Gulf strikes resume. Dovish bets retreat.

7 min read

Share

US-Iran peace talks stall as fresh Gulf strikes hit the wires. Strait reopening hopes fade. Sterling holds as BoE hawks push for hikes. Eurozone inflation rose to 3.2% in May, the ECB keeps its June tightening plans. US job openings blew past forecasts. The Fed's rate cut window closes further.

GBP: Sterling Steadies as BoE Turns More Hawkish

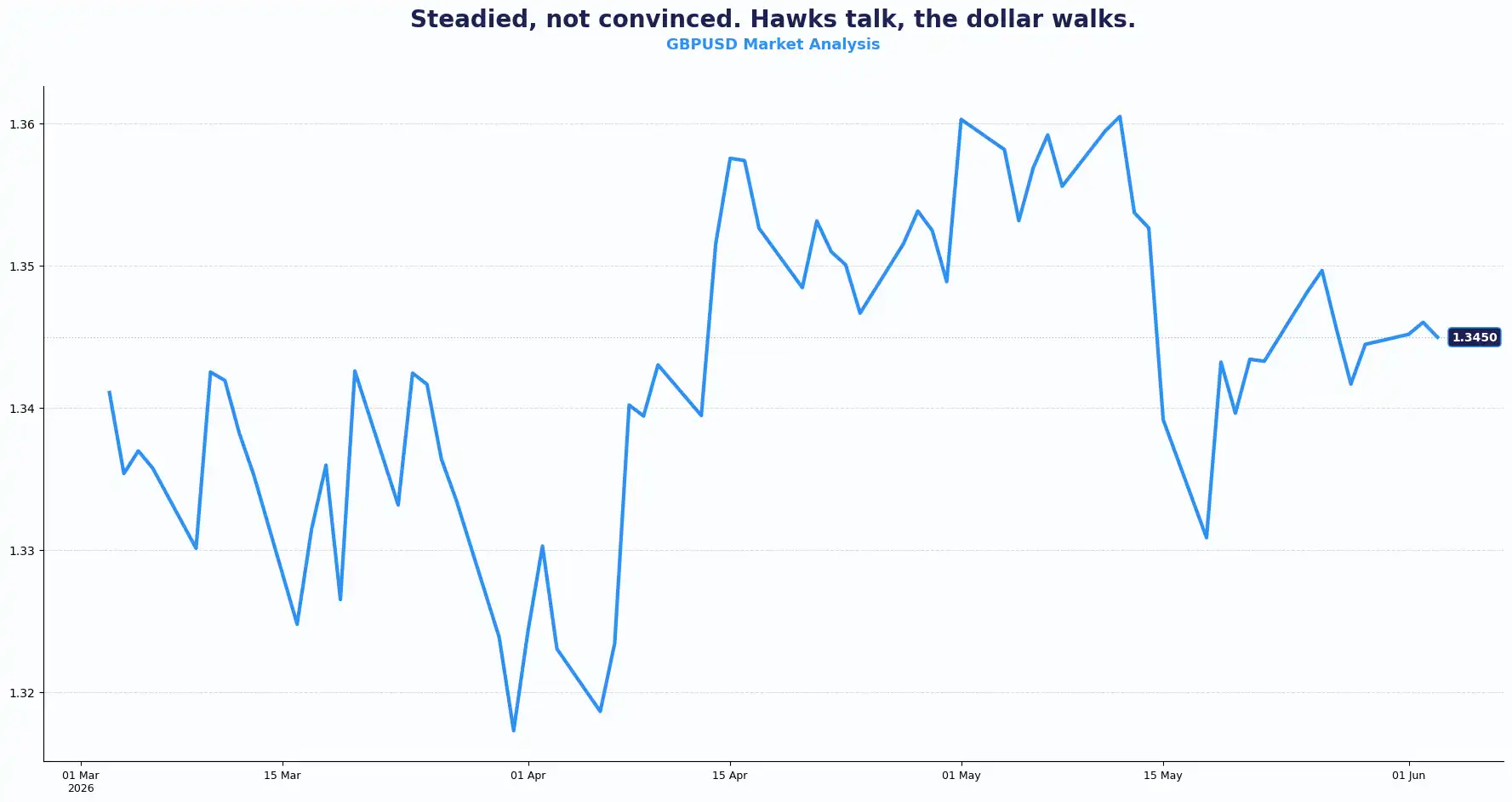

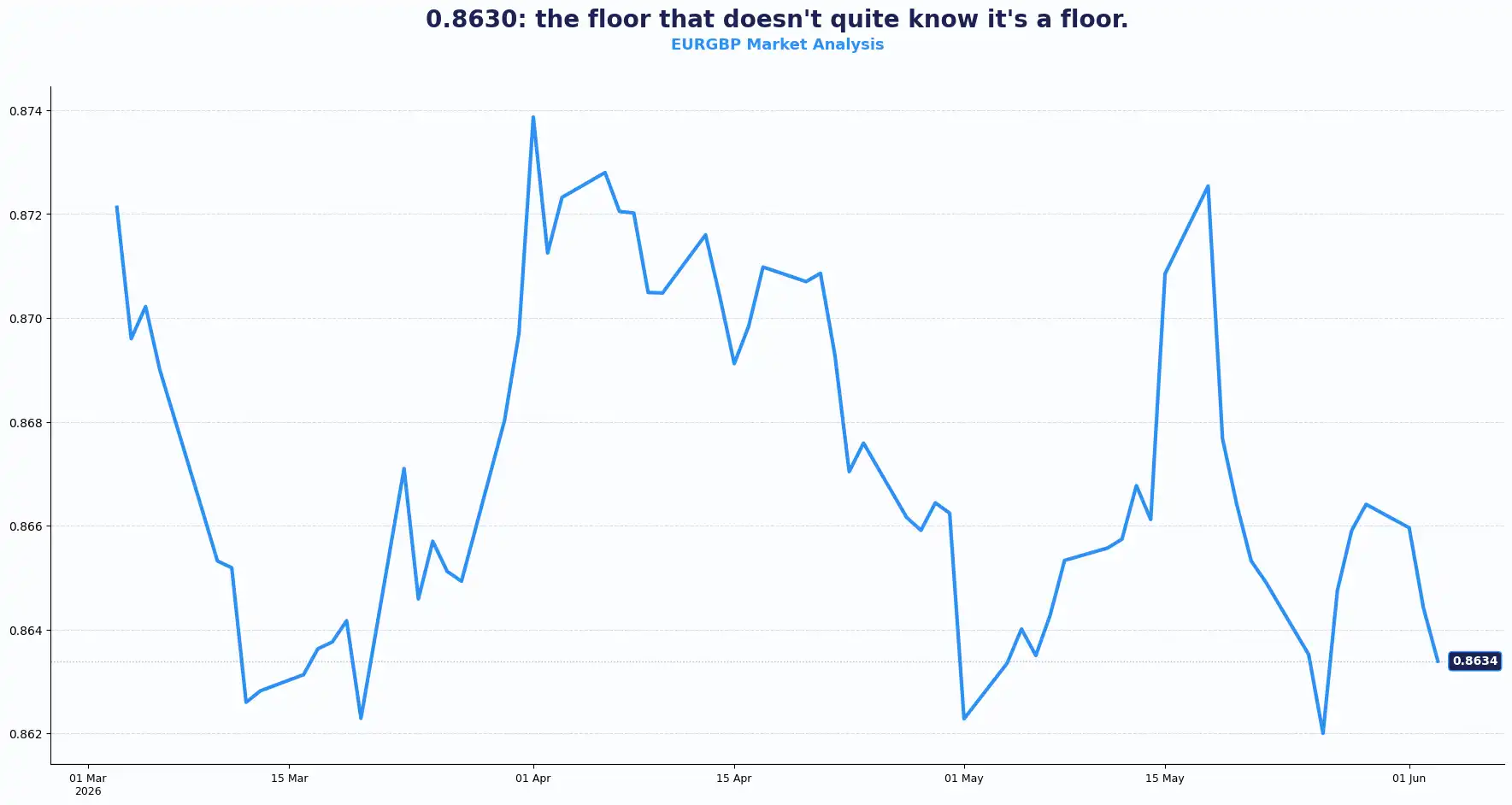

GBPUSD 1.3450 | EURGBP 0.8634

Sterling traded in a tight range on Wednesday, with the GBP/USD pair hovering near 1.3455 while the EUR/GBP pair held around 0.8640. Safe-haven demand for the dollar, driven by stalled US-Iran peace talks and renewed Gulf strikes, offset the pound's otherwise supportive backdrop. However, hawkish comments from Bank of England (BoE) officials helped sterling outperform the euro.

BoE external MPC member Megan Greene set the hawkish tone, arguing that the case for interest rate hikes strengthens as the Iran conflict persists and that acting sooner rather than later matters as much as the size of the move. "A stitch in time saves nine," she told her audience at the University, applying the old adage directly to monetary policy. She went further, that the risk of acting is less severe than the risk of failing to act. She also pointed to consumers' heightened sensitivity to inflation after successive supply shocks.

