Sterling Stands Tall While Global Trade Shifts

8 min read

Share

The dollar retreats as Trump’s State of the Union triggers trade uncertainty. Sterling holds above 1.35 on hawkish BoE rhetoric. The euro tests 1.18 on dollar weakness, while the yen slides after Takaichi signals a pause on interest rate hikes.

GBP: Sterling Pierces 1.3500 as Rate Cut Hopes Fade

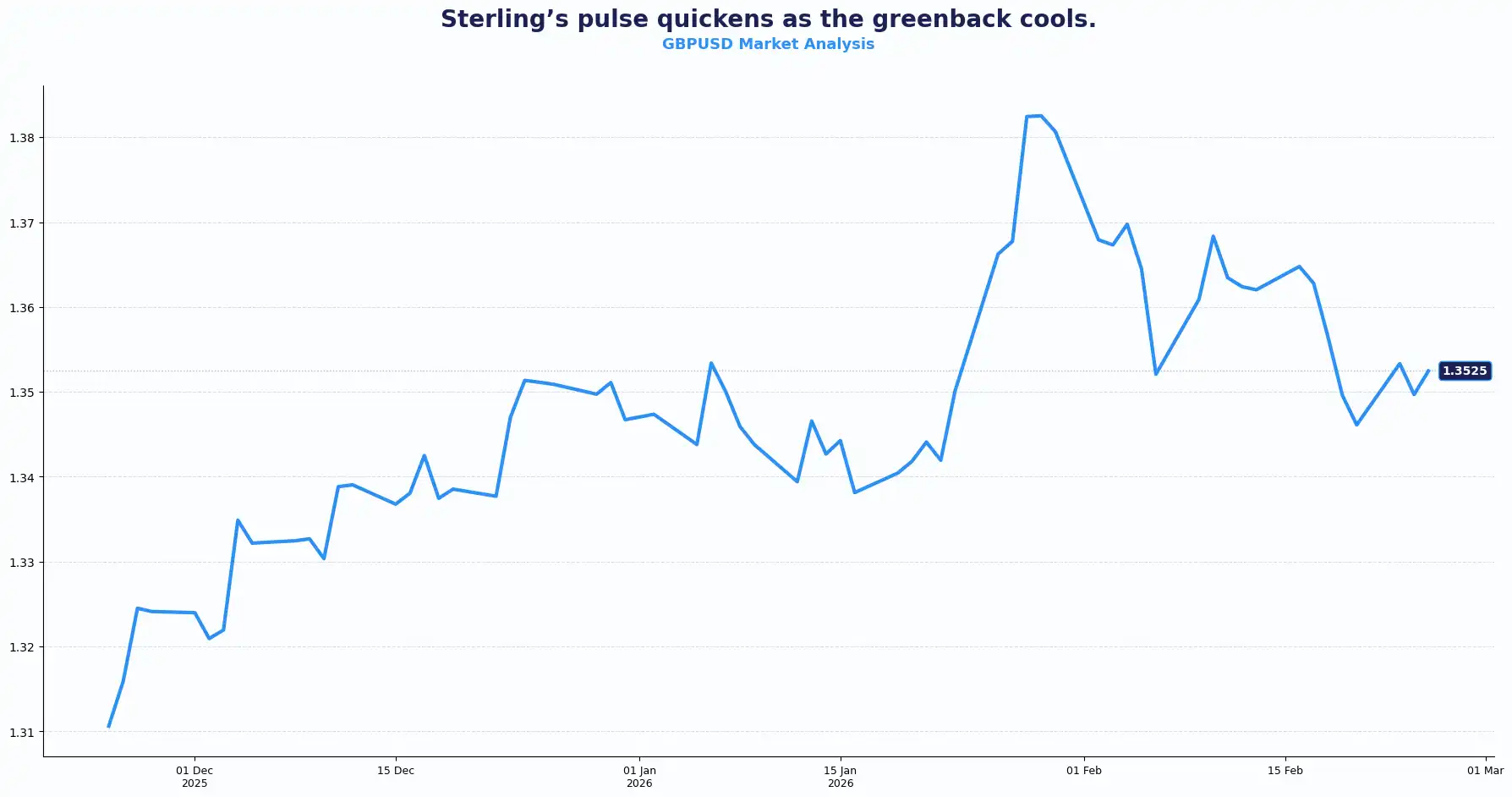

Sterling opened Wednesday at $1.3492 and climbed to $1.3525 through Asian hours. A softer dollar did the heavy lifting post-SOTU, but domestic conviction sustained the move. While the currency thrives on the surface, underlying data paints a conflicted picture.

