War, Oil and the Dollar Upend FX on Monday

7 min read

Share

Global volatility surges and ignites safe-haven demand across the currency landscape. US-Israel strikes kill Iran's Supreme Leader, sending oil up 9% and the dollar surging. Sterling and the euro slide. Safe havens dominate. Inflation risk returns to centre stage.

GBP: Sterling Slips as War Nerves Override Pill

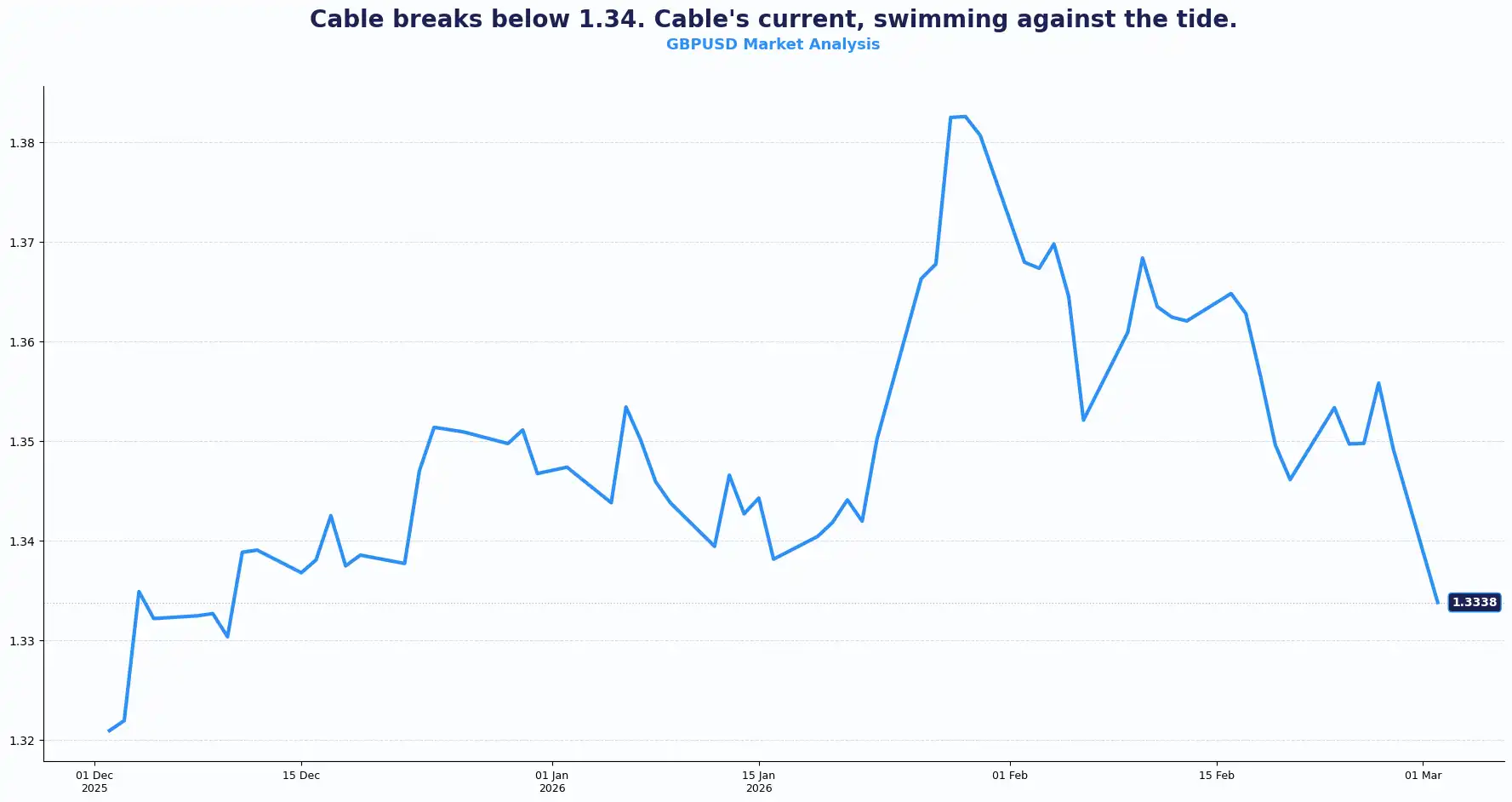

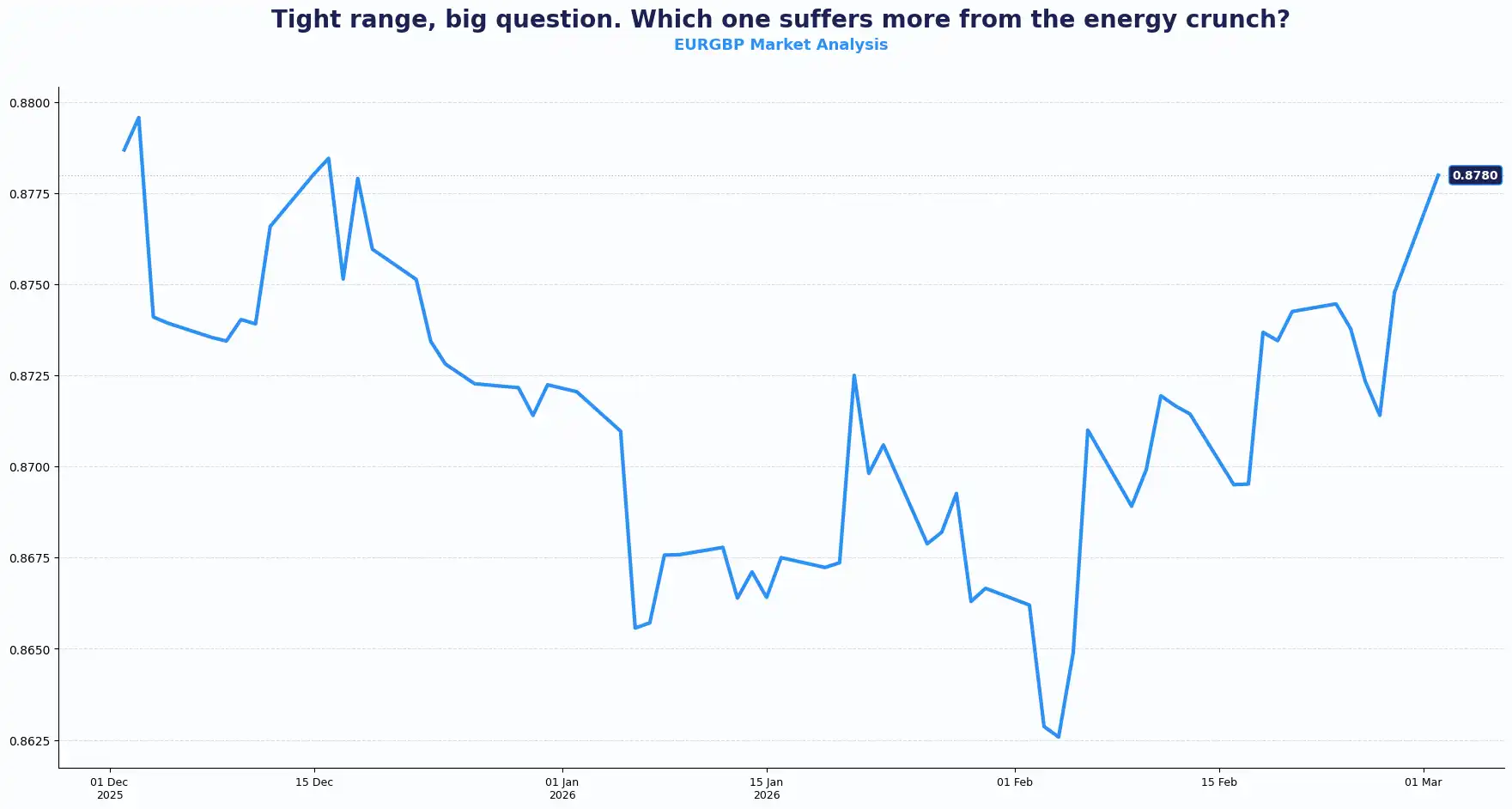

Sterling fell against its major peers on Monday. The GBP/USD pair slipped through the 1.34 support level, dropping 0.81% to 1.3377. EUR/GBP held at 0.8771, up 0.10%, as the euro absorbed its own pressures. The British currency faced selling pressure as the shockwaves from the Middle East reached the City. Only the antipodean currencies fared worse than the pound.

