Midnight Ultimatum: Dollar Grips, Cable Slips

7 min read

Share

Trump's midnight GMT deadline on Iran lights up the dollar. Energy risks tighten the screws on volatility. Sterling slips near $1.3220, the euro holds steady on ECB hawkishness. Oil above $111 keeps stagflation live.

GBP: Sterling Buckles Under Geopolitical Weight

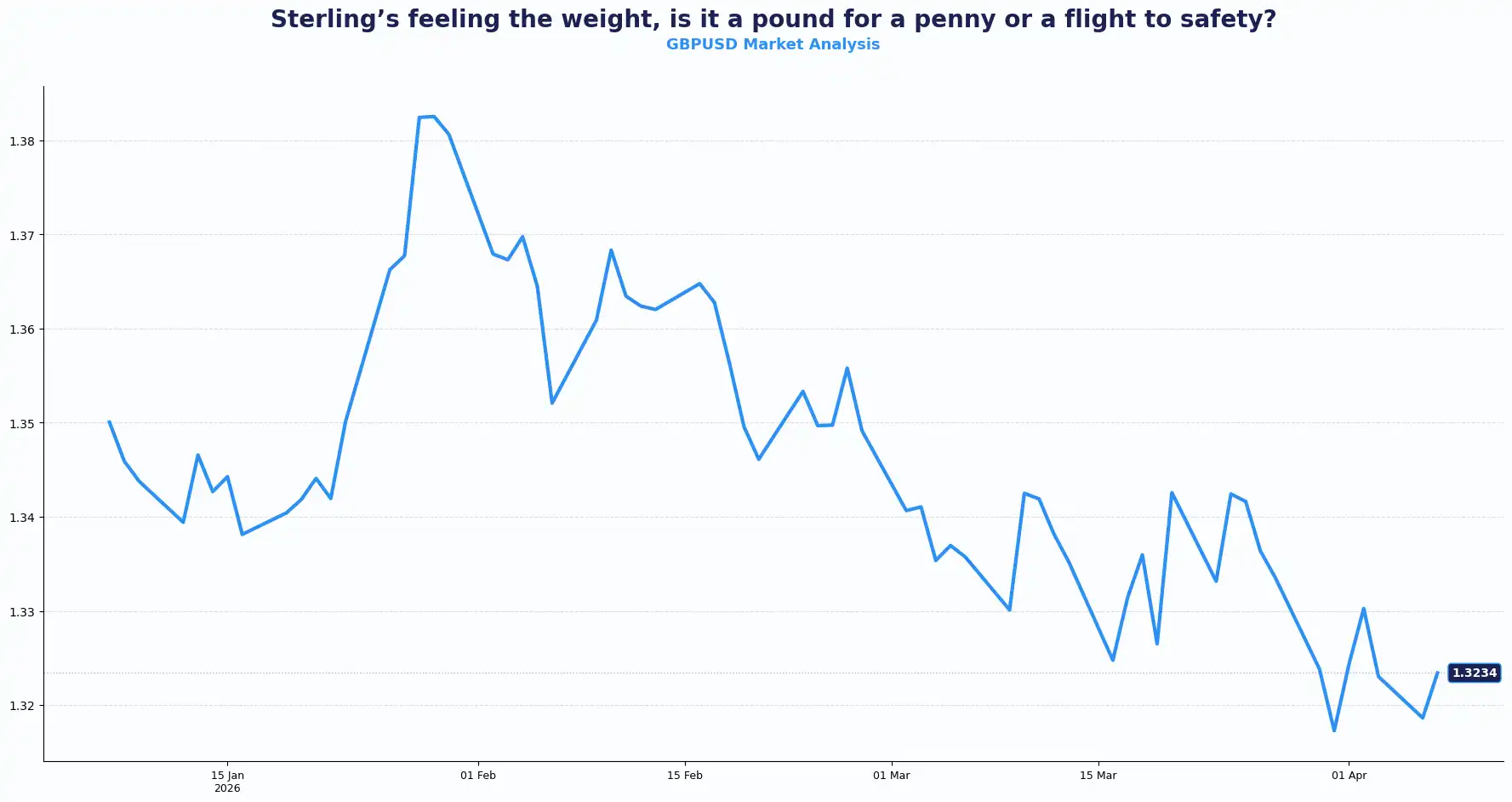

Cable: 1.3220 | EURGBP: 0.8720

Cable trades near 1.3220 this Tuesday morning as a wave of risk aversion sweeps through the Asian session. Investors shed sterling positions in favour of the dollar ahead of Trump's 8 p.m. Eastern Time (midnight GMT) Iran deadline.

