From Ceasefire to Blockade in 48 Hours: What the Islamabad Collapse Means for Your Currency Book

6 min read

Share

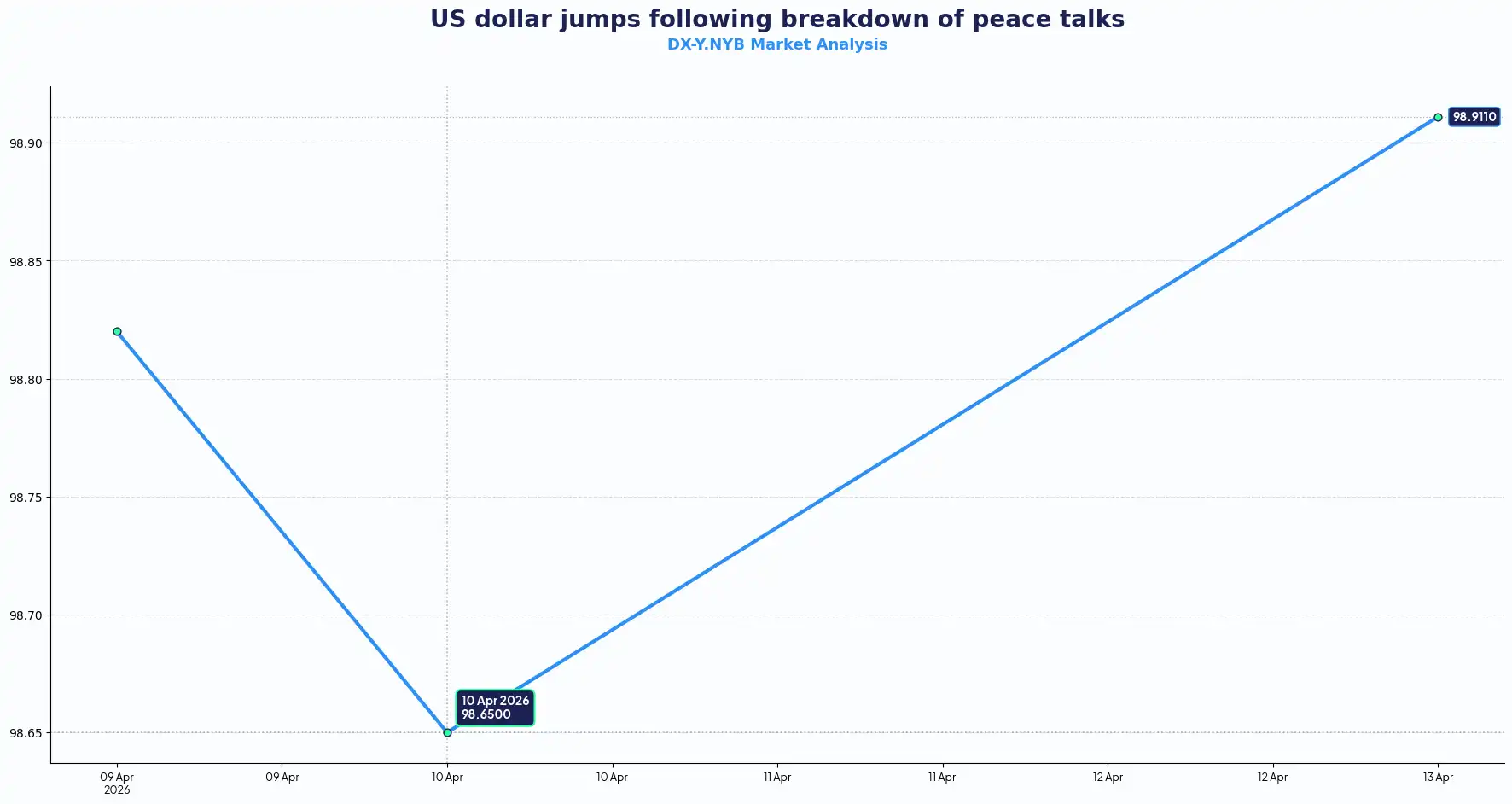

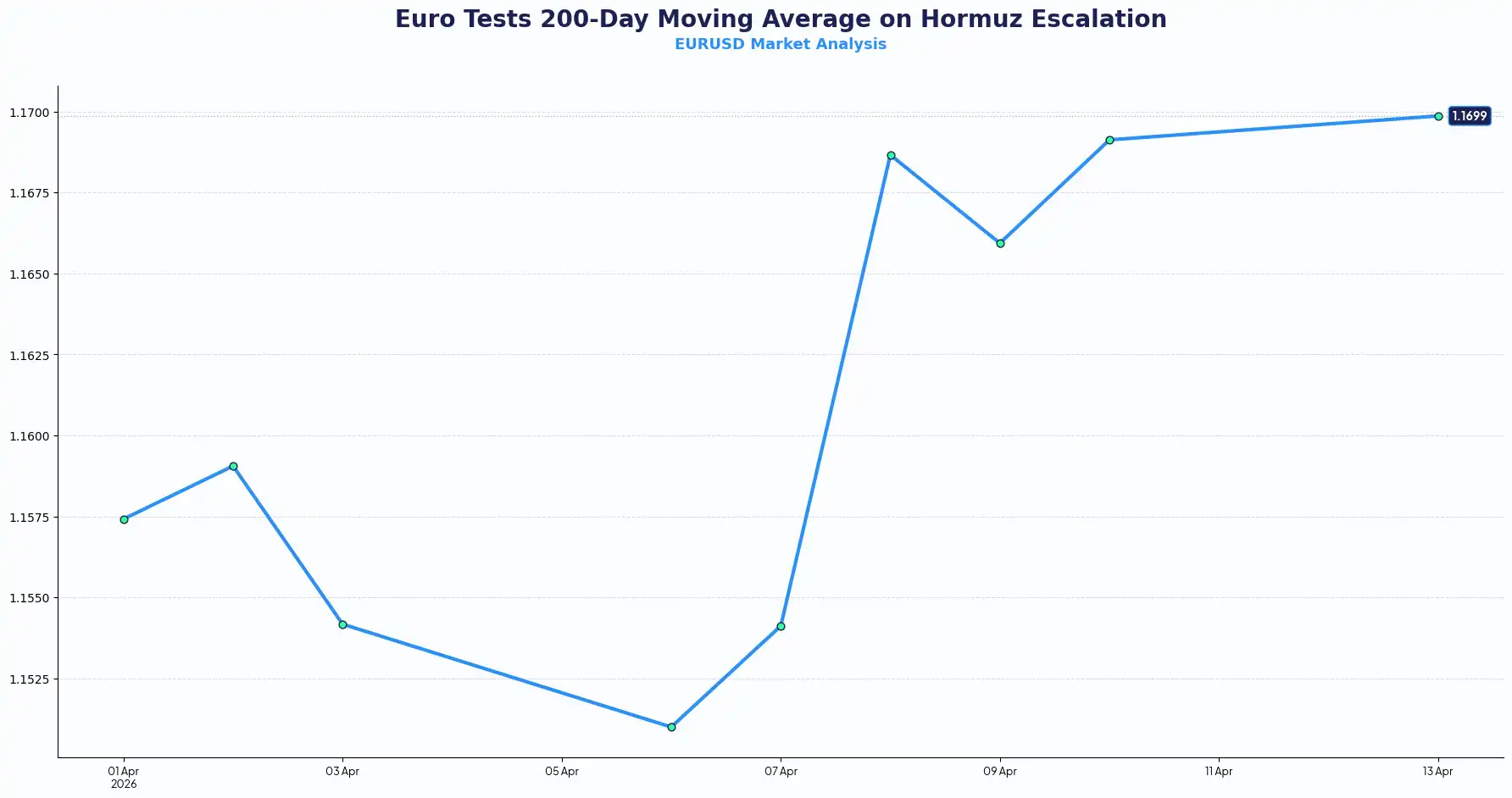

US-Iran peace talks collapsed in Islamabad on Sunday after 21 hours of negotiations, and President Trump announced a US Navy blockade of Iranian ports effective this morning. WTI crude surged to approximately $104-105 on the Asia open. The market reaction at the London open is firm but measured: GBP is at 1.3423, EUR/USD at 1.1699, AUD holding 0.7041, USD/JPY at 159.64, and DXY confirmed at 99.02. The moves are real but not panicked, which likely reflects the ceasefire technically remaining in force until April 22 alongside early positioning limits.

GBP

Sterling is at 1.3423 this morning, 46 pips below Friday's close of 1.3469. That is a contained move relative to the severity of the weekend headline, and the structure holds: the pair remains above the 1.3400 level that has attracted buyers on dips throughout the past two weeks. Support at 1.3350 has not been tested. The near-term picture stays constructive while it holds above that cluster.

The rate differential continues to provide the underlying floor. The BoE is priced for approximately 33 basis points of additional tightening by year-end, while CME FedWatch prices just 27.5% probability of any Fed cut before December. That gap is enough to keep sterling relatively bid against the euro, even in a risk-off session. GBP's relative outperformance versus EUR this morning is the differential playing out exactly as you would expect.

