Sterling Leads as Tariff Shock Hits Dollar

7 min read

Share

The US Supreme Court just dismantled Trump’s tariff empire, sparking a global reset in currency markets. As the dollar’s haven wavers; the sterling and the euro rise amidst a sea of fiscal volatility.

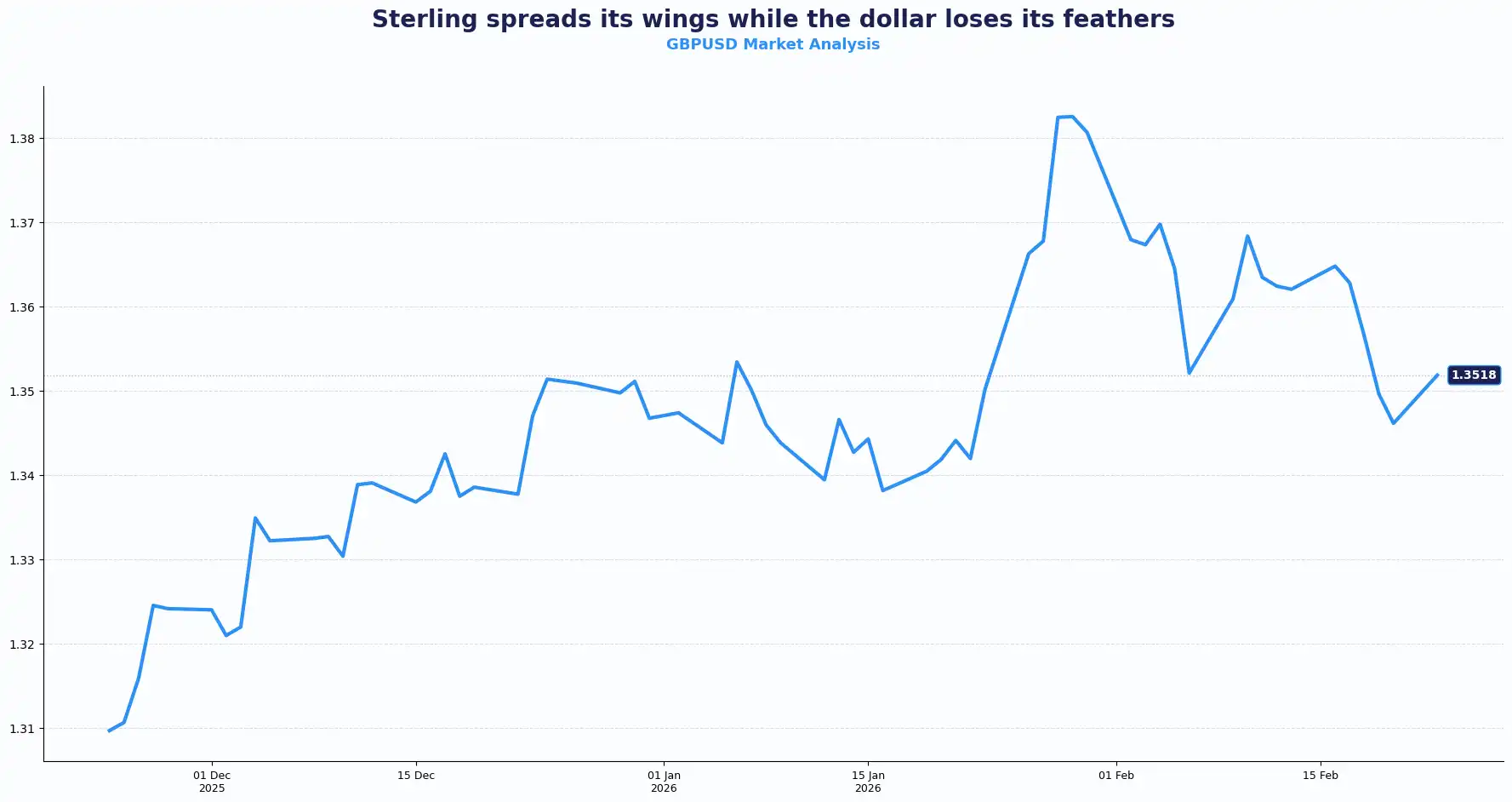

GBP: Sterling Reigns Supreme; Cable Reclaims the 1.35

Sterling surged above $1.3500 on Monday, after touching a one-month low. GBP/USD trades near 1.3520, up from 1.3478. This recovery follows the US Supreme Court’s decision to strike down President Trump’s emergency tariffs. While the dollar nursed its wounds, the pound capitalised on a "double-top" of bullish news: explosive UK economic data and a sudden vacuum in American trade policy.

Structure dictates the flow. The latest UK PMI confirms that private-sector activity is at its fastest pace since April 2024. The UK's Manufacturing and services sectors are sprinting. Combine this with a 1.8% jump in retail sales, and you see a UK economy far more resilient than the grim forecasts suggested. While the Bank of England’s (BoE) Alan Taylor speaks today, the market is already sensing a policy divergence. The UK is firming up just as US trade certainty dissolves.

Speeches today from BoE’s Alan Taylor and Federal Reserve (Fed) Governor Christopher Waller could shape rate narratives.

Still, tariff policy volatility in Washington injects two-way risk into GBP/USD. Rate expectations across the Atlantic continue to drive direction. Periods of policy uncertainty often coincide with increased FX volatility. Recent price action shows how quickly GBP/USD can reprice when macro signals shift.

The current climb above 1.3500 suggests a shift in momentum that rewards the decisive. Traders are watching the 1.3520 level closely; sustaining this height changes the narrative for the quarter.

Key technical levels for Cable (GBP/USD): Resistance sits at 1.3550, 1.3630, 1.3749 & Support: 1.3500, 1.3474, 1.3421

