Labour Succession Clouds Sterling as PMIs Loom

7 min read

Share

UK PM Starmer resigns, Burnham leads the succession field. Gilt yields near 18-year highs as fiscal uncertainty builds. Lagarde signals contained inflation pass-through; ECB tightening expectations ease. EUR/USD near three-month lows. Hormuz tensions ease as Iran resumes crude loading. The dollar firms on hawkish Fed bets. Global flash PMIs due today.

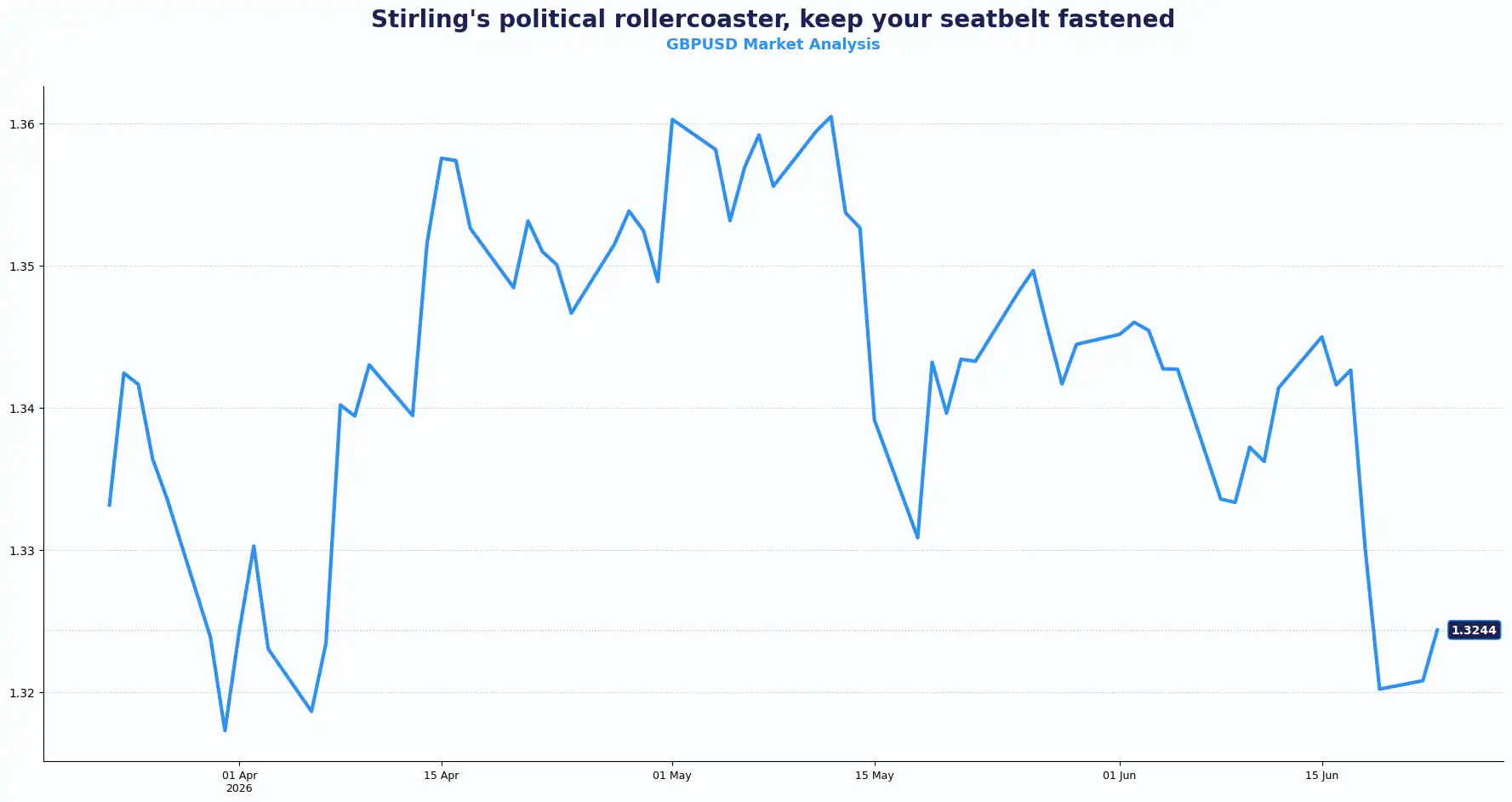

GBP: Sterling Takes a Political Hit Amid Fiscal Concerns

GBPUSD 1.3244 | EURGBP 0.8628

GBP/USD holds near $1.3250 after Prime Minister Keir Starmer's resignation triggered another leadership transition in Westminster. The Labour Party now faces a leadership contest. Andy Burnham is the frontrunner. Pound faces a fiscal test as the leadership race begins. The EUR/GBP pair held near 0.8630.

The key question for Sterling right now is whether it's a coronation or a contest. A swift, clean transition is likely to hold the pound relatively steady. A drawn-out race with rival candidates making fiscal pledges could pull the sterling lower and fast.

Burnham has pledged to respect Rachel Reeves' fiscal rules. But investors will still want evidence that spending commitments and fiscal discipline can coexist, and the gilt market does not appear patient. UK ten-year gilt yields sit around 4.85%, near their highest since the 2008 financial crisis. Britain now borrows at a higher rate than any other developed nation in the medium term, making it a structural vulnerability. Britain’s stretched finances and political uncertainty leave sterling highly sensitive to fiscal headlines.

Traders are already paying more to hedge sterling volatility in the options market than they were on Friday. Any candidate who signals fiscal loosening will likely see those hedges get more expensive, quickly.

Today's UK PMI data could offer the next directional signal. Manufacturing PMI is expected at 53.6, slightly below the previous 53.9. Services PMI is forecast at 50.0, up from 49.3.

Manufacturing activity remains in expansion territory. The bigger focus may fall on services, which account for the largest share of UK economic output. A stronger reading could support the view that domestic activity is holding up despite political uncertainty. Political risk still remains the dominant driver in the near term.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3300 and Support sits at 1.3200

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8680 and Support sits at 0.8590

