Hormuz Blockade, Toll Demand and CPI Test the Dollar

8 min read

Share

The Hormuz blockade is live and a 20% toll demand is on the table. Sterling holds above 1.3350 as BoE rate hike bets build ahead of Bailey's speech today. The euro edges higher on a softer dollar but the downside bias is intact. US CPI for June and Fed Chair Warsh's speech are likely to set the dollar's direction today.

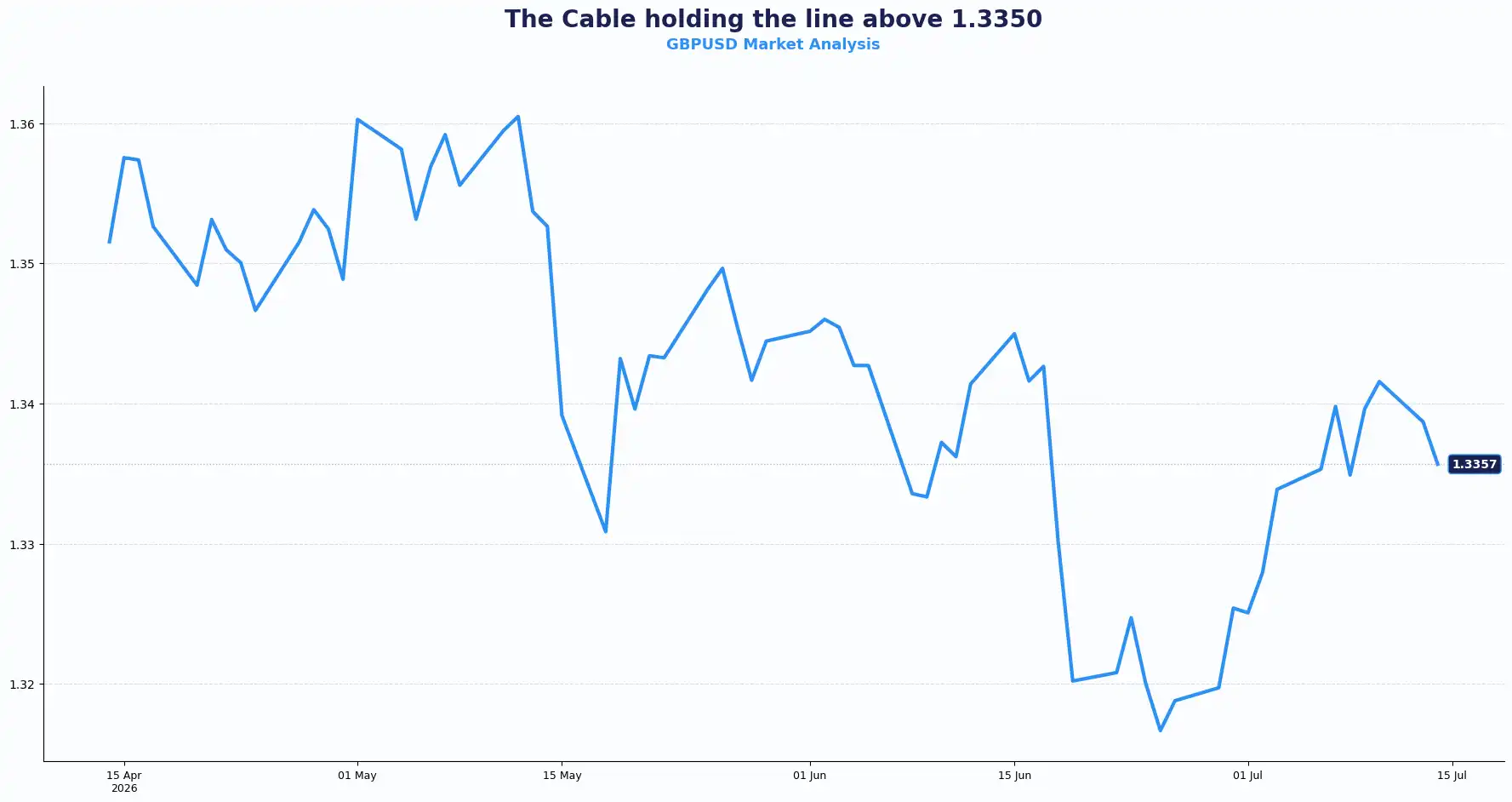

GBP: The Cable Holds Its Ground, but Hormuz Has Other Plans

GBPUSD 1.3357 | EURGBP 0.8530

GBP/USD trades near 1.3357 in the early European session, drawing strength from a softer dollar ahead of today's US CPI print. The pair has found support near 1.3370 with upside momentum building but not yet overextended, per RSI readings around 57.6. The geopolitical backdrop is doing its best to cap the rally.