Governor Andrew Bailey struck a parallel note: “Rate cuts”, he said, “are off the table”. The BoE has already tightened in response to a world that had priced in cuts before the conflict. He sees slower growth, not recession, and flags this as highly uncertain. He argued that waiting for second-round inflation effects to appear would leave policymakers behind the curve.

GBP/USD slipped modestly despite growing expectations that UK rates could stay higher for longer. Key Technical levels for the GBP/USD pair: Resistance sits at 1.3500, 1.3575 and Support sits at 1.3400, 1.3350

Meanwhile, EUR/GBP stayed under pressure as traders weighed fresh inflation risks against weak eurozone growth. The EUR/GBP pair pulled back from last Friday's high of 0.8681. Risk-off sentiment and elevated oil prices weighed on the euro side of the cross. Hot eurozone inflation data on Tuesday provided little support. A break below 0.8630 puts the 2026 lows at 0.8610-0.8615 in view.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680, 0.8720 Support sits at 0.8610, 0.8580

The latest rhetoric suggests policymakers see inflation risks outweighing growth concerns for now. Wednesday brings HCOB composite and services PMI figures for May alongside the BoE Monetary Policy Report. Investors will also watch Bailey's appearances over the next two days for further clues on the central bank's policy path through the second half of the year.

EUR: Tightening Bets Hold Firm Despite Diplomatic Uncertainty

EURUSD 1.1614

The euro edged lower against the dollar, trading near 1.1620 after failing to build on gains from stronger inflation data earlier in the week. The EUR/GBP pair also struggled to recover after retreating from highs above 0.8680 reached last Friday. Higher energy prices and rising geopolitical risks weighed on sentiment across Europe.

