Gulf Attacks, PCE Day and a Dollar Holding Firm

8 min read

Share

Ceasefire optimism shattered as the US and Iran exchange fresh attacks. Oil jumps 3.6%. PCE lands today, the Fed's preferred inflation gauge. The dollar holds 99.50. Sterling steady. ECB June hike near-certain. AUD slides. Oil shocks, central bank divergence and inflation fears drive FX flows.

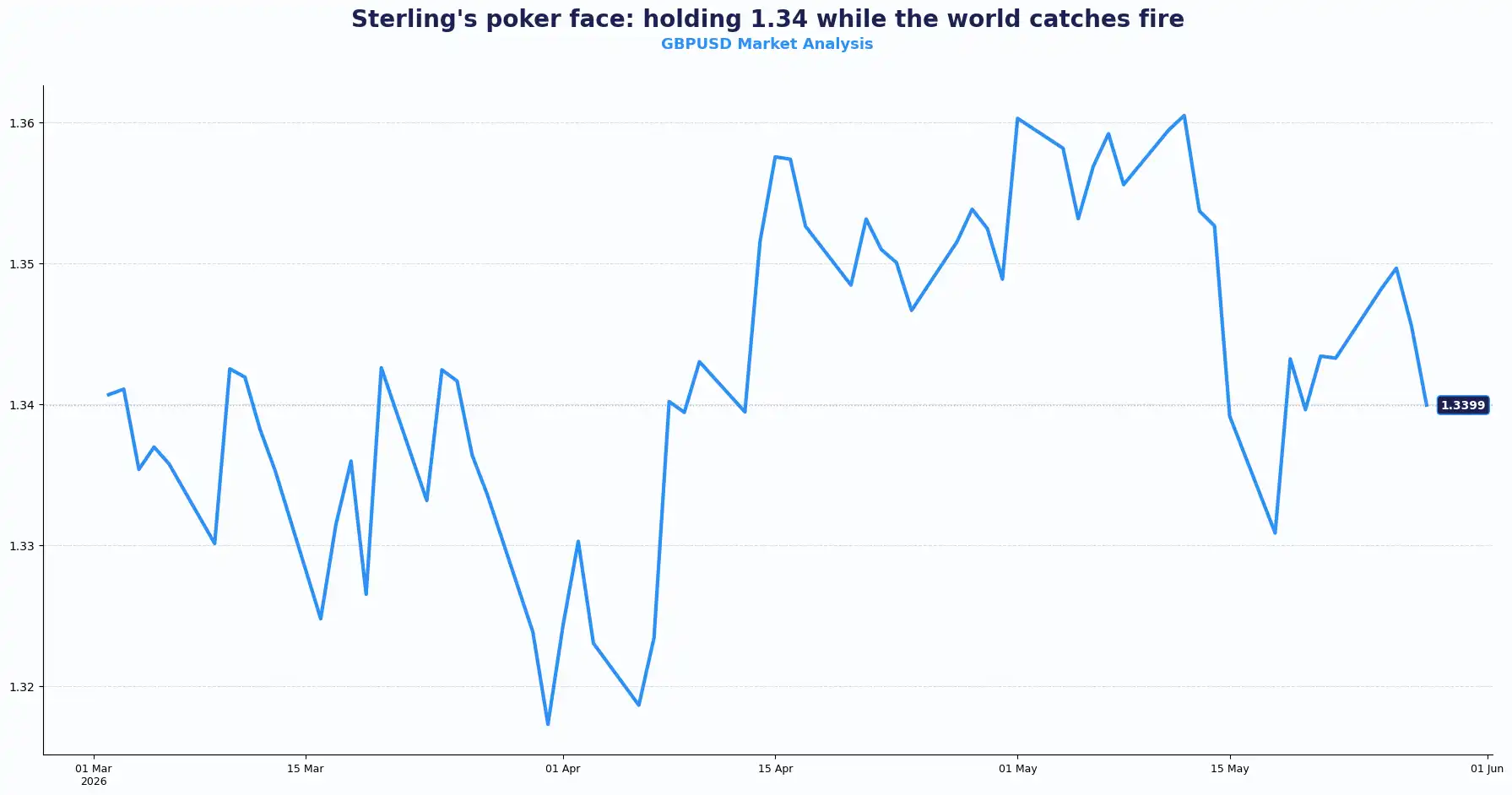

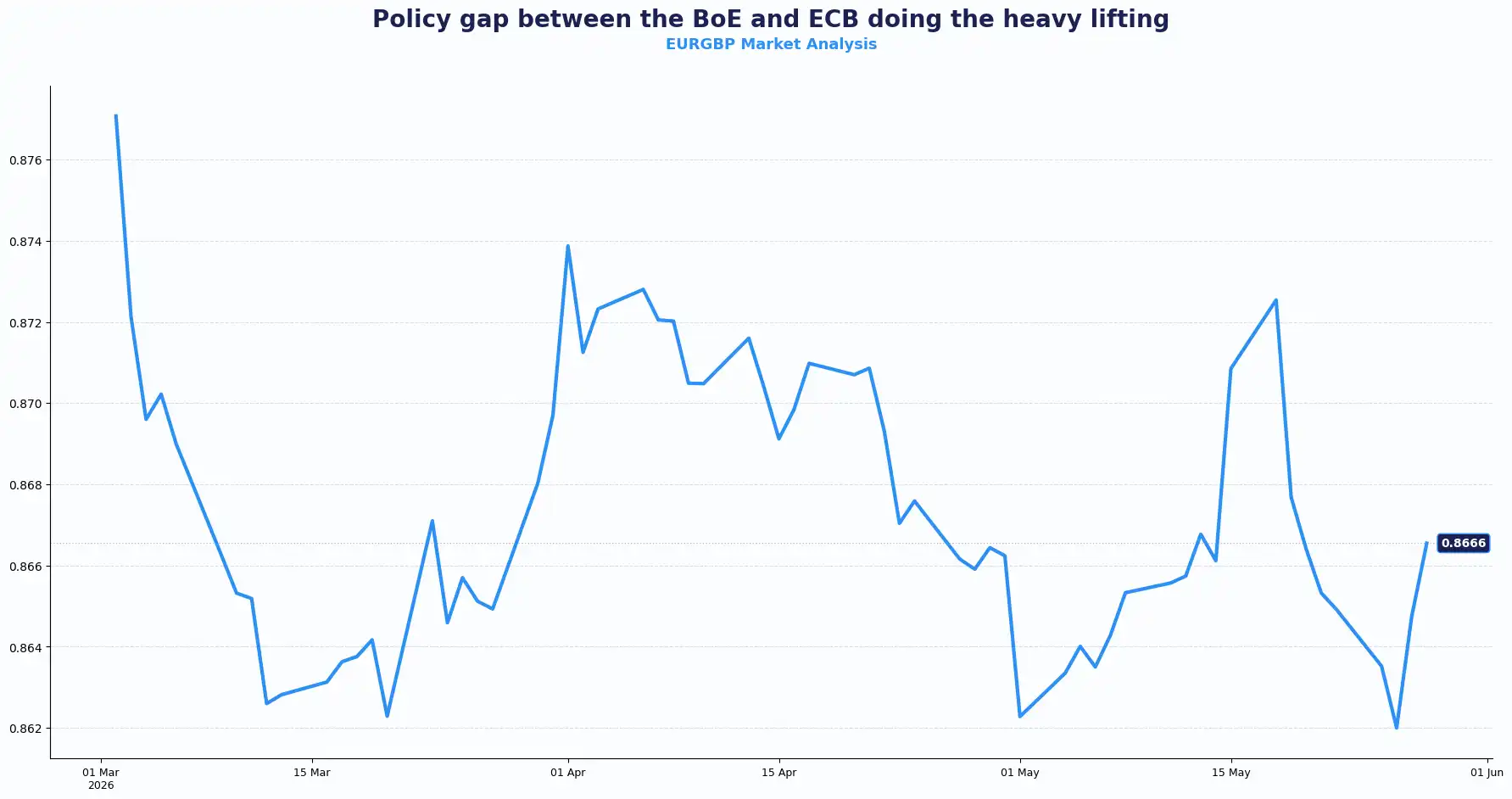

GBP: Steadies as Oil Shock Tests Risk Appetite

GBPUSD 1.3399 | EURGBP 0.8666

Sterling is testing 1.34 against the dollar on Thursday, trading near the 1.3393 mark in the previous session. The sterling found some footing despite a broader risk-off tone sweeping through Asian and European sessions. The EUR/GBP pair retreated toward the 0.8660 baseline as investors weighed Middle East tensions against diverging central bank paths.

