The Dollar Reclaimed 100. Sterling and Euro Slide.

7 min read

Share

The BoE held at 3.75%. Strong UK retail sales failed to lift sterling as a hawkish Fed reset global rate expectations. The dollar climbed back above 100. EUR/USD slid as US-Iran talks stalled. Policy divergence is back in the driving seat.

GBP: Retail Sales Surge but Politics Clouds the Pound

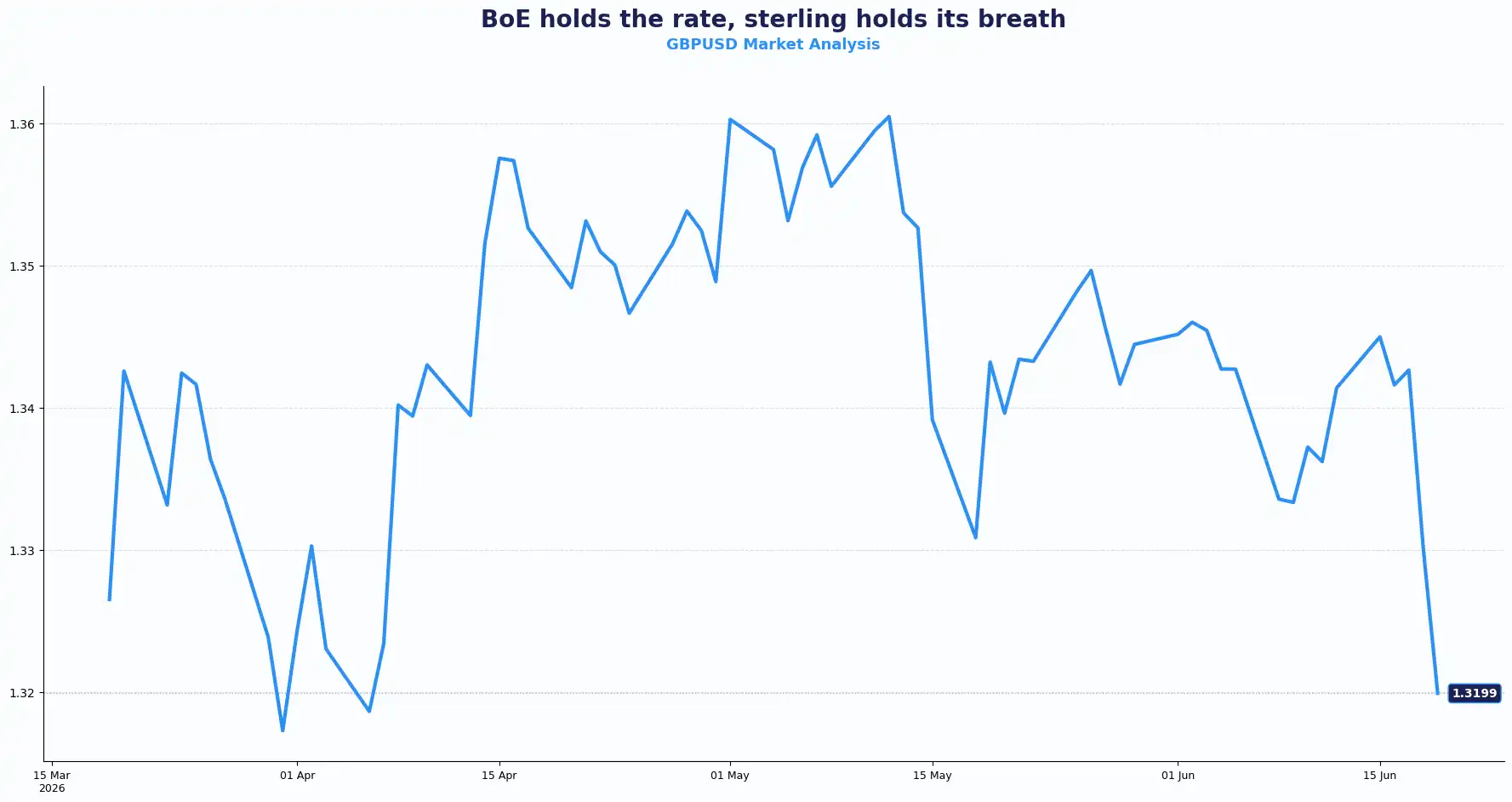

GBPUSD 1.3199 | EURGBP 0.8665

Sterling opened on Friday under pressure. The GBP/USD pair traded at 1.3168, down 0.3% on the day and extending Thursday's slide before testing 1.3200 level.

