Pound, Euro Pressured as Dollar Holds One-Year Peak Pre-PCE

7 min read

Share

Sterling at 7-month lows on UK succession risk. Euro fades below 1.1370 as Fed hawkishness swamps ECB hike. Dollar holds 13-month highs at 101.53. Yen through 161 on BoJ hawkishness. Oil prices ease as Hormuz reopens. All eyes on core PCE today.

GBP: Pound Absorbs Political Shock as PCE Takes Centre Stage

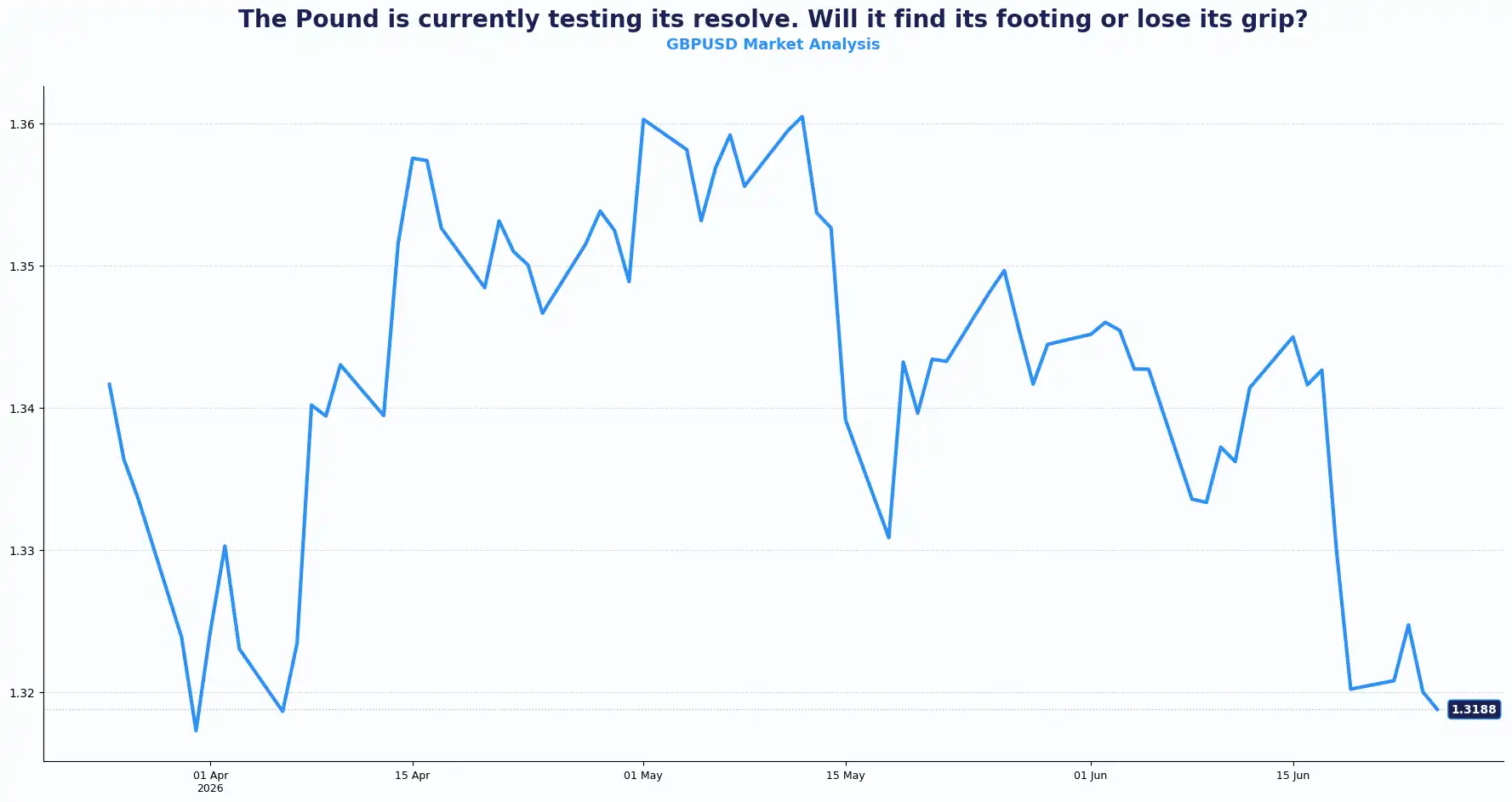

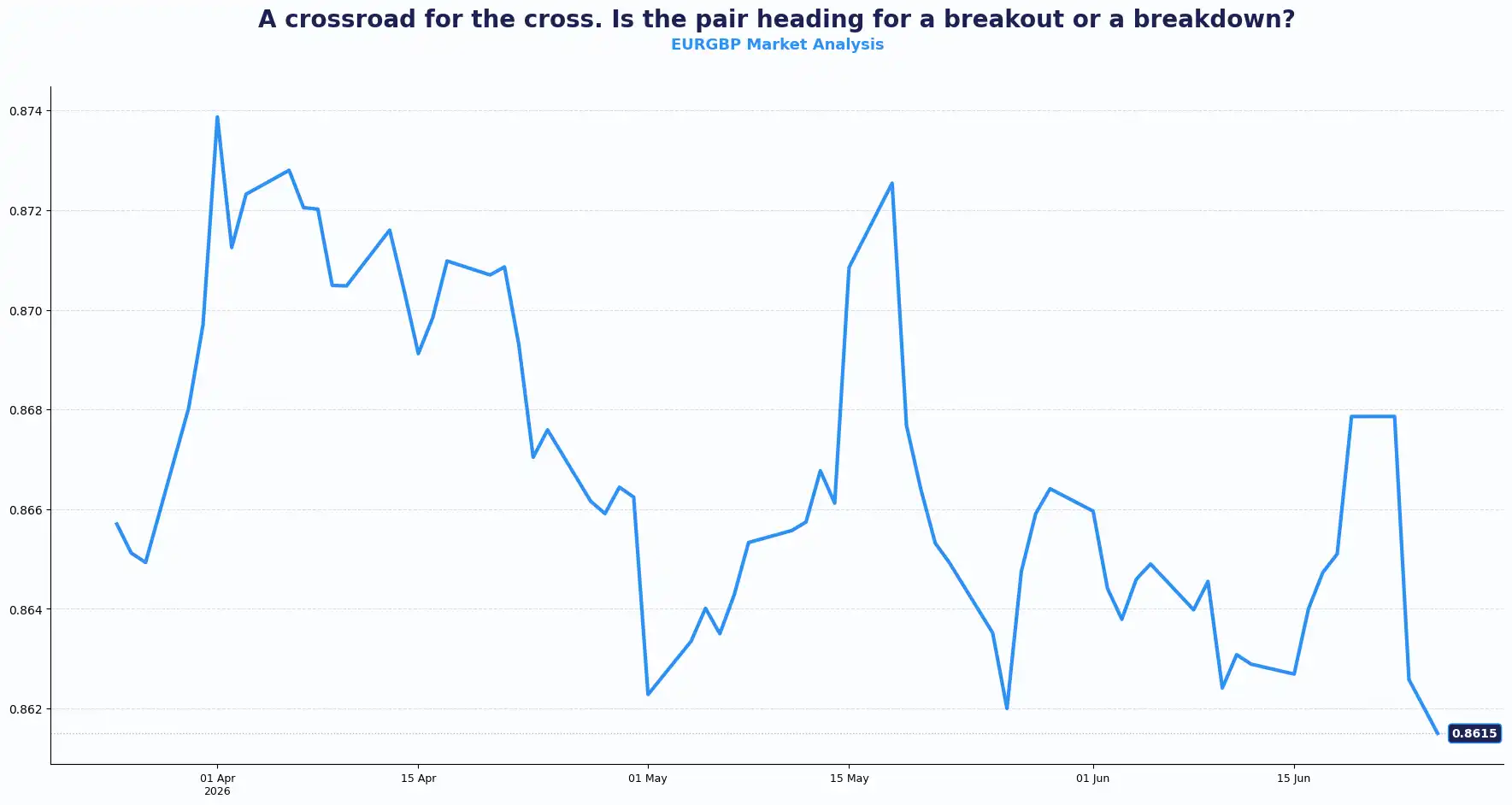

GBPUSD 1.3188 | EURGBP 0.8615

GBP/USD trades near 1.3188 in the early London session, having touched a seven-month low of 1.3140 overnight before recovering marginally. Political instability threatens to undo recent gains; the resignation of Prime Minister Keir Starmer casts a long shadow over the UK outlook.

While the pound showed resilience in early trading, uncertainty regarding the transition to a new leadership under Andy Burnham suggests that tail risks are