Domestic hurdles compound the geopolitical weight. The Bank of England (BoE) Chief Economist Huw Pill told Parliament's Treasury Committee on Friday that the disinflationary trend has been slower than anticipated. He flagged that the BoE placed too much emphasis on inflation sitting near the target, rather than looking ahead. That warning signals building upside inflation risks. The hawkish lean offered sterling some structural support against the euro but did nothing against a strengthening dollar.

Last Thursday's Manchester local election handed the Green Party a notable win and dealt the Labour Party another blow. Prime Minister Keir Starmer's approval has slid over the past year. Sterling absorbs domestic political noise with relative calm, but this week the focus shifts to Chancellor Rachel Reeves's budget update. Usually, budget updates anchor the pound; however, the current global chaos is likely to override local fiscal narratives.

Current price action highlights how quickly sentiment shifts from domestic policy to global risk. Sterling now trades at the intersection of geopolitics, sticky inflation and fiscal scrutiny. Volatility has picked up. Price action reflects shifting expectations around growth and policy.

UK consumer credit printed £1.524bn last month. Strong borrowing can signal demand strength, but it can also flag strain.

S&P Global Manufacturing PMI is likely to hold at 52. A print above 50 signals expansion. Manufacturing keeps its head above water, but energy costs could test margins.

Key technical levels for GBP/USD: Resistance sits at 1.3450, 1.3520 and Support at 1.3300, 1.3220.

Key technical levels for EUR/GBP: Resistance sits at 0.8800, 0.8850 and Support at 0.8720, 0.8650