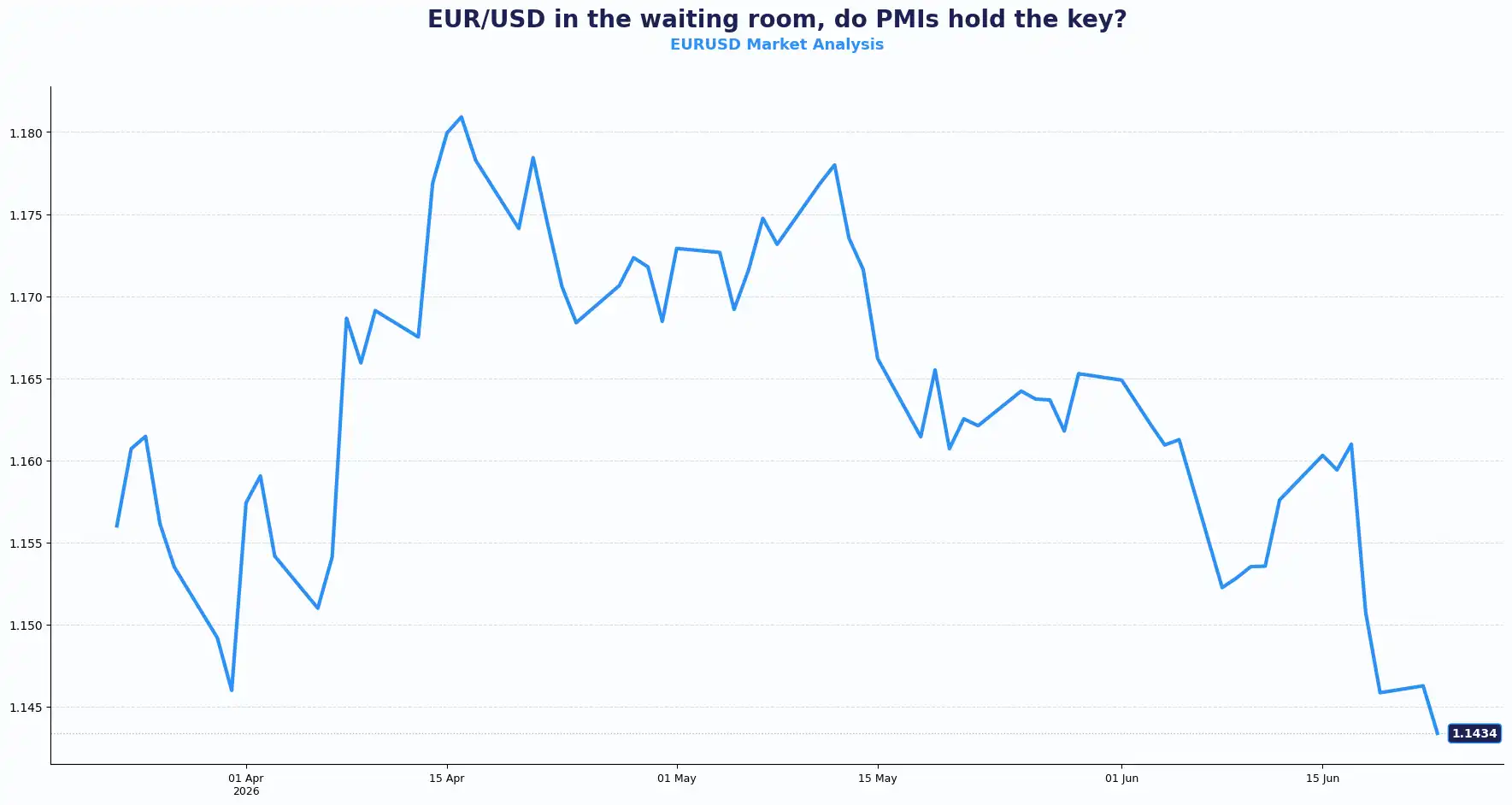

EUR: Euro Slips as ECB Tempers Inflation Fears

EURUSD 1.1434

EUR/USD sits at $1.1434, near a three-month low. The euro is caught between ECB caution and global risk aversion.

ECB President Lagarde’s recent commentary on limited inflationary pass-through dampened expectations for aggressive rate hikes, leaving the currency vulnerable to economic data surprises. She noted that inflationary pass-through may prove more limited than the 2022-23 episode, though she acknowledged that wage formation could be more sensitive to new shocks. On the Gulf situation, Lagarde said recent developments remain within the ECB's pre-modelled scenarios. No surprise, no pivot, no urgency.

That stance contrasts with growing expectations for a more hawkish Federal Reserve (Fed). The widening policy gap continues to favour the dollar over the euro.

Market pricing suggests only 33 basis points of tightening by year-end, down sharply after Lagarde's comments. The euro currently lacks a policy catalyst to move higher.

The day's critical data point is the flash PMI print from Germany and the Eurozone. The Eurozone manufacturing PMI consensus stands at 51.2, up from 51.6 previously, still expanding. The services PMI consensus is 48.1, up from 47.7, still in contraction but improving at the margin. It is the services reading that carries the weight for the EUR/USD pair today. A positive surprise could push the pair back toward $1.15, while a miss could trigger the three-month low as the floor to test below.

The euro is also carrying risk-off pressure from uncertainty around the US-Iran peace deal; the single currency is failing to find a firm footing. Progress on Hormuz talks would typically support risk appetite, but the path to a confirmed deal is not straight. Until clarity arrives, the euro is likely to remain defensive.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1500 and Support sits at 1.1380

USD: The Hawkish Fed Ascendant

DXY 101.04

The dollar index DXY trades at 101.04, close to its strongest level since May last year. The catalyst is clear: the Fed held rates at its last meeting but opened the door to hikes, and traders are repricing it fast.

Fed funds futures now price a 54% implied probability of at least two 25bps hikes before year-end, up from 15.2% just one week ago. New Fed Chair Kevin Warsh is taking a more aggressive posture than his predecessor. US two-year Treasury yields hit 4.236% on Monday, the highest since February 2025, before retreating slightly to 4.209% in today’s Asian trade. Ten-year yields sit at 4.500%.