rising. Leadership nominations open on 9 July and close by the summer recess on 16 July, with a new leader expected in place before Parliament returns in September. Starmer continues as caretaker in the interim.

For sterling, the uncertainty is structural rather than transitory. The immediate question among analysts centres on Burnham's fiscal positioning. His public spending commitments during the Makerfield campaign sit to the left of current Treasury policy, and the UK gilt market has a history of PM's changing tack on borrowing. Any signal of looser fiscal rules from an incoming Burnham administration could prompt a reassessment of the UK's sovereign risk premium, with knock-on effects across GBP-denominated assets.

The BoE held the Bank Rate at 3.75% on 18 June in a 7-2 vote, two members pushed for an immediate hike to 4.00%, and the next decision falls on 30 July. With UK CPI at 2.8% and services inflation at 3.7%, the MPC faces its own debate over tightening, irrespective of who occupies Downing Street.

Investors now watch the US PCE data closely; a strong US print will likely exacerbate the divergence between a policy-constrained Bank of England (BoE) and a hawkish Federal Reserve (Fed).

The Fed's preferred inflation gauge could determine whether current dollar strength extends into month-end or pauses after an already powerful run higher.

For now, sterling continues to trade between domestic political uncertainty and external dollar strength. The currency has shown resilience, but upcoming US data will likely dictate the next move.

The euro softens to 0.8620 against the pound as the market recalibrates its expectations for European Central Bank (ECB) policy.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3250, 1.3335 and Support sits at 1.3100, 1.3000

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8660, 0.8700 and Support sits at 0.8580, 0.8540

