Central Banks in the Energy Trap, FX in the Middle

7 min read

Share

ECB expected to deliver first hike in eight meetings. US core CPI undershoots on the month, giving the Fed room to breathe. The ceasefire between the US and Iran shows signs of strain, with fresh strikes from both sides. BoE meets 18 June. Hike bets are building on energy shock, not growth. Next week's calendar is data-heavy for sterling.

GBP: The Gilt Market Is Doing the Talking

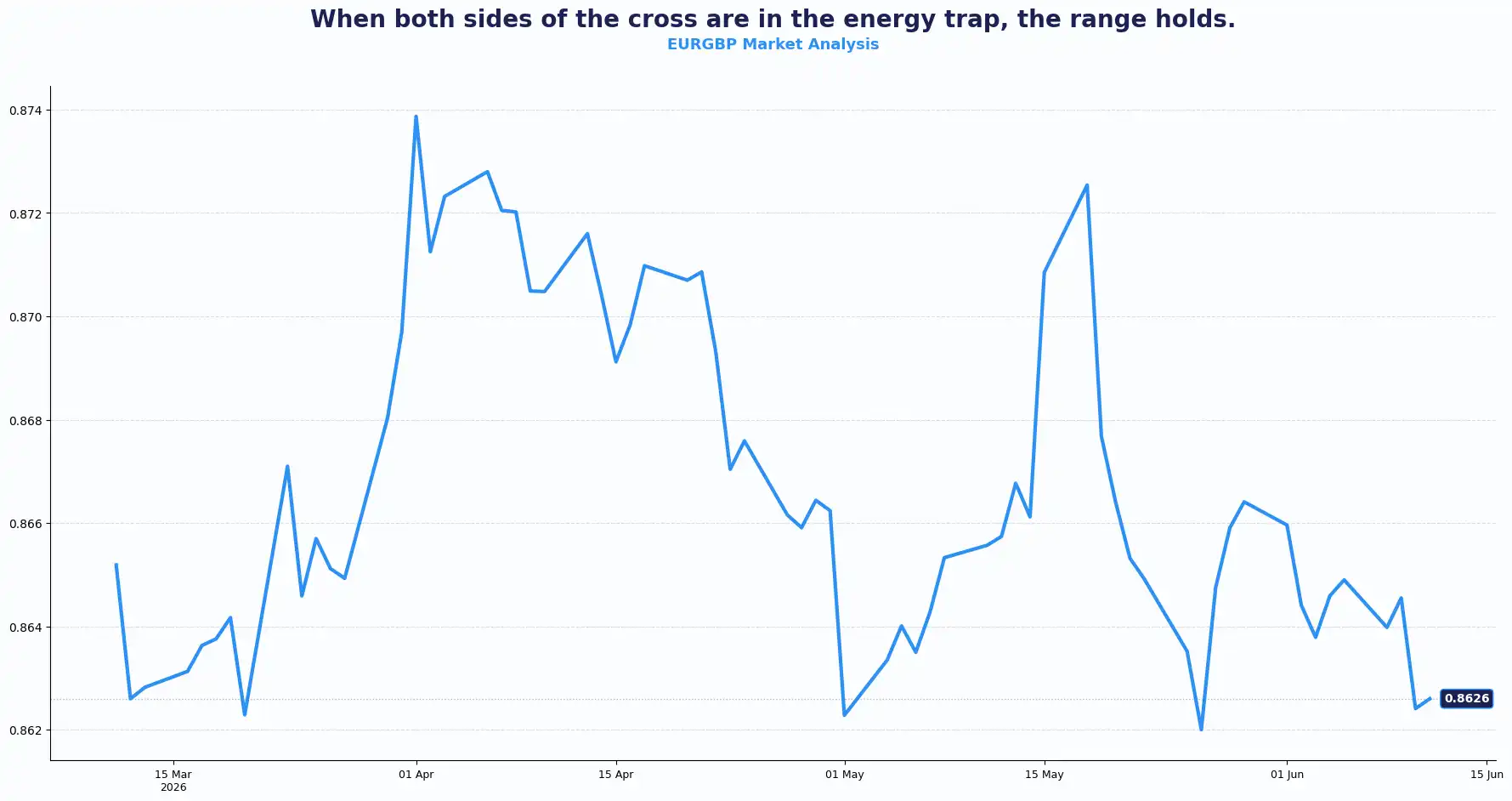

GBPUSD 1.3380 | EURGBP 0.8626

The GBP/USD pair trades at 1.3380, clinging to a narrow range ahead of Friday's UK GDP release. The pair has found modest support on broad dollar softness, but the ceiling sits firmly at 1.3400, and the week's data calendar is heavy enough to keep positioning tentative.

The energy shock leaves the Bank of England (BoE) with very few choices. Policymaker Alan Taylor confirmed earlier this week that current rates are already restrictive for the economy, and he sees no justification for hiking further to address energy-driven inflation. Governor Andrew Bailey echoed that view last week, describing the bank as in no rush to act. Rate-hike bets are building, but they are based on energy costs rather than economic expansion.