Sterling hit $1.3227 earlier, just above late March lows, before slipping back. While cable tried to recover this week, the current atmosphere stalled momentum. Now, GBP/USD pares gains as markets digest the rejected ceasefire proposal. Risk aversion acts as the primary driver, directly linked to the uncertainty surrounding the Middle East truce.

The Bank of England (BoE) has executed a sharp U-turn. Previously, policymakers like Sarah Breeden and Swati Dhingra favoured rate cuts, but now advocate a "wait-and-see" approach. The Middle East conflict has sent energy costs soaring, prompting the BoE to warn that CPI inflation could reach 3.5% in the coming months. Higher energy prices act as a tax on UK consumers and complicate the growth outlook, even with rates at 3.75%. The BoE has shifted from a cutting bias to a defensive hold, prioritising price stability over growth support.

With a central bank on hold, energy costs climbing, and risk appetite soured, GBP has no clear catalyst for a sustained push higher. UK S&P Global Composite PMI figures for March are due today. Consensus sits at 51.0 for the composite and 51.2 for services, both in line with February. Readings above 50 imply sector expansion. However, risk-off positioning ahead of tonight's deadline could offset any positive impact from the data.

Investors are navigating timing risks rather than long-term directional conviction. With positioning light and reactive, the current environment often sees sharp, sudden moves.

Key Technical levels for the GBP/USD pair: Resistance sits at 1.3300, 1.3350 and Support sits at 1.3200, 1.3150

