Iran Tensions and US CPI Hold the Dollar in Check

7 min read

Share

Sterling consolidates below 1.34 as geopolitics and domestic political noise weigh. The euro steadies around 1.1550. The tit-for-tat attacks in the Middle East Oil prices surging, yet Brent remained below the $100 per barrel level. The Dollar Index (DXY) hovers near 99.87 ahead of May US CPI figures that could reset Fed rate expectations for the rest of the year.

GBP: Sterling Buckles Under Double-Edged Pressure

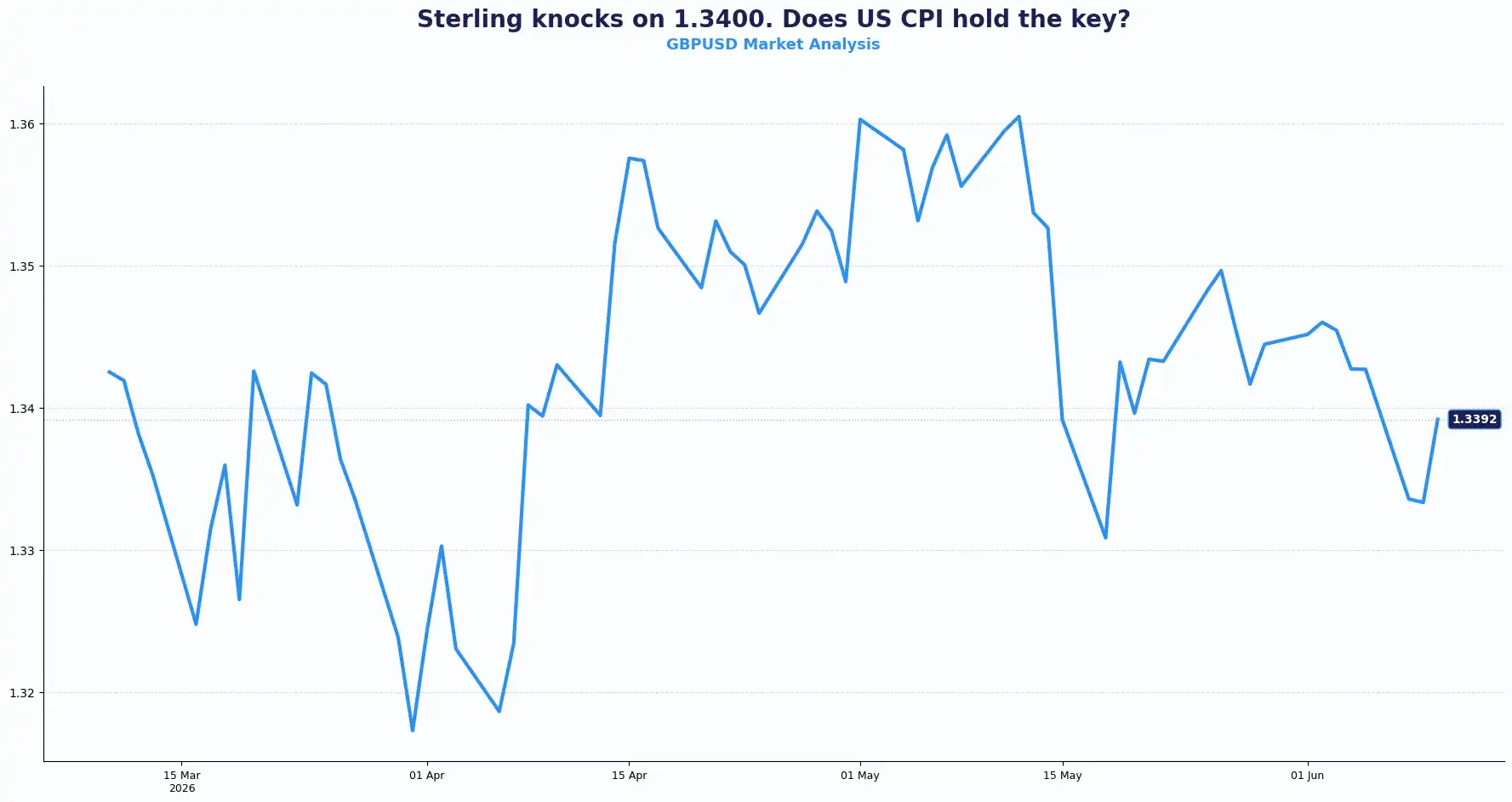

GBPUSD 1.3392 | EURGBP 0.8626

Cable trades around 1.3365-1.3370 in the Asian session, essentially flat on the day. The pair has pulled back from a three-week low near 1.3300, yet struggles to build on that recovery - testing 1.34. Both buyers and sellers are waiting for fresh geopolitical developments and for the US May CPI data due later today.

The anchor holding the pair down is the dollar's safe-haven bid. Renewed US military strikes against Iran, ordered by President Trump in retaliation for the shooting down of a US helicopter in the Strait of Hormuz, have put the risk appetite on the back foot in Asian trade. The lack of progress in US-Iran negotiations deepens that caution. Oil prices have surged amid the escalation, stoking concerns that the Federal Reserve (Fed) will have less room to stay on hold. Traders currently price roughly a 70% probability of at least one 25-basis-point Fed rate hike by year-end, and around a 38% chance the move comes as early as September, according to CME FedWatch data. This rate outlook continues to underpin the dollar.

Sterling's own domestic picture adds another layer of drag. UK political uncertainty runs counter to expectations of a 25 basis-point BoE rate hike before the end of 2026. The two forces largely offset each other: BoE tightening bets, historically speaking, should lift GBP, but political noise caps it. Iran's Foreign Minister Abbas Araghchi has meanwhile warned Gulf states of their "legal and moral responsibility" to prevent US and Israeli strikes, keeping geopolitical risk alive. There is a "strange calm" in the market for now, with both sides appearing to avoid major escalation, but the ceasefire agreed in April is hanging by a thread.

UK GDP and industrial production data for April arrive on Friday, which could give traders a firmer read and insights into domestic momentum.

The pair's tight range reflects a genuine stalemate between two competing macro forces. Until the CPI print lands and the geopolitical fog lifts, the GBP/USD pair is likely to remain anchored within the 1.3300-1.3400 band.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450 and Support sits at 1.3330

