Strikes and Bargains: The Gulf Paradox Stalling the Pound

7 min read

Share

Sterling steadies as Gulf strikes and Trump's deal talk pull in opposite directions. The BoE stays cautious, the ECB eyes a June hike, and the dollar draws quiet strength from the geopolitical uncertainty in between.

GBP: Sterling Stalls as Bailey Preaches Patience

GBPUSD 1.3469 | EURGBP 0.8656

Sterling traded near 1.3460 during Monday's European session, holding close to recent highs despite renewed geopolitical tensions in the Middle East. The GBP/USD pair stayed confined to the mid-1.3400s while the EUR/GBP pair drifted lower towards 0.8650.

The pound faces pressure from two directions. The Bank of England (BoE) kept rates on hold at its last meeting and is widely expected to repeat that in June. Governor Andrew Bailey signalled on Friday that the Bank is in no rush to raise rates. With the outcome of the Iran conflict still unclear and UK growth staying weak, the BoE is watching and waiting. Bailey's message was explicit: "We have to monitor the situation in the Middle East and how it affects the UK economy and inflation very closely."

The latest developments between the United States and Iran injected fresh caution into currency trading. Reports of US strikes on Iranian targets and retaliatory attacks near the Strait of Hormuz lifted oil prices and revived demand for the dollar as a defensive asset. Brent Crude moved back above $90 per barrel while WTI climbed towards $89.

Before the conflict, two rate cuts in 2026 from the BoE looked probable as inflation eased towards the target. In late February, the energy shock from the Iran war reversed that expectation. Markets now price 32 bps of tightening by year-end, a one-quarter-point hike, and roughly a 30% chance of a second. That is a significant shift, but it has done little for sterling because the BoE itself refuses to confirm the path.

UK inflation came in softer than forecast. The Unemployment Rate unexpectedly climbed to 5.0% in April. Bailey acknowledged that tolerating above-target inflation temporarily in a weak economy is appropriate, but drew a firm line: if second-round effects emerge, that tolerance goes. The BoE effectively tightened relative to prior market expectations simply by removing rate cuts from the table, and mortgage rates have risen since the start of the Iran conflict.

Bailey's comments included a notable observation: UK banks do not currently have access to Mythos, a reference to the frontier AI model. A 60-day ceasefire in Iran would "still create uncertainty." The message is consistent, the Bank moves when the data warrants, and right now the data does not.

The EUR/GBP pair trades soft near 0.8650, with the BoE's hawkish repricing giving sterling a marginal edge over the euro despite both central banks sitting on their hands.

The UK’s S&P Global manufacturing PMI figures for the month of May will also be released today.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3500, 1.3560, 1.3650 and Support sits at 1.3400, 1.3340, 1.3280

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680, 0.8720, 0.8760 Support sits at 0.8620, 0.8580, 0.8540

