Rate-Driven. Court-Shaken. February Signs Off

8 min read

Share

Sterling stalls near 1.35 as BoE doubts grow and politics stir. The euro steadies, the dollar drifts, and rate divergence drives FX into March.

GBP: Rate Cut Bets Dampen Sterling’s Fire

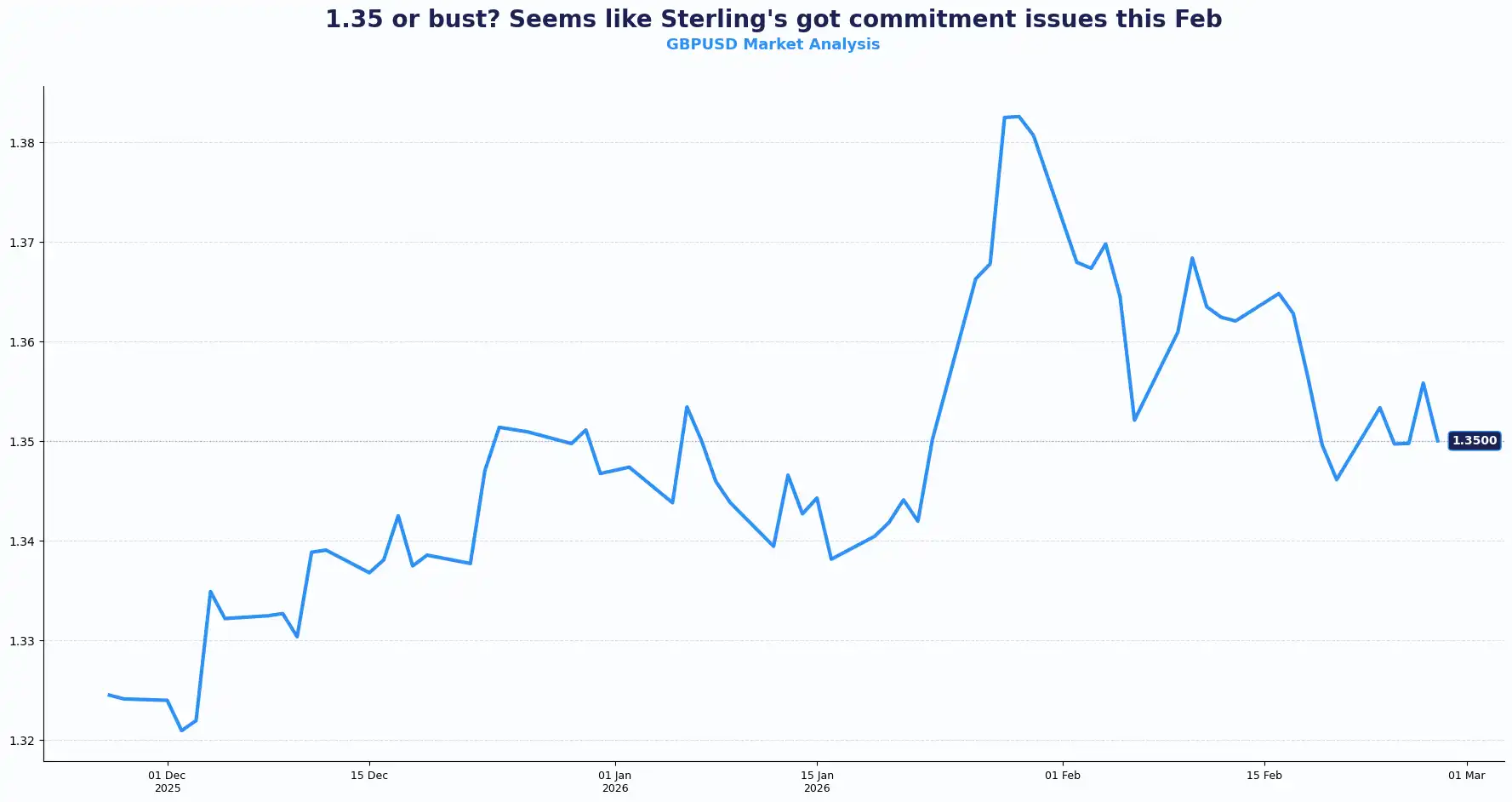

The British pound firmed up to $1.3492 before settling flat near $1.3484. The pound is on course to snap three straight months of gains, down 1.5% in February. A distinct shift in tone from the Bank of England (BoE) has pulled the rug from under sterling.