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8650 Support sits at 0.8600

EUR: Euro Finds Support Above 1.15

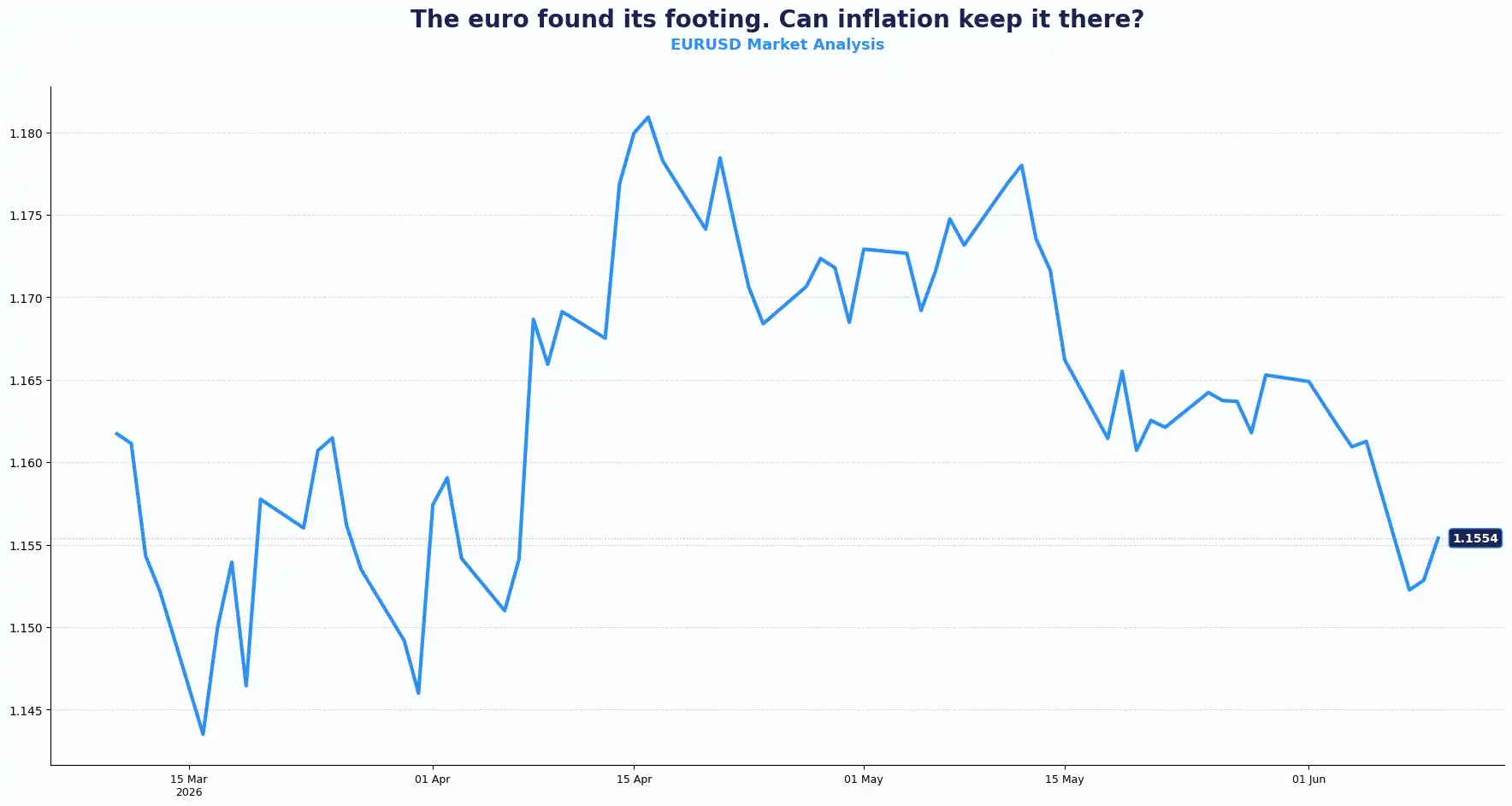

EURUSD 1.1554

The EUR/USD pair trades around 1.1545-1.1555, bounced off a two-month low, but with limited follow-through to the upside. The dollar's safe-haven appeal, sustained by Middle East tensions and expectations of a Fed rate hike, keeps the pair capped in the near term. The immediate price action reflects a defensive posture, with spot prices pinned into a tight range as the market braces for a potential macroeconomic shock.

The structural narrative now hinges on core inflation metrics. A hot monthly core CPI reading could further lift Fed tightening odds, lifting the dollar and sending the EUR/USD pair lower from current levels. A soft reading could ease the pressure, but market analysts widely expect any USD weakness to be limited and short-lived; the broader geopolitical backdrop and the energy-driven inflation story are not going away.

The European Central Bank (ECB)'s decision on the deposit facility rate is also on the calendar this week. ECB policy expectations have leaned hawkish, providing some support to the euro. The EUR/JPY pair trades near 185.20, with scope to test the 186 level while the cross holds above 185. Germany's Harmonised Index of Consumer Prices (HICP) for May also arrives on Friday, which could recalibrate ECB bets ahead of that decision.

The structural picture for the EUR/USD pair is one of cautious stabilisation rather than directional conviction. The euro has support from ECB rate expectations and improving regional data, but the energy shock with crude up more than 50% since the conflict began in late February, continues to weigh on the Eurozone's terms of trade. The dollar holds a structural advantage here: the US economy is broadly more insulated from energy price shocks than its European peers. That relative resilience helps explain why USD safe-haven demand has been sticky even as the CPI narrative evolves.