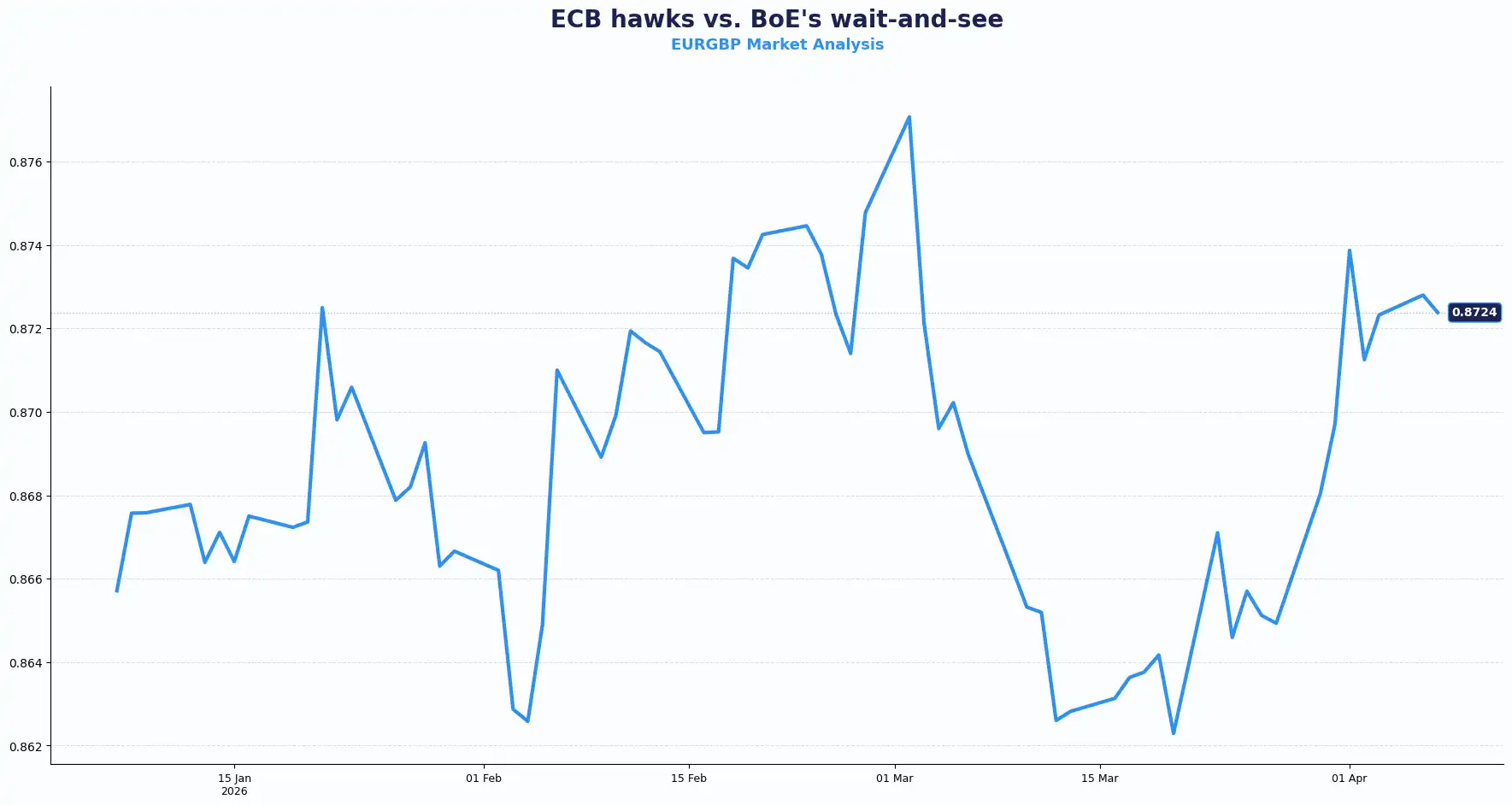

EUR/GBP holds above 0.8700, trading near 0.8720. The euro's relative strength against sterling reflects a divergence in rate trajectory: the European Central Bank (ECB) leans toward hikes while the BoE holds.

Key Technical levels for the EUR/GBP pair: Resistance sits at 0.8780 and Support sits at 0.8700

