ECB Warns, RBNZ Holds by One Vote as Oil Keeps Inflation in Play.

7 min read

Share

Iran's ceasefire violation claim stalls peace talks, Brent holds near $100. ECB's Lane flags an upward inflation revision for June. RBNZ holds OCR at 2.25% in a split vote; hike bets build, kiwi jumps. Gilt yields at a monthly low as BoE rate expectations scale back. Dollar flat, DXY at 99. Thursday brings US PCE and jobless claims data.

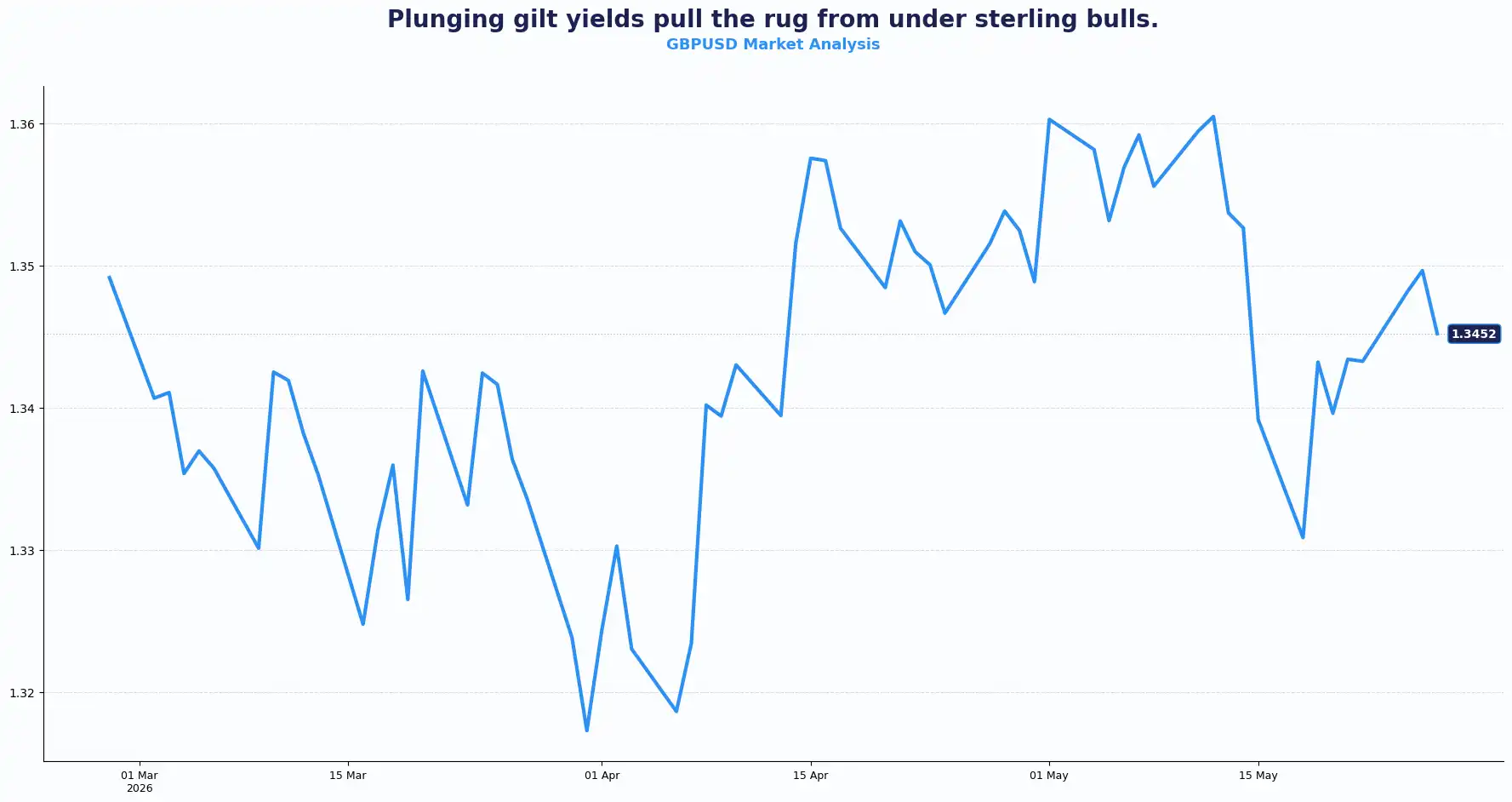

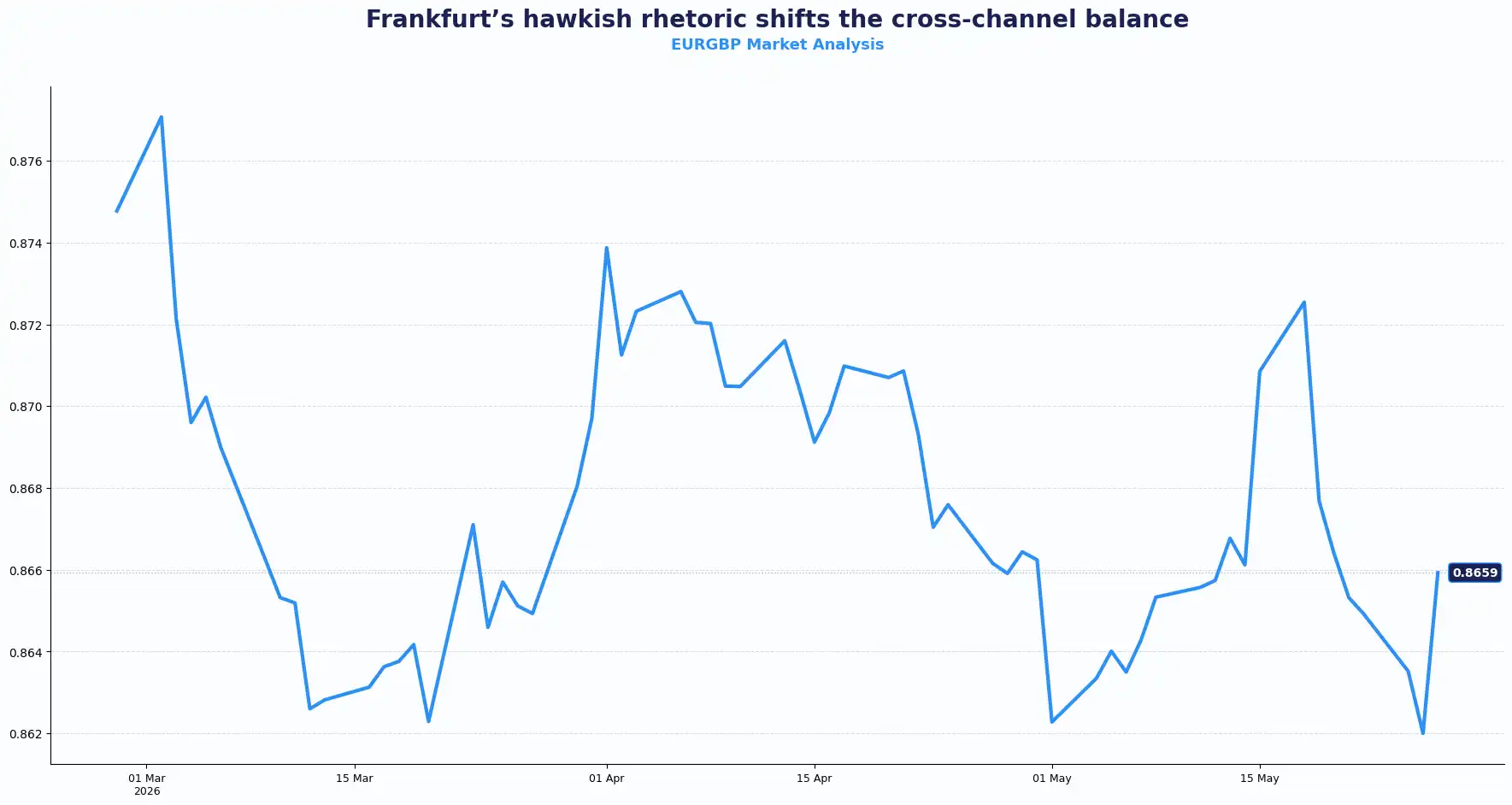

GBP: The Gilt Yield Trap

GBPUSD 1.3452 | EURGBP 0.8659

The GBP/USD pair trades near 1.3450 as two forces press on sterling simultaneously. The US-Iran ceasefire hangs unresolved. Secretary of State Rubio puts a deal "a few days" away, and Iran's foreign ministry called US strikes in Hormuz province a "gross violation" of the truce. Brent Crude holds near $100 per barrel through all of it. That kept demand intact for the dollar and weighed on risk appetite across FX.

