Oil Moved. The FX followed

8 min read

Share

A week of oil shocks, collapsed rate bets and safe-haven scrambles. Oil’s surge and rising yields drive a stronger dollar while sterling and the euro drift lower. Energy risk and geopolitics dominate FX pricing as traders scan labour data and central-bank signals.

GBP: Sterling Suffers Loud Drop on a Quiet Calendar

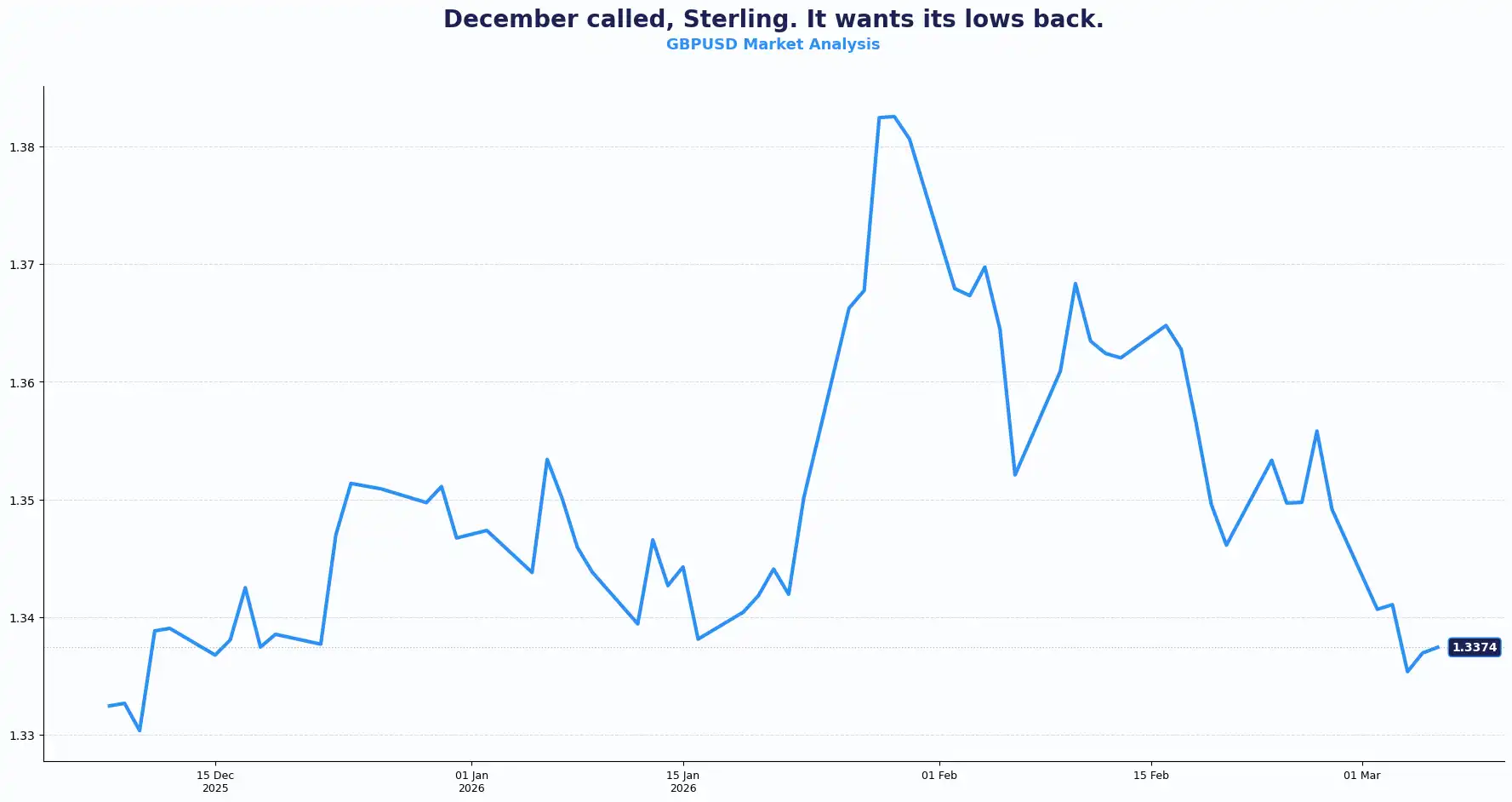

Sterling sat at 1.3354 against the dollar on Friday, posting a 0.95% weekly drop and trading close to its weakest level since December.

