EUR/GBP Gains on Hopes for EU-US Trade Breakthrough

10 min read

Share

EUR/GBP climbed to near 0.8559, as Germany's May Retail Sales data exhibited an unexpected decline, adding to the evidence of soft economic momentum and fluctuating the shared currency. The German retail sales figures for May declined 1.6% against the market expectations of a 0.5% rise, pressuring the euro. On Monday, the Federal Statistical Office of Germany announced that German import prices fell by 1.1% year-on-year in May, exceeding the market expectation of 0.8%. Germany's initial consumer price figures for June are expected to show a slightly higher increase, with a 0.2% monthly rise and a 2.2% annual rate, up from 0.1% and 2.1%, respectively, in the previous month. Markets are closely watching negotiations in Brussels, especially as German Chancellor Olaf Scholz and European Commission President Ursula von der Leyen seek a breakthrough. On Thursday, French President Emmanuel Macron expressed support for a quick and fair EU-US trade deal. He also warned that if the US maintains a 10% tariff, Europe will retaliate with an identical levy on US companies. Macron emphasised his backing for a rapid and equitable trade agreement but warned that persistent US tariffs could soon pressure the shared currency.

On the other hand, the Bank of England's (BoE) cautious stance on rate cuts amid persistent inflationary pressures supports the pound. On the data front, the core current account deficit, excluding trade in precious metals, shrank slightly to £18.6 billion, or 2.5% of gross domestic product (GDP), in the first quarter of 2025 (January to March). This is a £0.1 billion improvement from the previous quarter's deficit of £18.7 billion. However, including trade in precious metals, the UK's current account deficit increased by £2.4 billion to £23.5 billion, which is 3.2% of GDP in Q1 2025. The total trade deficit, excluding precious metals, decreased to £7.5 billion (1.0% of GDP), down from £10.2 billion in the previous quarter. This decline was mainly due to a reduction in the goods trade deficit to £55.3 billion, while the services trade surplus also shrank to £47.8 billion. Meanwhile, the UK economy resumed growth in the first quarter of 2025. Final GDP figures released on Monday by the Office for National Statistics confirmed a 0.7% quarter-on-quarter increase and a 1.3% rise year-on-year. Despite this, uncertainties remain as both domestic and global factors continue to influence the economic outlook. Meanwhile, political tensions have risen in the UK as Prime Minister Keir Starmer reduced welfare reform proposals to prevent rebellion among Labour Party lawmakers. Over 100 Labour MPs publicly opposed the plan, which sought to save £5 billion annually from the rapidly increasing welfare budget.

Apart from the EU-US trade deal, the final Manufacturing PMI from both regions and the European Unemployment Rate will influence the EUR/GBP exchange rate.

