Strait Talk: FX Counts the Cost of Conflict

9 min read

Share

Strikes on Iran push oil to $83/bbl. Sterling and the euro retreat on inflation repricing. The dollar rises for a third straight day. Asian equities sell off hard. Safe-haven flows dominate.

GBP: Sterling Slips, Rate Bets Shift, Cable Fades

GBP/USD trades at 1.3319, down on the day and hovering near 1.3300. Rising Middle East tensions drive a bid into the dollar and pull “Cable” lower. Traders cut risk exposure amid escalating US and Israeli strikes on Iran. What makes this move stickier than a standard risk-off episode is the inflation channel.

UK BRC shop price inflation dropped to 1.1% yesterday. This move down from 1.5% shows the British consumer finds some relief at the till; however, surging oil prices have reshaped the Bank of England’s (BoE) outlook at speed. The probability of a March rate cut has collapsed from around 80% last week to below 20% today. That repricing should, in principle, offer the pound some support. But political uncertainty over Prime Minister Keir Starmer's leadership is capping any recovery.

EUR/GBP holds at 0.8705, flat on the day. The cross sits between two repricing stories running in parallel. The BoE is pulling back from rate cuts on one side. The ECB faces a policy environment it did not expect to navigate this week. Neither central bank is comfortable. The cross reflects that standoff.

A shift in rate expectations of this scale, from near-certain cut to near-certain hold in under a week, has in prior episodes been associated with elevated volatility across sterling crosses. Price swings reflect shifting rate expectations and geopolitical risk, not just technical flows. Periods like this often coincide with adjustments in corporate risk management and FX budgeting assumptions.

Key technical levels for GBP/USD: Resistance sits at 1.3400, 1.3480 and Support at 1.3280, 1.3200

Today’s focus turns to US ADP employment and ISM services PMI, UK S&P global services and composite PMI for fresh direction for the pair.

Key technical levels for EUR/GBP: Resistance sits at 0.8745, 0.8780 and Support at 0.8680, 0.8625

Sterling draws partial support from reduced BoE cut expectations. That keeps EUR/GBP contained rather than allowing it to trend. EUR/GBP now trades at the intersection of two shifting policy paths. Inflation sensitivity has increased on both sides. Cross-currency exposures tied to UK or eurozone revenues may experience wider ranges if oil volatility persists.