Fresh US strikes on Iranian targets and reports of missile attacks near Kuwait hit risk sentiment across Asia and Europe. This sudden escalation completely broke the early optimism surrounding a regional peace deal and revived inflation fears across developed economies, driving investors back toward the dollar. Oil prices surged again. Brent Crude climbed towards $98 a barrel while WTI pushed above $92.

Rising energy prices support the dollar by boosting Treasury yields and tightening Federal Reserve (Fed) expectations. At the same time, the Bank of England (BoE) still looks less aggressive than the European Central Bank (ECB).

Insurance costs for shipping through the Strait of Hormuz have become prohibitively expensive. This reality cuts off traffic to a mere trickle. Over the next fortnight, the market faces a binary outcome: either diplomatic channels secure a fresh ceasefire or the current truce might collapse into open hostilities. For the UK, this energy shock complicates the macroeconomic picture just as domestic fundamentals show underlying strength.

Tomorrow's Nationwide housing data is expected to show a solid print of 3.0% YoY and 0.4% MoM. Higher property values indicate a highly sensitive economic recovery that continues to hum despite global headwinds. A softer print would reinforce the BoE's rationale for holding rates, while its continental peers face much heavier pressure.

The UK faces imported inflation risks through energy, while domestic growth momentum cools. That leaves the BoE trapped between sticky inflation and fragile demand.

Governor Bailey speaks on Friday. His tone on inflation persistence and rate guidance is particularly significant at a time when the market is closely watching UK data for any shift in the BoE's stance.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3500 and Support sits at 1.3300, 1.3200

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700, 0.8730 and Support sits at 0.8600, 0.8550