The Bank of England (BoE) held the Bank Rate at 3.75% in a 7-2 vote. Chief Economist Huw Pill and MPC member Megan Greene voted for a 25 bps hike for a second consecutive meeting. Governor Andrew Bailey pushed back, citing continued disinflation and softening in the labour market. The MPC's minutes flagged a range of views over whether tighter financial conditions since March are sufficient to tackle inflation. Forward-looking wage indicators suggest the pace of decline is stalling, even as current wage growth sits close to target-consistent levels.

UK Retail Sales delivered a genuine upside surprise. Core Retail Sales stripping out auto motor fuel rose 1.2% MoM in May, against a 0.4% forecast and a prior reading revised to -0.1%. Annual core Retail Sales jumped 4.6%, well above the 3.3% consensus and April's 1.1% reading. GBP attracted buyers briefly on the data, touching 1.3195, before slipping back.

The BoE's hold drew an immediate contrast with the European Central Bank (ECB) and the Bank of Japan, both of which tightened policies in the preceding days. Relative rate differentials are doing the heavy lifting. The BoE now reads as the dovish outlier in a G10 field that is turning hawkish. Two-year Gilt yields held firmer at 4.183%, up 4 basis points on the day. The FTSE 100 slipped 1%.

Domestic politics introduced a separate pressure point. Greater Manchester Mayor Andy Burnham won the Makerfield by-election with 24,927 votes, ahead of Reform UK on 15,696. The result clears a significant obstacle to a Burnham leadership challenge against Prime Minister Keir Starmer. Investors' concern over Burnham's spending outlook pushed Gilt yields to multi-year highs in May. His subsequent commitment to existing fiscal rules has partially calmed that move, but Gilts and Sterling both face heightened sensitivity to any further political development through the session. It appears that domestic politics might now be dictating the next leg for sterling.

Sterling carries dual weight: a central bank trailing its peers on tightening and a domestic political backdrop that has become a live pricing variable. Periods of elevated political uncertainty have historically been associated with wider bid-offer spreads and increased volatility in GBP pairs.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3250 and Support sits at 1.3100

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8700 and Support sits at 0.8630

EUR: Euro Under Pressure as Hormuz Hopes Hit a Wall

EURUSD 1.1451

The EUR/USD pair traded at 1.1423 in early European hours, slipping from the 1.1450 area after the Swiss Foreign Ministry confirmed that US-Iran talks at Bürgenstock would not proceed as planned. The Iranian negotiating team postponed its trip to Switzerland following ongoing Israeli attacks in southern Lebanon. US Vice President JD Vance cancelled his attendance in Switzerland. The dollar drew a safe-haven bid on the news.

ECB Governing Council member José Luis Escrivá flagged on Friday that energy costs are spreading into services and transport. He cited material uncertainty across the inflation baseline: oil production recovery timelines, price pass-through dynamics, and second-round wage effects all lack clarity. MPC member Pierre Wunsch separately indicated the ECB could cut rates once the dynamics shift, language that keeps a Q4 easing in view without locking in a date. The ECB is attentive but not yet directive.

The EUR/USD pair sits in a technically fragile range with a bearish bias intact. A durable resolution to the US-Iran situation would likely provide relief for the pair. Until that picture clarifies, the dollar's safe-haven function continues to cap the upside. Investors tracking ECB policy might read Escrivá's comments as consistent with a central bank that is carefully monitoring energy transmission before moving.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1450 and Support sits at 1.1411

USD: Warsh's First Meeting Sends the Dollar Back Above 100

DXY 101.07

The dollar index (DXY) extended its weekly gain to 1.3%, printing at 101.07. The Federal Reserve's (Fed) hawkish pivot under newly appointed Chair Kevin Warsh, caught short-duration traders off guard. Two-year Treasury yields rose 9 basis points on the week to 4.179%, while Ten-year yields fell 3 basis points to 4.451%, and thirty-year yields dropped 7 basis points to 4.901%, near a two-month low.

