Gulf Fog Thickens as Hormuz Deal Keeps FX in Limbo

9 min read

Share

Israel and Lebanon agreed to a ceasefire. Trump says a resolution is closer. Tehran says no progress on the peace deal. The Strait stays shut and the fog over the Gulf is thicker than ever. The ECB meets next week and is expected to hike. Policy divergence is moving EUR/GBP. The dollar sits firm as war-driven inflation pushes Fed hike bets to 85%. US payrolls land tomorrow.

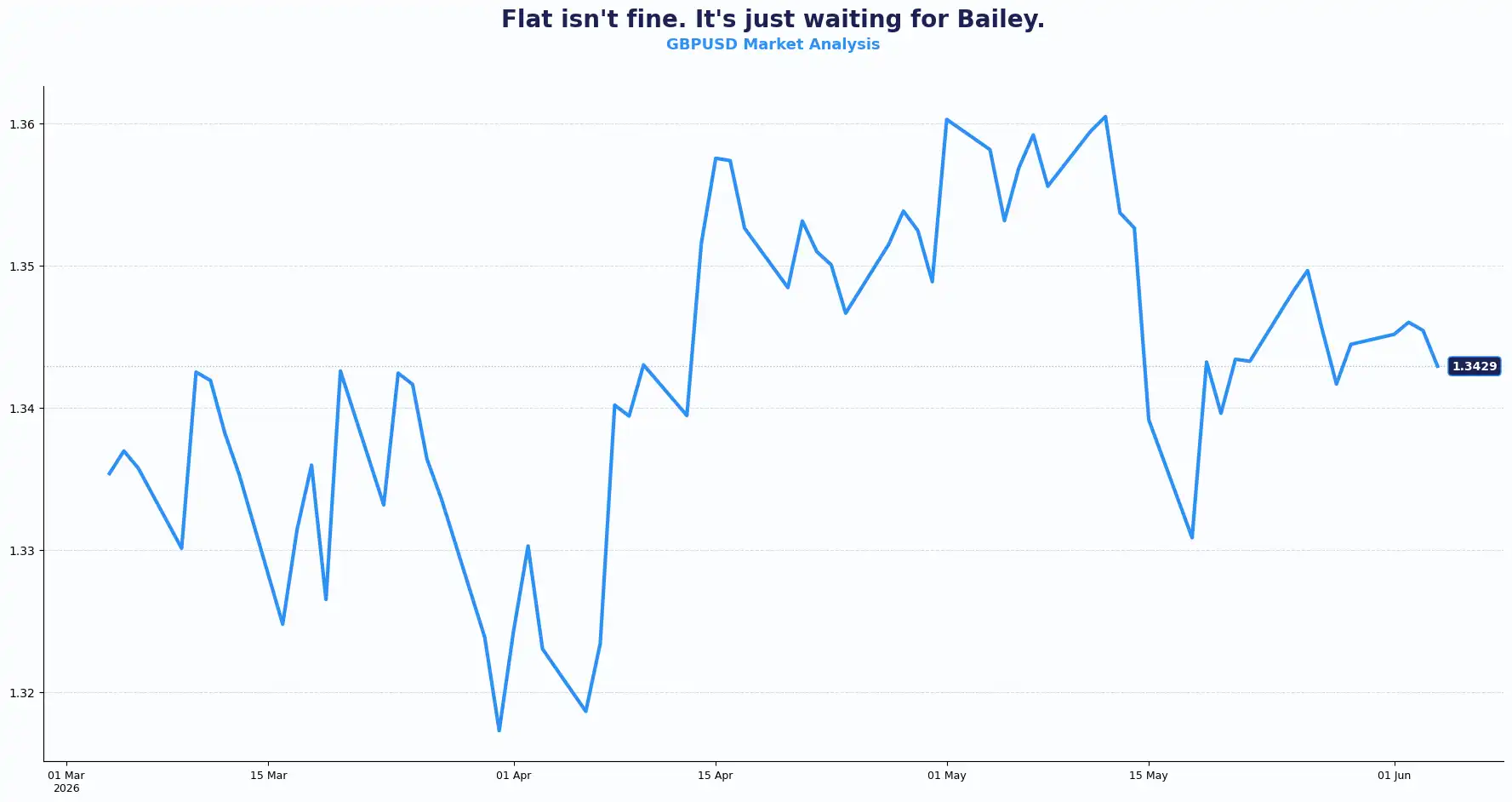

GBP: Sterling Holds Its Ground with Thin Conviction

GBPUSD 1.3429 | EURGBP 0.8643

Cable traded around 1.3430 on Thursday, while the EUR/GBP pair hovered near 0.8650. Sterling edged higher during Asian trading as the dollar eased from recent highs, though gains stayed limited.