The second and arguably more corrosive pressure is domestic. Ten-year UK gilt yields tumbled sharply to 4.82% on Tuesday, marking their steepest weekly contraction since late 2023. Sterling bulls failed to sustain the currency above its critical 20-day Exponential Moving Average (EMA), triggering technical liquidation.

This unwinding reflects a profound reassessment of the Bank of England (BoE) policy trajectory. Softer inflation data and an unexpected spike in the April unemployment rate to 5.0% have fundamentally altered institutional positioning. Traders now price in one full interest rate hike for 2026, compared with last week's forecasts.

This domestic economic cooling coincides with a significant reduction in domestic political risk premia. Odds indicating a replacement for Sir Keir Starmer have dropped, and Andy Burnham has explicitly committed to maintaining current fiscal rules. Consequently, domestic policy stability has driven yields lower, leaving the pound exposed as its interest-rate cushion erodes.

The ECB now sounds more determined to contain inflation, while the BoE faces slowing domestic momentum. That policy divergence pushed the EUR/GBP pair higher.

Friday brings the UK Nationwide House Price Index for May. Housing data could offer another signal on domestic demand and consumer resilience. If the numbers disappoint, Sterling may struggle to attract fresh support.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3520, 1.3575 and Support sits at 1.3400

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8685, Support sits at 0.8610