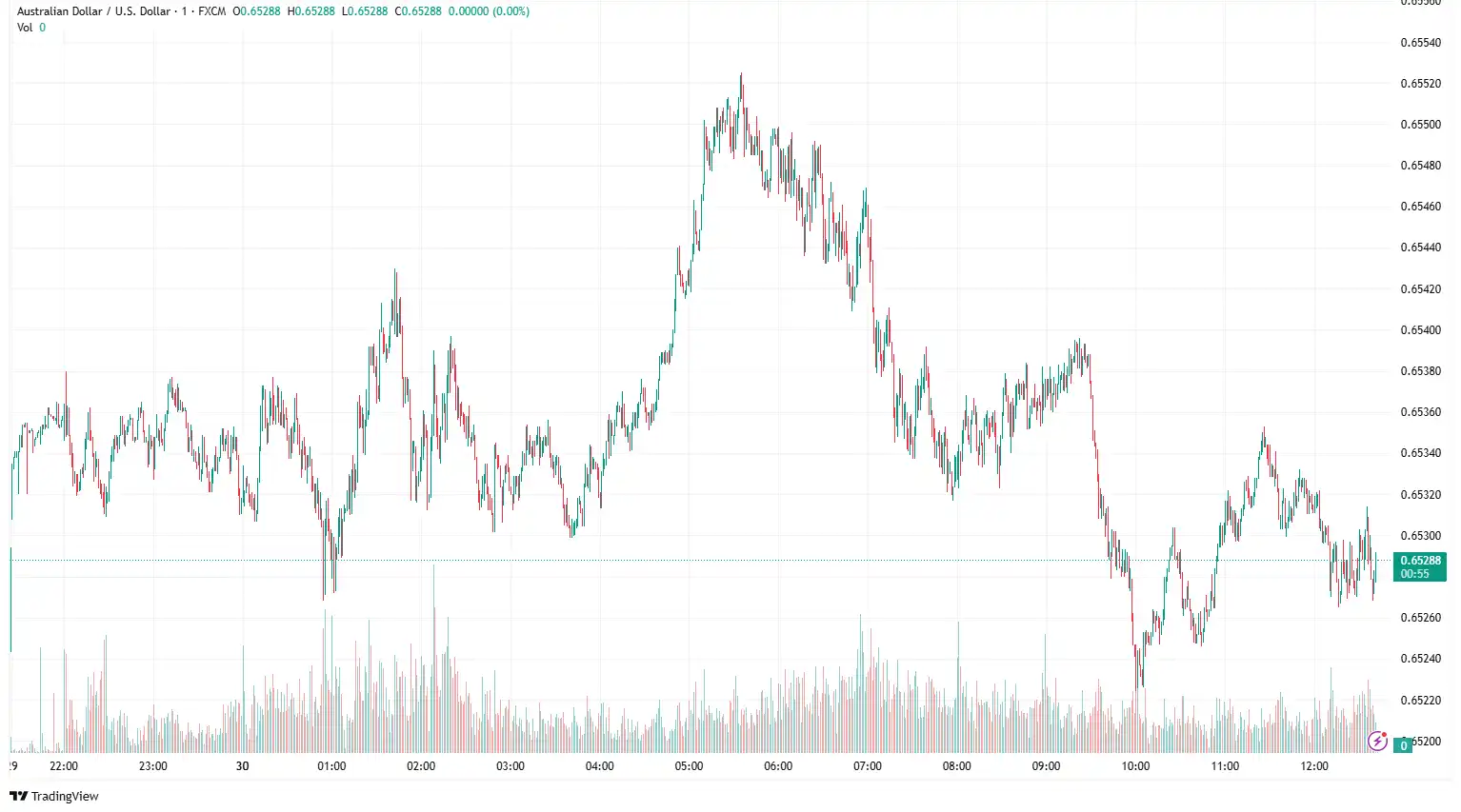

AUD/USD Sinks Following the MI Inflation Gauge

AUD/USD edged lower near 0.6536 following the release of Australian and Chinese economic data. The TD-MI Inflation Gauge increased by 0.1% month-on-month in June, reversing a 0.4% decline previously recorded. This rise occurred even though both headline and core inflation continued to decline within the Reserve Bank of Australia's (RBA) 2–3% target range. Australia's Private Sector Credit grew by 0.5% month-on-month in May, defying market expectations and following a 0.7% increase in the prior month. The slowdown was mainly driven by a deceleration in business loans, which eased to 0.8% from 1% in April. In Australia's close trading partner, China, the NBS Manufacturing Purchasing Managers' Index (PMI) rose to 49.7 in June, up from 49.5 in May. The data aligned with the market consensus for the reported month. The NBS Non-Manufacturing PMI increased to 50.5 in June from 50.3 in May, matching the expected 50.3 reading. Moreover, market anticipation that the RBA will continue cutting interest rates in the coming months continues to weigh on the Aussie.

