Trump Tariffs Stir the FX Cauldron

7 min read

Share

Sterling falters on dovish BoE signals and a bruising by-election. The euro holds its range ahead of Wednesday's CPI. The dollar claws back lost ground as Trump rewrites tariff rules mid-game. Asian markets are steady, barely.

GBP: Sterling Stumbles Under Political Shadow

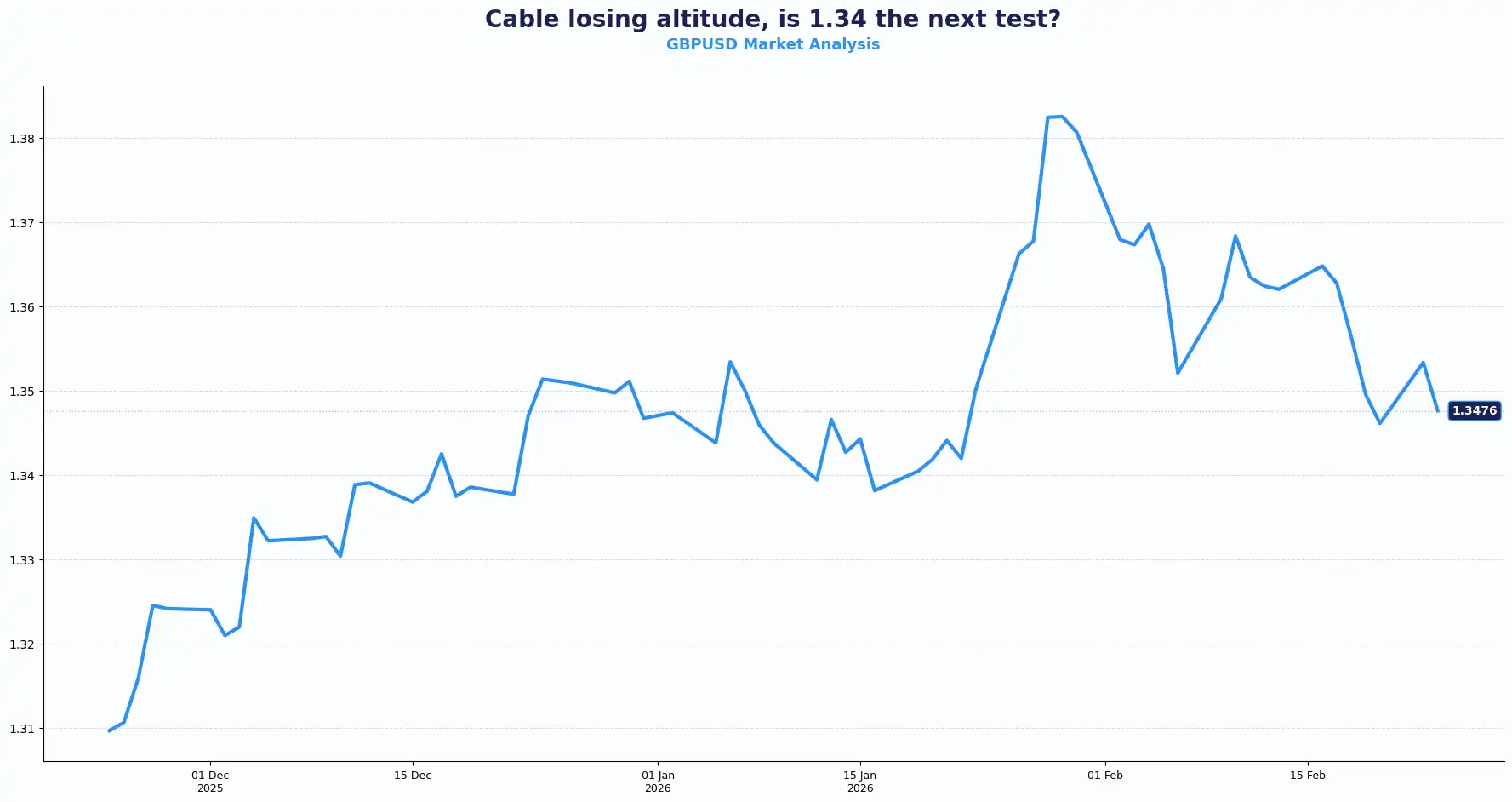

Sterling started the week on a firm footing but soon slipped against the dollar. Cable is trading at 1.3481, down from its previous close of 1.3492. Not a dramatic sell-off, but the direction tells the story.