EUR: The Euro Shakes Under Inflation Heat and Energy Shock

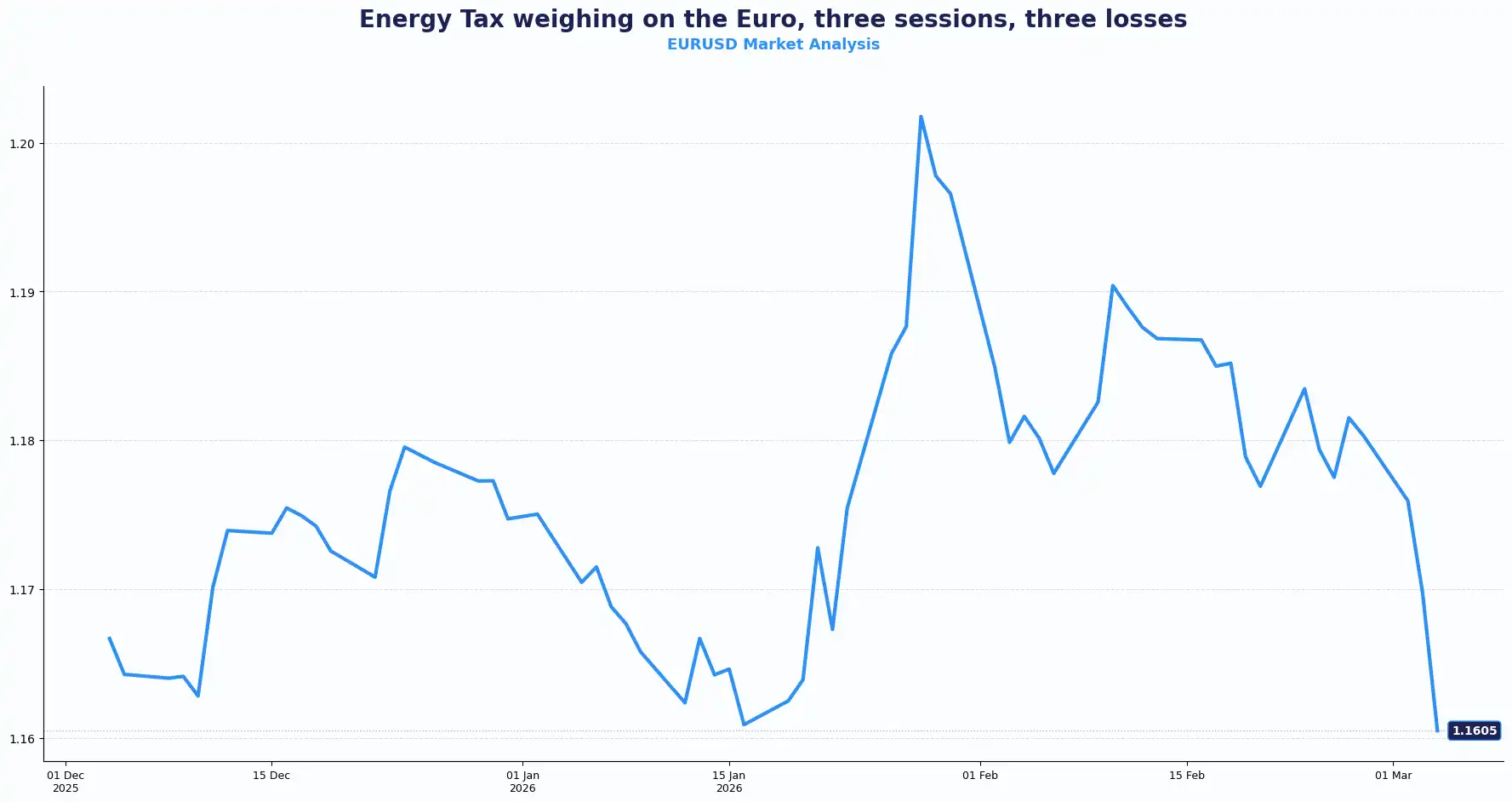

EUR/USD trades at 1.1595, down from a previous close of 1.1612. Losses extend into a third consecutive session. The pair touched its weakest level since late November earlier today.

Brent Crude climbed to $83.23 per barrel on Wednesday, the highest since July 2024, taking gains from Friday to around 14%. European natural gas prices have risen 70% since the end of last week. This represents a material shift in the cost base for the eurozone economy.

The euro grabbed headlines yesterday as flash estimates showed inflation rising to 1.9% in February. This data surprise caught many off guard, as core inflation also climbed to 2.4%. These figures complicate the European Central Bank’s (ECB) path. Traders sold the single currency aggressively as the "soft landing" narrative for Europe began to fracture under the weight of rising services costs. This structural shift stems from a double-sided squeeze. Energy costs continue to plague industrial output while services inflation refuses to budge from 3.4%.

The ECB now confronts an uncomfortable mix. ECB policymaker Yannis Stournaras acknowledged the bank is watching developments closely, with "no rush to change policy." ECB's François Villeroy de Galhau cautioned against predicting rate moves in haste. But the possibility of ECB rate hikes, a scenario that was remote two weeks ago, is now being priced in. The probability is small but the consequence of misjudging the trajectory is elevated.

The euro faces a clear structural headwind: Growth slows as energy costs bite. Inflation rises as import prices surge. A central bank that was guiding towards cuts must now re-examine that path. The euro sits between a weakening growth outlook and a hawkish policy scenario that almost nobody positioned for. Participants with eurozone exposure have been reassessing carry and duration positions against that backdrop.

ECB policymakers themselves have flagged that a sharp, prolonged price increase could put the bank in a genuine dilemma, one where raising rates becomes a live consideration rather than a theoretical one.

This fiscal fragility creates a heavy ceiling for the euro. The euro's inability to reclaim the 1.1800 handle against the dollar suggests a deepening bearish sentiment.

Key technical levels for EUR/USD: Resistance sits at 1.1650, 1.1720 and Support at 1.1550, 1.1480

If energy pressure persists, bond spreads across the bloc could widen. Carry trades funded in low-yielding euros face greater uncertainty. Geopolitical risk weighs more heavily on the euro than on the dollar. EUR/USD volatility reflects structural exposure to energy costs. When oil drives the narrative, the euro often trades with a heavier tone. Treasury teams with euro receivables or payables may see wider intraday ranges than earlier in the year.

USD: The Dollar Firms, Three Days, One Direction

The DXY dollar index trades at 99.20, rising for a third consecutive session to its strongest level since 28 November.

An oil shock is a negative supply shock for economies that import energy. Europe and Asia pay for energy in dollars, increasing demand for the currency. This demand, combined with safe-haven flows, is driving the dollar's recent movement. The currency situation reflects an ongoing negative supply shock. In effect, Europeans are directly taxed by paying foreign producers in dollars. This is the clearest explanation for what is happening with DXY now.