The Middle East continues to dominate sentiment. Ongoing disruption around the Strait of Hormuz keeps energy prices elevated and injects uncertainty into global growth and inflation expectations. Iranian attacks on Kuwait damaged the country's airport and injured dozens. US forces carried out strikes near the Strait. A fragile ceasefire held in name. Hope for a diplomatic resolution faded further.

For the UK, that matters more than for many peers. Britain imports a significant share of its energy needs, more than the United States does, making it more sensitive to prolonged fuel price shocks. Price action reflects that uncertainty. Oil prices have pulled back from their late April peaks, but they have not returned to pre-war levels. The US-Israeli campaign against Iran began on 28 February, and energy costs have not normalised since.

This energy vulnerability directly alters the Bank of England (BoE) policy trajectory. Investors have pushed back expectations for a quarter-point rate hike at the September meeting, with fewer than two hikes priced for the remainder of the year. Traders have avoided aggressive positioning ahead of fresh comments from BoE Governor Andrew Bailey in the next 48 hours, and Friday's US non-farm payrolls report.

The pound now sits between two competing forces.

Higher energy prices create inflation risks and could justify a tighter policy stance. At the same time, weaker growth prospects argue for patience from the BoE. Recent comments from Bailey suggest policymakers are in no rush to tighten further. The BoE continues to stress that the inflation outlook depends heavily on how long the energy shock lasts. If next domestic inflation prints without upside surprises, the monetary pause could widen the interest rate differential against more aggressive central banks, fundamentally capping sterling upside.

It is almost as if the market has given the BoE a window to wait this out, as long as the Strait opens pretty soon. A diplomatic breakthrough, even a partial one, could ease pressure on the public finances and provide a relief bid, supporting the pound.

Meanwhile, the European Central Bank (ECB) looks increasingly likely to deliver a June rate hike. That narrows the policy gap between the UK and the eurozone and limits sterling's advantage against the euro.

For now, sterling trades more on external developments than domestic data. Further escalation would likely keep investors cautious. Today's focus shifts to Bailey's remarks. Traders will watch closely for any change in tone on inflation risks and the policy outlook.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3500, 1.3550 and Support sits at 1.3370, 1.3300

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680, 0.8720 Support sits at 0.8600, 0.8560