GBP/USD opened weaker at 1.3483, struggling to find momentum amid a 83% chance of a March rate cut. This follows Governor Andrew Bailey’s no pushback stance at the parliamentary Treasury Committee this week. He called a March cut "a genuinely open question" and pointed to services inflation at a “sticky” point.

The data support the doves' argument. The structural weight on the pound stems from a cooling economy. Sluggish fourth-quarter GDP growth and rising unemployment, paired with January’s lower inflation, force the BoE’s hand. While the bank held rates in a tight 5-4 split earlier this month, the pivot toward easing is now undeniable.

Domestic politics adds a layer of fog; the Manchester by-election in Gorton and Denton acts as a litmus test for Prime Minister Keir Starmer. A Labour defeat would likely trigger fresh questions about his leadership following the Peter Mandelson scandal.

Gilt yields fell to their lowest level since December 2024. British 10-year yields sit at 4.31%. Investors are waiting for the UK Debt Management Office to release bond issuance plans. Next week, Chancellor Rachel Reeves delivers updated forecasts. No fireworks are forecast, but the inflation narrative will set the tone for how traders read the BoE's next move, and shape the direction of gilts and sterling.

Policy divergence defines this move. The BoE shifts while others stay the course. Political instability adds a risk premium to the pound. A weaker Labour Party suggests a weaker currency.

Sterling now trades at the intersection of rate repricing and political risk. Rate expectations have shifted quickly. Periods of sterling volatility of this kind have historically coincided with increased hedging activity among UK-based importers and exporters, as currency risk reprices fast.

Key technical levels for GBP/USD: Resistance sits at 1.3600, 1.3720 and Support at 1.3420, 1.3300;