The constraint on sterling upside is the UK's net energy importer status. Oil above $100 is inflationary without any of the current account benefits that commodity exporters receive. CFTC data as of April 7 shows leveraged funds net long GBP at 55,779 contracts versus 29,246 short, supportive positioning that has not yet been forced to unwind. Bailey and Greene both speak this week ahead of the April 30 MPC. If Greene repeats her language on inflation persistence, that firms the rate story and provides a clearer floor. A close below 1.3400 today shifts the picture; a recovery above 1.3480 would suggest the weekend gap has been absorbed.

USD

DXY is holding at 99.02 (as at time of writing), essentially flat from Friday's close. The dollar has not surged on the Islamabad failure, which is the more interesting development this morning. The structural case for USD strength is intact: the US is a net energy exporter, WTI at $104-105 feeds through the current account favourably, and the Fed is frozen with 97.9% probability of a hold priced at the April 29-30 FOMC. All of that is true. The market is simply not chasing it aggressively yet.

Friday's CPI provided a genuinely split read. Headline at 3.3% year-on-year was driven almost entirely by a 21.2% monthly surge in gasoline. Core came in at 2.6%, 0.1 percentage points below consensus. Goldman Sachs flagged the Fed would likely look through the energy component. That interpretation appears to be holding this morning, with the dollar bid but not breaking out.

CFTC data shows asset managers recently flipped to net-short the USD index. That crowded short is sitting uncomfortably against both the Hormuz blockade and a structurally supportive current account position. The squeeze potential is there. PPI tomorrow is the next clean test: a firm number would tighten the stagflation narrative further and could push DXY through 99.40, the resistance that capped three of last week's four sessions.

EUR

EUR/USD is at 1.1699 this morning, approximately 26 pips below Friday's close and just above the 200-day simple moving average at roughly 1.1672. That moving average is the level this session. A daily close below it opens 1.1600-1.1620. The fact the pair is testing it so early in the session, before European data or ECB commentary, reflects euro-specific vulnerability rather than broad dollar strength.

The ECB is priced for roughly two 25 basis point hikes by year-end, which should in theory support EUR against a Fed on hold. The problem is the eurozone's energy import dependency. Oil at $100-plus is a direct terms-of-trade shock that weakens the current account and makes ECB hike expectations harder to sustain in practice. RBC Capital Markets has described EUR as functioning increasingly as a funding currency during energy shocks, and the data supports that: EUR is the weakest of the three major pairs this morning despite the smallest nominal pip move.

CFTC data shows asset managers holding 433,195 net long EUR contracts against 175,145 short. That crowded positioning creates asymmetric downside risk if 1.1672 breaks convincingly. We think the path of least resistance through this week is lower for EUR/USD unless the blockade de-escalates or ECB speakers signal a more aggressive hike path. If you have EUR payables due this month, the 200-day moving average is a natural decision point rather than something to ignore.