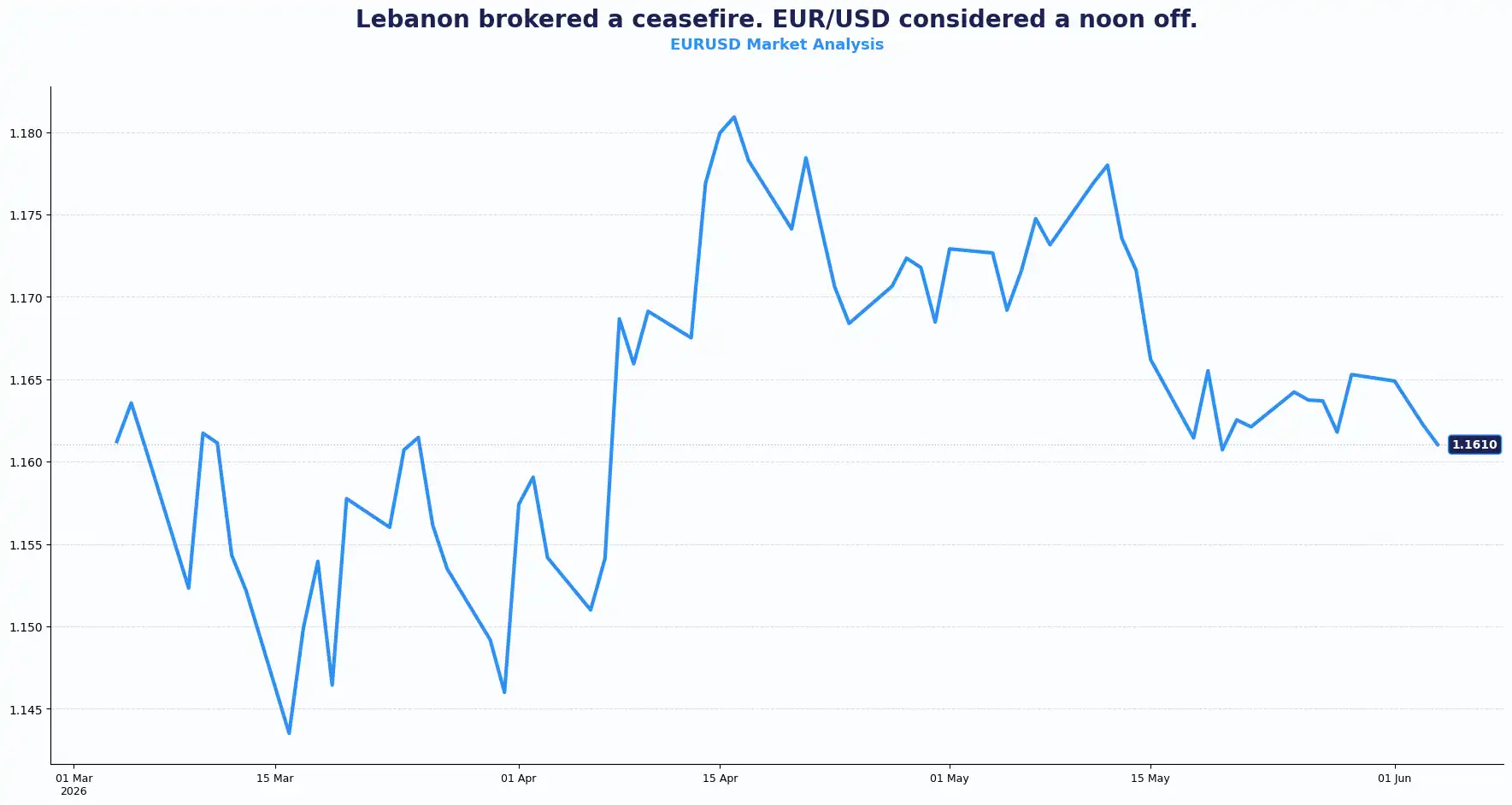

EUR: Lebanon Deal and ECB Hike Bets Keeps Euro Supported

EURUSD 1.1610

The EUR/USD pair traded near 1.1606, bouncing off its weekly low. A ceasefire between Israel and Lebanon, brokered through Washington negotiations, provided the immediate lift. The agreement reduced the perceived probability of a broader regional escalation, which took the edge off the dollar's safe-haven bid, and the euro recovered.

The single currency also found support from growing confidence that the ECB is likely to raise rates at its upcoming June meeting. Markets have largely priced in this move; expectations for further tightening later in the year continue to support the euro.

In contrast, ongoing geopolitical risks continue to support broader demand for the dollar, preventing the EUR/USD pair from establishing a stronger upward trend.

The ECB faces a difficult balancing act. Inflation remains above target and energy prices continue to add pressure. Growth, however, has slowed across much of the eurozone. Policymakers appear willing to tolerate weaker growth if it helps prevent inflation expectations from becoming entrenched.

That policy stance contrasts with the BoE's more cautious approach. The challenge for euro bulls is that much of the June hike story already sits in current market pricing. Future gains may depend more on guidance from ECB President Christine Lagarde than on the rate decision itself.

Lagarde is expected to preserve optionality on the forward path, including the possibility of a further hike over the summer. Limited new data will be available by the July meeting, making a firm assessment of second-round inflationary effects difficult. The analytical consensus is that a single hike does not materially alter economic conditions on its own; a second move in Q3 is what many expect the ECB to deliver. That trajectory holds the EUR/USD pair's downside relatively well contained, as long as the Iran situation does not deteriorate sharply enough to send the dollar surging again.

Friday's US Non-Farm Payrolls (NFP) report acts as the immediate swing factor for the pair. A strong read could reinforce the Fed hiking narrative, lifting the dollar, and capping EUR/USD. A soft read opens the pair to the upside. Lagarde's press conference next week is the second scheduled test. The ECB-Fed divergence story is not resolved; it has simply shifted to one of relative timing and magnitude.

Eurozone retail sales data arrives today, with Q1 GDP figures due tomorrow. These data could help shape expectations ahead of next week's ECB meeting. Unless the data surprise significantly, traders are likely to focus on policy signals rather than economic releases.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1650, 1.1720 and Support sits at 1.1550, 1.1500

USD: The Dollar Pivot - Safe Havens and Macro Data

DXY 99.47

The dollar stayed firm on Wednesday, with the Dollar Index (DXY) trading around 99.30 after posting modest gains overnight. Stronger-than-expected US labour data and renewed geopolitical uncertainty helped underpin demand for the Greenback.