The US military carried out further strikes on Iran on Monday as Trump simultaneously reinstated the naval blockade of Iranian maritime traffic and announced a demand for a 20% toll on all cargo transiting the Strait of Hormuz. The enforcement mechanism for the toll has not been detailed, and its legal basis is contested; the blockade itself, however, is live and operational. Safe-haven demand for the dollar tends to build in conditions like these, and sterling, however well-supported domestically, cannot fully escape that gravitational pull.

EUR/GBP holds at 0.8525, near its lowest level in around a year. The BoE stance has left the traders guessing. BoE Pill confirmed that interest rates are on course to rise this year to prevent inflation from becoming entrenched. BoE Governor Andrew Bailey speaks today; his commentary on the growth-inflation trade-off could attract close attention. Bailey has already suggested that the BoE must monitor developments in the Middle East and their effect on the UK economy, adjusting policy as required. He has also framed the decision to hold rates as an active policy tightening in itself by taking expected cuts off the table; the committee has already moved in a restrictive direction.

Markets are pricing one BoE quarter-point rate hike and a roughly one-in-three chance of a second one over the remainder of 2026. That hawkish repricing provides sterling with a structural support layer that distinguishes it from peers where central banks are less explicitly on a tightening path.

Thursday's UK data releases will have investors’ attention. GDP for May, Industrial Production, and Manufacturing Production all land on what is shaping up to be a significant domestic data day. Strong output figures would validate the BoE's hawkish tilt and could push sterling rate expectations further.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3470 and Support sits at 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8480 and Support sits at 0.8600