The euro softened as Middle East tensions pushed traders towards the dollar. US Central Command (CENTCOM) confirmed it intercepted Iranian missile and drone strikes targeting Kuwait and Bahrain and conducted self-defence strikes on Iran's Qeshm Island in response, darkening the diplomatic backdrop.

ECB policymaker Pierre Wunsch signalled that even a confirmed US-Iran peace agreement before next week's meeting would not automatically change the outlook for higher rates. He was direct about it: Even a confirmed US-Iran peace deal before the June meeting would not derail the case for tightening, he said, because credibility takes time. "If a peace deal is confirmed just before the meeting, it will be part of the discussion. But we won't know whether it will last or be credible".

Fellow ECB member Gediminas Simkus reinforced the message: inflation expectations now mirror levels seen four years ago. A timely response is critical to prevent further price pressures from cementing.

Eurozone inflation accelerated to 3.2% YoY in May, up from 3.0% previously. Energy and services costs drove the increase and strengthened the case for tighter European Central Bank (ECB) policy. The Strait of Hormuz closure feeds directly into that picture, with higher energy prices lifting European import costs and complicating the ECB's inflation outlook.

Today's German, Eurozone Composite and Services PMI releases should provide a clearer picture of business activity heading into summer. Investors will also monitor Eurozone Producer Price Index data for further evidence of pipeline inflation pressures.