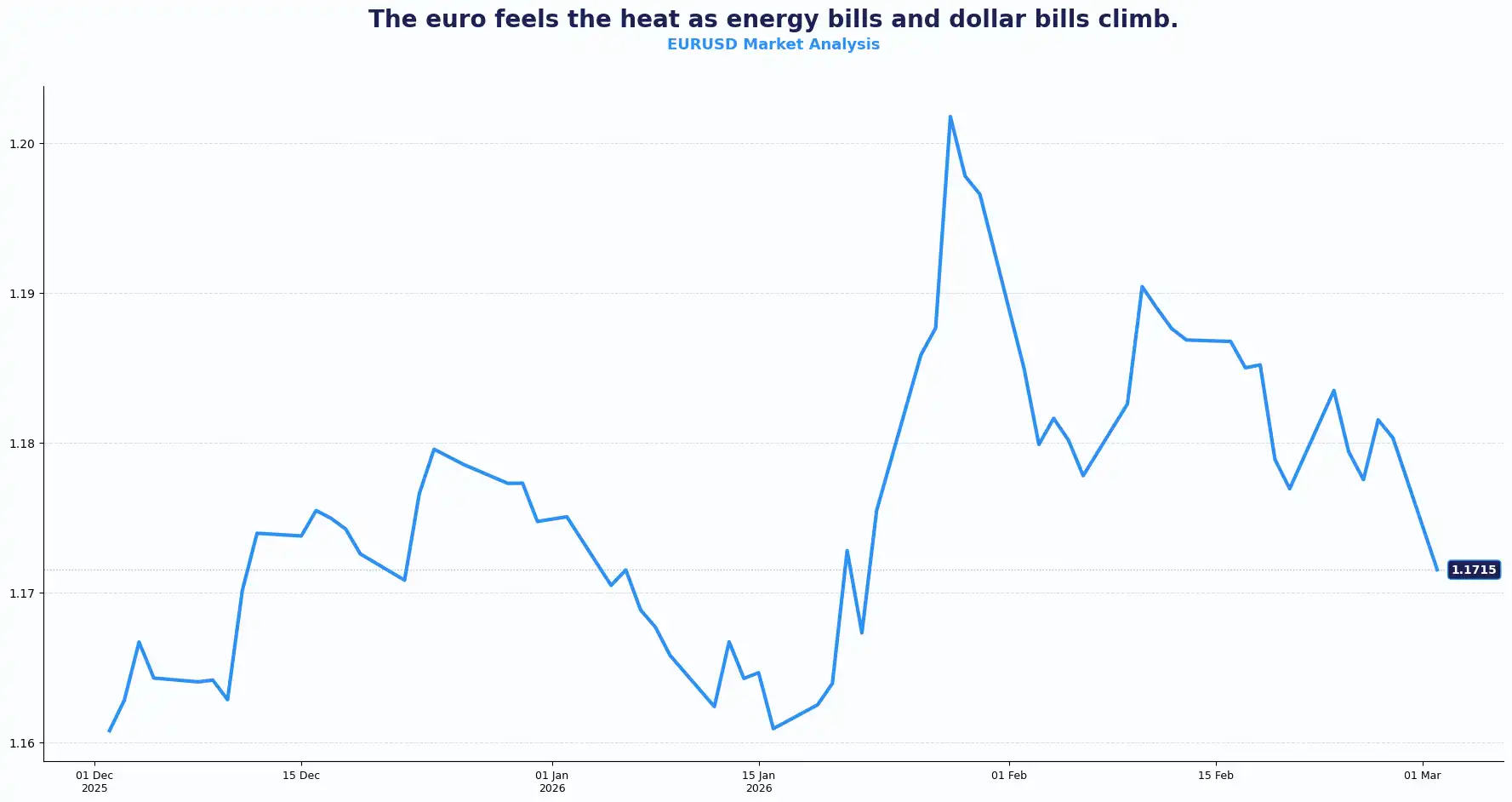

EUR: The Euro Feels the Energy Squeeze

The EUR/USD pair fell to 1.17 trading near 1.1731, the lowest levels since January 2026. Over four weeks, the euro lost 0.6% against the dollar. Year-on-year it is still up 12.02%, though that advantage erodes with each session of conflict-driven risk-off.

While the currency attempted a minor intraday recovery, it stayed tethered to soaring energy prices. German inflation data recently came in below forecasts, while price growth in France and Spain accelerated, creating a fragmented picture for the Eurozone.

Europe faces a structural energy crisis. The natural gas storage refill season begins now, yet the EU holds record-low stocks. This forces the bloc to purchase vast quantities of energy exactly as the US-Iran conflict sends prices vertical.

The divergence inside the eurozone complicates the European Central Bank’s (ECB) path. Money-market pricing assigns just a 30% probability to a rate cut by December. ECB President Christine Lagarde said last Thursday that headline inflation is on course to converge toward 2% over the medium term, with food inflation projected to hold slightly above 2% later this year.

Today’s Eurozone Manufacturing PMI survey responses offer a pulse on regional economic health. Investors will look to upcoming HICP figures to gauge whether the medium-term 2% inflation target stays achievable despite the current energy-driven volatility.

The euro now trades as an energy proxy. If oil and gas hold higher, inflation expectations could reprice. If growth data softens, policy expectations may shift again. The cross-currents keep the EUR pairs reactive.

Key technical levels for EUR/USD: Resistance sits at 1.1800, 1.1850 and Support at 1.1700, 1.1620;

USD: the Dollar Leads the Safe-Haven Pack

The dollar jumped as investors scrambled for safety, with the Dollar Index (DXY) hitting 97.94. U.S. Treasury yields initially hit an 11-month low of 3.926% before reversing to 3.970% - a classic risk-off dip followed by a partial unwind. This "U-turn" suggests the market is reconsidering the pace of Federal Reserve (Fed) easing amid new inflationary threats from the Middle East.