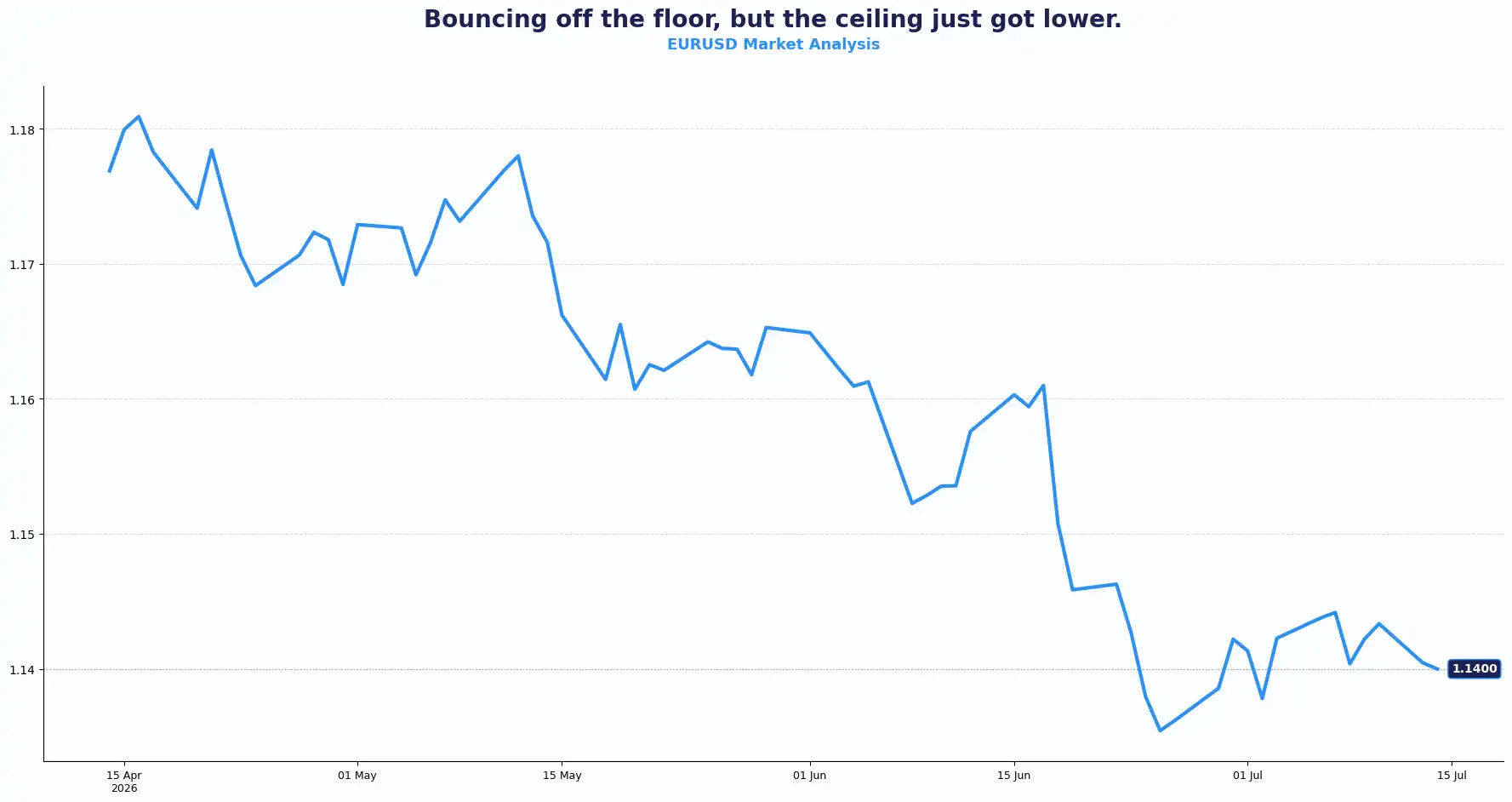

EUR: Euro Tests Critical Supports

EURUSD 1.1400

EUR/USD trades near 1.1387, edging up as the dollar softens ahead of the US CPI print. Oil prices surged following another round of US strikes on Iran, with both sides disputing the status of the Strait of Hormuz. Geopolitical uncertainty has fuelled inflation concerns and prompted traders to price in further ECB rate hikes.

The downside bias on this pair has not dissolved. EUR/USD has tested one-year lows in recent weeks, and the current bounce reads more as a dollar correction than a euro resurgence. Any hawkish surprise from Fed Chair Warsh later today could flip that dynamic.

The ECB's June rate hike, its first since 2023, established the policy direction. The ECB's June Euro system projections put headline inflation at 3.0% in 2026, 2.3% in 2027, and 2.0% in 2028, with the governing council citing pressures from the Middle East war as the primary driver of inflation. Market pricing for a September ECB rate hike sits at around 70% probability, as the latest oil price surge following renewed US-Iran strikes has outweighed the more cautious tone struck by officials at the Sintra forum in early July.

Investors are watching for ECB commentary today. Any signal of urgency about a second hike this year could provide the euro with a firmer foundation. Tomorrow brings eurozone Industrial Production data for May. A strong reading is likely to reinforce the case for sustained ECB tightening. A soft reading might land the Hawks a headache.

The policy divergence question is real. If the ECB delivers a second hike in September while the Fed holds, a plausible scenario is that if today's US core CPI disappoints, EUR/USD could recover ground. If the Fed leans hawkish and the ECB blinks, the euro faces renewed pressure toward the 1.12 region. The pair is off its lows but has not broken its downtrend. Both the ECB path and the Fed's reaction today are likely to redraw the near-term range.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1470 and Support sits at 1.1200

USD: Caught Between Safe-Haven and Its Own Inflation Problem

DXY 101.17

The DXY trades near 101.17, pulling back from Monday's high of 101.33 as the dollar pauses ahead of today's data double. Trump reinstated the Hormuz blockade on Monday and announced a demand for a 20% toll on all non-Iranian cargo transiting the waterway. Secretary of State Rubio previously stated that charging fees in international waters violates international law, and the UN's maritime agency has taken the same position.

Strait of Hormuz crossings dropped by more than half from the prior week. Brent Crude climbed above $83 a barrel following Monday's announcement. A 20% charge, if ultimately enforced, would amount to approximately $32 million for a fully loaded very large crude carrier at current prices, a figure that flows directly into shipping costs, commodity prices, and eventually core inflation. The dollar is being pulled in two directions: safe-haven demand from geopolitical escalation pushes it higher; the inflationary overshoot that eventually undermines growth pulls it lower. Both forces appear active today.