The data landed hard. The CBI Retail Sales Balance plummeted to -43 in February, far missing the -16 forecast. Retailers called seasonal sales "poor." Consumer demand has been softening since mid-2023, and February marked a sharp step down. The currency pairs find support despite these internal headwinds.

The Bank of England (BoE) is treading carefully. Governor Bailey said a March rate cut is an "open question" with services inflation at 4.4%, still above the 4.1% projection. This data point stops the momentum for early policy easing. Chief Economist Huw Pill warned against being "beguiled" by headline inflation easing toward the 2% target. The Monetary Policy Committee (MPC) held rates after a narrow split vote. Before Bailey's speech, traders had priced in two cuts this year, taking the benchmark rate to 3.25%.

Domestic factors drive the near-term appeal of the pound. Jobless figures rose in the final quarter of 2025. January inflation hit a low point. These stats reinforce the need for a cautious stance.

The tariff story adds another layer. William Bain, head of trade policy at the British Chambers of Commerce, put it plainly: "While a new 10% tariff rate, instead of the threatened 15%, provides some relief, it highlights how difficult it is for businesses to plan ahead."

A local election in Manchester tomorrow tests the strength of Prime Minister Keir Starmer. Political stability dictates the next leg of this trend.

Weak retail, a split MPC, and tariff uncertainty are pulling in different directions. Traders have shifted focus to domestic factors as the key driver of sterling's near-term direction. Historically, elevated policy uncertainty of this kind is associated with wider bid-offer spreads and sharper short-term GBP volatility. Periods like this often coincide with adjustments in corporate FX positioning and hedging behaviour.

EUR/GBP hovers near 0.8727, trading in a tight range with no clean directional conviction. The cross needs a break above 0.8760 to shift momentum. A move below 0.8700 would tilt the short-term bias towards sterling strength.

GBP/USD holds above the 1.3500 handle after the recent breakout. Key technical levels for GBP/USD: Resistance sits at 1.3560, 1.3600 and Support at 1.3480, 1.3420, with the Pivot zone being 1.3500