Sterling lost ground against the dollar as three forces converged: a Bank of England (BoE) that sounds increasingly inclined to cut, fresh tariff uncertainty from Washington, and a by-election on Thursday that could shake Keir Starmer's grip on Labour leadership.

BoE policymaker Alan Taylor said it plainly, “two or three more cuts stand between now and a neutral rate”. That comment sharpened expectations for policy easing across the curve. Poor employment data and cooling inflation support the case for a March cut. Traders now price a 75% chance of a 25bps reduction, eroding the pound's yield advantage. Since the BoE held its hand earlier this month, the upcoming appearance of Governor Andrew Bailey before the Treasury Committee carries immense weight for the pound’s trajectory. His tone could either steady sterling or reinforce the dovish narrative building beneath the surface.

Trade policy adds another layer. The U.S. Supreme Court struck down the previous tariff framework, only for President Trump to announce a new 15% levy on all imports. This sudden shift from a 10% baseline injects fresh volatility into the British currency. While the full economic impact is still unclear, renewed tariff friction tends to weigh on trade-sensitive currencies such as sterling.

The political backdrop sharpens the risk. Thursday's Gorton and Denton constituency by-election reads as a verdict on Starmer's leadership. Polymarket now prices the probability of him leaving office by year-end at 63% (up 12%this month). Allegations that UK Ambassador to Washington Peter Mandelson once leaked government information to Jeffrey Epstein (which Mandelson denies) have given opposition rivals ammunition at a moment when the government can ill afford it. A heavy Labour defeat could revive leadership speculation and typically, sterling does not thrive in political vacuums.

Dovish BoE trajectory plus political noise is a familiar recipe for sterling softness. Periods like this often coincide with higher FX volatility and shifting corporate risk profiles. Bailey's testimony and Thursday's result are the week's two pressure points for the GBP/USD pair.

Key Technical Levels for GBP/USD: Resistance sits at 1.3520, 1.3585 and Support at 1.3440, 1.3390

EUR: Euro Stagnates Despite German Data Beat

The German IFO Business Climate Index rose to 88.6 in February, surpassing the expected 88.4. However, the euro failed to take flight. EUR/GBP trades sideways at 0.8730, unable to break the multi-month resistance near 0.8750. Against the greenback, the euro slid to $1.1769 as the European Parliament postponed a vote on the EU-US trade deal, citing the disruption from the new US import levy.

The euro's relative calm is a product of enforced patience. Two high-impact data releases land on Wednesday: the Eurozone flash CPI estimate, where core HICP is forecast to ease to 2.2% YoY from 2.3% and the headline HICP is expected to hold at 1.7%. German Q4 GDP preliminary data arrives on the same day. Preliminary inflation prints from France and Spain are scheduled for later in the week.

These numbers will either validate or complicate the consensus view that the European Central Bank (ECB) holds rates through the year. An upside CPI surprise would test that assumption fast. A softer reading gives the ECB room to do nothing, which is exactly what it’s indicating: the ECB continuing to hold its rate steady.

The EUR/GBP structure tells its own story of policy divergence. The ECB appears content to wait, while the BoE leans towards rate cuts; that spread gives the cross a floor. However, repeated rejections at the 0.8750 level confirm the ceiling is holding for now. Until Wednesday's data shifts the ECB narrative, the cross has no obvious catalyst to break the range.