Tomorrow's Eurozone retail sales figures could offer another test of consumer resilience. Both sets carry weight for the near-term EUR direction.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1650, 1.1700 and Support sits at 1.1575, 1.1500

USD: Dollar Holds, Labour Data Surprises, Gulf Tensions Flare

DXY 99.30

The dollar stayed firm on Wednesday, with the Dollar Index (DXY) trading around 99.30 after posting modest gains overnight. Stronger-than-expected US labour data and renewed geopolitical uncertainty helped underpin demand for the Greenback.

US job openings rose sharply in April. JOLTS data showed vacancies increased to 7.618 million, well above the 6.88 million forecast and up 10.6% from the revised March figure. It is the largest monthly gain in five years. The labour market has strengthened after a soft patch in 2025. Combined with sticky inflation, markets now expect the Federal Reserve (Fed) to begin a rate-tightening cycle in December 2026, pricing roughly 18 bps of Fed hikes by year's end.

The geopolitical overhang remains a live driver. A resumption of Middle East hostilities reinforces the case for a stronger dollar. Higher oil prices push global inflation up. That pushes central banks to hold rates higher for longer. The dollar benefits from all three channels.

The WSJ also reported that Fed Chair nominee Kevin Warsh has chosen two interim policy advisers, one of whom, Paul Winfree, authored the 'Project 2025' chapter on the Fed, recommending the institution drop its employment mandate. The appointment adds a layer of institutional uncertainty to an already complex Fed outlook.

Traders now await ADP private payrolls and ISM Services PMI, which are due later today. Initial jobless claims and the four-week average figures are due tomorrow, and Non-Farm payrolls (NFP) for May arrive on Friday. The sequence amounts to a near-complete read of the US labour market in 72 hours.

The labour market has become one of the most important drivers of Fed expectations. Strong employment data could reinforce the view that policymakers have little urgency to ease financial conditions.

Markets currently price only limited policy tightening expectations through year-end, leaving room for repricing if labour and inflation data continue to surprise to the upside.

Yen at the Brink, Antipodeans Under Pressure

AUDUSD 0.7163 | NZDUSD 0.5908 | USDJPY 159.90 | GBPJPY 215.12

The USD/JPY pair drifted to 159.90, near the 160 intervention level. The Gulf escalation gave dollar bulls fresh impetus. Higher crude oil prices act as a structural tailwind for the pair. Japan's oil-import dependency ties the yen's fortunes directly to energy prices. Japanese Finance Minister Satsuki Katayama confirmed authorities stand ready to act. The 160-161 range is the zone traders are watching. It is not a precise line, but it functions as one.

The Aussie dollar trading near 0.7163. The Kiwi dollar dropped to 0.5908. Both antipodean currencies found limited shelter in Chinese data. China's services PMI expanded at its fastest pace in three months, which would ordinarily lend support to the commodity-linked Kiwi and Aussie dollar. In this environment, though, it was not enough. Risk-off conditions and a firmer dollar dominated the session. Any signs of weakness in the US labour market later this week could ease pressure on both pairs.

Current Rate Table:

| Pair | Level | Trend |

|---|---|---|

| GBP/USD | 1.3450 | Bullish |

| EUR/GBP | 0.8634 | Bearish |

| EUR/USD | 1.1614 | Bullish |

| USD/JPY | 159.90 | Bullish |

| GBP/JPY | 215.12 | Bullish |

| AUD/USD | 0.7163 | Neutral-Bearish |

| NZD/USD | 0.5908 | Bearish |

Market Lookahead

Wed, June 3

- Global Composite and Services PMI releases across EU, US, UK

- Eurozone Producer Price Index (May)

- Australia’s Q1 GDP

- GBP BoE monetary policy hearings

Thurs, June 4

- Eurozone retail sales

- US Initial jobless claims

- Australia’s Trade balance

Fri, June 5

- US Unemployment rate (Apr)

- US Average hourly earnings (Apr)

- US Nonfarm payrolls (Apr)

- BoE governor bailey speech

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.