The Bank of England (BoE) rate cut story flipped this week, and it flipped hard. A near-certainty of a cut just seven days ago had collapsed to 23% by Friday. Energy prices drove that shift. Britain's dependence on oil and gas imports puts it in the direct line of fire whenever Middle East tensions spike, and this week they spiked hard. Raising the risk of imported inflation returns.

Domestically, the backdrop did not flatter sterling. UK GDP growth was sluggish in Q4 last year. The Labour Party lost the Manchester by-election. UK Prime Minister Keir Starmer drew criticism over Britain's stance on the US-Israel-Iran conflict. This political noise, layered on macro pressure, rarely ends well for a currency. While political noise does not drive FX on its own, it influences confidence in fiscal discipline and policy stability.

Chancellor Rachel Reeves delivered a Spring Statement on Wednesday. The headline numbers looked clean, with borrowing and inflation projections below forecast. Despite this, the OBR cut its UK growth outlook for the year, signalling concerns that could dampen confidence in the UK economy. Adding to these concerns, the OBR projections did not account for further instability in the Middle East. Should energy costs rise for a prolonged period, the outlook could change again.

The UK data calendar looked quiet, so with limited domestic data, external factors such as energy prices and global risk sentiment now exert greater influence on sterling moves.

Sterling now sits at the intersection of soft growth, energy exposure and uncertain rate expectations.

Key technical levels for GBP/USD: Resistance sits at 1.3420, 1.3500 and Support at 1.3300, 1.3225; Bias sits with downside pressure below 1.3420.