Market pricing now points to 38 bps of Fed tightening over the remainder of 2026. That repricing is compressing yield differentials across the G10 and narrowing the carry premium available on commodity-linked currencies. Oil's trajectory adds complexity. WTI crude rose 0.8% to $77.23 a barrel on Friday as the Hormuz ceasefire faced its first crack. Economists note that even if the peace deal holds, Strait traffic could track the Red Sea precedent, where volumes stayed over 50% below pre-crisis levels despite a ceasefire in May 2025. The durability of any Hormuz deal is not yet tested.

The dollar has reasserted itself as the week's defining narrative. A Fed unwilling to yield to political pressure, combined with easing oil dynamics, has produced a dollar that looks structurally supported at current levels.

Global Currency Shifts: The Ripple Effect

AUDUSD 0.7007 | NZDUSD 0.5730 | USDJPY 161.39 | GBPJPY 212.75 | USDIDR 17,840.00

The Australian and New Zealand dollars struggled as US yields moved higher and interest rate differentials narrowed. AUD/USD traded around 0.7007. Markets increasingly believe the Reserve Bank of Australia (RBA) may have reached the end of its tightening cycle after leaving rates unchanged this week.

Governor Michele Bullock maintained that further action remains possible if inflation proves persistent. However, investors now look for stronger evidence of renewed price pressures before pricing another move. That shift reduced support for the Australian dollar as US yields rose.

The New Zealand dollar faced similar pressure. NZD/USD traded near 0.5730 and hovered around three-month lows as investors favoured the dollar. The kiwi continues to face headwinds from a softer domestic outlook and less favourable yield dynamics.

Both currencies illustrate how quickly exchange rates can respond when relative rate expectations move in favour of the United States.

Yen weakness pushes intervention risk back into focus. The Japanese yen remained one of the weakest major currencies. USD/JPY climbed to 161.39, extending gains beyond the 160 level that many investors view as a potential trigger point for official concern. The move came despite the BoJ raising rates earlier in the week.

That outcome highlights a persistent challenge for the yen. Even when Japanese policymakers tighten policy, the yield gap with the United States remains substantial. Investors continue to favour dollar-denominated assets. Attention now turns to whether Japanese authorities increase verbal warnings or take more direct action if yen weakness accelerates further. Falling oil prices may offer some support to Japan's external position, but interest rate differentials continue to dominate price action. GBP/JPY traded near 212.75 as sterling benefited from the same dynamic.

The Indonesian rupiah edged higher despite fresh concerns surrounding market accessibility. MSCI raised questions about investability standards, coordinated trading activity and ownership transparency. Investors are now closely watching next week's classification review.

At the same time, lower oil prices and improved global risk sentiment helped stabilise conditions. USD/IDR traded around 17,800, though the pair continues to balance domestic risks against a stronger dollar backdrop. The rupiah's direction may depend on whether global investors focus more on local structural concerns or on broader shifts in US monetary policy.

Current Rate Table:

| Pair | Rate | Trend |

|---|---|---|

| GBP/USD | 1.3199 | Bearish |

| EUR/USD | 1.1451 | Bearish |

| EUR/GBP | 0.8665 | Neutral/Mild GBP weakness |

| USD/JPY | 161.39 | USD bullish / JPY weak |

| GBP/JPY | 212.75 | Bullish bias capped |

| AUD/USD | 0.7007 | Bearish |

| NZD/USD | 0.5730 | Bearish |

| USD/IDR | 17,840 | USD bullish |

Market Lookahead

Mon, 22 June

- Canada’s CPI (May)

- Eurozone Consumer Confidence (Jun)

Tue, 23 June

- Global PMI’s (Manufacturing, Services, Composite) (Jun)

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.