Fire in the Gulf. Frost on the Pound

8 min read

Share

Energy shocks and Middle East tensions push inflation fears back into focus. Sterling wobbles on stagflation risks, the euro gains policy support from stronger data, while the dollar regains ground amid resilient US labour signals.

GBP: Stagflation Knocks at the Door

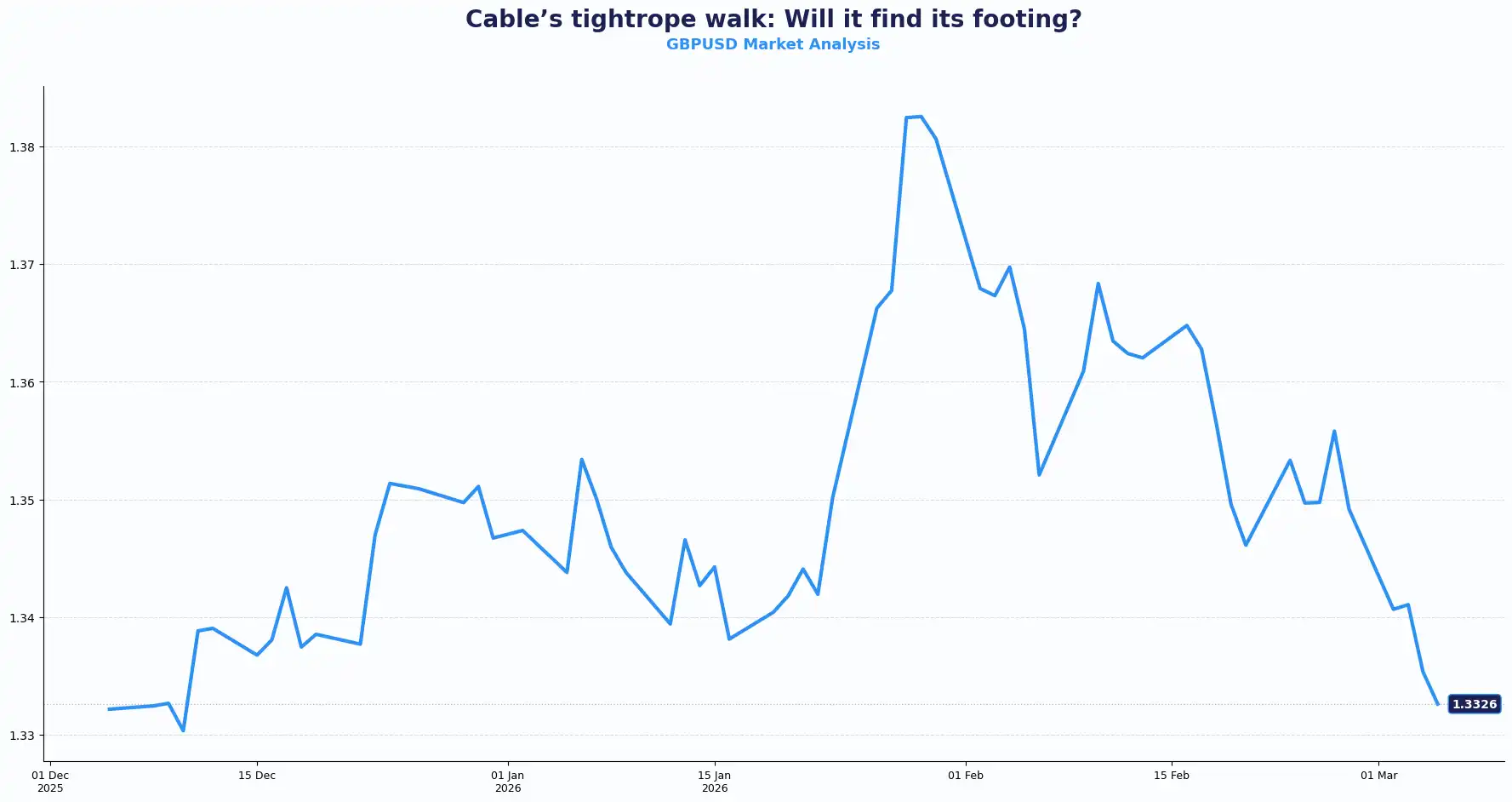

GBP/USD hit a three-month low of 1.3253 on Tuesday. By Wednesday, it clawed back to near 1.3400. The pair now trades near 1.3334. The recovery ran out of conviction the moment Tehran denied CIA negotiation talks and threatened a prolonged conflict. The dollar resumed its advance, and the sterling absorbed the blow. The EUR/GBP pair holds near 0.8706.

