.

The EUR/USD pair also pushed higher, trading around 1.1438 in the early European session before continuing to trade in range between 1.1420 - 1.1435 The euro absorbed the softer dollar environment well, finding support above 1.1400. The pair has notched two straight sessions of gains. That reflects a broad shift in Fed rate expectations following yesterday's CPI. The dollar gave background as traders trimmed hawkish bets, benefiting the euro.

The structural picture for the euro remains complex. The ECB raised rates by 25 bp at its June meeting, marking its first hike since 2023, citing Middle East-driven energy inflation. It simultaneously revised its 2026 headline inflation forecast to 3.0% and trimmed Eurozone GDP growth to 0.8%. The risk is that tighter policy compounds weaker growth. For now, oil-driven hawkishness has the upper hand.

The Euro and Sterling now face many of the same inflation challenges, particularly from higher energy costs. The key difference lies in how quickly each central bank chooses to respond. That policy balance could continue to influence G10 pairs in the sessions ahead.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8560 and Support sits at 0.8490

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1500 and Support sits at 1.1380

USD: A CPI Reprieve, Hormuz Flashpoint, and PPI in the Queue

DXY 100.40

The dollar index trades below 101, steadying at 100.40 on Wednesday morning. Yesterday's June CPI print handed the dollar its biggest single-session setback in weeks; the 3.5% headline figure landed well below forecasts, the monthly read posted its largest decline since April 2020, and core inflation eased to 2.6% YoY. Traders trimmed Fed hike bets promptly.

But the dollar's downside has limits. Geopolitical risk pulls in the opposite direction. Iran's IRGC struck US military facilities in Bahrain overnight, widening the uncertainty that comes with the Hormuz standoff. Brent Crude hit its highest level since mid-June, trading near $85.92 a barrel in early Asian hours, as traffic through the Strait continued to contract sharply. Roughly 130 vessels transited the strait daily before the conflict began; just six were tracked in a single overnight window last Friday. That matters for inflation directly - Hormuz carries around a fifth of global oil and LNG in peacetime. Supply disruption at that scale feeds energy costs globally and keeps the Fed's finger close to the trigger.

Fed Chair Kevin Warsh was clear in his Congressional testimony on Tuesday: the Fed has "no tolerance for persistently elevated inflation." Governor Christopher Waller added that it would take several months of positive readings before he feels confident inflation is returning to target. The message is hawkish in tone even as the data offered temporary relief. CME FedWatch now shows an ~85.6% probability that the Fed holds rates at its late July meeting, a sharp jump from ~58.3% the prior day, with the balance of hike risk concentrated in September and beyond. The pivot risk remains two-sided. Soft inflation cools the dollar; oil-fuelled re-escalation in Iran pushes its demand higher, again. Today's US June PPI release is the next dollar test. Prior, the May PPI came in at 6.5% YoY, the highest since November 2022. A materially softer print could sustain recent dollar softness; a hotter-than-expected reading could revive hawkish bets quickly.

Other Currencies:

USDJPY 162.13 | GBPJPY 217.50 | NZDUSD 0.5820 | AUDUSD 0.6989

The Australian dollar climbed to around $0.699, its highest in over three weeks. Softer the US CPI reduced Fed rate expectations, putting the dollar on the back foot and lifting high-beta currencies. The Reserve Bank of Australia (RBA) has delivered three rate hikes since February, and recent business surveys point to softening operating conditions and easing cost pressures, though July consumer confidence improved. Rising oil prices pose a renewed challenge to that benign domestic picture. The New Zealand dollar also gained, trading around $0.582, tracking the same broad dollar-softness theme.

USD/JPY slipped below 162.00 during the Asian session, with the pair struggling to hold up the prior day's late bounce. A softer dollar pulls the pair lower, but renewed US-Iran tensions partially offset this through safe-haven dollar demand. The persistent gap between US and Japanese policy rates acts as a structural ceiling on yen strength. The pair is likely to remain range-bound at current levels until the Fed's September decision provides clearer direction.

USD/CNY has drifted back toward 6.77, a mild appreciation in the yuan. China's domestic demand picture, soft retail sales and investment, despite strong export growth and sizeable trade surpluses, constrains the case for further material yuan strength. A sharp or rapid appreciation would compress the export competitiveness that Beijing depends on. Markets expect the People's Bank of China to maintain a managed appreciation path rather than allow a significant breakout.

USD/CHF steadied around 0.8090 on Wednesday after registering losses of roughly 0.7% in the prior session. The pattern here is the same: dollar weakness on CPI, partially checked by safe-haven demand from Hormuz tensions. The franc remains supported by its traditional geopolitical bid.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3406 | Bullish |

| EUR/GBP | 0.8522 | Mild bullish bias |

| EUR/USD | 1.1426 | Bullish |

| USD/JPY | 162.13 | Bearish (USD) |

| AUD/USD | 0.6989 | Bullish |

| NZD/USD | 0.5820 | Mild bullish |

| USD/CHF | 0.8090 | Bearish (USD) |

| GBP/JPY | 217.50 | Bullish |

| USD/CNY | 6.7700 | Steady / mild CNY appreciation |

Market Lookahead

Wed, July 15

- US Producer Price Index (PPI) (Jun)

- BoC Interest Rate Decision

Thurs, July 16

- Australia’s Consumer Inflation Expectations (Jul)

- UK Gross Domestic Product (GDP) (May)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.