US job openings rose sharply in April. JOLTS data showed vacancies increased to 7.618 million, well above the 6.88 million forecast and up 10.6% from the revised March figure. It is the largest monthly gain in five years. The labour market has strengthened after a soft patch in 2025. Combined with sticky inflation, markets now expect the Federal Reserve (Fed) to begin a rate-tightening cycle in December 2026, pricing roughly 18 bps of Fed hikes by year's end.

The geopolitical overhang remains a live driver. A resumption of Middle East hostilities reinforces the case for a stronger dollar. Higher oil prices push global inflation up. That pushes central banks to hold rates higher for longer. The dollar benefits from all three channels.

The WSJ also reported that Fed Chair nominee Kevin Warsh has chosen two interim policy advisers, one of whom, Paul Winfree, authored the 'Project 2025' chapter on the Fed, recommending the institution drop its employment mandate. The appointment adds a layer of institutional uncertainty to an already complex Fed outlook.

Traders now await ADP private payrolls and ISM Services PMI, which are due later today. Initial jobless claims and the four-week average figures are due tomorrow, and Non-Farm payrolls (NFP) for May arrive on Friday. The sequence amounts to a near-complete read of the US labour market in 72 hours.

The labour market has become one of the most important drivers of Fed expectations. Strong employment data could reinforce the view that policymakers have little urgency to ease financial conditions.

Markets currently price only limited policy tightening expectations through year-end, leaving room for repricing if labour and inflation data continue to surprise to the upside.

AUD and NZD: Commodity Currencies Stay Defensive

AUDUSD 0.7123 | NZDUSD 0.5868 | GBPAUD 1.8833

The Aussie dollar hovered near a two-week low at $0.7123. A return to a trade surplus of AUD 1.79 billion in April, driven by iron ore and coal, offered baseline support, but softer Q1 GDP figures confirm that previous interest rate hikes are successfully cooling domestic demand. The markets have ruled out an immediate rate hike this month from the Reserve Bank of Australia (RBA), leaving the market evenly split on an August move. Meanwhile, the New Zealand dollar rebounded slightly to $0.5868, as traders continue to monitor whether the Reserve Bank of New Zealand (RBNZ) maintains its relatively hawkish stance amid global uncertainty. Both currencies remain highly sensitive to shifts in risk sentiment and developments in commodity prices.

CAD, CNY and JPY: Diverging Regional Themes

USDCAD 1.3900 | USDCNY 6.7746 | USDJPY 159.92 | GBPJPY 214.62 | GBPCNY 9.0981

The Canadian dollar weakened to an eight-week low of 1.3900 against the US dollar. Canada’s economy contracted at an annualised rate of 0.1% in the first quarter, following a revised 1.0% contraction in the prior period. Although the domestic services sector returned to modest growth in May, firms reported the fastest increase in operating costs in four years due to elevated global fuel prices.

In China, the onshore yuan firmed slightly to 6.7746 per dollar, tracking the minor index correction. Strong services activity expanded at its fastest pace in three months, yet the broader economy exhibits two-speed growth: artificial intelligence and robotics are accelerating, while old-economy sectors like real estate contract. To manage liquidity, the People's Bank of China paused cash injections by setting its seven-day reverse repo operations to zero.

Across the East China Sea, the Japanese yen traded tightly near the critical 160.00 level against the dollar. The currency has erased all gains achieved via Tokyo's recent 11.7 trillion yen intervention. Prime Minister Sane Takaichi issued fresh verbal warnings, stating the government stands ready to address excessive movements, while Bank of Japan (BoJ) Governor Kazuo Ueda indicated the central bank will weigh rate hikes if inflationary risks continue to mount.

Current Rate Table:

| Pair | Level | Trend |

|---|---|---|

| GBP/USD | 1.3429 | Neutral |

| EUR/USD | 1.1610 | Neutral-Bullish |

| EUR/GBP | 0.8643 | Rangebound |

| GBP/CNY | 9.0981 | Neutral-Bullish |

| GBP/AUD | 1.8833 | Bullish |

| AUD/USD | 0.7123 | Bearish |

| NZD/USD | 0.5868 | Neutral |

| USD/JPY | 159.92 | Bullish |

| GBP/JPY | 214.62 | Bullish |

| USD/CAD | 1.3900 | Bullish |

| USD/CNY | 6.7746 | Rangebound |

Market Lookahead

Thurs, June 4

- Eurozone retail sales

- US Initial jobless claims

Fri, June 5

- US Unemployment rate (Apr)

- US Average hourly earnings (Apr)

- US Nonfarm payrolls (Apr)

- BoE governor bailey speech

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.