EUR: Euro Tests 1.18 on Fresh Dollar Selling

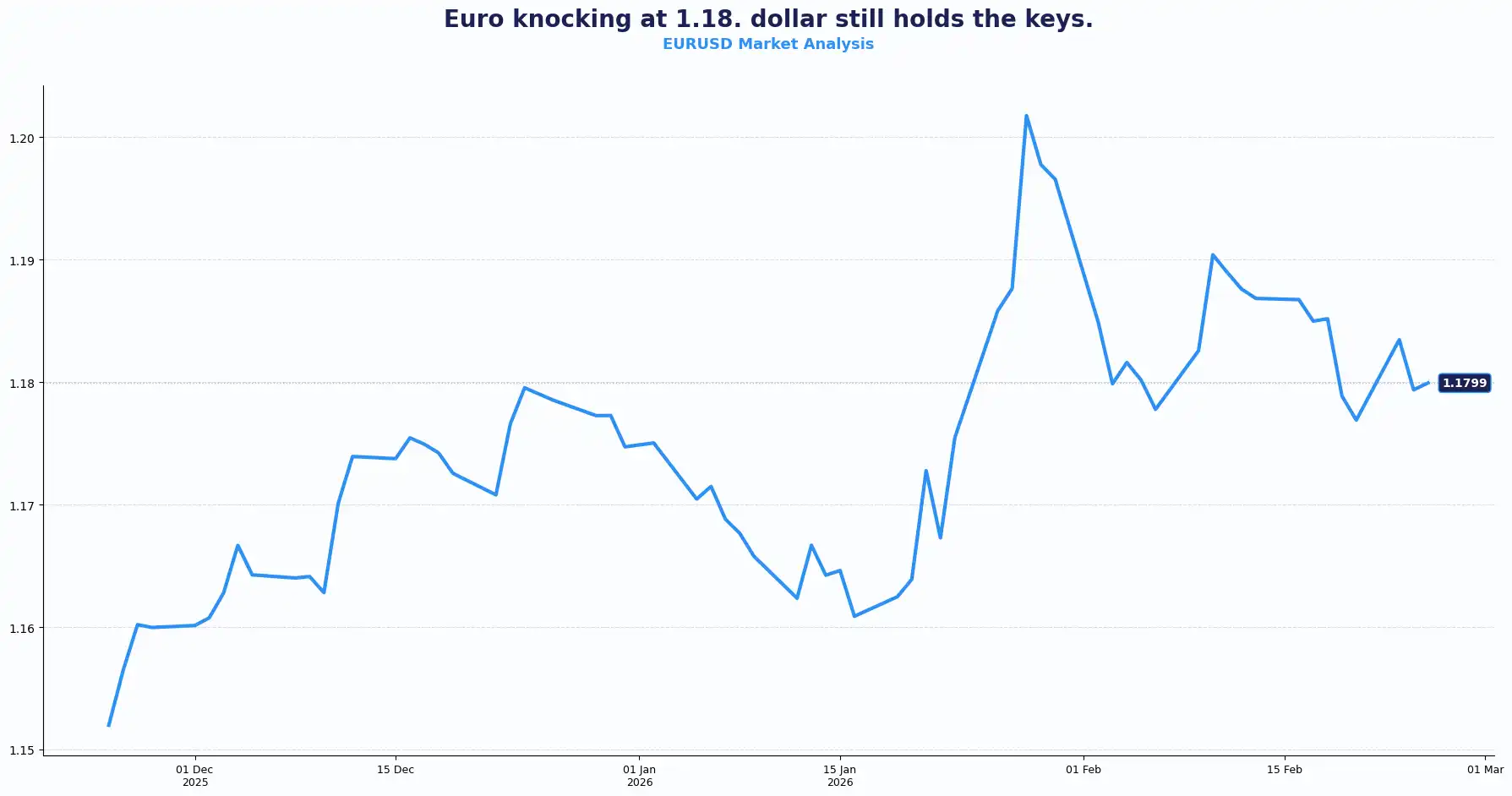

The euro is currently testing the 1.1800 handle, after EUR/USD opened at 1.1773 in the Asian session. Trade uncertainty sponsored this upward move. Fresh selling around the dollar weighs on the pair.

Trump's SOTU confirmed the tariff structure, and traders didn't welcome the detail. The White House confirmed a temporary 10% global tariff for 150 days under Section 122, with a 15% target in the pipeline. Retaliatory risks and concerns about global supply chain disruptions weigh on the dollar, lifting the EUR/USD pair.

Germany gave the single currency something genuine to stand on today. The final Q4 2025 GDP print from Destatis landed above expectations on both measures: QoQ growth came in at +0.3%, beating the +0.2% forecast, while the YoY figure hit +0.6%; the strongest annual reading in three years, against a consensus of +0.3%

Defence and infrastructure spending, now moving through the budget pipeline after the 2026 approval was finally secured late last year, point to further domestic demand support ahead. Germany ended 2025 in positive territory after a bruising year for foreign trade. That is not a trivial footnote.

At the policy level, ECB President Lagarde maintains her "no change" stance, providing a floor for the euro. The European Parliament's decision to postpone a vote on an EU-US trade deal, however, puts a ceiling on aggressive bullish positioning. Uncertainty cuts both ways.

The upside for EUR/USD is real but contained. The pair's gains are more USD-driven than euro-driven. The euro does not carry significant undervaluation at current levels, and the ECB is not about to turn hawkish. On the other side of the equation, the Fed is sounding firmer than traders had expected. A delayed and shallower US easing cycle is a structural cap on how far EUR/USD can push from here. Germany's fiscal pivot supports growth, but it does not resolve the fundamental policy divergence question that will ultimately drive this pair.

The next test is the final eurozone CPI print. That will either validate Lagarde's steady hand or force the ECB into a conversation it would rather not have yet.

Participants typically interpret the current setup as dollar-led rather than euro-led.

The German print removes downside alarm but does not create a new bullish narrative. With the ECB steady and the Federal Reserve sounding comparatively firm, positioning behaviour tends to favour tactical range engagement near 1.1800 rather than aggressive trend conviction.