EUR: Euro Waits for Inflation Test

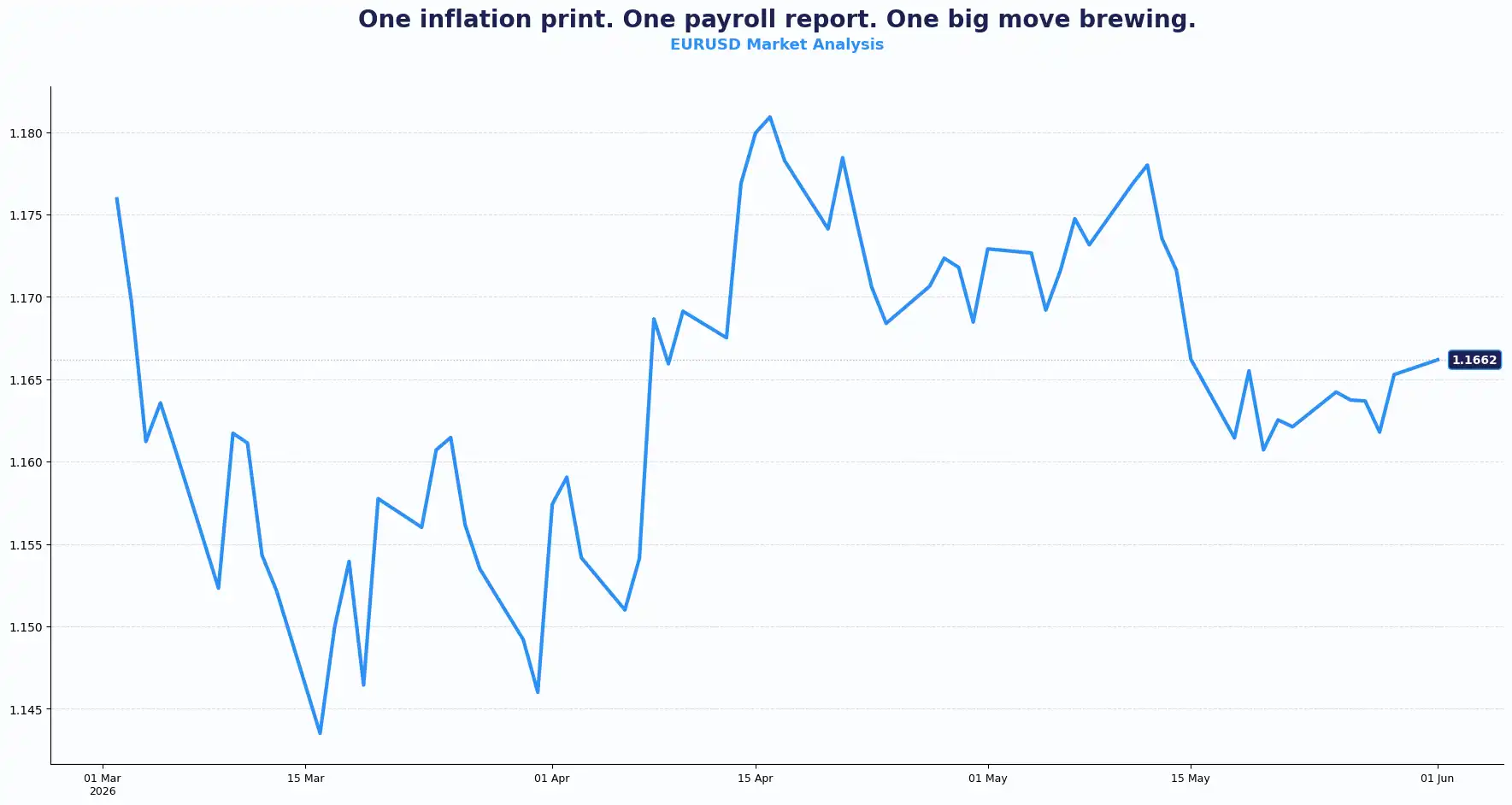

EURUSD 1.1662

The EUR/USD pair edged down to 1.1645 in earlier sessions as the dollar ticked higher, before trading around 1.1660’s in the early European session. The pair spent the entire past week between 1.1585 and 1.1661, and the week ahead provides the catalysts to break or confirm that range. Investors now await Eurozone inflation data and Friday's US Non-Farm Payrolls report.

Flash Eurozone HICP data for May drops on Tuesday. Preliminary readings from France, Italy, and Spain showed inflation rising; Germany saw a modest slowdown. All four printed above the European Central Bank (ECB)'s 2% target. Recent ECB meeting minutes revealed that some members favoured a rate hike as early as April. A June increase of 25 bps at the 11 June meeting now represents the consensus in money markets.

The structural case for the euro is building. The ECB's inflation problem is embedded in the data across the bloc's major economies, rather than a transitory narrative. An ECB hike next week, combined with a softer-than-expected US NFP reading on Friday, could sharpen the divergence between Frankfurt and Washington, influencing the direction of the EUR/USD pair.

The wild card, as with most currencies this week, is oil. With Brent Crude trading around $93 per barrel, a durable reopening of the Strait of Hormuz compresses energy inflation for the bloc and softens the case for rate urgency. Without a deal, energy price pressure could persist, and the ECB is likely to face a harder trade-off.