EUR: ECB Hawkishness Gives the Euro a Floor

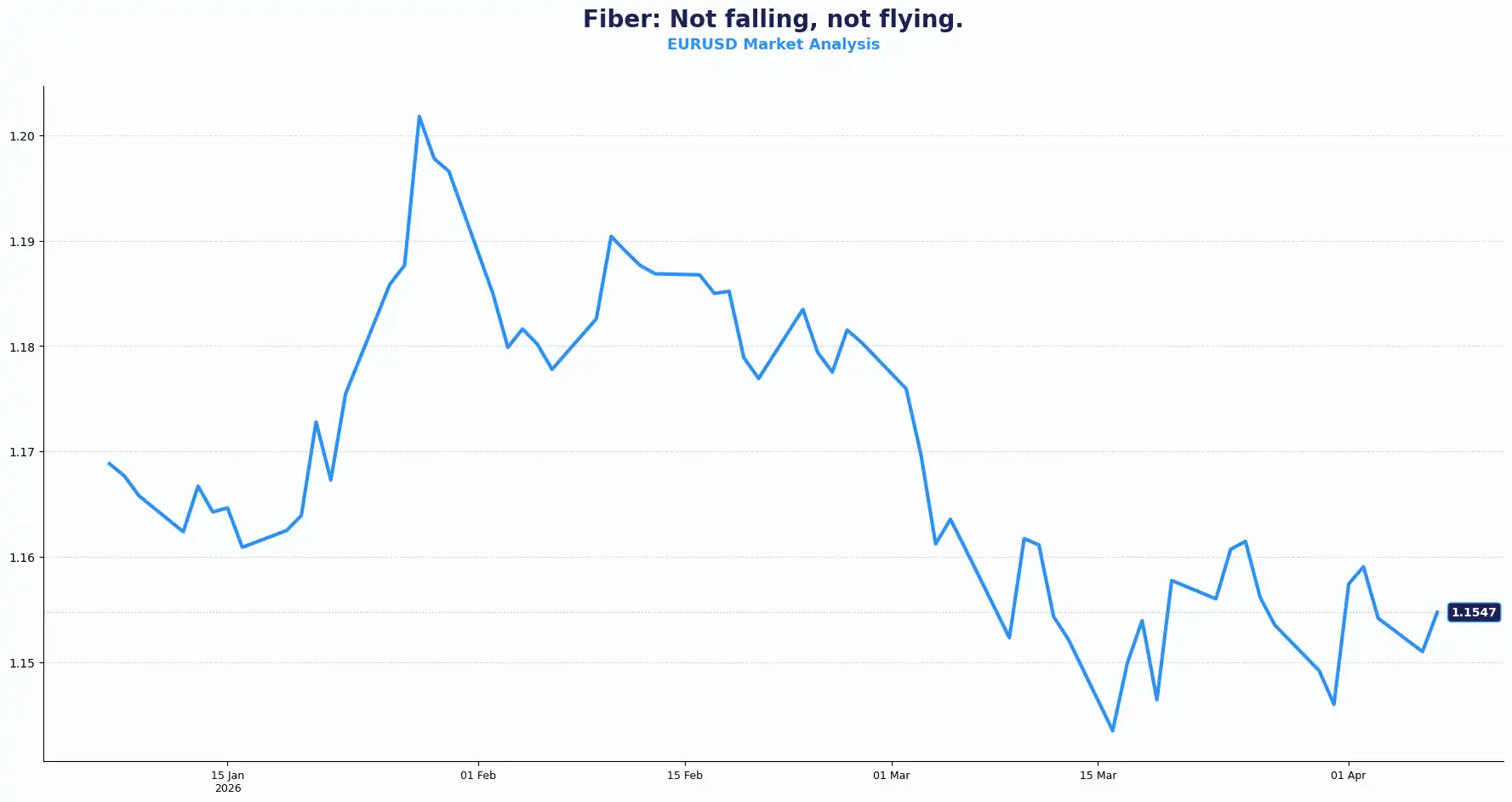

EURUSD: 1.1530

The euro holds steady at 1.1530, but the calm is rather deceptive. European futures point to a slightly higher open after the holiday break, yet the underlying mood is one of suspense. Traders are largely parked on the sidelines, watching the countdown while the unrelenting demand for the dollar makes any attempt at a euro rally feel like an uphill battle. Eurozone’s Manufacturing data later today will reveal the real-world impact of the six-week-long war on the European economy and whether pricing pressures are truly warranted.

Despite the geopolitical gloom, the European Central Bank (ECB) maintains a surprisingly stern posture. President Christine Lagarde insists policy must stay restrictive until inflation hits the 2% target. More notably, Francois Villeroy de Galhau suggests the next move will likely be a rate hike, though timing is unclear. The market has now priced in multiple 2026 hikes, a sharp reversal from the prior consensus of a hold. The euro finds a floor here only because the ECB refuses to blink in the face of energy-driven inflation, even as growth forecasts soften across the bloc.

Against sterling, the euro's position tracks this repricing. The BoE is on hold too, but without the ECB's upward rate trajectory. EUR/GBP has reflected this divergence in recent price action, holding firm above 0.8700.

The data calendar sharpens the picture this week. Today brings HCOB Composite and Services PMI readings for Germany, France, and the eurozone. Consensus puts the eurozone Services PMI at 50.1 and Composite at 50.5, both in line with prior prints. Eurozone Retail Sales and German inflation data follow later in the week, clarifying if the ECB can actually follow through on its hawkish outlook.

Wednesday brings the ECB non-policy meeting and FOMC minutes. Further hawkish ECB commentary could draw attention to the EUR/GBP and EUR/USD pairs, as traders weigh whether the rate gap against sterling widens further. The divergence between a hawkish ECB and a "safe-haven" dollar creates a tug-of-war.