EUR: The Euro Buckles Under Oil and Uncertainty

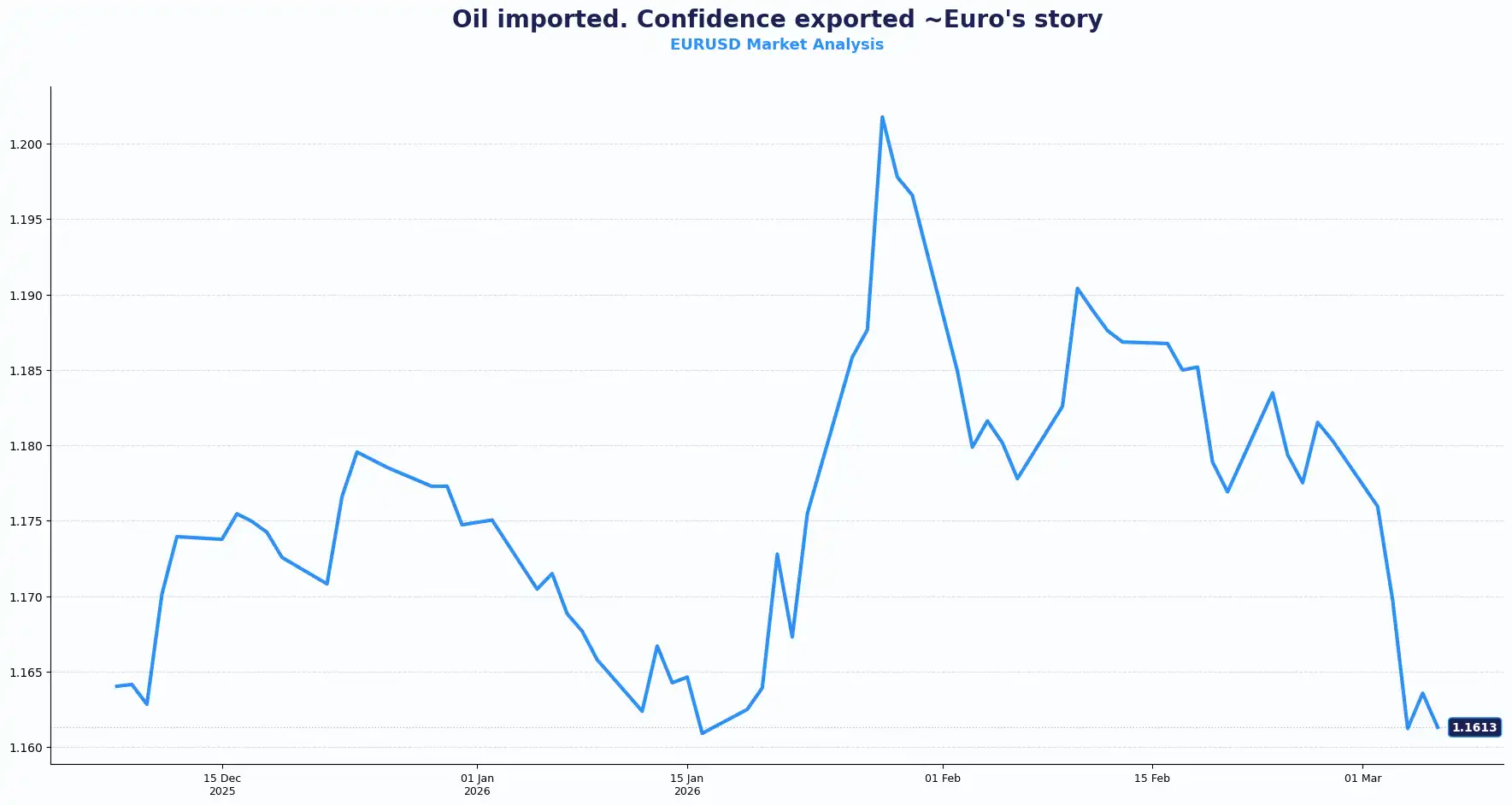

EUR/USD sat at 1.1606 on Friday, facing a 1.7% weekly drop. Europe's structural dependence on energy imports put the euro squarely in the firing line as oil surged past $85 a barrel on Friday.

Conversely, EUR/GBP held close to 0.8686, showing the euro holds ground against sterling even as it loses traction against the dollar.

Thursday’s Minutes from the European Central Bank’s (ECB) February meeting offered insight into the Governing Council’s thinking. The council noted upside growth surprise but kept its language deliberately non-committal on future policy direction. Yet, uncertainty around trade policy and geopolitics shaped the discussion. One view held that rates could stay at current levels for an extended period. Others flagged inflation risks tilted to the downside.

That internal split tells a clear story, the ECB has no unified path forward. Trade policy uncertainty and geopolitical tension sit at the centre of its concern. The council emphasised flexibility, with policymakers wanting full optionality in either direction, which, in practice, means the euro confronts a policy vacuum heading into a period of acute global risk.

Against that backdrop, some participants now price ECB rate hikes by year-end, not from any ECB signal, but from the inflationary impulse of surging oil prices. The gap between the council's cautious tone and hawkish market pricing creates live tension for the euro heading into next week.

That tension explains the euro’s behaviour this week. Rising energy prices usually lift inflation expectations. Yet they also raise recession risks across the euro area. FX traders struggle to price that balance.

Euro crosses are caught between a structurally non-committal central bank and a market pricing in higher rates amid energy-driven inflation fears. That divergence produced choppy, low-conviction price action, which is precisely what EUR/USD delivered this week.

The ECB sits in a holding pattern while energy prices and geopolitics reshape the outlook. That uncertainty tends to translate into wider swings in EUR pairs when global headlines shift.

Key technical levels for EUR/GBP: Resistance sits at 0.8745, 0.8780 and Support at 0.8680, 0.8625; Bias sits with a gradual upside while above 0.8680.

Key technical levels for EUR/USD: Resistance sits at 1.1680, 1.1750 and Support at 1.1550, 1.1480; Bias bearish while below 1.1680.

USD: Payrolls Day. War Day. Dollar's Day

The US Dollar Index (DXY) trades around 99.07 after a strong week. The dollar heads toward a 1.4% weekly gain, supported by safe-haven demand and rising Treasury yields.