The ECB appears closer to another rate increase than many of its major peers. Until one side gains a clear advantage, the EUR/USD pair may continue to rotate around the 1.1600-1.1700 range.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1670, 1.1720, 1.1800 and Support sits at 1.1600, 1.1550, 1.1500

USD: Safe-Haven Bids Intensify

DXY 99.05

The US Dollar Index (DXY) gathers momentum above 99.05, capitalising on escalating friction in the Gulf and conflicting messages regarding a potential Washington-Tehran truce.

Geopolitics and institutional stability dominate the Greenback’s narrative. While President Donald Trump suggests Iran desires a diplomatic resolution, real-world events tell a far more assertive story. US Central Command launched strikes over the weekend following attacks on a US airbase in Kuwait. Iran's IRGC confirmed it targeted a US airbase in Kuwait used to launch an attack on Sirik Island in the Strait of Hormuz. Washington continues to push for Iran to surrender highly enriched uranium and seeks further amendments to the Hormuz framework. Defence Secretary Pete Hegseth confirmed the US stands ready to resume full military operations if negotiations collapse.

This physical instability coincides with an institutional standoff. Markets currently price a 41.2% probability of a 25bps Fed rate hike by year's end. Former Fed Chair Jerome Powell, speaking over the weekend, warned that political interference in the Fed's leadership would permanently damage the institution's credibility. His remarks came as the Supreme Court deliberates the case of Fed Governor Lisa Cook, whom President Trump sought to remove over allegations of mortgage fraud that Cook denies. The Fed's credibility, Powell said, has taken decades to build, and it functions as a public asset.

Friday's payrolls report is another important catalyst for the dollar's direction this week.

Consensus forecasts point to roughly 85,000-96,000 new jobs and an unemployment rate holding at 4.3%. A stronger outcome would reinforce expectations that the Fed can maintain a restrictive policy stance.

The dollar's direction depends on two variables.

First, developments in the Middle East. Second, incoming US economic data.

Strong payroll data, combined with elevated oil prices, could strengthen the case for higher US rates and could further support the dollar.

Yen, Aussie and Kiwi Watch Global Growth

AUDUSD 0.7187 | NZDUSD 0.5970 | USDJPY 159.47 | GBPJPY 214.70

The Aussie dollar pivots flatly around 0.7100, while the Japanese yen struggles underneath the critical 160.00 psychological barrier, prompting acute intervention awareness.

A profound split characterises the broader Asian session. Equity benchmarks, including South Korea’s Kospi, scaled to historic highs amid insatiable global demand for artificial intelligence (AI) infrastructure.

This equity optimism persists despite slowing Chinese factory activity, which is bearing the weight of elevated global input costs stemming from the Strait of Hormuz disruption.

For the Aussie dollar, local macroeconomic data, specifically upcoming GDP and trade balance releases, could confirm whether domestic momentum supports the 70% probability that investors place on a final RBA rate hike to 4.6% this year.

Resource-linked and import-dependent currencies respond with extreme sensitivity to supply-chain friction. Commodity currencies continue to balance global growth optimism against geopolitical uncertainty. For the yen, the 160.00 level remains the line that traders are watching most closely.

Current Rate Table:

| Pair | Level | Trend |

|---|---|---|

| GBP/USD | 1.3469 | Neutral to bullish |

| EUR/GBP | 0.8656 | Bearish |

| EUR/USD | 1.1662 | Neutral |

| USD/JPY | 159.47 | Bullish |

| GBP/JPY | 214.70 | Bullish |

| AUD/USD | 0.7187 | Neutral to bullish |

| NZD/USD | 0.5970 | Neutral |

Market Lookahead

Mon, June 1

- Germany Retail Sales

- Eurozone Unemployment Rate

- Global Manufacturing PMI releases across EU, US, UK, Canada

Tues, June 2

- Eurozone HICP (May)

- US JOLTS job openings (monthly)

Wed, June 3

- Global Composite and Services PMI releases across EU, US, UK

- Eurozone Producer Price Index (May)

- Australia’s Q1 GDP

- GBP BoE monetary policy hearings

Thurs, June 4

- Eurozone retail sales

- US Initial jobless claims

- Australia’s Trade balance

Fri, June 5

- US Unemployment rate (Apr)

- US Average hourly earnings (Apr)

- US Nonfarm payrolls (Apr)

- BoE governor bailey speech

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.