Friday's April GDP print is forecast at -0.1% MoM, a contraction, down from +0.3% previously. April industrial production is forecast to recover to +0.1% from -0.2%, offering limited offset.

That distinction is the crux of Sterling's predicament. A committee is edging toward hikes while output contracts do not project strength. It is reflecting that the energy shock has left it without good options. The gilt market seems to price that reality bluntly: 10-year gilt yields were much of May at or above 5%, a level last visited during the financial crisis. That is a risk premium and not a growth signal. It prices energy costs, a deteriorating fiscal arithmetic with every additional hike, and a political backdrop that has itself become a tradeable variable.

Next week, the UK CPI, the labour market report, and the BoE MPC decision are scheduled within two days. The MPC meeting falls on 18 June. Markets are pricing roughly a 90% chance of rates being held unchanged at that meeting, though traders are watching closely for any signals on the rate trajectory beyond June. Economic forecasters see the UK CPI climbing to 3.6% this year, up from the last print of 2.8%, with unemployment holding at 5% and payroll employment continuing to shrink.

The political dimension adds another layer. The Wigan by-election could return Greater Manchester Mayor, Andy Burnham, to Westminster as the governing Labour Party's candidate. If Burnham wins, it opens the possibility of a party leadership contest and renewed questions over UK fiscal direction. Technical analysis suggests sterling's holding pattern over the past two weeks reflects nothing decisive enough to break the range, but it's too risky to push it higher.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3450, 1.3400 and Support sits at 1.3330

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700, 0.8660 and Support sits at 0.8580

EUR: Will This One Be ECB's First Hike in Eight Meetings?