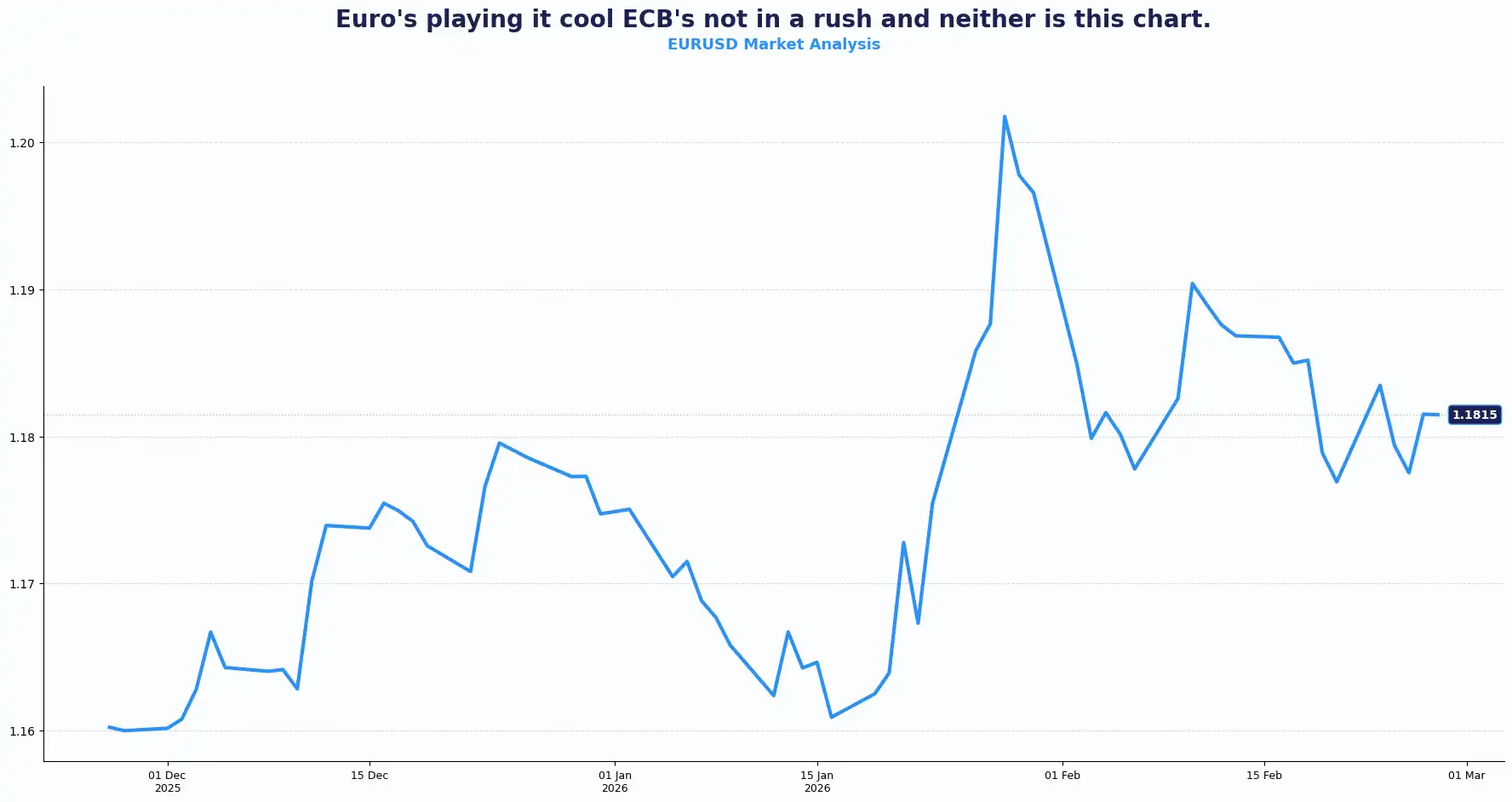

Euro Stasis: Lagarde’s Long Game

The euro hovers near 1.1800. Investors await inflation data to gauge how currency strength affects price pressures. The euro opened at 1.1796 on Friday, barely moved, and headed for a monthly loss of just over 0.4%.