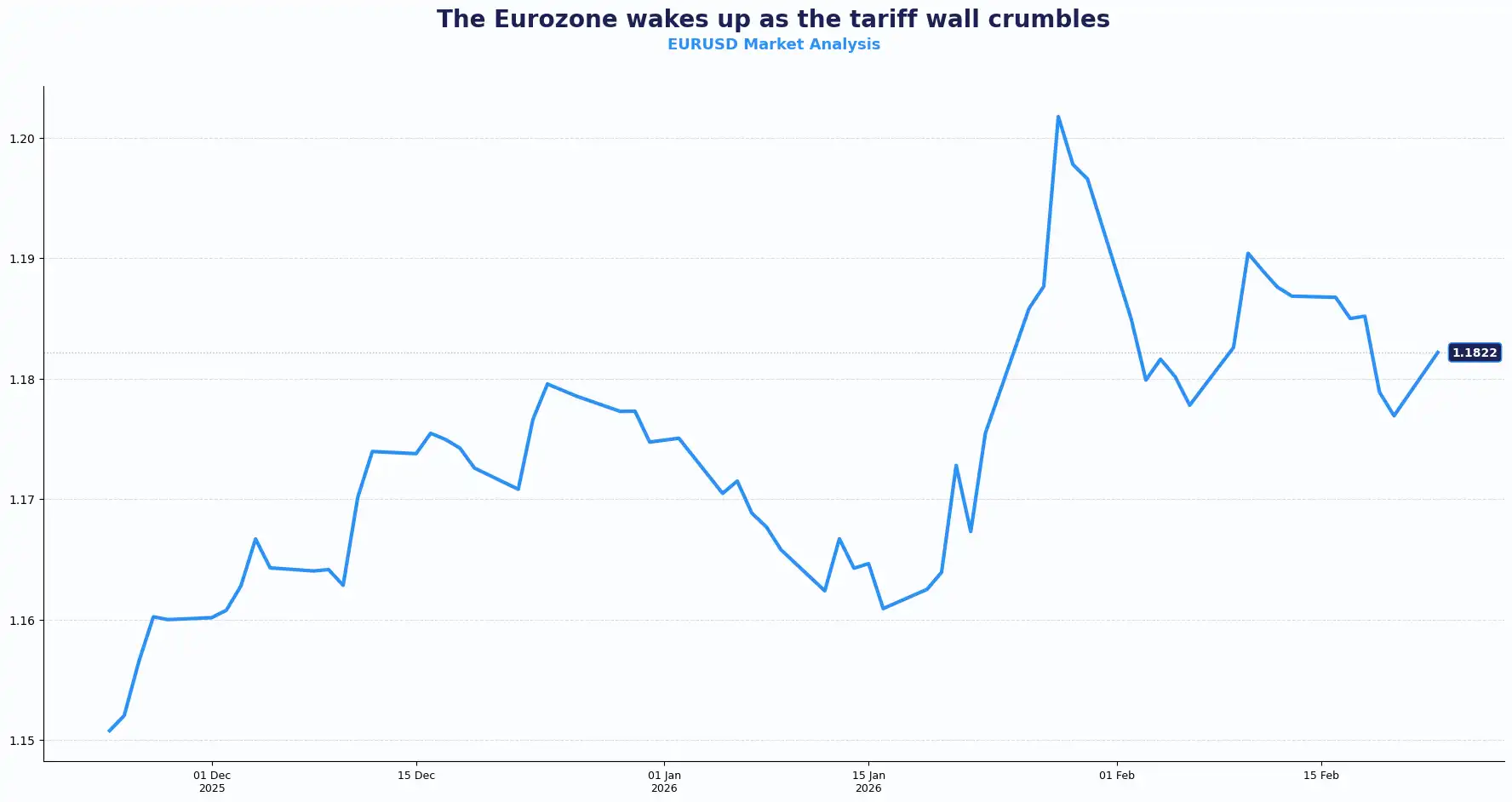

EUR: Euro Pushes Forward, But Sterling Holds the Room

The euro rose to $1.1820, up 0.37%, riding the wave of relief following the tariff ruling. Against sterling, the story was less flattering. EUR/GBP stabilised near 0.8742 as both currencies exhibited competitive strength. UK retail sales and PMI data simply outpaced the Eurozone's own strong showing. The pound absorbed both data sets and came out ahead.

European equities hit record highs, marking their most significant weekly jump since January. The market has spoken: the removal of "emergency" trade barriers acts as a massive shot of adrenaline for the Eurozone.

The "why" is rooted in a manufacturing resurrection. For the first time since October, the sector swung back into growth. Although the services sector marginally lagged, overall Eurozone activity accelerated past all major forecasts. The European Commission is already playing hardball, demanding the US honour existing zero-tariff deals on items including aircraft and spare parts, signalling that Brussels is not treating Trump's replacement levies as settled.This assertiveness, backed by improving PMIs, shifts the euro from a passive observer to a proactive contender.

Today's German Ifo Business Climate survey for February lands with a consensus forecast of 88.4, up from January's 87.6. A print above 88.4 signals that Germany's industrial base is turning which feeds directly into eurozone growth projections. A beat supports the euro across its pairs. A miss reopens the structural conversation about German drag on the broader eurozone recovery.

Lagarde Speaks, But for How Long?

ECB President Christine Lagarde addresses today and what she says carries weight beyond the usual policy commentary. Reports emerged last week that Lagarde intends to step down from the ECB ahead of her October 2027 term. Inside the ECB, staff are reportedly in shock, confused and uncertain about her authority in the interim. That is not a comfortable backdrop for a central bank that prides itself on institutional credibility.