Key Technical levels for the EUR/USD pair: Resistance sits at 1.1600, 1.1650 and Support sits at 1.1500, 1.1450

USD: The Dollar Dominates the Doomsday Circuit

The dollar index (DXY) hovers near recent highs at 100.04. President Trump’s warning that Iran could be "taken out in one night" has sent a shiver through the global markets. Investors currently view the greenback as the only viable shelter as the threat to destroy Iranian power plants, and bridges becomes a tangible market risk.

Iran rejected the temporary ceasefire proposal, pushing instead for a permanent end to the war. That stance removed the residual optimism that had held off further dollar buying over Easter.

The US services sector shows signs of strain. Monday's ISM Services PMI for March came in at 54.0, down from 56.1 in February and below the 55.0 consensus. The sector holds in expansion: nine of ten sub-indices printed above 50. While growth continues, businesses have paid input prices at the fastest rate in 13 years. This suggests the war is directly boosting inflationary pressure. Consequently, traders have erased expectations for Federal Reserve (Fed) rate cuts this year. The "higher for longer" narrative has evolved into "higher because of war." Long-term inflation expectations are holding for now, with Friday's US CPI print as the next major test.

Trump's Monday press conference sharpened the stakes of the deadline. He confirmed that every power plant and bridge faces destruction if no deal is reached by tonight and warned that Iran could face "complete demolition". Any follow-through on these threats would mark a significant escalation, raising the risk of retaliatory action against Gulf energy facilities. The greenback’s dominance reflects a total absence of risk appetite amid total war.

US Treasury yields signal a stagflationary hedge, anchoring the dollar’s liquidity. The 8:00 PM ET deadline is key for the next 24 hours. As the Strait of Hormuz handles 20% of global oil, ongoing uncertainty bolsters safe-haven flows. Geopolitical stress typically drives stronger dollar demand and tighter global liquidity.

Risk-Off Sweeps the Commodity Bloc and Asia

AUDUSD: 0.6916 | NZDUSD: 0.5702 | USDJPY: 159.77 | GBPJPY: 211.39

The Japanese yen sits at 159.77, flirting with the 160.00 "line in the sand." Tokyo officials have increased their verbal warnings, leaving markets on high alert for direct intervention. Meanwhile, the Australian and New Zealand dollars trade softly as the destruction of Middle East energy infrastructure weighs on commodity-linked currencies.

Traditional market correlations are snapping. Usually, there is a trade-off between growth and inflation; now, both the won and the Indonesian rupiah are hitting record lows despite local policy. The dollar's strength is a blunt instrument, crushing emerging market currencies as the cost of energy imports becomes unsustainable for these economies. The US leaving the conflict does not automatically reopen the Strait; as long as the waterway remains a choke point, the fundamental pressure on global currencies persists. Structural risks are now outweighing local economic data across Asia and the Pacific.

Gold eased to $4,640 per ounce in early trade. GBP/JPY prints at 211.39.

Brent Crude trades at $111.43 per barrel, up around 53% since the conflict began. Oil is the critical transmission channel: it anchors inflation expectations and sets the tone for whether risk assets find footing or extend their losses into tonight's deadline.

Current Rate Table:

| Pair | Level | Trend |

|---|---|---|

| GBP/USD | 1.3220 | Bearish bias below 1.3300 |

| EUR/USD | 1.1530 | Neutral, Supported above 1.1450 |

| EUR/GBP | 0.8720 | Bullish above 0.8700 |

| USD/JPY | 159.77 | Bullish, intervention risk near 160 |

| GBP/JPY | 211.39 | Bullish, momentum-led above 210 |

| AUD/USD | 0.6916 | Soft, capped below 0.7000 |

| NZD/USD | 0.5702 | Weak below 0.5800 |

| DXY | 100.04 | Strong |

(as at the time of writing)

Market Lookahead

Tue, 7 April

- UK, Eurozone, France, Germany PMI (March)

- US - Durable goods orders (Feb), Consumer credit, API crude stocks, ADP employment

- Trump Iran deadline: 8 p.m. ET / Midnight GMT

Wed, 8 April

- Eurozone PPI (Feb), retail sales (Feb)

- NZ rate decision

- FOMC minutes

Fri, 10 April

- US CPI

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.