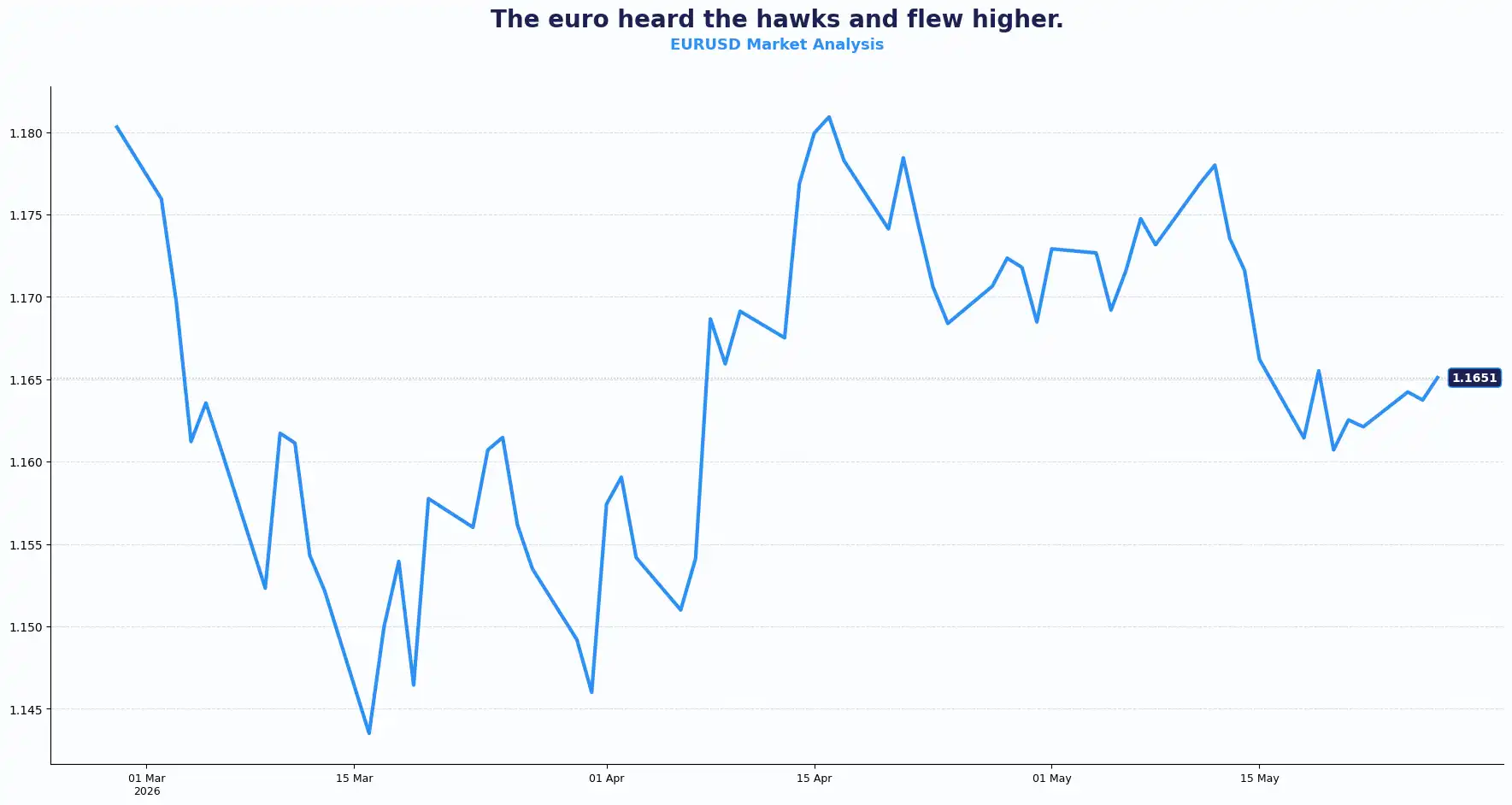

EUR: Euro Draws Strength From ECB Hawkishness

EURUSD 1.1651

The euro staged a disciplined advance in early trading, pushing the EUR/USD pair to $1.1651 and securing modest gains across cross-currency pairs. This upward movement occurred despite structural headwinds flowing from the Middle East. The euro is supported by a string of hawkish ECB signals that show no sign of softening.

ECB member Isabel Schnabel made the case for a June rate hike even in a scenario where a US-Iran deal gets across the line. Schnabel notes that the size and persistence of the current energy shock mean that looking through inflation is no longer an option. Even if peace talks yield a comprehensive geopolitical resolution, extensive physical damage to energy infrastructure dictates a monetary tightening response.

Governing Council member François Villeroy de Galhau reinforced the message, affirming that the central bank will do whatever is necessary to anchor long-term inflation targets.

While Chief Economist Philip Lane acknowledges that higher oil prices hit consumption and investment, he warns of significant secondary transmission effects across the wider consumption basket. The June inflation forecast gets an upward revision. The ECB's June decision framework now leans toward action, and the scale of that action depends on how persistent the oil price shock proves to be, a point Lane addressed directly.

Money markets have now fully priced in two hikes to the ECB’s 2% deposit rate, assigning a 50% probability to a third consecutive hike within the year. Economists are more conservative, pencilling in two hikes followed by a cut in mid-2027.

Tomorrow brings Eurozone Consumer Confidence and Business Climate data for May. Consensus expects consumer confidence to hold steady from the previous month. Business climate data, published by the European Commission, provides the most current read on cyclical conditions across the euro area: a rise in these figures points to improved activity, a fall in deterioration. Traders will watch closely for any signs that reflect if higher energy prices and geopolitical uncertainty are starting to hit sentiment and industrial activity harder.