The EUR/USD pair needs a clean break above 1.1600 to shift the near-term tone. That means either a soft US CPI print today or a meaningful de-escalation in the Middle East, and neither is certain. For now, the 1.1480-1.1400 zone remains the key support area on any renewed USD strength.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1600 and Support sits at 1.1480-1.1400

USD: Dollar Holds Waiting on CPI, Amid Middle East Tensions

DXY 99.92

The dollar index sits near 99.87, softer on the session but underpinned by safe-haven demand and persistent pricing for Fed rate hikes. The back-and-forth between the US & Iran over fresh strikes has dominated overnight headlines and kept the dollar supported, even as Treasury yields pull back.

The US Bureau of Labour Statistics (BLS) releases the May CPI today. The headline reading is expected to rise 4.2% YoY, up from 3.8% in April, the highest annual pace since May 2023, driven by persistently elevated energy prices. The monthly headline CPI is forecast at 0.5%, down marginally from April's 0.6% rise. Core CPI, which strips out food and energy, is expected to come in at 0.3% MoM and 2.9% YoY. Crude oil prices are up more than 50% since the Middle East conflict began at the end of February, and the energy channel into core goods and services inflation is broadening.

A hot core print today could push the September rate hike probability above 38% and give the dollar fresh upside. If CPI disappoints, the Fed retains more flexibility at next week's meeting, but any dollar pullback is likely to be contained by the geopolitical backdrop.

US stocks slid overnight as a tech rebound ran out of steam, with AI valuation concerns, rising rate expectations, and Middle East tensions weighing on sentiment. The dollar index (DXY) could dip towards 99.50–99.00 on a soft CPI outcome. A firm reading keeps the index anchored above 99.50. US Producer Price Index data for May will also be released tomorrow.

Global Crosses: Asian and Emerging Markets Fracturing

AUDUSD 0.7018 | NZDUSD 0.5814 | USDJPY 160.37 | GBPJPY 214.67

USD/JPY climbed to 160.37 and continues to trade close to levels that have previously attracted official intervention. Japan's wholesale inflation accelerated at its fastest pace in three years during May. The data strengthened expectations that the Bank of Japan could tighten policy further.

The Bank of Japan faces a difficult balancing act. Persistent yen weakness increases imported inflation. At the same time, rising US rate expectations continue to widen the policy gap between Tokyo and Washington. Traders now see a BOJ rate increase in June as a realistic possibility.

Meanwhile, AUD/USD held above 0.7000, while NZD/USD traded near 0.5814, as commodity-linked currencies tracked broader shifts in risk sentiment.

Across emerging markets, pressure from a stronger dollar and higher energy costs is already emerging. Bank Indonesia surprised investors with an off-cycle rate increase as officials moved to support the rupiah.

Asian and emerging-market currencies remain highly sensitive to shifts in US inflation expectations, energy prices, and central bank policy signals.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3392 | Consolidating |

| EUR/USD | 1.1554 | Flat |

| EUR/GBP | 0.8626 | Range-bound |

| USD/JPY | 160.37 | Slow uptrend |

| EUR/JPY | 185.2 | Watching 186 |

| AUD/USD | 0.7018 | Recovery bias |

| NZD/USD | 0.5814 | Consolidating |

| GBP/JPY | 214.67 | Firm |

| USD/CNY | 6.80 | Bearish bias |

Market Lookahead

Wed, 10 June

- US CPI Inflation (May)

- Bank of Canada Interest Rate Decision

Thurs, 11 June

- ECB Interest Rate Decision

- ECB Press Conference

- Australia Inflation Expectations

- US Producer Price Index (May)

- US Initial Jobless Claims

Fri, 12 June

- UK GDP

- UK Industrial Production

- Germany HICP Inflation

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.