The UK’s heavy reliance on imported energy means price spikes flow directly into the veins of the economy. As a result, a "stagflation" trap emerges: prices climb while growth and jobs stay stuck. Inflation already sits above the Bank of England's (BoE) 2% target, with January's headline CPI printed at 3% YoY. Even with Services PMI holding at 53.9, the structural drag from high input costs limits the BoE's room to breathe. Meanwhile, the Office for Budget Responsibility just slashed the 2026 growth forecast to 1.1% from 1.4%, while projecting a recovery to 1.6% in both 2027 and 2028.

This energy shock, which now connects all three major central banks, is having immediate policy implications. For the Federal Reserve (Fed) and the BoE, fewer rate cuts are now priced as energy costs threaten to push inflation higher. For the European Central Bank (ECB), the conversation has moved further still. In this context, the BoE faces a difficult call, and the pound sits at the intersection of a hawkish repricing it did not invite and a growth story that is losing its footing.

Key technical levels for GBP/USD: Resistance sits at 1.3400, 1.3470 and Support at 1.3250, 1.3180. The technical bias for GBP/USD remains soft, signalling a likelihood for further downside as long as the pair stays below 1.3400.

Key technical levels for EUR/GBP: Resistance sits at 0.8745, 0.8780 and Support at 0.8680, 0.8625; Bias sits with a gradual upside while above 0.8680

This growth versus inflation divergence has influenced positioning across sterling crosses, as participants reassess the rate trajectory. Periods of stagflation risk have historically been associated with increased volatility in GBP pairs and shifts in hedging behaviour.

EUR: The Ecb Hike No One Saw Coming

The euro held firm despite geopolitical volatility. The EUR/USD pair trades near 1.1607.

Eurozone business activity surprised on the upside. The Eurozone's February composite PMI rose to 51.9 from 51.3 in January, a three-month high and the 14th consecutive month of private sector expansion. Services PMI climbed to 51.9, with domestic demand driving growth as export orders contracted marginally. Growth data across the region was mixed. Germany led the expansion, Italy accelerated, Spain slowed, and France stayed in contraction territory.

The stronger PMI readings shifted the policy debate in Europe. The ECB's rate outlook flipped from a marginal chance of a cut this year to a roughly 50% probability of a hike in two trading sessions. Euro money markets now price approx. 40% odds of an ECB rate hike before year-end. Every EMEA central bank faces the same transmission question: “How far does the energy shock travel through domestic prices, and how wide can the policy gap with the ECB grow?”

Energy prices explain part of the shift, with surging oil costs feeding directly into Eurozone inflation. At the same time, domestic demand in the services sector shows resilience despite weak export activity. Upcoming data could sharpen the picture.

ECB President Christine Lagarde addresses the public today and tomorrow. Her framing of energy risk relative to the inflation trajectory will set the next directional move across EUR pairs. Higher rates support the euro over the medium term, while near-term growth concerns and dollar strength could exert countervailing pressure. The direction depends on which force the ECB chooses to address first.

Tomorrow brings Eurozone Q4 GDP, forecast at 0.3% QoQ and 1.3% YoY against a prior 1.4%. Q4 employment change data follows. A downside GDP miss would deepen the growth-versus-inflation conflict the ECB now navigates. The Swiss National Bank will also release the February foreign currency reserves tomorrow; January's figure was CHF 712 billion. Changes in these reserves often reflect efforts to influence the franc’s exchange rate against the euro. Participants will watch for evidence of active SNB intervention during the energy-driven volatility.

The euro now sits at the intersection of stronger domestic activity and rising inflation risks. Currency pricing has historically shifted quickly when growth data alters expectations for central bank policy.

Key technical levels for EUR/USD: Resistance sits at 1.1650, 1.1720 and Support at 1.1550, 1.1480; Bias sits bullish above 1.1540.