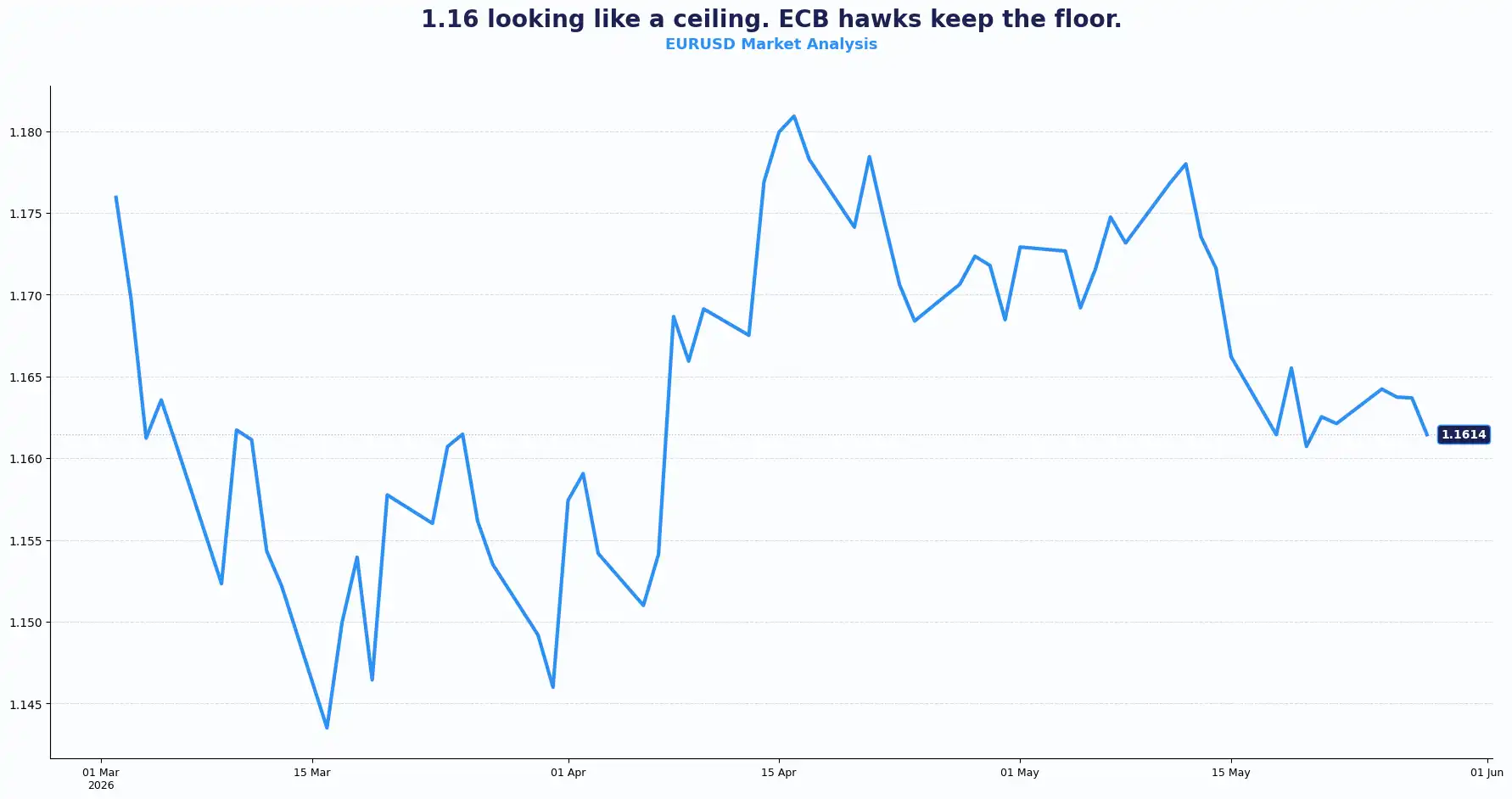

EUR: Euro Fragile but the Policy Story Stays Intact

EURUSD 1.1614

The euro slipped 0.3% to trade around $1.1590, though it continues to draw underlying support from the ECB-Fed policy divergence narrative, now testing the 1.16 level. Investors still expect the ECB to raise rates at its June meeting, with pricing implying around a 91% probability of a hike, according to the ECB Watch Tool. The conviction has kept the single currency from a more pronounced sell-off even on a day when risk appetite is taking a notable hit.

ECB Chief Economist Philip Lane struck a clear note this morning, warning that inflationary consequences of the US-Iran conflict will outlast the fighting itself. His comments reinforced concerns that higher energy costs may seep into broader inflation expectations across the Eurozone and that the focus should be on preventing long-run inflation expectations from becoming entrenched.

Policymakers want to stop another energy shock from embedding itself into wages, services, and consumer behaviour. The bank appears more willing to tolerate slower growth if it keeps inflation expectations anchored.

A signal that the ECB has no appetite for a policy pause. ECB President Christine Lagarde joins a central bankers' meeting today; Markets will listen closely for signals on how aggressively the ECB plans to respond if energy prices stay elevated.

On the data front, today brings Eurozone Consumer Confidence for May (consensus: -19, in line with the prior 19), alongside the Economic Sentiment Indicator, Industrial Confidence, and Services Sentiment figures, which could shape expectations around regional demand. Consensus expects no surprise, but any deviation from the -19 print matters given the backdrop of oil-driven inflation risk.

Tomorrow adds Germany's import price index for April, followed by Germany's CPI and HICP prints for May. German CPI consensus sits at +0.1% MoM (prior: +0.6%) and +2.8% YoY (prior: +2.9%). The Harmonised Index of Consumer Prices (HICP) consensus is +0.2% MoM (prior: +0.5%) and +2.9% YoY (prior: 2.96%). A softer German inflation print could test ECB hike conviction at the margin and could further shape ECB’s narrative into June.

European equity futures reflected the mood, with EURO STOXX 50 futures falling 1.2%, DAX futures dropping 1.0%, and FTSE futures shedding 0.9%, as investors reduced risk exposure.

The euro still draws support from monetary policy divergence. Traders see the ECB leaning hawkish while the BoE and Fed balance inflation risks against weakening growth.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1650, 1.1700 and Support sits at 1.1500, 1.1450

USD: Holds Ground on Hawkish Fed Rhetoric, PCE Lands Today

DXY 99.43

The dollar trades at 99.50 on the DXY index, steady on the week and anchored by a hawkish shift in Fed expectations. Today's key catalyst for the dollar is the April Personal Consumption Expenditure (PCE) report, the Fed’s preferred inflation gauge.

US Treasury yields tracking the 10-year note climbed four basis points to 4.526%, reflecting the intense upward pressure that expensive oil exerts on inflation. The greenback squeezed its major counterparts as investors swiftly pivoted toward defensive assets, anticipating tonight’s crucial economic releases and a media briefing from Treasury Secretary Scott Bessent.