Today’s US flash PMIs figure adds to the picture. Manufacturing PMI is expected at 54.7, down from 55.1 previously. Services PMI is forecast at 51.0, up from 50.7. Stronger-than-expected data could further support the dollar by reinforcing confidence in the US growth outlook.

Oil prices retraced after earlier gains. US Vice President JD Vance confirmed progress in US-Iran talks and said the Strait of Hormuz is allowing ships to pass. Washington also granted Tehran a 60-day licence to sell oil on international markets. Iran resumed loading crude from its Kharg island export terminal following the lifting of the US Navy blockade. Brent Crude sits at $77.50 a barrel, down 0.5% as supply concern eases. Lower oil prices briefly tempered the inflation read, but the Fed's hawkish stance remains the dominant narrative.

Gold extended losses on the same dynamic. Silver is also under pressure. The PCE report later this week is the Fed's preferred inflation gauge, which could be the next major flashpoint for the dollar.

Fed Governor Waller noted the dollar's role is evolving, with rapid moves to expand access to dollar-denominated assets and more competition described as "a good thing." That framing does not signal concern but confidence.

The passing of former Fed Chair Alan Greenspan at 100 added a reflective note to Monday's session. Warsh cited Greenspan directly at his own swearing-in last month: "Chair Greenspan was the first to tell me and show me what this role demands." The contrast between Greenspan's era of opacity and Warsh's current hawkish clarity was not lost on traders.

Analysts now see potential for an additional 2% to 3% upside in the dollar index on a clear break above the 14-month high at 101.97.

Other Currencies: Intervention Risks and Carry Trades

AUDUSD 0.6960 | NZDUSD 0.5690 | USDJPY 161.60 | GBPJPY 213.95

USD/JPY traded around 161.60 and remained close to levels that have previously triggered intervention concerns. The divergence theme continues to dominate. Japan still operates with significantly lower interest rates than the United States. That gap keeps pressure on the yen. Traders continue to monitor the 161.95 area in USD/JPY. Any move beyond that region could increase speculation about official intervention.

Australian and New Zealand yields remain relatively attractive, but both currencies have struggled against a stronger dollar. The Australian dollar fell towards 0.6960 while the New Zealand dollar weakened near 0.5690.

The Reserve Bank of New Zealand is still expected to raise rates in July. Even so, shifting Fed expectations have overshadowed local factors. Market attention remains on growth indicators, inflation data, and central bank guidance.

The Swiss franc also lost ground as rising US rate expectations boosted demand for the dollar.

Across Asia, regional currencies face a balancing act between softer oil prices and renewed dollar strength. The Indonesian rupiah faces pressure amid looming MSCI downgrade risk. The Indian rupee is grinding between a firm dollar and lower oil prices, with those forces pulling in opposite directions. Asian equities are broadly softer, with South Korea's KOSPI among the notable underperformers.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3244 | Bearish |

| EUR/GBP | 0.8628 | Mildly bullish EUR |

| EUR/USD | 1.1434 | Bearish |

| USD/JPY | 161.60 | Bullish USD |

| GBP/JPY | 213.95 | Bearish GBP |

| AUD/USD | 0.6960 | Bearish |

| NZD/USD | 0.5690 | Bearish |

Market Lookahead

Tue, 23 June

- Global PMI’s (Manufacturing, Services, Composite) (Jun) Australia, Eurozone, the UK and the US

Wed, Jun 24

- Australia’s CPI (May)

- Germany’s IFO Business Climate and Current Assessment (Jun)

Thurs, Jun 25

- US Personal Consumption Expenditure (PCE) (May)

- US GDP Q1

Fri, Jun 26

- Tokyo CPI (Jun)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. Forward contracts can help businesses manage foreign exchange exposure by providing greater certainty over future exchange rates, although they may also mean that businesses do not benefit from favourable exchange-rate movements. Businesses should consider their individual circumstances and speak with their dealer to understand how forward contracts may support their specific foreign exchange requirements. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.