EUR: ECB Dovishness Weighs on Sentiment

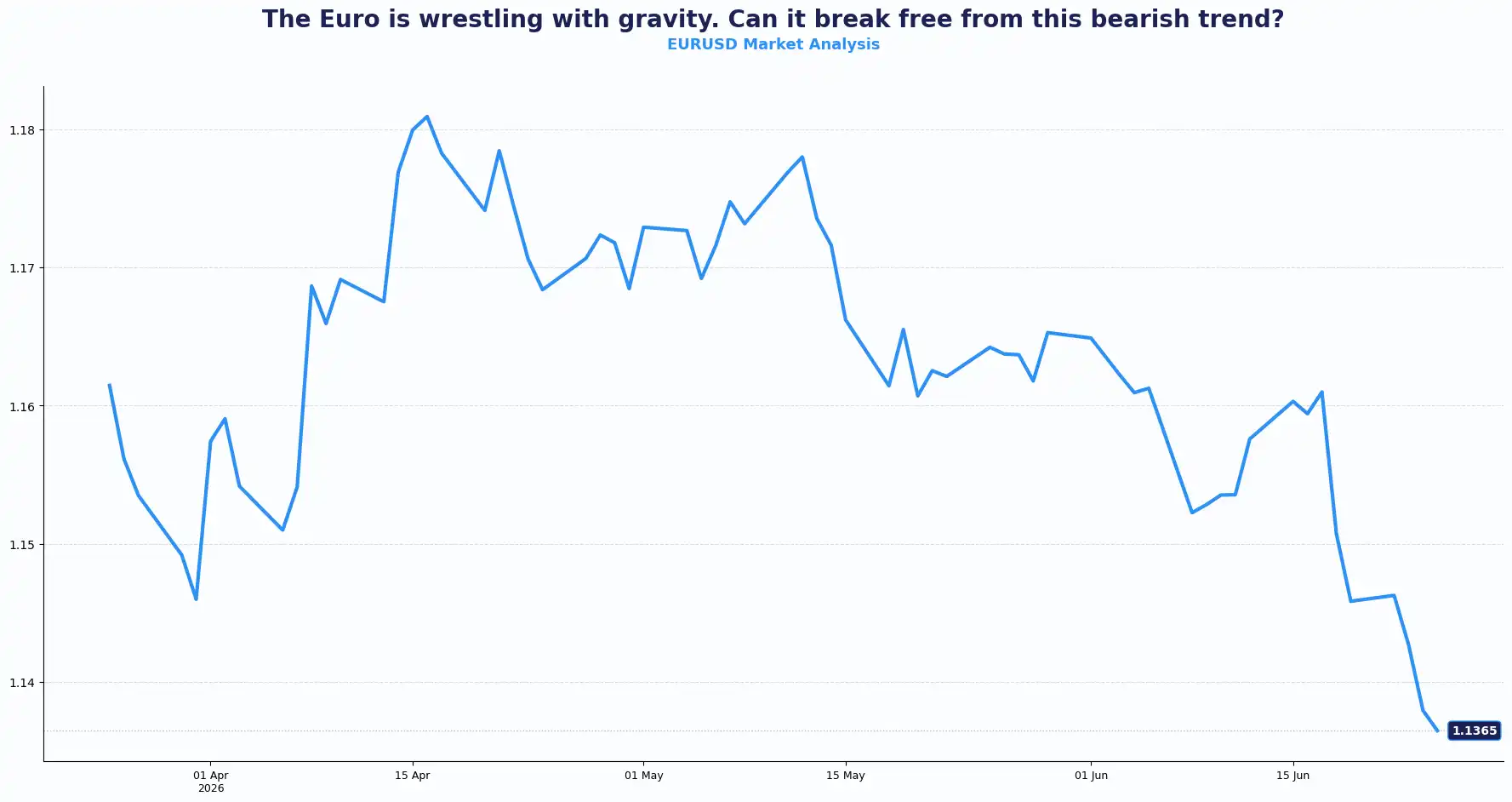

EURUSD 1.1365

The euro struggled to hold gains and slipped back near 1.1360. The pair has shed more than 150 pips from the 1.1500 area that held following the ECB's June hike, reflecting that a single rate move might not override the force of a widening transatlantic yield differential.

The ECB lifted its deposit rate to 2.25% on 11 June, its first hike since 2023, and markets had already priced in the move. Lagarde's recent commentary in the press conference played down second-round inflation risks and stopped short of pre-committing to further tightening, leaving the euro without a fresh catalyst to absorb the subsequent dollar bid.

German business confidence edged up for the second consecutive month, with the June IFO Business Climate Index printing at 85.6, up from 85.0 in May, with current conditions at 87.0 and expectations at 84.1; the absolute levels still reflect the softest sentiment since early 2025. A German economy stabilising at the floor is not the same as one recovering from it.

The yield gap remains the primary driver. Two-year US Treasury yields currently outpace their German counterparts by a significant margin. This widening spread, coupled with lukewarm data, though German IFO figures showed a slight uptick, leaves the single currency vulnerable. The euro cannot easily rally against that backdrop, even with its own rate hike. The outlook stays bearish below key resistance.