Safe-haven demand and scaled-back rate cut expectations drove the dollar's strength. Investors now price roughly 40 basis points of Fed easing this year, down from 56 basis points a week ago. Brent Crude hit $85 a barrel, up from $69 just a week prior, a rise of more than 15% for the week, the largest single-week jump since February 2022. U.S. Crude touched a 20-month high earlier in the week.

The war escalated on Thursday. US and Israeli jets struck areas across Iran. Gulf cities came under renewed bombardment. President Donald Trump stated he wanted a say in deciding Iran's next leader, and publicly weighed in on succession naming Mojtaba Khamenei as an unlikely choice to succeed his father, the late Supreme Leader Ali Khamenei.

Thursday also brought US labour data. Initial jobless claims held steady week-on-week. Layoffs dropped sharply in February, consistent with stable labour market conditions.

With so much going on, one could almost forget that U.S. nonfarm payrolls are due later in the day. Expectations are for the world's largest economy to have added 59,000 jobs in February after accelerating by 130,000 in January, while the unemployment rate is forecast to have held steady at 4.3%. Any concrete sign of AI-driven labour market disruption is yet to surface in the data but the report faces close scrutiny for weak job growth or any upward creep in unemployment.

Fed Governor Michelle Bowman spoke this week, highlighting the central bank’s focus on financial stability. She noted signs of stabilisation in the labour market and pointed to energy prices as a factor the Fed watches closely during the Iran conflict. She also referenced work to rebalance supervisory frameworks for smaller banks.

Dollar strength is tied directly to elevated oil risk premia this week. Strategists note dollar upside may persist while crude risk premia stay elevated, a dynamic that echoed June 2025 price action. A regime shift in Iran with US backing could change that picture quickly. When the dollar rallies and US yields rise together, financial conditions tighten. Historically, that pattern amplifies moves in levered positions across asset classes.

Yen, Aussie, Kiwi: Navigating the Storm

USD/JPY held around 157.5 on Friday, putting the yen on course for a third consecutive weekly decline. The Australian dollar firmed against the greenback with AUD/USD at 0.7035. The New Zealand dollar rose, with NZD/USD at 0.5903.

Japan faced a compound problem this week. Soaring oil prices hit hard, given Japan's near-total dependence on Middle East energy imports. Bank of Japan Governor Kazuo Ueda warned the conflict could significantly affect Japan's economy and signalled a prolonged hold on interest rates. Finance Minister Satsuki Katayama confirmed that authorities are monitoring the yen's decline with urgency, coordinating with the US on any potential support measures, and treating currency intervention as an option on the table.

The Antipodean currencies caught a different wind entirely on Friday. Both the Aussie and Kiwi firmed against the dollar, bucking the broad trend of the week.

Asia-Pacific equities outside Japan fell more than 6% this week, their steepest drop since March 2020. Technology stocks and indices including the Kospi led the selloff as investors booked profits to cover losses elsewhere. Safe-haven flows appeared across other assets. Gold held steady. Bitcoin fell. Ether extended its decline.

The range of plausible outcomes for this conflict has widened. Both an exceptionally constructive resolution and a deeply destructive one sit within the distribution. Pricing those tails with limited reliable information about probabilities or the path between them is the central challenge for participants right now.

Energy costs, regional growth risks and intervention rhetoric now shape the outlook for Asia-Pacific currencies. Those forces often interact with shifts in global risk sentiment.

Current Rate Table

| Pair | Spot | Short-term Trend Bias |

|---|---|---|

| GBP/USD | 1.3354 | Downtrend this week |

| EUR/USD | 1.1606 | Downtrend |

| EUR/GBP | 0.8686 | Mild upward bias |

| USD/JPY | 157.5 | Uptrend |

| GBP/JPY | 209.41 | Uptrend |

| AUD/USD | 0.7068 | Range trading |

| NZD/USD | 0.5917 | Weak bias |

(rates as at the time of writing)

Market Look ahead

Friday, 6 March

Eurozone Q4 GDP (final)

ECB President Christine Lagarde speech

US Nonfarm Payrolls and Unemployment Rate

US Avg Hourly Earnings + Retail Sales

US Fed Monetary Policy Report

SNB Feb Foreign Currency Reserves

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.