Key technical levels for EUR/USD: Resistance sits at 1.1800, 1.1850 and Support at 1.1740, 1.1680, with the Pivot zone being 1.1775

USD: The Dollar Retreats After Trump’s Union Address

The dollar index fell 0.22% to 97.66. Trump's address ran nearly two hours, spanning tariffs, Iran, DEI, prescription drugs, a government-matched 401(k) contribution of up to $1,000, and a promise to "make peace whenever I can." Currency traders were left with more questions than answers. Despite the "USA, USA" chants and claims of an "American turnaround for the ages," the greenback lacked its usual bite. US Treasury yields edged higher, but the currency failed to follow suit.

The Fed is in no rush. Boston Fed President Susan Collins said it would be appropriate to hold rates for some time. Richmond Fed President Thomas Barkin called monetary policy "well-positioned" to manage risks. Fed Governors Lisa Cook and Austan Goolsbee signalled that the labour market may be stabilising, though conditions are still soft and acting as a source of disinflationary pressure. Forecasts signal the Fed easing in June, with 75 bps of cuts across 2026.

On tariffs, the SOTU confirmed 10% global levies for 150 days under Section 122, with a 15% target. Trump warned countries not to "play games" with trade agreements, and pointedly referenced a "very unfortunate ruling" after the Supreme Court blocked several of his broader tariff packages. The gap between executive intent and judicial outcome is keeping the dollar's trajectory unclear.

The dollar has shed ground this week on a mix of tariff ambiguity, soft labour signals, and a Fed in no hurry to move. The next catalyst is fresh Fed speak and any new trade policy development. Traders are watching both very closely.

Other Currencies: Yen Slides, Aussie Climbs, Yuan Firms

The yen is the standout story in Asia this morning. The Mainichi reported that Prime Minister Sanae Takaichi told Bank of Japan Governor Kazuo Ueda she had reservations about further rate hikes during their meeting last week. If accurate, this signals friction between the government and the BOJ's stated rate path. The yen hit $156.28 overnight before edging back to $155.88.

The yen has been sliding for years due to Japan's low-rate environment. Takaichi's arrival in October deepened those concerns. The reflationist tilt of her cabinet, including at least one super-dovish BOJ board nomination, tells the story. Traders had priced in a roughly 70% chance of a hike by April. That has been repriced to 51% for April and 65% by June. A separate report noted the US-led "rate checks" in January that helped prop up the yen. Intervention risk still acts as a brake against the 160 mark.

The Australian dollar is the session's strongest gainer. AUD/USD climbed 0.3% to $0.7074 after Australian inflation data picked up, raising rate hike expectations. The SOTU-driven dollar weakness added further tailwind.

The Chinese yuan is quietly asserting itself. It posted its sharpest one-day rise in nine months on Tuesday, gaining 0.35%. The Supreme Court's decisions on US tariffs pointed toward a lower overall rate on Chinese goods. Structural support from currency undervaluation and export sector strength underpins the move. With Trump's planned China visit at the end of March reducing the near-term risk of fresh Section 301 tariffs, the yuan has room to firm further.

The New Zealand dollar edged to $0.5971.

Asian equities opened in the green, building on the overnight Wall Street rebound. South Korea, Taiwan, and Japan are benefiting directly from AI hardware capex. Trump touched on AI briefly in the SOTU with a "rate-payer protection pledge" requiring major tech firms to build their own power plants for data centres. Details on implementation were absent. One analyst framed it well: "AI is not a bubble technology, but that doesn't mean every AI bet will pay off. There are companies spending significantly on AI that likely won't see a return."

Oil edged up 0.6%. Prices dipped when Trump said his preference was to resolve Iran's nuclear question diplomatically, though the US military posture in the region signals a different kind of pressure. As is typical with State of the Union addresses, broader currency moves were contained.

Current Rate Table

| Pair | Spot | Short-Term Bias |

|---|---|---|

| GBP/USD | 1.3525 | Mild bullish |

| EUR/USD | 1.1797 | Testing resistance |

| EUR/GBP | 0.872 | Range-bound |

| USD/JPY | 155.88 | Yen soft |

| GBP/JPY | 210.53 | Uptrend intact |

| AUD/USD | 0.7074 | Constructive |

| NZD/USD | 0.5971 | Steady |

| DXY Index | 97.66 | Soft bias |

*(Live-rates as at the time of writing)

Market Look ahead

Thursday, 26 Feb

UK - Manchester Election

Friday, 27 Feb

UK - Gfk Consumer Confidence

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.