Fed fund futures now imply a lower chance of aggressive rate cuts. A June move stands at a 50-50 toss-up. While January PPI rose 0.5% and exceeded expectations, some analysts note that the category driving the headline beat - trade services, often does not capture real-time price changes. Investors now look to Friday’s US Nonfarm Payrolls to see if the labour market supports a "higher for longer" stance. Today’s US Manufacturing PMI is also a critical leading indicator for the business cycle.

Iran's national security chief, Ali Larijani, confirmed the country will not negotiate with the United States, despite earlier reports of back-channel contact via Oman. President Trump said the US sank nine Iranian naval vessels and will continue the bombardment. He added he is open to lifting sanctions if Iran's new leadership takes a pragmatic approach.

The dollar benefits from two sides: a resilient US economy and its status as the world’s ultimate fire escape during wartime. The dollar's role as the world's ultimate hedge is back in focus. Periods of geopolitical instability traditionally favour the greenback.

Global fallout: The Oil Shock Reverb

Oil prices leapt 9% on Monday morning. Brent crude briefly topped $82.00 before settling near $77.00. Share prices across Asia fell. Airlines and banks took the heaviest hits. The Swiss franc rose to 0.7693 against the dollar and to its strongest level since 2015 against the euro, at EUR/CHF 0.9077.

The effective halt of traffic through the Strait of Hormuz creates a physical supply squeeze. This waterway carries a fifth of the world’s seaborne oil and a third of its fertiliser. Shippers now fear the passage. War insurance costs ballooned overnight. President Trump suggested the military campaign might last four weeks. This timeline threatens to reignite global inflation. The situation mirrors the 1970s oil embargo. Back then, prices rose 300%. In 2026 terms, a similar move seems achievable if the blockage persists.

Other currencies feel the heat. The Australian dollar tumbled 1.2% before paring some losses to 0.7096. The New Zealand dollar fell to 0.5990. The Japanese yen weakened, and USD/JPY traded at 156.74. GBP/JPY sits near 210.47 after a sharp intraday rebound. Despite an initial haven bid, the yen suffered as investors weighed the cost of oil imports. The Bank of Japan is likely to adopt a more cautious stance, reducing the likelihood of a spring rate hike.

A prolonged spike in energy costs acts as a global tax on business. The shift toward safe havens such as the Swiss franc and the dollar reflects a change in global risk appetite. Understanding the link between the Strait of Hormuz and G10 currency pairs is now essential for every treasurer. The current halt in shipping capacity forces a recalibration of risk across all asset classes. Participants continue to monitor tanker traffic and diplomatic signals to gauge whether this supply shock will be persistent or transitory.

Current Rate Table

| Pair | Spot | Short term Trend |

|---|---|---|

| GBP/USD | 1.3377 | Soft below 1.3400 |

| EUR/USD | 1.1731 | Heavy near 1.1700 |

| EUR/GBP | 0.8771 | Firm above 0.8720 |

| USD/JPY | 156.74 | Elevated |

| GBP/JPY | 210.47 | Rebounding |

| AUD/USD | 0.7090 | Pressured |

| NZD/USD | 0.5990 | Soft |

| EUR/CHF | 0.9077 | down |

(rates as at the time of writing)

Market Look ahead

Tue, 3 Mar

US ISM Manufacturing PMI

Wed, 4 Mar

Australia GDP Q4

Eurozone, UK, US S&P Global Composite & Services PMIs

Eurozone PPI (Jan)

US ADP Employment Change (Feb)

Thu, 5 Mar

US Initial Jobless Claims

ECB Monetary Policy Meeting Accounts

Fri, 6 Mar

Eurozone GDP Q4 (SA)

ECB Speech by Christine Lagarde

US Unemployment Rate & Nonfarm Payrolls

US Fed Monetary Policy Report

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.