On the other hand, rising odds of the Federal Reserve (Fed) cutting interest rates at the September meeting strengthened the US dollar. Data released on Friday indicated that the Personal Consumption Expenditures (PCE) Price Index increased to 2.3% in May from 2.2% in April (revised from 2.1%), according to the US Bureau of Economic Analysis. This figure aligned with market expectations. The core PCE Price Index, which excludes volatile food and energy prices, rose by 2.7% in the same period, up from 2.6% (revised from 2.5%) in April. Both the PCE Price Index and the core PCE Price Index grew by 0.1% and 0.2%, respectively, on a monthly basis. The report also revealed that Personal Income decreased by 0.4% month-on-month, while Personal Spending fell by 0.1%. Investors are awaiting crucial US labour data expected later this week to better understand the Federal Reserve's policy stance. The Nonfarm Payrolls (NFP) are forecasted to show an increase of 110,000 jobs, down from 135,000 in May, with estimates ranging from a high of 140,000 to a low of 75,000. Additionally, the unemployment rate is expected to rise slightly to 4.3% from 4.2%.

On the global stage, recently, US Treasury Secretary Scott Bessent confirmed that the US and China reached an agreement on rare earth imports, which concludes the pact signed a few weeks ago and normalises the relationship between the world's two major economies. Chicago Fed President Austan Goolsbee said that political dynamics and the appointment of a so-called shadow chair do not influence policy decisions. Goolsbee added, "That would not affect the FOMC itself." "Just look at the minutes and transcripts. You can see, word for word, what the rationale is in making the decisions, and they're not about elections, and they're not about partisan politics."

In the upcoming sessions, US labour market figures, ISM Manufacturing PMI, and Trade Balance, along with Australian retail sales data and Goods Trade Balance, will influence the AUD/USD exchange rate.

USD/CAD Rebounds Amid Renewed Hopes of US-Canada Trade Talks

USD/CAD recovered near 1.3677 due to positive risk sentiment following the announcement of the resumed US-Canada trade talks. On Sunday, Canada's Prime Minister, Mark Carney, confirmed that trade negotiations with the US would resume this week after the country withdrew the digital services tax that had caused the negotiations to end last week. On Friday, US President Donald Trump announced the suspension of trade discussions with Canada, criticising the digital tax, which he described as a "direct and blatant attack on our Country (sic)." President Trump appears frustrated that Canada is moving ahead with closing a predatory taxation loophole that allows US tech firms to sell their products in Canadian markets tax-free. The new fee for cross-border tech services has been in development for years, but the Trump administration has only now decided to pull out. Canada's monthly GDP decreased by 0.1%, defying expectations of no change, mainly due to weak manufacturing activity and trade tensions. April's GDP growth also slowed, and softer inflation data has renewed investor hopes of forthcoming rate cuts by the Bank of Canada (BoC). Rising crude oil prices continue to support the commodity-linked Canadian dollar. However, the potential upside of crude oil prices could be limited amid easing fears over supply disruptions driven by the Middle East ceasefire.

Conversely, dovish comments from Neel Kashkari, President of the Federal Reserve Bank of Minneapolis, amid rising expectations of the Federal Reserve (Fed) cutting interest rates at the September meeting, continue to cause fluctuations in the US dollar. Kashkari reaffirmed his view that cooling inflation would enable the Fed to cut its policy rate twice this year, starting in September. Recent US Personal Spending unexpectedly fell in May, marking the second decline this year. Meanwhile, US Personal Income dropped by 0.4% in May, the largest decrease since September 2021. The Personal Consumption Expenditures (PCE) Price Index rose to 2.3% in May from 2.2% in April (revised from 2.1%), the US Bureau of Economic Analysis reported on Friday. This reading aligned with market expectations. The core PCE Price Index, which excludes volatile food and energy prices, increased by 2.7% in the same period, up from the 2.6% (revised from 2.5%) recorded in April. The PCE Price Index and the core PCE Price Index increased by 0.1% and 0.2%, respectively, monthly. Other details of the report showed that Personal Income declined by 0.4% month-on-month, while Personal Spending fell by 0.1%. The US Nonfarm Payrolls report is expected to indicate that the economy added 110,000 new jobs in June, down from 135,000 in May. The current estimate ranges from a high of 140,000 to a low of 75,000. Additionally, unemployment is anticipated to rise slightly to 4.3% from 4.2%.