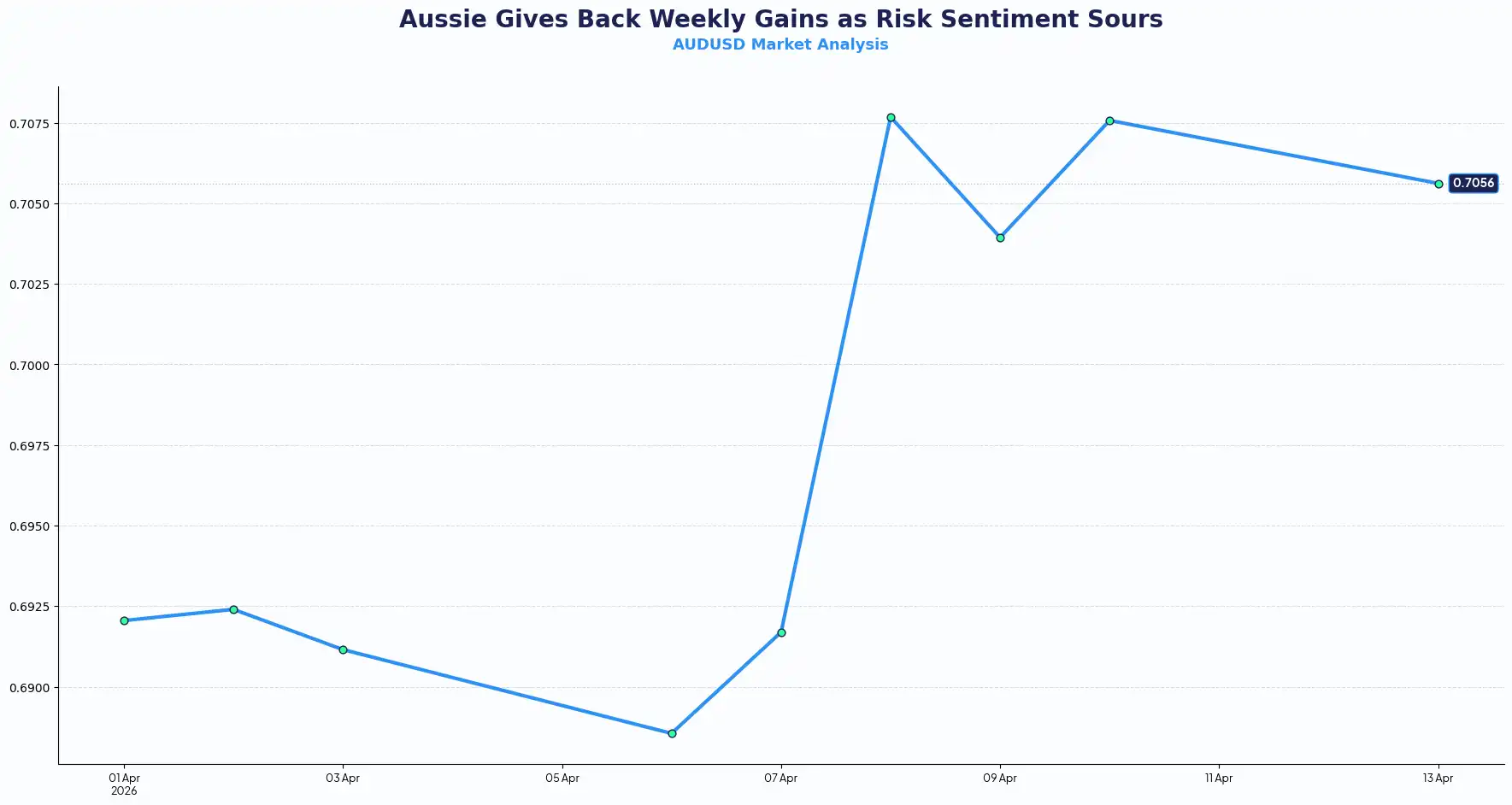

AUD

AUD/USD is at 0.7041 this morning, 22 pips below Friday's close of 0.7064. That is a notably contained move. A weekend that delivered failed peace talks, a confirmed US Navy blockade, and WTI surging to $104-105 would typically produce a far sharper sell-off in the highest-beta G10 currency. The relative resilience has a straightforward explanation: Australia is a net energy exporter, and oil at these levels is a terms-of-trade positive that is actively cushioning the downside.

The 0.7000 level has not been seriously threatened this morning. That matters because it is the level sell-side wave targets and options positioning cluster around. While the pair holds above it, the bias appears more range-bound than directionally bearish.

Thursday is the session that defines AUD's week. The RBA rate decision and China Q1 GDP land on the same day. A hawkish RBA hold or a China GDP beat would likely firm the pair toward 0.7100. A dovish surprise or a China miss reopens 0.7000 and potentially the 0.6900 area beyond it.

Market Snapshot

As at early London session, 13 April 2026

| Pair | Spot | Move vs Friday Close | Key Technical Level |

|---|---|---|---|

| GBP/USD | 1.3423 | -46 pips | 1.3400 support / 1.3480 resistance |

| EUR/USD | 1.1699 | -26 pips | 200-day SMA ~1.1672 |

| USD/JPY | 159.64 | +39 pips | 160.00 intervention level |

| AUD/USD | 0.7041 | -22 pips | 0.7000 support / 0.7100 resistance |

| DXY | 99.02 | Flat | 99.40 resistance / 98.98 support |

Week-Ahead Calendar

| Date | Event | Time (GMT) | Context |

|---|---|---|---|

| Tue 14 April | US PPI March 2026 | 13:30 | Key input for PCE deflator estimate; follows Friday's split CPI print |

| Tue 14 April | IMF World Economic Outlook | 14:00 | Watch for revised growth and inflation projections |

| Thu 17 April | RBA Rate Decision | ~03:30 | Live meeting; ~60% market pricing for May hike |

| Thu 17 April | China Q1 GDP | ~02:00 | Primary AUD and CNH catalyst |

| Thu 17 April | UK GDP, Eurozone CPI, Canada CPI | 07:00 / 10:00 / 12:30 | Heavy data day across G10 |

| Fri 18 April | Good Friday | All session | Reduced liquidity across European and some US markets |

All spot rates are indicative and subject to change. This briefing is for informational purposes only and does not constitute financial advice or a recommendation to transact. Currency Solutions is authorised and regulated by the Financial Conduct Authority.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.