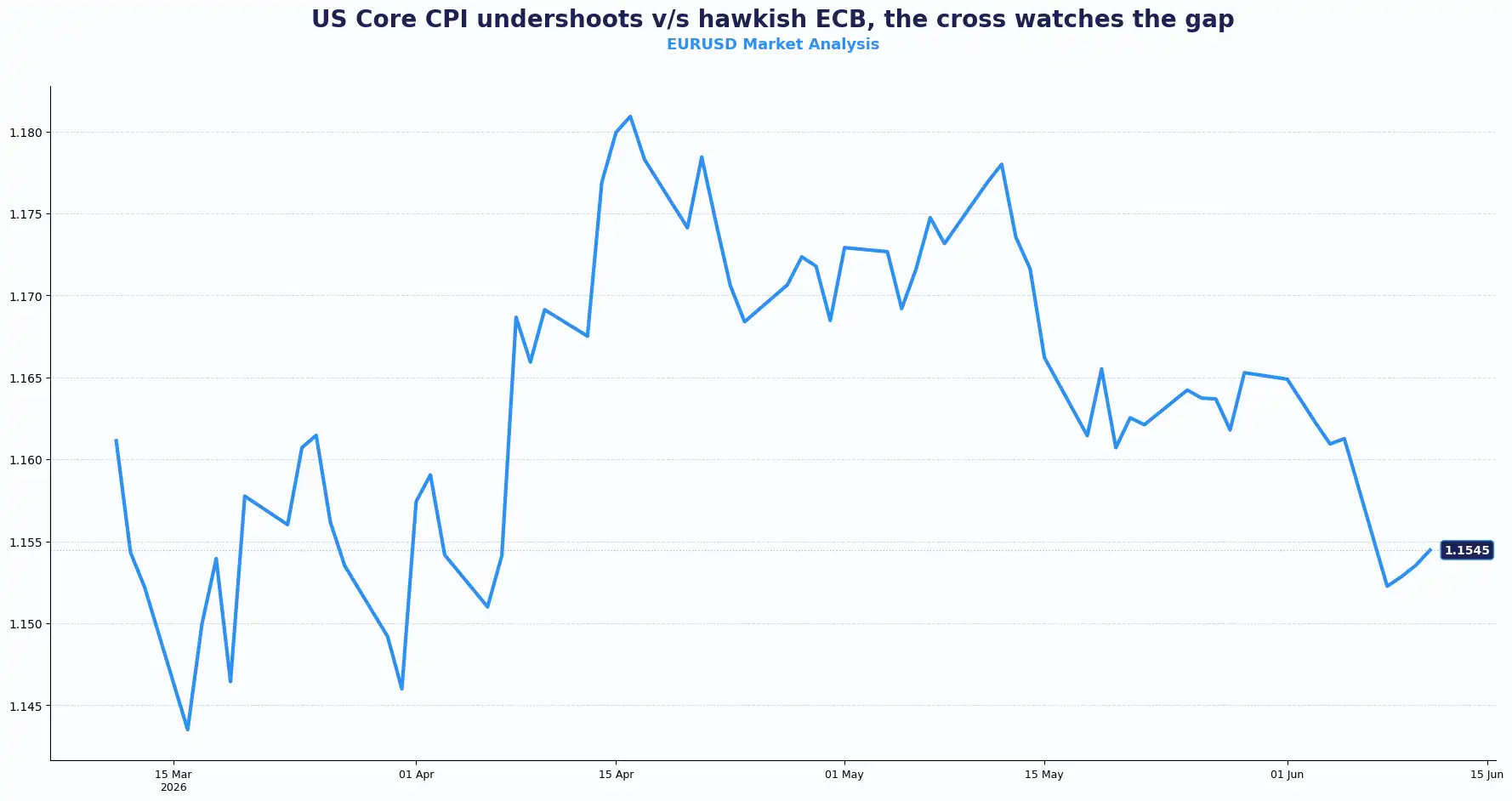

EURUSD 1.1545

The EUR/USD pair trades near 1.1545 ahead of the European Central Bank (ECB)'s policy announcement, following the Eurogroup meeting earlier in the session. The pair has edged higher through the morning, but 1.1500 could act as the near-term floor and 1.1520 as immediate support, with the upside dependent on how the ECB frames what follows today's decision.

Investors expect the ECB to raise its deposit facility rate by 25bps to 2.25%. If the ECB does hike, it will be its first rate adjustment after eight consecutive meetings with no rate change. A succession of ECB officials has pointed to the need for action, citing accelerating inflation driven by the ongoing energy supply crisis. Euro-area inflation already stands above 3%, beyond the ECB's 2% target.

Attention shifts to President Christine Lagarde's press conference, specifically to whether she signals second-round inflationary effects across the bloc. Markets anticipate that the ECB is unlikely to commit to a predetermined path of further hikes, yet given the financial conditions, markets already price more than three additional 25bps increases by March 2027. MPC’s Commentary that falls short of endorsing that trajectory could weigh on the euro through the afternoon session.

Growth is the complicating factor here. Economic expansion across the bloc is soft. Economists are divided on whether the tightening cycle is warranted in this environment, or whether the ECB is tightening into weakness. The answer to that question will shape the EUR/USD pair’s path through the summer more than any single rate decision alone.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1620, 1.1580 and Support sits at 1.1500, 1.1520

USD: Core Inflation Relief, Fed’s Room to Breath

DXY 99.94

The dollar holds at 99.94 on the DXY, recouping a portion of its early session losses as geopolitical risk reasserts itself. The ceasefire between the US and Iran, which is showing signs of strain, is the proximate driver of dollar demand amid the safe-haven bid.

US May CPI data delivered the headline the Fed could use to its advantage. Annual inflation printed at 4.2% as expected. Core CPI, stripping out food and energy, rose 0.2% MoM versus the 0.3% consensus, marginally softer and enough to give the Federal Reserve (Fed) some room to breathe in the near term. Year-on-year core held at 2.9%, in line with expectations.

The data, however, have not altered the direction of rate expectations. Pricing for a 25bps hike in December now stands at 43.7% probability, up from approximately 14% a month ago, per CME FedWatch. A combination of robust payrolls and sticky inflation has reinforced the Fed's higher-for-longer posture. Markets anticipate the Fed to hold through 2026, with the first cut not entering price discovery until 2027.

Today's US PPI report for May is the next test. Consensus sits at +0.7% MoM versus +1.4% previously, and +6.4 % YoY versus +6.0% previously. Core PPI ex-food and energy is expected at +0.5% MoM and +5.4% YoY. Fed Chair Kevin Warsh has taken the helm, and traders are calibrating his tolerance for above-target inflation amid elevated energy costs. A hotter-than-expected PPI could reinforce hike pricing and potentially give the dollar renewed momentum.

Israel's Home Front Command issued an early warning during the Asian session following launches from Lebanon toward northern Israel. The dollar showed no immediate directional move on the headline.

JPY: Governor Ueda Hospitalised, Intervention Levels in View

USDJPY 160.52 | GBPJPY 214.83

The USD/JPY pair trades at 160.52, approaching ¥160.70, the level at which Japanese authorities entered the market on 30 April, deploying tens of billions of dollars to arrest the yen's slide. That intervention briefly pushed the pair from near ¥161 to around ¥155 before price action retraced.

BoJ Governor Kazuo Ueda has been hospitalised since 9 June for approximately two weeks of medical treatment, working remotely, and confirmed to attend the 30-31 July policy meeting. The absence introduces an additional layer of uncertainty around near-term BoJ communication. The BoJ's cautious approach to rate normalisation continues to weigh on the yen. With US rates elevated and December hike probability rising, yield-seeking flows continue favouring dollar-denominated assets. The GBP/JPY pair trades at 214.83, reflecting the cumulative carry differential.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3380 | Sideways/cautious |

| EUR/USD | 1.1545 | Mild upside bias |

| EUR/GBP | 0.8626 | Range-bound |

| USD/JPY | 160.52 | Upside bias |

| AUD/USD | 0.7009 | Neutral |

| NZD/USD | 0.5795 | Neutral |

| GBP/JPY | 214.83 | Upside |

Market Lookahead

Thurs, 11 June

- ECB Interest Rate Decision

- ECB Press Conferences

- US Producer Price Index (May)

- US Initial Jobless Claims

Fri, 12 June

- UK GDP

- UK Industrial Production

- Germany HICP Inflation

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.