In today's session, broader market sentiment around the Chicago PMI, FOMC Member Bostic, and FOMC Member Goolsbee will influence the USD/CAD exchange rate.

EUR/JPY Tumbles on Downbeat German Data

EUR/JPY trades at 169.04, following a cautious stance from the Bank of Japan (BoJ) regarding interest rate hikes, which weigh on the yen. The headline Tokyo Consumer Price Index (CPI) for June increased by 3.1% year-on-year, compared to 3.4% in the previous month, the Statistics Bureau of Japan announced on Friday. Furthermore, Tokyo's CPI, excluding fresh food, rose by 3.1% year-on-year in June, against the 3.3% forecast, and declined from 3.6% in the previous month. The Tokyo CPI, excluding fresh food and energy, also increased by 3.1% year-on-year in June, down from 3.3%. Retail sales in Japan fell by 0.2% month-on-month in May, following a revised growth of 0.7% in the previous month. On an annual basis, retail sales increased by 2.2% in the reported month, below the revised 3.5% growth in April and falling short of market forecasts of 2.7%. These figures reinforce expectations that the Bank of Japan may refrain from raising interest rates in 2025. Japan's core inflation has remained well above the BoJ's 2% target for over three years and reached its highest level in more than two years in May.

Additionally, Japan's Corporate Services Producer Price Index, an early indicator of consumer inflation, has stayed above 3% year-on-year for several months. Japan's industrial production increased by 0.5% month-on-month in May, recovering from a 1.1% decline in April. However, the figures missed market forecasts of 3.5% growth as elevated US tariffs continued to cast a shadow over the outlook. On Monday, Japan's top trade negotiator, Ryosei Akazawa, noted that he will continue working with the United States to reach an agreement while defending national interests. Akazawa mentioned that he is aware of President Trump's comment about declining to discuss the auto. "It was unfortunate I couldn't meet Bessent this time."

On the euro's front, renewed optimism about the EU-US trade deal, alongside disappointing German retail sales data, influences the euro. German retail sales figures, which fell 1.6% in May compared to market expectations of a 0.5% increase, have weighed on the euro (EUR) rally. The shared currency, however, maintains its broader positive outlook following an almost 2% rally last week. Italy's Consumer Prices Index (CPI) accelerated by 0.2% in June, up from the 0.1% contraction seen the previous month, yet remains below the 0.3% forecast by market analysts. Yearly inflation held steady at 1.7%, against expectations of a slight rise to 1.8%. Later today, Germany's preliminary consumer price data for June are expected to show a marginal increase, with a 0.2% monthly rise and a 2.2% year-on-year rate, up from 0.1% and 2.1%, respectively, in the previous month. European Central Bank (ECB) Vice President Luis de Guindos stated on Monday that the current interest rate stance is appropriate but emphasised the need to keep all options open due to prevailing uncertainty. He also added, "I hope there is a US-EU trade agreement by July 9."

Upcoming preliminary Eurozone Harmonised Index of Consumer Prices (HICP) data for June and the BoJ's upcoming quarterly Tankan survey for the second quarter (Q2) will provide fresh impetus on the EUR/JPY exchange rate.

Stay Ahead in the Currency Game

Whether you're a daily FX trader or handle international transactions regularly, our 'Currency Pulse' newsletter delivers the news you need to make more informed decisions. Receive concise updates and in-depth insights directly in your LinkedIn feed.

Subscribe to 'Currency Pulse' now and never miss a beat in the currency markets!

Ready to act on today’s insights? Get a free quote or give us a call on: +44 (0)20 7740 0000 to connect with a dedicated portfolio manager for tailored support.

Important Disclaimer: This blog is for informational purposes only and should not be considered financial advice. Currency Solutions does not take into account the investment objectives, financial situation, or specific needs of any individual readers. We do not endorse or recommend any specific financial strategies, products, or services mentioned in this content. All information is provided “as is” without any representations or warranties, express or implied, regarding its accuracy, completeness, or timeliness.