The stated rationale is political timing: Lagarde wants to exit before the French presidential election in April 2027, which would allow both President Macron and German Chancellor Merz to jointly select her replacement. Current frontrunners for the role include Klaas Knot, the former Dutch central bank chief, and Pablo Hernández de Cos of Spain, with Knot viewed as the "Goldilocks" candidate: hawkish enough for Berlin, experienced enough for the Governing Council.

Today's speech carries a dual reading. On policy, participants will listen for any shift in tone. On institutional confidence, any hesitation or ambiguity from Lagarde feeds directly into euro volatility. A lame-duck central bank president is not a comfortable narrative for a currency trading near its strongest levels against the dollar.

For EUR/USD, the picture is a race between two central bank paths. The Fed is expected to ease toward 3.25% through 2026. The ECB is parked at 2.00%. The rate differential currently favours the euro but only if European growth holds up and the ECB does not blink first on rate cuts. A strong German IFO today keeps that story intact. A weak one starts to chip at it.

The "Sell America" meme has gained traction, and the euro is the primary beneficiary. ECB communication and German data often shift rate expectations quickly. EUR/USD continues to respond to changes in perceived policy paths on both sides of the Atlantic.

Technical Levels for EUR/USD Resistance sit at 1.1850, 1.1918, 1.2020 & Support: 1.1775, 1.1746, 1.1615

USD: The Dollar, the Court, and the Chaos That Followed

The dollar index (DXY) slipped to 97.40, ending a four-session winning streak with a definitive thud. The Supreme Court effectively ruled that the President broke the law for nearly a year by overstepping his authority. Trump’s immediate retaliation of a blanket 15% global tariff effective Tuesday has only deepened the confusion. In the East, the Yen strengthened toward 154 as traders sought sanctuary from the unfolding dollar uncertainty.

Markets are witnessing a fiscal identity crisis. Trump’s new 15% levy, enacted under a different bill, lasts only 150 days and creates a nightmare of "undiscriminated" trade. This includes everyone from the UK to North Korea. US Treasury Secretary Bessent’s threats of self-imposed embargoes suggest an administration willing to blockade its own ports to prove a point. From a macro lens, the lack of a ruling on $170 billion in potential tariff refunds leaves a massive hole in US finances. The dollar is falling because the market hates a king who loses his court.

Some countries, including the UK and Australia, now face higher rates under the 15% structure. Others, including China, could see lower effective rates. India has paused its trade deal with the US. The European Commission has ruled out changes on its side.

The short-term read is that cleaner tariffs mean lower near-term inflation and a faster path to Fed rate cuts. The ruling reflects a checks-and-balances moment that reduces some risk premium on US assets. The longer view is murkier. The fiscal gap that the tariff revenue was meant to bridge still exists. The administration's spending propensity has not changed. Bond participants are closely tracking fiscal discipline closely and the steepening yield curve reflects that concern directly.

The dollar's status as a reliable haven is under interrogation. With US GDP growth missing the mark and the fiscal deficit spiralling out of control, the "greenback exceptionalism" of 2025 has evaporated.

Episodes of policy uncertainty often coincide with repricing across FX and rates. The latest developments highlight how quickly dollar sentiment can change when fiscal and trade narratives shift.

Yen Finds Support Amid Tariff Talks

USD/JPY trades near 154.25 while GBP/JPY sits around 208.77. The yen strengthens as the dollar softens.

In Tokyo, Prime Minister Sanae Takaichi outlined a “responsible and proactive” fiscal strategy after earlier spending plans unsettled investors. Trading volumes stay light due to a Japanese public holiday.

Safe-haven flows return to the yen during periods of US policy volatility. Domestic fiscal reassurance from Tokyo also helps stabilise sentiment. However, rate differentials with the US still cap aggressive yen strength.

Haven currencies often react first when global policy uncertainty rises. Recent yen moves reflect that pattern.

Market look ahead:

Monday, 23 February

Focus turns to speeches from Christine Lagarde, Alan Taylor and Christopher Waller. Traders also watch the German Ifo survey and US factory orders for fresh macro direction.

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.