The EUR/USD pair's near-term recovery from Thursday's lows will depend more on US data than on any further ECB communication.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1420, 1.1575 and Support sits at 1.1300, 1.1250

USD: Hawkish Fed Keeps the Greenback Tall

DXY 101.53

The dollar index sits at 101.53, its highest level in over a year. The move reflects a combination of stronger US economic expectations, rising Treasury yields, and a Fed that continues to signal concern over inflation risks.

The latest Fed meeting reinforced that message. Chair Kevin Warsh maintained a firm stance on price stability, prompting traders to push up rate expectations. Those expectations have widened yield differentials across major economies and strengthened demand for the dollar. The numbers underline the trend.

The structural argument for the dollar goes beyond the immediate inflation read: analysts point to productivity growth, partly AI-driven, that supports earnings and generates dollar-positive capital inflows. That thesis has now absorbed the geopolitical noise that defined April and May.

The US-Iran interim peace agreement has put the Strait of Hormuz back in service, and energy prices have retreated sharply from the above-$100 levels seen last month. Oil approaching its pre-conflict range removes the headline inflationary tailwind, but core inflation is the Fed's preferred lens. The PCE price index for May, the Fed's own inflation gauge, publishes today.

Headline PCE ran at 3.8% YoY in April. Core PCE stood at 3.3%. The May print arrives against the backdrop of the US CPI already at 4.2% YoY, its highest since April 2023 driven by the Iran-war energy shock. With oil now retreating, the May PCE read could signal whether that shock passed through to services and shelter, or whether it remained concentrated in energy.

Other data due today include final Q1 GDP, May personal income, preliminary durable goods orders, and weekly jobless claims for the period ending 20 June. The dollar's position at a 13-month-high makes it sensitive to any downside surprise in the PCE data. An in-line or stronger print could likely extend the DXY's run toward 102.00.

Others: Yen Pressure Mounts, Antipodeans Under Water

AUDUSD 0.6895 | NZDUSD 0.5645 | USDJPY 161.77 | GBPJPY 213.19

The Australian dollar fell below 0.6900. The New Zealand dollar traded at 0.5645, near recent multi-week lows. Both currencies carry a risk-sensitive character that is amplified during periods of broad dollar strength, and the current environment, equity volatility, a hawkish Fed, and uncertainty around the Iran peace process. These factors are working against the Antipodeans on multiple vectors simultaneously. Domestic data in Australia pointed to resilience in employment and consumer demand, but those readings failed to offset the gravitational pull of a stronger Greenback. AUD/USD holds above the 0.6850 support area for now; a break below opens the path toward 0.6800.

USD/JPY trades at 161.77, deep into the territory that previously drew scrutiny from Japanese officials. BoJ board member Naoki Tamura delivered his clearest public case yet for an accelerated tightening path on Thursday, calling for rate hikes every few months toward a 2% neutral rate. Tamura placed underlying Japanese inflation already at the 2% target and argued that delaying further normalisation risks forcing sharper moves later. He voted against the board's decision to pause JGB purchase tapering, pushing instead for immediate balance sheet normalisation.

Across the region, the key theme remains unchanged. Lower energy prices are helping contain inflation pressures, while higher US yields continue to shape currency performance.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3188 | Bullish recovery |

| EUR/GBP | 0.8615 | Bearish |

| EUR/USD | 1.1365 | Bearish |

| DXY | 101.53 | Bullish |

| USD/JPY | 161.77 | Bullish |

| GBP/JPY | 213.19 | Bullish |

| AUD/USD | 0.6895 | Bearish |

| NZD/USD | 0.5645 | Bearish |

Market Lookahead

Thurs, Jun 25

- US Personal Consumption Expenditure (PCE) (May)

- US GDP Q1

Fri, Jun 26

- Tokyo CPI (Jun)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. Forward contracts can help businesses manage foreign exchange exposure by providing greater certainty over future exchange rates, although they may also mean that businesses do not benefit from favourable exchange-rate movements. Businesses should consider their individual circumstances and speak with their dealer to understand how forward contracts may support their specific foreign exchange requirements. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.