Friday also brings Germany’s April Import Price Index. Stronger import prices could reinforce expectations for tighter ECB policy and keep the euro supported.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1700 and Support sits at 1.1580

USD: Flat Dollar, Open Questions. Iran and PCE in Focus

DXY 99.07

The US Dollar Index (DXY) maintained a tight, constructive consolidation at 99.07, defending its recent gains against major peers. Global equity capital found a temporary sanctuary in Wall Street's record-setting artificial intelligence (AI) rally. The Iran situation remains the dominant variable. Tehran seeks the release of $24 billion in frozen overseas funds as part of any deal. US strikes described by Washington as "defensive" drew a sharp rebuke from Iran's foreign ministry. Rubio's timeline of "a few days" gives the dollar little to work with in either direction; too much optimism is already baked into the price.

The Greenback’s structural dominance is supported by solid domestic data and a high core inflation floor. Ahead of the crucial Personal Consumption Expenditures (PCE) deflator release, consensus estimates project a hot 0.5% MoM reading for April. This would bring the year-on-year print to 3.8%, following a robust 4.5% quarter-on-quarter expansion in Q1.

Because the PCE deflator accounts for substitution effects, consumers switch between goods as prices shift, in a way that CPI does not. Sticky readings could strengthen the case for higher-for-longer Fed bank rates and keep the dollar supported across major pairs.

The domestic labour market shows persistent tight conditions. Initial jobless claims are projected at a modest 211k, leaving the underlying four-week moving average near historical lows. The four-week average, previously at 202.5k, provides the smoother signal on labour market conditions; a sustained rise there could carry more weight for the dollar direction than any single week's print.

Asia-Pacific: Records, Holds, and Supply Shocks

AUDUSD 0.7159 | NZDUSD 0.5876 | USDJPY 159.28 | GBPJPY 214.29

Japan's Nikkei jumped to a record, following Wall Street's AI-driven all-time highs during the US holiday week. The USD/JPY pair firmed slightly to 159.19 but remains structurally weak. Bank of Japan (BOJ’s) Governor Kazuo Ueda, speaking at a central bankers' meeting in Tokyo, flagged supply-side shocks as a growing concern, a signal worth watching given the BoJ's sensitivity to imported inflation through a weak currency.

The Reserve Bank of New Zealand (RBNZ) holds its key rate at 2.25% today, a decision the market had fully anticipated, leaving the NZD//USD pair subdued at 0.5876. The accompanying statement to the MPC decision and any forward guidance on the rate path might carry more weight for RBNZ rates. Australia's April CPI came in at 0.4% MoM and 4.2% YoY from the prior 4.6% and has impacted the movement in the AUD/USD pair. The pair holds firm at 0.7159.

Friday brings Tokyo CPI for May alongside Japan's April unemployment rate. Consensus has CPI ex-fresh food unchanged at 1.5% year-on-year. The RBNZ’s dramatic internal split demonstrates that inflation pressures are forcing even hesitant central banks toward higher terminal interest rates.

Current Rate Table:

| Pair | Spot | Trend |

|---|---|---|

| GBP/USD | 1.3452 | Bearish below 1.3500 |

| EUR/USD | 1.1651 | Bullish above 1.1600 |

| EUR/GBP | 0.8659 | Bullish |

| USD/JPY | 159.28 | Bullish |

| GBP/JPY | 214.29 | Volatile bullish |

| AUD/USD | 0.7159 | Neutral bullish |

| NZD/USD | 0.5876 | Neutral bearish |

Market Lookahead

Wed, 27 May

- US ADP Employment Change

- EU Financial Stability Review

Thu, 28 May

- Eurozone Consumer Confidence and Business Climate Data

- US Core PCE Price Index

- US Durable Goods Orders

- US Initial Jobless Claims

Fri, 29 May

- UK Nationwide House Price Index

- Germany Import Price Index

- Tokyo CPI and Japan Unemployment Data

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.