Consensus puts headline CPI easing to around 3.8% year-on-year from 4.2%, with core inflation seen easing to 2.8%. The headline softness is largely mechanical, driven by a June energy price decline of around 10%, and broadly expected to reverse sharply in July data as the ceasefire collapse feeds back into energy costs. Core CPI figures are where the Fed's attention will be. Shelter inflation and services inflation have both stayed sticky, and Fed Chair Warsh flagged AI-driven energy demand as an additional inflationary pressure in the June FOMC minutes.

Warsh testifies before the House Financial Services Committee today, his first full congressional appearance since taking office in May 2026. With the consensus headline CPI near 3.8% year-on-year, analysts note that nearly all the improvement comes from the decline in petrol prices. Without a deceleration in services inflation, getting overall inflation sustainably lower is likely to prove difficult. The CME FedWatch Tool shows approximately 70% odds of a Fed hike by September. Warsh's stance today will shape whether that conviction holds or gets walked back. A softer-than-expected core CPI, paired with cautious commentary from Warsh, would likely pressure the dollar lower. A hotter print or hawkish tone from Warsh would push the DXY back toward 101.50 and above.

Tomorrow brings US PPI data; the producer price read could offer a forward signal on whether pipeline inflation from the Hormuz disruption is already feeding through.

Other Currencies

USDJPY 162.32 | GBPJPY 216.81 | NZDUSD 0.5786 | AUDUSD 0.6931

USD/JPY trades at 162.32. GBP/JPY holds at 216.81. Economic risks from the Middle East conflict and the wide rate gap continue to undermine the yen, meaning that even as geopolitical risk builds, the yen does not behave as the clean safe-haven play it once was. A hawkish Warsh outcome or a hot CPI print today would widen that rate differential further and likely keep USD/JPY elevated.

AUD/USD softens to near 0.6931 after an early dip toward 0.6915. The Australian dollar faces selling pressure as geopolitical risk sentiment weighs, though China's June trade balance, a surplus that widened due to strong export performance, provides some underlying support given Australia's commodity export dependency on Chinese demand.

On the domestic front, market consensus signals that further RBA rate increases are on the table. The RBA has delivered three 25-basis-point hikes so far this year, lifting the Official Cash Rate to 4.35%. Futures currently price approximately a 16% probability of a move to 4.60% at the August meeting. That is not a strong conviction bet, but it keeps the Australian dollar supported on dips, provided risk sentiment does not deteriorate sharply.

NZD/USD trades near 0.5786, pushing toward the 0.5810–0.5820 confluence zone after RBNZ Chief Economist Paul Conway struck a hawkish tone in recent commentary. The kiwi's four-week high reflects a combination of fresh rate-hike expectations and a pausing dollar ahead of today's US data. A clean break above 0.5820 opens the next leg higher. A hot US CPI print today could close that door.

USD/IDR pulls back to near 18,140 after gains in the prior session. S&P's affirmation of Indonesia's stable BBB credit rating boosted domestic equity sentiment, drawing capital back into IDR-denominated assets. The rupiah's recovery sits within a broader emerging market context: when the dollar pauses, rating stability can do meaningful work. A hawkish US CPI outcome could quickly reverse that logic.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3357 | Bullish bias |

| EUR/USD | 1.1400 | Neutral / bearish bias |

| EUR/GBP | 0.8530 | Sterling outperforming |

| DXY | 101.17 | Consolidating |

| USD/JPY | 162.32 | Elevated / range-bound |

| GBP/JPY | 216.81 | Elevated |

| AUD/USD | 0.6931 | Soft / neutral |

| NZD/USD | 0.5786 | Recovering |

| USD/IDR | 18,140 | Pulling back |

Market Lookahead

Tue, July 14

- US Consumer Price Index (CPI) (Jun)

Wed, July 15

- US Producer Price Index (PPI) (Jun)

- BoC Interest Rate Decision

Thurs, July 16

- Australia’s Consumer Inflation Expectations (Jul)

- UK Gross Domestic Product (GDP) (May)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.