President Trump posted on Truth Social that he has ordered the US Development Finance Corporation to provide political risk insurance for tankers in the Gulf. He raised the possibility of the US Navy escorting shipping through the Strait of Hormuz. The announcement paused the sell-off, but it did not resolve the underlying risk.

This raises questions about the practical scope of US Navy assistance. Most tankers transiting the strait are not US-owned or US-flagged. The DFC's capacity to absorb insurance risk at scale is untested. Using naval assets in a contested, narrow waterway with hostile forces nearby involves significant operational complexity. Legal challenges to these arrangements are widely anticipated. The announcement bought time, but the disruption it addressed is unresolved. Crucially, the administration did not have this in place before the strikes, providing little reassurance about the depth of planning behind the wider operation.

Meanwhile, a robust retail sales report showed that American consumers continue to spend despite elevated borrowing costs. The immediate reaction saw the greenback claw back losses, putting immense pressure on high-beta currencies.

The structural driver here is American exceptionalism. The US economy continues to grow while some European economies struggle. Federal Reserve (Fed) officials have shifted their tone, now emphasising that they are in no rush to loosen the reins. This "strong dollar" environment sucks capital out of peripheral regions and back into US Treasuries.

This environment has led some participants to reconsider their long-term exposure to the greenback. The dollar's role as the ultimate safe haven persists, especially as geopolitical tensions simmer.

The dollar’s strength stems from both cyclical and structural drivers. Safe-haven demand and energy invoicing in dollars reinforce each other. Cross-border cash flow planning may require updated assumptions if the conflict extends.

Beyond the Majors: Asia Catches the Fallout

AUD/USD trades at 0.7004 and stays under pressure despite stronger domestic data. Australian Q4 GDP beat estimates, printing at 0.8% QoQ against a 0.6% forecast. The data beat did not translate into currency support. Global risk aversion is the dominant force in the session. The underlying detail in the GDP release was mixed, and the RBA is likely to note that growth running above potential constrains the case for further easing, even as the external backdrop deteriorates.

NZD/USD trades at 0.5896, modestly higher on the day. USD/JPY trades at 157.55. GBP/JPY trades at 209.85 as yen volatility rises alongside equity swings. Today's move wiped out all of the Nikkei's gains since Prime Minister Sanae Takaichi's election win in early February. Investors who bought Japanese equities after that result have been selling into the latest wave of risk-off pressure. Offshore USD/CNH trades at 6.9287 after mixed Chinese PMI readings. Official gauges signalled contraction while private surveys beat expectations.

The sharpest moves came from Seoul. The KOSPI shed 15% over two sessions, the heaviest fall since 2009, triggering circuit breakers as South Korea's export-driven economy priced in the risk of sustained energy disruptions. The Korean won fell to a 17-year low. When the scale of the Hormuz disruption became clear, there were no diversified bids to absorb the selling.

This sell-off has changed character. It is no longer being priced as a short-term headline shock. The repricing now reflects a potential conflict that could run for weeks. Knock-on effects are spreading across energy logistics, inflation timelines, and risk premia across the region. Asia's sell-off is turning disorderly because pricing no longer treats this as a one-week event. Bitcoin and Ether also continued their decline.

Commodity and Asia-linked currencies now trade in a global macro frame. Energy logistics, supply chain security and rate differentials shape direction. Range expansion across G10 and Asia pairs may persist while oil volatility stays elevated.

Current Rate Table

| Pair | Spot | Short-term Trend Bias |

|---|---|---|

| GBP/USD | 1.3319 | Bearish below 1.3400 |

| EUR/USD | 1.1595 | Bearish below 1.1700 |

| EUR/GBP | 0.8705 | Range 0.8650–0.8780 |

| USD/JPY | 157.55 | Bullish above 155.00 |

| GBP/JPY | 209.85 | Volatile, upside bias |

| AUD/USD | 0.7004 | Heavy below 0.7100 |

| NZD/USD | 0.5896 | Range-bound |

| USD/CNH | 6.9287 | Firm above 6.9000 |

(rates as at the time of writing)

Market Look ahead

Wednesday, 4 March

Australia Q4 GDP

Eurozone HCOB PMI

UK S&P Global Composite and Services PMI

US ISM services PMI

Eurozone PPI (January)

US ADP Employment Change,

Thursday, 5 March

US Initial Jobless Claims

ECB Monetary Policy Meeting Accounts

Friday, 6 March

Eurozone Q4 GDP (final)

ECB President Christine Lagarde speech

US Nonfarm Payrolls and Unemployment Rate

US Fed Monetary Policy Report

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.