USD: The Dollar’s Dominance in a War Economy

The dollar resumed its advance after a brief pause. The Dollar Index (DXY) trades near 99.00, holding over 1% up for the week and emerging as one of a handful of winners in a session that dragged equities, bonds, and at times even gold lower.

Safe-haven demands strengthened as the US-Iran conflict intensified. Washington’s political support for the military campaign signalled a longer conflict horizon, which helped sustain demand for the dollar.

Oil prices climbed further. US Crude sits at $77.60 per barrel and Brent Crude at $84.25 - both up roughly 16%, since the war began. Energy Secretary Chris Wright called the conflict's economic impact a "bump on the road." IMF Managing Director Kristalina Georgieva described the world as entering a potentially prolonged period of flux. The US Senate backed the military campaign against Iran; however, the resolution does not seem close.

US employment signals added support. The ADP private payroll report showed 63,000 jobs added in February, above the 50,000 forecast and sharply higher than the previous 11,000 reading. Stronger employment has pushed traders to reduce dovish Fed bets. The Fed faces no compelling pressure to cut rates in this environment.

Fed’s regional reports paint a mixed economic picture. The Fed’s Beige Book described activity as flat in several districts, modestly weaker in others, and moderately stronger in a handful. Price pressures continue to build. Eight districts reported moderate price growth, while firms across several sectors passed tariff-related cost increases to customers.

Consumer behaviour also shows caution. Several districts reported slower sales as households responded to economic uncertainty and rising prices. Despite those headwinds, the labour picture signals stability. Job levels held steady across most districts, and manufacturing orders improved in several regions.

Upcoming data today will test the strength of that narrative. US initial jobless claims are forecast at 215,000 against the prior 212,000. Investors will also monitor the four-week average of 220,250, which might offer a clearer signal of labour trends. Import and export price index data also arrive today. Tomorrow brings non-farm payrolls for February, January retail sales, and average hourly earnings. That trio will determine the dollar's direction further into next week.

Sustained dollar strength has historically been associated with shifts in positioning across emerging markets and risk-correlated currencies. Participants have been observed reassessing dollar exposure in light of the employment data and geopolitical developments.

Global Pulse: Aussie Proxies and Asian Rebound

AUD/USD sat at 0.7068, holding its prior-session 0.57% gain. In Asia, the KOSPI surged 11.2%, following a Wall Street rebound, while China set a 4.5%-5% growth target for 2026. The New Zealand dollar eased to $0.5917.

The Aussie dollar is acting as a proxy for risk; it benefits from energy abundance but suffers when global sentiment sours. In China, the yuan’s 34-month midpoint high shows a clear attempt by Beijing to stabilise the currency amidst growth woes. However, with Iran launching missiles at Israel, these gains stay fragile.

Generally considered a safe-haven, the yen softened against the dollar with USD/JPY trading at 157.07 and GBP/JPY near 209.41. Gold advanced, while Bitcoin and Ethereum fell against the dollar.

Geopolitical risk can reignite quickly. Oil flows have yet to normalise. If the conflict extends, more production facilities may go offline. Risk-linked currencies often react quickly to geopolitical headlines and shifts in commodity prices. Participants across global FX markets closely watch these moves as indicators of broader sentiment.

Current Rate Table

| Pair | Spot | Short-term Trend Bias |

|---|---|---|

| GBP/USD | 1.3334 | Downtrend below 1.3400 |

| EUR/USD | 1.1607 | Uptrend above 1.1500 |

| EUR/GBP | 0.8706 | Range, Gradual upside bias |

| USD/JPY | 157.07 | Uptrend |

| GBP/JPY | 209.41 | Uptrend |

| AUD/USD | 0.7068 | Range trading |

| NZD/USD | 0.5917 | Weak bias |

(rates as at the time of writing)

Market Look ahead

Thursday, 5 March

US Initial Jobless Claims

ECB's Lagarde Speech

ECB Monetary Policy Meeting Accounts

Friday, 6 March

Eurozone Q4 GDP (final)

ECB President Christine Lagarde speech

US Nonfarm Payrolls and Unemployment Rate

US Avg Hourly Earnings + Retail Sales

US Fed Monetary Policy Report

SNB Feb Foreign Currency Reserves

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.