Consensus places the headline PCE at +3.8% YoY, a three-year high), with energy prices providing the lift. Core PCE, which strips out food and energy, is projected at +0.3% MoM and +3.3% YoY, sitting well above the Fed's 2% target. The Q1 PCE figure is anticipated to arrive at +4.3% annualised, unchanged from prior.

US GDP for Q1 also prints today, with consensus at +2.0% annualised, matching the prior reading.

Initial jobless claims are projected to tick up modestly from 209k to 211k. A reading in line with or below that consensus would reinforce a stable labour market picture. The four-week average figures are what most investors would look for cues.

Fed Governors Jefferson and Cook both noted that inflation risks remain tilted firmly to the upside. Jefferson noted that risks to inflation are "tilted to the upside," whilst signalling that the current policy rate position leaves the Fed "well positioned." He expects more modest growth as households absorb high energy costs. Fed Governor Cook repeated her view that inflation is "clearly moving in the wrong direction," with core PCE estimated at +3.3%, and stated preparedness to raise rates if disinflation fails to materialise. Both officials retained a hold bias for now.

Fed's Goolsbee flagged that an oil shock amplifies the inflation problem from anticipated future productivity growth; the bigger the AI productivity hype, the higher rates may ultimately need to go.

This collective hawkish pivot has forced traders to price a 50/50 chance of a 25bps rate rise in the funds rate to a 3.75%-4.0% range by year-end. This completely erases previous assumptions of an easing bias and keeps the dollar highly supported.

Oil Jumps, Yen Wobbles, AUD Slides; Crosses Under Pressure

AUDUSD 0.7116 | NZDUSD 0.5876 | USDJPY 159.54 | GBPJPY 213.69

The global flight to safety severely battered Asia-Pacific assets. South Korea's KOSPI index plummeted 3.2%, Japan's Nikkei shed 1.4%, and the broad MSCI Asia-Pacific index fell 2.1%.

In the currency space, the Australian dollar fell toward 0.7116, approaching its major technical chart support at 0.7080, after weak domestic spending data and rising geopolitical tensions pressured sentiment.

Australian household spending dropped 1.1% in April as consumers cut back on travel, food, and clothing. Furthermore, reducing market expectations for further Reserve Bank of Australia (RBA) tightening. Markets now price almost no chance of a June RBA hike. Expectations for an August move also dropped sharply.

At the same time, New Zealand’s hawkish policy outlook lifted the kiwi. Investors now expect the Reserve Bank of New Zealand (RBNZ) to continue tightening, with rates potentially reaching 3% by year-end. This policy contrast triggered a massive unwinding of the nine-month uptrend in AUDNZD, sending the cross to a six-week low of 1.2072.

The Australian dollar also struggled against broader dollar strength and falling risk appetite as conflict headlines dominated trading.

Meanwhile, the Swiss franc softened as investors focused on the SNB’s intervention stance and safe-haven demand shifted toward the dollar.

In Tokyo, Bank of Japan Governor Kazuo Ueda warned that persistent oil shocks could prompt faster policy tightening, with markets pricing a 70% chance of a June rate hike to prevent a catastrophic breach of the 160.00 intervention line. The Greenback crept up to a four-week high against the yen at 159.54, aggressively testing the critical 160.00 psychological barrier. Tomorrow, inflation figures from Tokyo could give further insights into BoJ’s direction, and its influence on the yen and crosses.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3399 | Sideways |

| EUR/USD | 1.1614 | Mild bearish intraday |

| EUR/GBP | 0.8666 | Mild bullish |

| USD/JPY | 159.54 | Bullish (USD) |

| AUD/USD | 0.7116 | Bearish |

| NZD/USD | 0.5876 | Bullish |

| AUD/NZD | 1.2072 | Bearish |

| GBP/JPY | 213.69 | Sideways-bullish |

Market Lookahead

Thu, 28 May

- Eurozone Consumer Confidence

- Eurozone Business Climate

- US Core PCE Inflation

- US GDP Q1

- US Initial Jobless Claims

- ECB President Lagarde speaks

Fri, 29 May

- Tokyo CPI

- UK Nationwide House Prices

- Germany CPI and HICP

- Germany Import Price Index

- BoE Governor Bailey speech

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.