For the EUR/USD pair, the divergence between a stagnant European trade outlook and a resilient US dollar keeps the euro pinned against the ropes. The 61.8% Fibonacci support level at 1.1775 is currently the only thing preventing a deeper slide. The trade deal delay suggests the Eurozone anticipates a prolonged scuffle with Washington, dampening growth prospects for the bloc.

Key Technical Levels for EUR/GBP Resistance sits at 0.8750, 0.8780 and Support at 0.8700, 0.8660

Key Technical Levels for EUR/USD Resistance sits at 1.1850, 1.1920 and Support at 1.1775 (61.8% Fibonacci), 1.1720

USD: The Dollar Claws Back as Trump Defies the Court

The dollar index rallied 0.2% to 97.90. The greenback recovered all intraday losses. Trump warned trade partners against "playing games." After the Supreme Court struck down emergency tariffs, Trump invoked a different 1977 law to slap a 15% levy on all imports. This move caught the world off guard, creating a frantic environment for global trade desks. This "Art of the Deal" 2.0 approach fuels inflation fears, which in turn keep US Treasury yields at 4.04%.

The trade landscape looks fractured. The Fed itself is watching. Fed Governor Christopher Waller signals a willingness to hold rates in March if February jobs data shows a solid footing. Since higher tariffs often fuel inflation, the Fed may delay cuts until June or later. Higher for longer is back on the menu. CME FedWatch puts the probability of a March hold at 95.5% but the tariff cloud sits directly above the fundamental picture.

Two competing narratives are running in parallel. The first: more tariffs push US inflation higher, reduce the odds of Fed cuts, and support the dollar through rate differentials. The second: escalating uncertainty and overreach accelerate de-dollarisation trends, which are structurally negative for the currency over the medium term. Both arguments have data behind them. Neither is settled. That ambiguity is the dominant condition for the dollar right now.

Tonight's State of the Union address is expected to set a combative tone. The justices will be seated in the chamber as Trump speaks. That particular optic is unlikely to reduce market uncertainty.

The Trump administration is also weighing national security tariffs on large-scale batteries, cast iron fittings, plastic piping, industrial chemicals and power grid and telecoms equipment. The scope of potential trade restrictions keeps widening.

Geopolitical risk adds a further layer. The State Department has pulled non-essential personnel from the US embassy in Beirut amid tensions with Iran. A military escalation in the region would historically lift the dollar against most currencies with the yen and franc as exceptions, given their safe-haven characteristics.

The combination of fiscal aggression and a hawkish Fed creates a strong floor for the currency. The dollar currently benefits from rate stability and yield support, yet the broader FX backdrop stays reactive as tariff policy continues to evolve.

Asia-Pacific: The Trade Tangle Deepens

USD/JPY rose to 155.26 while the Aussie dollar held firm at $0.706.

A fresh "trade tangle" erupted as China prohibited exports of dual-use items to 20 Japanese entities. Meanwhile, Japan’s trade minister, Ryosei Akazawa, is pleading for "favourable treatment" under the new US regime. The yen is fragile despite reports of US-led "rate checks" to support the currency.

In contrast, the Australian dollar finds support ahead of Wednesday's CPI data, with markets eyeing a 3.7% inflation print.

Geopolitical friction in the East adds a layer of complexity to the G10 space. Whether it is Yen intervention or Aussie inflation surprises, the macro landscape is shifting beneath our feet.

The macro thread connecting all of the above: Trump's tariff reset has not resolved uncertainty; it has relocated it. Every central bank, every trade negotiator, and every FX participant is now repricing against a 15% blanket floor that may itself be temporary. Wednesday's Eurozone data and tonight's State of the Union are the next two inflection points.

Current Rate Table

| Pair | Level | Trend |

|---|---|---|

| GBP/USD | 1.3481 | Soft |

| EUR/GBP | 0.8730 | Flat |

| EUR/USD | 1.1769 | Weak |

| USD/JPY | 155.26 | Strong |

| AUD/USD | 0.7060 | Firm |

| DXY Index | 97.90 | Bullish |

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.