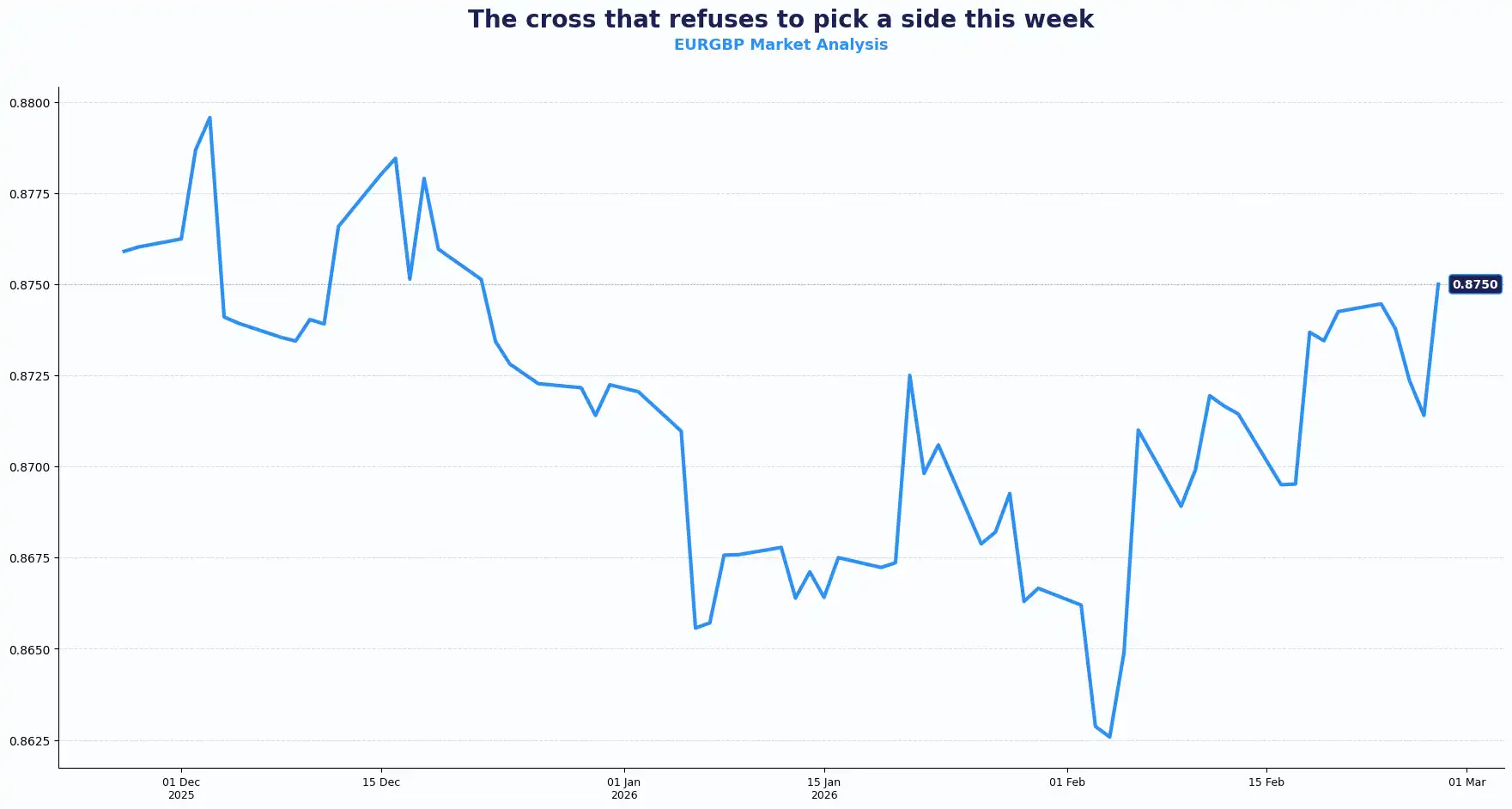

EUR/GBP trades near 0.8753 with policy divergence between the ECB's patience and the BoE's softening stance shaping positioning for the pair.

ECB President Christine Lagarde addressed the European Parliament committee on Thursday with a familiar tone: headline inflation is on track to reach the 2% target over the medium term, food inflation is expected to sit just above 2% later this year, and she expects to see out her term in full. She drew a clear line on FX: the ECB will watch currency moves but will not intervene directly in foreign exchange markets.

Thursday's data confirmed the ECB reduced the dollar's weight in its foreign exchange reserves in early 2025 by selling some dollar assets. This move signals a subtle shift in the central bank’s balance sheet strategy and a structural shift worth noting as reserve diversification feeds into longer-term currency flows.

Money market pricing tells you where the consensus sits: just a 30% chance of an ECB cut by December. Easing wage growth and subdued inflation give the ECB cover to wait. Lagarde is not blinking.

Corporate behaviour is telling its own story. A survey conducted by a software provider of around 750 finance decision-makers at North American, European and UK companies. These companies have market capitalisation between $50 million and $1 billion. They found that 88% now hedge currency risk, up from 81% a year prior. Of those not yet hedging, nearly two-thirds said they were considering it amid current conditions of volatility and geopolitical uncertainty. Companies are extending hedge tenors and running balanced hedge ratios. The survey highlights a structural shift in risk management behaviour.

The ECB prioritises stability over stimulus. While the dollar retreats, the euro finds a floor. The shift away from dollar reserves shows a desire for diversification.

Policy divergence with the UK and the United States drives cross-flows for the euro.

Key technical levels for EUR/GBP: Resistance sits at 0.8800, 0.8850 and Support at 0.8700, 0.8625

Key technical levels for EUR/USD: Resistance sits at 1.1850, 1.2000 and Support at 1.1700, 1.1620;

USD: The Dollar Softens, Amid Fed Hawks and Legal Wars

The dollar index sits at 97.66. The Federal Reserve is expected to hold rates through at least June, balancing elevated inflation against softening labour signals. Fed funds futures price in a 98% probability of no change at the 18 March meeting. The Fed is parked.

The week's defining moment came from the Supreme Court. On 20 February, it struck down Trump's emergency tariffs, a ruling that reinforced institutional constraints on executive power and added to the dollar's near-term headwinds. Uncertainty over President Trump's response lingers and will keep traders guessing on trade policy.

Jobless claims increased marginally last week. The unemployment rate stays steady. US initial jobless claims came in at 212,000 for the week, up 4,000. The four-week moving average holds at 220,250. The insured unemployment rate two weeks ago sat at 1.2%, unchanged.

Former St. Louis Fed President James Bullard offered his read in an interview this week: one further 25bp rate cut in the second half of 2026, data permitting. He also suggested Jerome Powell could serve out his remaining term as a governor even with Kevin Warsh now at the helm of the FOMC.

The structural argument building against the dollar is not new but it is gaining traction. Some analysts point to the dollar's strained status as haven, the continued "hedge America" trade, and a backdrop of solid global growth, lower rates abroad, and expanding fiscal buffers elsewhere. That combination has historically been bearish for the dollar and the data is starting to rhyme with history.

The "exceptional" U.S. narrative is fracturing. Legal setbacks for the executive branch and a cautious Fed limit dollar’s upside The dollar trades without clear conviction. Rate expectations anchor the front end. Global growth and policy divergence steer the medium term.

Global Pulse: Aussie Heat, Yen Lags, the PBOC Pulls the Handbrake

The Aussie dollar climbed to 0.7130. It gained 2% this month. It is the best G10 performer so far this year. A healthy domestic economy fuels expectations for a hawkish Reserve Bank of Australia. The Aussie dollar can gain another (U.S.) cent or two from here. One more 25bps hike from the RBA looks likely.

The USD/JPY fell below 156.00. Tokyo CPI rose to 1.6% in February. This backs a hawkish outlook from the Bank of Japan. Governor Kazuo Ueda signals a near-term hike. Domestic politics continue to muddy the rate-hike path and the yen's recovery stays incomplete. Geopolitical tension and the AI trade influence sentiment.

In China, the PBOC moved to slow yuan appreciation. It intends to scrap foreign exchange risk reserves for forward contracts, encouraging dollar buying. The yuan gained 4.4% in 2025. The upward momentum hit a wall as China applied the brakes. China gained leverage after the U.S. Supreme Court quashed the Trump tariffs. Onshore yuan (CNY) trades at 6.8572 per dollar. Offshore (CNH) sits at 6.8542. The two trade within a very tight margin, consistent with converging onshore-offshore dynamics.

Global tension persists. The U.S. and Iran made progress in nuclear talks. Oman mediated to avert strikes. However, the U.S. military presence in the Middle East stays large. Russia and Ukraine are still in a deadlock. U.S.-China relations stay fragile.

The February Close

Conviction has been low all month. Clear directional trends have been scarce. Traders navigated geopolitical tension, a landmark Supreme Court ruling, and volatile AI sentiment; all within four weeks.

But underneath it all, rate expectations drove the bus. Last year's question was which central banks would cut and by how much. This year's question is who leads the hiking cycle. The Aussie is already pricing in the answer. The yen is still waiting for politics to catch up.

“The rates are reflecting the changing macro situation”. That shift is the through-line for February. It is also the setup for March.

Geopolitical footnote: Talks between the United States and Iran made significant progress this week, with mediator Oman confirming advances aimed at resolving the nuclear dispute. A US military build-up in the Middle East adds context. Any escalation there, a shift in Russia-Ukraine negotiations, or renewed friction in US-China relations could reshape FX flows at short notice.

Current Rate Table

| Pair | Spot | Short term Trend |

|---|---|---|

| GBP/USD | 1.3492 | Soft below 1.3600 |

| EUR/USD | 1.1800 | Firm, range |

| EUR/GBP | 0.8753 | Firm, range |

| AUD/USD | 0.7130 | Uptrend intact |

| USD/JPY | 155.75 | Soft, Range 153–158 |

| GBP/JPY | 210.15 | Volatile, rate led |

| USD/CNY | 6.8572 | Managed band |

(rates as at the time of writing)

Market Look ahead

Today, 27 Feb

US Producer Price Index

Monday, 2 Mar

Eurozone Flash Manufacturing PMI

Germany’s Retail Sales & HCOB Manufacturing PMI

US - SM Manufacturing PMI & Employment Index

Tuesday, 3 Mar

Eurozone Harmonized Index of Consumer Prices

Eurozone - Producer Price Index

Friday, 6 Mar

US Non-Farm Payrolls

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.